In early May, while attending the Investments & Wealth ACE Academy conference in San Diego, I heard Jeremy Seigel deliver the opening keynote. Two of his comments on the risks of owning equities over the long-term were controversial and worth exploration. He said, “Stocks are the most volatile asset in the short run, but the most stable asset in the long run,” and, “While stocks were not a great inflation hedge in the short run, in the long run they were perfect.” (He emphasized perfect versus good or great).

The key theme of his comment was that the risk of owning equities declines as the time horizon increases, an effect often dubbed “time diversification.” I will explore those comments using historical data. I will demonstrate that evaluating the historical performance of equities depends on the definition of risk. When using appropriate definitions of risk (e.g., downside risk versus standard deviation) and wealth (incorporating inflation), the empirical evidence supports Seigel’s general assertion. But the inflation-hedging benefits of stocks aren’t perfect.

The long-run risk of equities

There is disagreement among academics about how the risk of equities changes over longer investment horizons, an effect commonly dubbed “time diversification.” One of the most notable advocates of the view that the risk of equities declines over longer horizons is Jeremy Siegel, as suggested in the title of his best-selling book Stocks for the Long Run. In that book, Siegel relied heavily on historical U.S. data (i.e., empirical outcomes) to make his case, as he did during his recent presentation.

To extend Siegel’s findings to international markets, Michael Finke, Wade Pfau, and I explored this effect in some research published roughly a decade ago. We relied on returns from the Dimson, Marsh, and Staunton dataset, which spanned 20 countries from 1900 to 2012. Consistent with Siegel’s findings, we found that returns for equities increased over longer time horizons across most markets. For virtually all risk-aversion levels, our findings were consistent with Siegel’s.

There were two explanations for our results. There was a negative autocorrelation effect between the returns on equities over time. After markets went up, they tended to go down (so returns aren’t completely random). This reduced the realized risk of equities over time and is an effect that has been noted by others (such as Campbell and Viceira 2003). Stock returns were notably higher than for cash and bonds, which is important when wealth is viewed in real terms (i.e., adjusted for inflation). Seigel made the case during his presentation that the drivers of stock returns are related to inflation. Not only should the returns of stocks exceed bonds because stocks are riskier (i.e., the equity risk premium) but also because they are driven by inflation.

The idea that owning stocks becomes less risky over longer periods doesn’t necessarily square with other findings, such as research by Zvi Bodie, a professor emeritus at Boston University. He used concepts based on options-pricing models, where the cost of insuring against negative returns increases over the long term (i.e., doesn’t decline). Additionally, Pastor and Stambaugh (2012) noted that while we can treat historical parameters such as the equity-risk premium as certain, an investor faces far more uncertainty into the future. Uncertainty becomes increasingly important over longer investment periods because estimation errors will compound over time.

I’ll demonstrate that how the perceived risk of equities changes over time varies depending on the risk metrics used (e.g., standard deviation versus downside risk) as well as the underlying wealth metric (nominal versus real).

Using the more appropriate definitions of risk (downside risk) and wealth (real), the empirical evidence shows that the risk of owning equities declines as holding periods increase, although the hedging benefits may not be as “perfect” as Siegel suggested.

Dataset

Data for my analysis was obtained from a relatively new historical dataset that is freely available online: the Jordà-Schularick-Taylor (JST) Macrohistory Database. The JST dataset includes data on 48 real and nominal returns for 18 countries from 1870 to 2020. Economic data for Ireland (IRL) and Canada (CAN) is not available, which limited the analysis to 16 countries: Australia (AUS), Belgium (BEL), Switzerland (CHE), Germany (DEU), Denmark (DNK), Spain (ESP), Finland (FIN), France (FRA), UK (GBR), Italy (ITA), Japan (JPN), Netherlands (NLD), Norway (NOR), Portugal (PRT), Sweden (SWE), and USA (USA).

