The Urgent Changes to Improve Your RIA Website

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Imagine a car dealership that doesn’t tell the public it sells cars. That is the rough equivalent of RIAs failing to tell the public that they plan retirement income. No self-respecting auto dealership would ever fail to tell the public about its product. A parallel failure of such magnitude is infecting the RIA community.

I wish I were kidding.

Unless RIAs modify their communications strategies, the failure to address the need for retirement income communications will be felt for years.

Allow me to make my case.

Caution: NSFW (“No Secure Future Warning!”)

Q. What does a prospective client do when looking for a new financial advisor?

A. Goes to Google to search for “financial advisor.”

Q.What percentage of women are worried about outliving their savings?

A. 63%

Q. What is the number one financial concern of retirees?

A. Retirement income

Q. What are the two words missing from RIAs’ websites?

A. Retirement Income

Even if you don’t recognize this as a disaster in the making, there’s still time to avert catastrophe. But not much. Consider what is taking place:

- The number of Americans reaching age 65 will soon accelerate to 12,000 per day.

- Retirement-age women are taking control of ever-larger amounts of assets, reaching $30 trillion in the next several years. Retirement income will be their financial priority.

- Millions of investors have been placed in income-investing strategies that lack emotional “guardrails” and risk mitigation features. As a result, retirees will be looking for new advisors.

- As their “boomer” husbands pass away in increasing numbers, widows will terminate the majority of advisory relationships with incumbent male advisors.

In a 2013 article that appeared in Retirement Management Journal, I wrote about the lack of retirement income messaging on RIA websites. Nine years ago, I said:

At random, I visited more than 40 RIA websites to assess how these firms are presenting their services related to retirement-income planning. In short, they are not. Looking across dozens of firms’ websites I find a consistent set of themes highlighting accumulation investment expertise, but literally nothing that addresses retirees’ retirement-income needs. Essentially, RIAs’ website messages all focus on better accumulation. For example, “seeking value in volatility,” “above average performance,” “25 years of building client wealth,” “costs matter,” and “the art and science of investing.”

What I viewed in 2013 as the stunning lack of retirement income messaging led me to conclude the following:

RIAs’ historical focus on maximizing investment returns is misaligned with retirees’ deeper concerns for downside protections and smooth, monthly income. And the Registered Investment Advisor channel is arguably the least prepared for retirement income. As a consequence, RIAs are at the greatest risk of becoming competitively marginalized by marketplace dynamics.

My view has not changed.

In fact, it has strengthened in the years since, albeit for reasons I did not foresee. One cannot overstate the degree to which the growth of retirement income planning in the RIA community has been stunted by a 14-year, Fed-engineered bull market.

Since asset prices began to climb following the 2008 breakdown, many advisors have been seduced into believing that systematic withdrawal plans (SWPs) are ideal for their retiree clients. Beginning with my article, “There is No Safe Withdrawal Rate,” I’ve written over recent months pointing out why, for a large segment of investors, including “constrained investors,” a SWP is anything but ideal. I fear for the repercussions retirees will suffer when the party ends. With stock prices dropping, interest rates climbing, inflation surging and the Fed tightening, we are past the bull market’s “last call.” Lots of people are going to needlessly suffer permanently impaired standards of living.

The RIA community’s biggest and most consequential blind spot

I recently had the privilege of making the closing presentation for Advisors Perspectives’ 2022 Market Outlook Summit. I discussed a number of issues that day related to my overarching theme: the retirement income revolution. One issue that has garnered extra attention is my analysis of RIA firms’ website content. I asserted that, while the RIA channel is the fastest growing, most dynamic, most technologically advanced, and the most sought after by product providers of all stripes, it is headed for failure in the greatest business opportunity of all: retirement-income planning.

Here’s the question I want to answer: Are RIAs ready to profit from the retirement income revolution? To find out, I embarked on a search for retirement income.

