In a previous article, I explored the accuracy of a statement Jeremy Seigel recently made during a presentation at the Investments & Wealth ACE Academy conference in San Diego. He suggested that “while stocks were not a great inflation hedge in the short run, in the long run they were perfect” (he emphasized perfect versus good or great). Using a dataset that includes 16 countries spanning 1870-2020, I found that while stocks may not have technically been the perfect inflation hedge, they were better than cash or bonds over extended periods.

In a previous article, I explored the accuracy of a statement Jeremy Seigel recently made during a presentation at the Investments & Wealth ACE Academy conference in San Diego. He suggested that “while stocks were not a great inflation hedge in the short run, in the long run they were perfect” (he emphasized perfect versus good or great). Using a dataset that includes 16 countries spanning 1870-2020, I found that while stocks may not have technically been the perfect inflation hedge, they were better than cash or bonds over extended periods.

While I assumed a mutually exclusive opportunity in the previous article, whereby one could invest in cash, bonds, or equities, in this article I extend the analysis to solve for the optimal allocations between cash and equities for various assumed levels of investor risk-aversion and investment periods.

Equity allocations should increase over longer investment periods, especially for more conservative investors; but even for extended periods, there is some benefit to taking a balanced approach to risk (i.e., allocating to cash). Additionally, when balancing the uncertainty of future market returns with the ability of an investor to leave a portfolio untouched for extended periods, the results suggest that while the equity allocation of portfolios should increase for longer investment horizons, the adjustment should be less than implied by the historical evidence, and it should be based on each investor’s unique situation and preferences.

Dataset

My analysis used a relatively new historical dataset that is freely available online: the Jordà-Schularick-Taylor (JST) Macrohistory database. The JST dataset includes data on 48 real and nominal returns for 18 countries from 1870 to 2020. (Economic data for Ireland and Canada is not available, which limits the analysis to 16 countries: Australia (AUS), Belgium (BEL), Switzerland (CHE), Germany (DEU), Denmark (DNK), Spain (ESP), Finland (FIN), France (FRA), UK (GBR), Italy (ITA), Japan (JPN), Netherlands (NLD), Norway (NOR), Portugal (PRT), Sweden (SWE), and USA (USA).) I focused on three time series variables available in the JST dataset: inflation rates, bill rates, and equity returns.

As I noted in my previous article, stocks outperformed bills for all countries (16/16) over the entire period. This effect is well documented and should not surprise readers, since this is the basis of the equity-risk premium. There are extended periods when stocks underperform, though, and the level of outperformance of equities varied across countries and over time. While stocks have outperformed bonds and cash over the long-term, it hasn’t been a “free lunch.”

My previous analysis focused on how the risk of equities relative to bills and bonds changed by investment period, using two definitions of risk: standard deviation and downside deviation, and two definitions of wealth growth: nominal and real (i.e., inflation adjusted). Downside deviation is a measure of risk that focuses on the returns below a minimum acceptable return (MAR), which was equal to inflation.

The most important metric is downside deviation in real terms, since it captures the negative outcomes when risk is defined in today’s dollars. The exhibit below includes information about how the real downside risk of cash, bonds, and equities changed over different investment periods and is taken from the previous article.

While the real downside deviation of equities was higher than bills and bonds for a one-year investment period, as the investment period increased, the relative real downside risk declined versus bills and bonds (although it still rose in absolute terms). The real downside risk of each of the asset classes also increased over time. All asset classes get riskier over longer investment horizon; what’s important is the relative differences, since one needs to invest in something and stocks have less real downside risk than bills or bonds.

These findings suggest that while equities may not have been a perfect inflation historically, they did better than other alternatives (cash and bonds). This doesn’t necessarily mean an investor should place his or her entire portfolio in stocks, though, since these asset classes aren’t mutually exclusive (i.e., you can invest in both cash and bonds). That’s what I explore in this article: What the optimal combination of safe and risky assets is over various investment periods.

Extended analysis

This article extends my previous analysis. I solve for the optimal allocation between cash and equities for various levels of risk aversion and investment periods. For each period, I solve for the optimal allocation that maximizes the certainty-equivalent wealth using a utility function that assumes constant relative risk aversion (CRRA). I tested three assumed risk tolerance levels: high, mid, and low, which correspond to risk aversion levels of 1, 2, and 8, respectively, in the utility function.

Unlike my previous analysis, which focused entirely on risk, the utility model for this analysis incorporates both risk and return when determining the optimal allocation, and attempts to balance the two, where the trade-off is determined by the risk aversion level. For this analysis, I solve for the optimal equity allocation across all available years at the individual country level. Any year where inflation exceeds 50% (i.e., hyperinflationary periods) is excluded from the analysis.