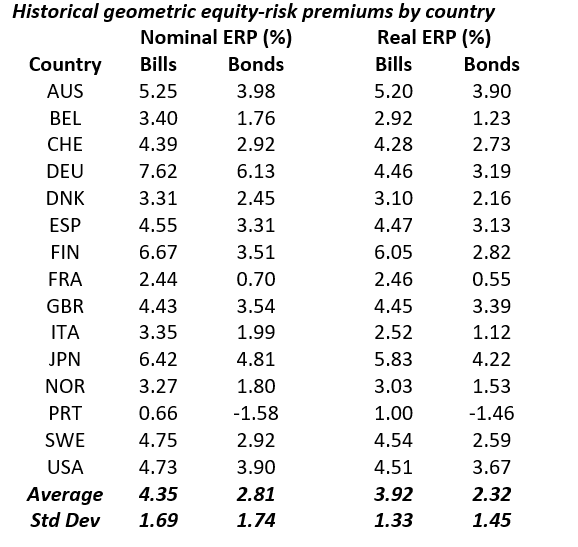

I focused on four time-series variables: inflation rates, bill rates, bond returns, and equity returns. The table below includes the historical equity risk premiums (ERPs) for each of the 16 countries where data is available, in both nominal and real terms.

Stocks outperformed bills for 100% of countries (16/16) and bonds for 94% of countries (15/16). The relative performance of stocks over bills and bonds is unlikely to surprise readers. The fact that stocks have had higher returns is consistent with their higher volatility (i.e., the notion of the equity-risk premium).

To what extent do the risks of owning stocks change over time horizons? I used two definitions of risk: standard deviation and downside deviation, as well as two definitions of wealth growth: nominal and real (i.e., inflation adjusted). Downside deviation is a measure of the risk that focuses on the returns below a minimum acceptable return (MAR). For this analysis, the MAR is a nominal return equal to inflation or a real return of 0%.

My analysis aggregated all periods across all countries simultaneously, and I provided some perspective on individual country results.

Risk over time

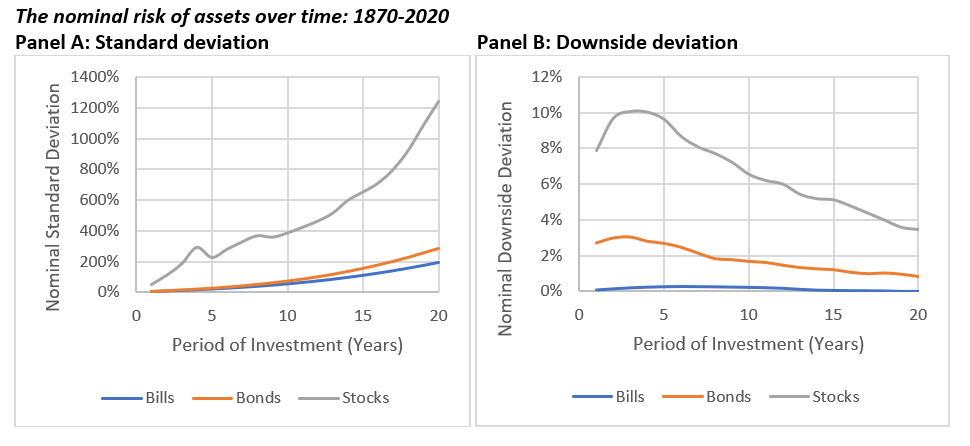

The exhibit below provides context on how the nominal risk of asset classes change over time, where risk is defined as either standard deviation (panel A) or downside deviation (panel B).

Over longer periods, the nominal risks associated with owning equities were greater than bills or bonds. If focusing just on standard deviation (panel A), the variability in wealth was clearly highest when owning equities. While the differences across asset classes lessened, to some extent, when considering only negative cumulative returns (panel B), even the downside risk of owning equities clearly exceeded bills and bonds over a 20-year period.