Searching for retirement income in the RIA community

Let’s say you wanted to search for retirement income in the RIA community. Where would you look? What would you look for? What searching methodology would you use? And how would you assess the relative effectiveness of retirement income communications among various RIA firms? These were some of the questions I was challenged to answer prior to launching my search. As I contemplated those questions, I thought to myself, “Perhaps I can I turn this into a scientific research project? Maybe even get it published in a prestigious academic journal!”

My excitement grew as I imagined revealing the results of my study. But my research study needed a name. I decided upon one: “Searching for Retirement Income in the RIA Community.”

Once I had the name, the next important question to answer was, where to look. For the simple reason that it is a firm’s most important and powerful communications tool, I decided that the RIA website would be the focus of the study.

Those decisions led to another key question: how to evaluate different websites. Voila! A ranking system. But a ranking requires a scoring methodology. Oh man, this was getting complicated. Happily, I was able to devise a scoring methodology, a sliding scale ranging from a low of “0” to a high of “5.” My presumption was that RIA websites with higher ratings will attract more retiree investors. Logical, right? Here are the ranking categories:

Discrete website area displaying exceptionally appealing content. Detailed explanation of the firm's income-planning process. Multiple integrated multimedia elements to enhance the impact of the message. High-end graphic design elements. One or more client examples. Navigated to by a direct menu option.

Discrete website area displaying exceptionally appealing content. Detailed explanation of the firm's income-planning process. Multiple integrated multimedia elements to enhance the impact of the message. High-end graphic design elements. One or more client examples. Navigated to by a direct menu option.

One or more website pages devoted to explaining the firm’s retirement-income planning services. Attractive design with one or more explanatory graphics. Includes at least one hypothetical client example. Navigated to by a direct menu option.

One or more website pages devoted to explaining the firm’s retirement-income planning services. Attractive design with one or more explanatory graphics. Includes at least one hypothetical client example. Navigated to by a direct menu option.

A single website page devoted to explaining that the firm offers retirement-income planning. May reference a methodology the firm favors.

A single website page devoted to explaining that the firm offers retirement-income planning. May reference a methodology the firm favors.

The website includes a single reference of not more than two sentences that inform website visitors that the firm offers retirement income planning.

The website includes a single reference of not more than two sentences that inform website visitors that the firm offers retirement income planning.

The RIA’s website makes no mention of the words “retirement income.”

The RIA’s website makes no mention of the words “retirement income.”

The “RIWCS” score

The “RIWCS” score

OK, I had a name for the study, a scoring methodology, and a system for ranking the websites. But to make this a truly professional endeavor, the next and especially important requirement was… a logo! Check!

Finally, just one more requirement: a shorthand name that everyone can remember, a name that I envision will, on an industry-wide basis, become synonymous with RIA website quality: The retirement income websites communications score, or “RIWCS” for short (pronounced roowks). Doesn’t it just roll off the tongue?

I recognized that simply having a name was not enough. The RIWCS score needed a definition:

I recognized that simply having a name was not enough. The RIWCS score needed a definition:

The RIWCS Score is a measure of the effectiveness of retirement income communications available at RIA websites.

The “RIWCS” Score is important. Why?

- Seismic forces have combined to make retirement income planning the greatest of business opportunities.

- When looking for a new advisor, a prospect visits the websites of local firms. RIAs with higher “RIWCS” scores are more likely to capture new retiree clients and assets.

Screening the RIA websites

To screen RIA websites, I used the Firefox browser’s “find in page” tool. I entered the search term, “retirement income” When the search term is found on the webpage, it is indicated in the search result.

When “Retirement Income” is not found on the webpage, “phrase not found” appears in red.

As I prepared to begin searching for retirement income in the RIA community, I paused. Which RIA firms’ websites should I look at? I decided that a neutral listing of RIA websites was needed. I consulted the CNBC list of top RIA firms. The list was published in 2021, however, I conducted the search during the week of March 6, 2022.