Results

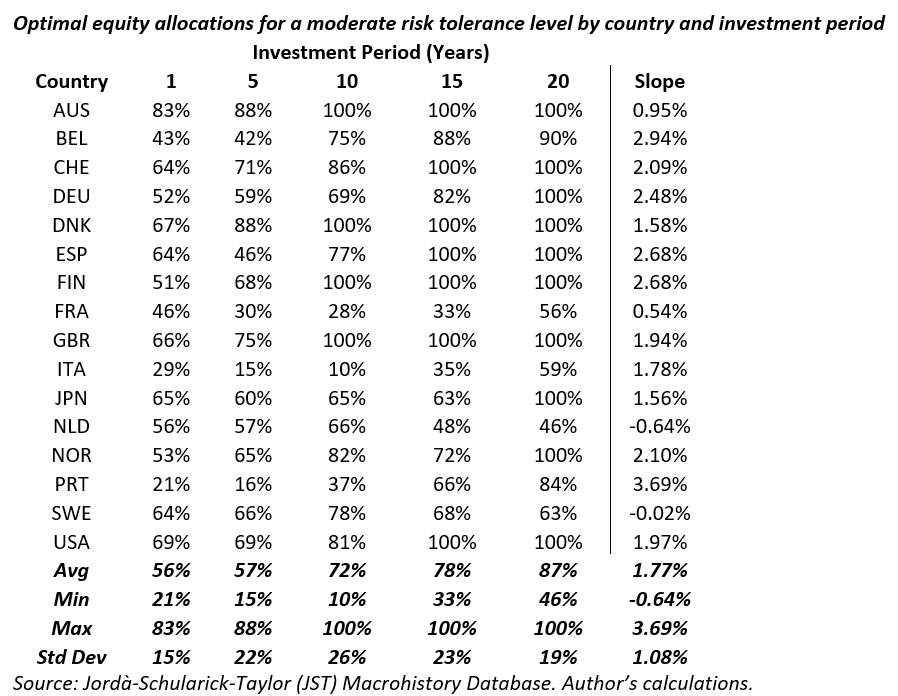

The next exhibit includes the optimal equity allocation for each of the 16 countries for five different investment periods: 1, 5, 10, 15, and 20 years, assuming a moderate risk-tolerance level.

While there were considerable differences in the optimal equity allocation by country for investors with a single-year investment horizon, ranging from 21% to 83% equities, the average allocation was 56%, which would be a relatively balanced portfolio. As the investment period increases to 20 years, the average equity allocation increases to 87%.

Portfolio risk levels rose as the investment period increased for all but two countries (the Netherlands and Sweden). The average increase in equity allocation (i.e., slope) is approximately 2% per year.

The increase in equity allocations was even more pronounced for lower risk tolerance (i.e., a more conservative investor), as demonstrated in the next exhibit. For example, an investor with a low risk tolerance would allocate roughly 20% to equities with a one-year investment horizon versus almost 80% with a 20-year investment horizon.

These results imply that a relatively conservative investor who has a lengthy investment period should invest relatively aggressively; but this assumes this same conservative investor will stay the course (and not transact) over the term (or at least follow a glide-path strategy implied by the previous exhibit). While some may be able to invest in relatively risky portfolios for extended periods, the ability to transact is easier than ever. I’m not convinced someone who would prefer a portfolio with ~20% equities would be okay with a portfolio that’s invested in ~80% equities given an extended duration.

It’s not clear whether past market conditions will continue. While the analysis uses market returns over an extended period for 16 countries, the observations aren’t independent (market returns are related, and increasingly so over time). There has been a negative autocorrelation effect in stock markets historically, whereby stocks went up after they go down. As markets have become more interconnected, there is always the possibility of a relatively pronounced (global) period of economic decline that we have yet to experience that could challenge the longer-term efficacy of stocks as an inflation hedge.

Parting thoughts

“Past performance is not a guarantee or reliable indicator of future results” is the most common disclaimer in the investment management industry. While historical (empirical) data can provide important insights into optimal portfolio decisions, markets are always changing. While equity allocations should increase for portfolios as the investment horizon increases, controlling for risk aversion, I recommend taking a more balanced approach to incorporating these findings.

People aren’t robots building investment strategies; we acknowledge that owning for the long-term can be difficult. Therefore, while the empirical data suggests equities for the long-term, a balanced portfolio for a more realistic term is a safer bet!

David Blanchett, PhD, CFA, CFP®, is managing director and head of retirement research at PGIM. PGIM is the global investment management business of Prudential Financial, Inc. He is also an adjunct professor of wealth management at The American College of Financial Services and a research fellow for the Retirement Income Institute.

Read more articles by David Blanchett

In a previous article, I explored the accuracy of a statement Jeremy Seigel recently made during a presentation at the Investments & Wealth ACE Academy conference in San Diego. He suggested that “while stocks were not a great inflation hedge in the short run, in the long run they were perfect” (he emphasized perfect versus good or great). Using a dataset that includes 16 countries spanning 1870-2020, I found that while stocks may not have technically been the perfect inflation hedge, they were better than cash or bonds over extended periods.

In a previous article, I explored the accuracy of a statement Jeremy Seigel recently made during a presentation at the Investments & Wealth ACE Academy conference in San Diego. He suggested that “while stocks were not a great inflation hedge in the short run, in the long run they were perfect” (he emphasized perfect versus good or great). Using a dataset that includes 16 countries spanning 1870-2020, I found that while stocks may not have technically been the perfect inflation hedge, they were better than cash or bonds over extended periods.