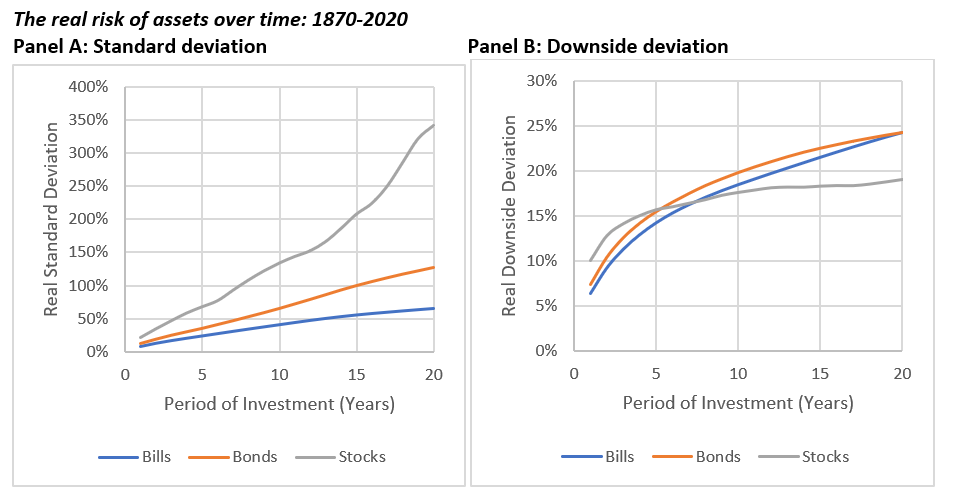

The problem with focusing entirely on nominal returns, though, is that it ignores the fact investors experience wealth in real terms (i.e., adjusted for inflation). The exhibit below includes the results when the risk definitions are adjusted for inflation (i.e., risk is viewed in excess of inflation).

While the variability of real wealth (as measured by standard deviation) increased over time for each asset class, the variation for equities was the highest. When considering real-downside risk, the risk of equities declined relative to bills and bonds. For example, the real downside deviation of equities crossed bonds at approximately a five-year holding period and cash at a seven-year holding period. The risks for all asset classes increased, but the relative risk of owning equities versus cash and bonds varied when viewed in real-downside-deviation terms.

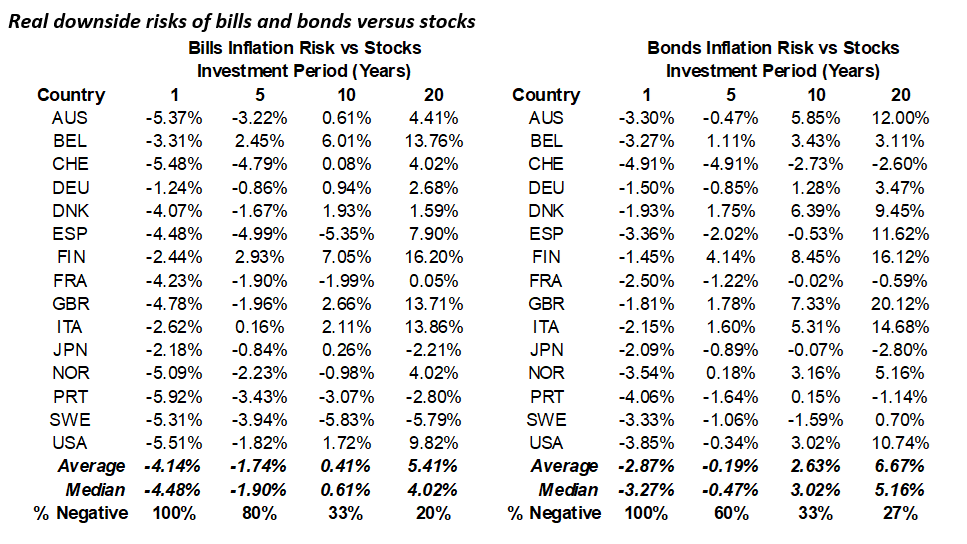

The exhibit below includes the differences in risk for the individual countries for additional context.

There is clear evidence that the real-downside risk of equities was higher over shorter time horizons. For example, the real-downside deviation of equities was higher than bills and stocks for every country for a one-year investment period; but as the period increased, the relative benefit of owning equities clearly increased. While equities might not be a perfect hedge for inflation over longer periods, they clearly became increasingly attractive as an inflation hedge over a longer investment period.

Conclusions

The debate regarding how the risk of equities change over time will never be settled. When thinking about the risk of equities, though, context is important, especially with respect to the definitions of risk and changes in wealth. Using historical returns for 16 countries from 1870 to 2020, my analysis shows that while the nominal variability of wealth was greater for equities over longer periods (e.g., versus bills or bonds), the reverse was true when considering real-downside risk.

Households who want to fund a goal over an extended period that is adjusted for inflation (e.g., retirement income) should actively consider owning equities, even if they are relatively risk averse.

Were equities Siegel’s “perfect” hedge against inflation? The historical evidence shows that the equity-inflation hedge hasn’t been perfect; but it has been better than bills or bonds. I’d describe equities as the “imperfect perfect” hedge against inflation for the long-term.

David Blanchett, PhD, CFA, CFP®, is managing director and head of retirement research at PGIM. PGIM is the global investment management business of Prudential Financial, Inc. He is also an adjunct professor of wealth management at The American College of Financial Services and a research fellow for the Retirement Income Institute.

Read more articles by David Blanchett