As I prepared to begin searching for retirement income in the RIA community, I paused. Which RIA firms’ websites should I look at? I decided that a neutral listing of RIA websites was needed. I consulted the CNBC list of top RIA firms. The list was published in 2021, however, I conducted the search during the week of March 6, 2022.

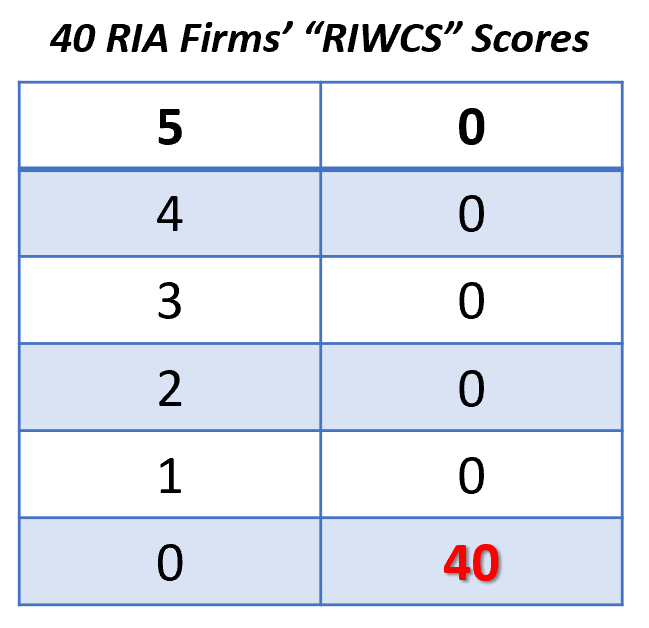

After visiting 10 or so websites from the CNBC listing, I decided to broaden the search. I next looked at Barron’s listing of top RIA firms. I focused on the top 10 on the Barron’s list but decided to stop there out of the concern that these firms, all exceptionally large, were perhaps not representative of the RIA profession.

I discovered a listing of Boston metropolitan area firms that were more diverse in size. My efforts thus have identified 30 RIA websites. Now, it is time to score them.

Scoring the websites

I’ve been at this for hours, yet I am truly excited to score the websites. Beginning with the CNBC listing, I assessed the first website, only to apply a score of “0.” A disappointing beginning, but only one firm. I carry on.

To my great regret, however, the next nine also earned a score of “0.” I became disappointed, but I told myself that, perhaps, this was just something that was a result particular to CNBC’s list. I took comfort in the belief that the “0” scores were nothing more than a statistical anomaly.

To my great regret, however, the next nine also earned a score of “0.” I became disappointed, but I told myself that, perhaps, this was just something that was a result particular to CNBC’s list. I took comfort in the belief that the “0” scores were nothing more than a statistical anomaly.

I next evaluated the RIA websites from the Barron’s list. Oh no! “0, 0, 0, 0, 0, 0, 0, 0, 0, 0.” Ten zeros? Incredible, but true. That said, I remained undaunted, telling myself that both lists favored the largest RIA firms which, unfortunately, were clearly not specializing in retirement-income planning.

Moving to the Boston metropolitan area firms, 10 in total, I remained optimistic. That was until I began the scoring process: “0, 0, 0, 0, 0, 0, 0, 0, 0, 0!” OK, now I was experiencing BITTER DISSAPOINTMENT! Thirty RIA websites and my search revealed not a single mention of the words, “retirement income.”

Moving to the Boston metropolitan area firms, 10 in total, I remained optimistic. That was until I began the scoring process: “0, 0, 0, 0, 0, 0, 0, 0, 0, 0!” OK, now I was experiencing BITTER DISSAPOINTMENT! Thirty RIA websites and my search revealed not a single mention of the words, “retirement income.”

Now, late at night, disappointed, and utterly exhausted from my fruitless search for retirement income in the RIA community, I said to my wife, “Darling, good night, I’m going to bed.”

Thankfully, sleep is restorative. I woke up filled with energy. “Good morning!” I decided to broaden my search for retirement income. I have it! I will pick 10 random cities in the U.S., search for “registered investment advisor” in each of those cities, and then assess the website of the first RIA firm that Google returned. I was optimistic.

I began with Cleveland, then moved to Los Angeles, Philadelphia, and Tampa. Tampa! Heck, If Tampa can attract Tom Brady to return for a third season, it certainly can attract retirement income. After all, it is Florida!

My search next took me to Charlotte, Denver Chicago, Dallas, Milwaukee and, finally, Minneapolis. With both my energy level and optimism high, I began the assessment. NO!@#@!#$! “0, 0, 0, 0, 0, 0, 0, 0, 0, 0.”

My unfortunate conclusion: “When it comes to retirement income, RIAs are a bunch of RIWCS zeroes.”

The serious research study conclusions

My analysis proved that RIA websites do not include communication on the critically important topic of retirement-income planning. But in a practical sense, what does that mean? Should we conclude that RIAs do not care about retirement income?

No, I don’t believe that.

Does it tell us that RIAs do not recognize retirement-income planning as a discrete business opportunity?

“Yes,” for sure.

Does it tell us the RIAs look at retirement-income planning as a reverse of dollar-cost-averaging? Yes! That is why the SWP so popular in the RIA community. Does the study’s results indicate that RIAs are overconfident? Perhaps. Or that RIAs view income planning as associated with annuities? Maybe.

But what the study tells us, more than anything else, is that $10 trillion in money creation, plus zero percent interest rates, plus growth of debt equal to $40 trillion since 2008 has created an unprecedented 14-year bull market that has distorted everything. Is this period of distortion ending? I believe it is. In fact, we have entered a new era in personal finance which will be notable for its sharp focus on risk mitigation.

RIAs, this is adjustment time.

Wining, or losing: The stakes are high

Failing to be in front in retirement income is a dangerous business strategy. The income planning business opportunity is too big to not pursue properly. To win, RIAs must align their communications, planning methodologies, and product set with the needs of retirees, especially women, whose priority is reliability-of-income more than return-on-investment.

To jumpstart your efforts, let me suggest some content to put on your websites.

The sentence below is taken from the back cover of my book, Constrained Investor. I hereby give any reader permission to use it on your website. This alone will give you a “RIWCS” score of 1:

Whether you have saved $100,000 or $10 million, the investing strategy you use to turn your savings into retirement income is one of the most consequential financial decisions you will ever make.

Other content you may add:

- At ‘Your Name Investment Advisors,’ we specialize in retirement-income planning.

- Women face financial challenges that men do not face. These, combined with the fact that women live longer, create a special level of dependence upon retirement income. We recognize these concerns and challenges, and we help women plan for their retirement income. (Add a photo along side this and you will earn a “RIWCS” score of 2.)

- Retirement-income planning is a specialty at ‘Your Name Investment Advisors.’ We help you answer these important questions:

-

- How much can I safely spend?

- How much risk should I take?

- What investments should I choose?

Knowing how to turn savings into retirement income that lasts, and keeps pace with inflation, requires a skill set that not all financial advisors possess. But it is a specialty at our firm.”

Conclusion

I began with this:

Unless RIAs modify their communications strategies, the failure to address the need for retirement income communications will be felt for years.

Have I made my case?

I’ll be looking at your website to see if I have.

Wealth2k® founder David Macchia is an entrepreneur, author, IP inventor and public speaker whose work involves improving the processes used in retirement income planning. David is the developer of the widely used The Income for Life Model®, and the recently introduced Women And Income®. David has authored many articles on the subjects of retirement income planning and financial communications. He is the author of two books, Constrained Investor®, and Lucky Retiree: How to Create and Keep Your Retirement Income with The Income for Life Model®.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All