Enhancing Investment Performance by Combining Factor-Based Stock Selection with Multi-Indicator Trend Following

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

To achieve superior, long-term investment performance, investors should adopt a good offensive and defensive strategy.

An offense-oriented investment strategy that invests in stocks that have significant quality, value, momentum or low-volatility factor advantages is an excellent way to produce long-term, market-beating returns. Unfortunately, those strategies can be volatile and subject to large drawdowns, which makes them poorly suited for risk-adverse investors.

However, by combining factor-based stock selection with a defense-focused, multi-indicator trend-following strategy as a portfolio overlay, investors will significantly reduce the risks associated with this form of stock selection, and thus, achieve better long-term absolute and risk-adjusted returns.

To obtain the best long-term risk-adjusted performance, investors should combine multiple trend-following factor strategies into a single portfolio.

Introduction

Like any great sports team, an investor needs to play good offense and good defense to win. By combining the offensive power of factor-based stock selection with the defensive benefits of multi-indicator trend following, an investor can do just that. The objective of such a combined strategy is to produce long-term market-beating returns through superior stock selection while also significantly reducing downside risk by using a robust trend-following strategy.

In my prior article, “Reducing Downside Risk through Multi-Indicator Trend-Following Strategies,” I discussed how an investor can achieve superior long-term investment performance by simply reducing portfolio drawdowns. I showed how a multi-indicator trend-following strategy applied as an overlay to a passive market index exchange traded fund (EFT) investment can produce better long-term absolute and risk adjusted returns compared to merely buying and holding the stock market index. In this article, I will demonstrate how combining this defense-focused trend-following strategy with offense-oriented factor-based stock selection models, such as those based on quality, value, momentum or low volatility, can produce even better long-term performance.

Adopting factor-based stock selection for good offense

Factor-based stock selection is one of the best ways for an investor to achieve long-term market-beating returns. But what exactly is it?

Factor-based stock selection is simply a systematic method of selecting individual stocks based on certain key characteristics or factors that have been shown to produce superior long-term investment performance. According to my own research, as well as that of the broader financial academic community1, the most significant factors are those based on a stock’s value, momentum, quality or volatility. For purposes of this article, I define each of these factors as follows:

Value = free cash flow yield (i.e., trailing 12-month free cash flow/enterprise value)

Momentum = trailing 12-month price return

Quality = profitability as measured by gross profit-to-assets ratio (i.e., gross profit/total assets)

Volatility = trailing 2-year standard deviation of monthly returns

To demonstrate the effectiveness of each factor, I create individual factor portfolios comprised of the 100 stocks within the S&P Composite 1500 stock market index2 that have the highest degree of specific factor exposure. For example, the value portfolio is made up of the 100 stocks within the S&P Composite 1500 Index with the highest free cash flow yield. The momentum portfolio is made up of the 100 stocks with the highest trailing 12-month price return. The quality portfolio is made up of the 100 stocks with the highest gross profit-to-total assets ratio. And the low volatility portfolio is made up of the 100 stocks with the lowest trailing 2-year standard deviation. In addition, the stocks within each portfolio are equally weighted and each portfolio is rebalanced and reconstituted on an annual basis.

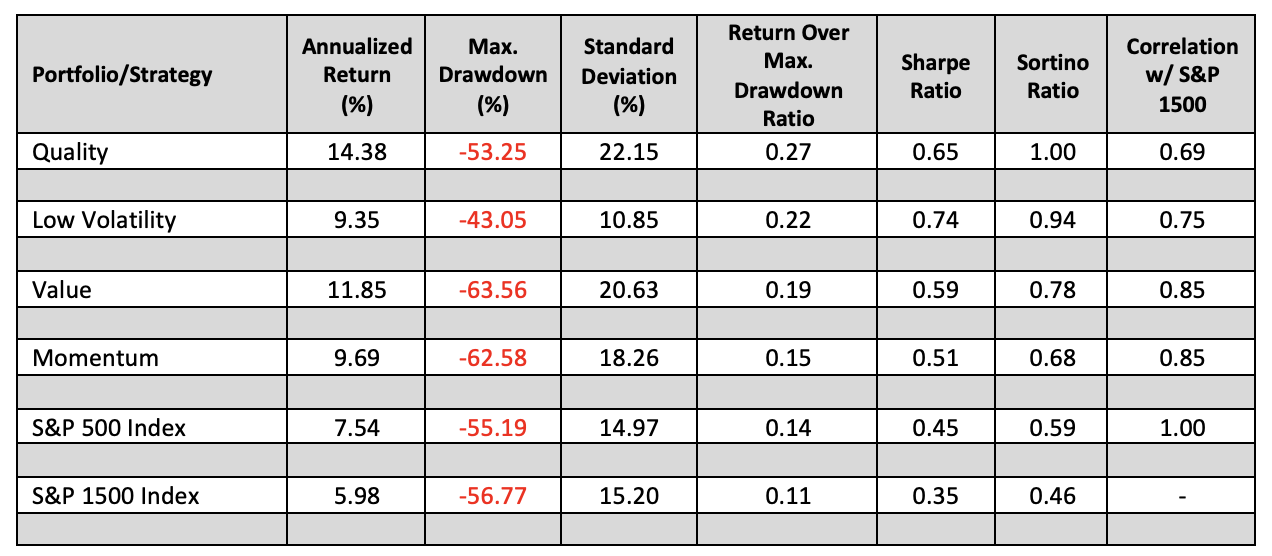

As seen in Figure 1, each factor portfolio substantially outperformed both the S&P 500 and S&P Composite 1500 stock market indexes on an absolute basis over the last 22-years based on their annualized return. Each factor portfolio also outperformed the two stock market indexes on a risk-adjusted basis as exhibited by their higher return over maximum drawdown, Sharpe and Sortino ratios. However, despite their outperformance, all factor portfolios also experienced a significant decline during this time period, with only the quality and low volatility portfolios experiencing a maximum drawdown lower than that of both market indexes. Moreover, except for the low volatility portfolio, each factor portfolio also was more volatile than each market index, as seen by their higher standard deviation. Therefore, despite their market-beating absolute and risk-adjusted performance, the high volatility and/or large drawdowns associated with each factor strategy suggests that achieving such results may be difficult for many investors to stomach.

Figure 1: 22-year performance statistics – Single factor portfolios vs. S&P 500 and S&P Composite 1500 Indexes (8/1/1999 – 8/1/2021)3

Source: MER Capital Management, with FactSet data via Portfolio 123.

Source: MER Capital Management, with FactSet data via Portfolio 123.

Adding multi-indicator trend-following for good defense

Fortunately, the risks associated with each factor strategy can be significantly reduced by applying a multi-indicator trend-following strategy as an overlay to each factor portfolio.

To demonstrate the benefits of such a combined strategy I use the same multi-indicator trend-following strategy that I outline in my prior article “Reducing Downside Risk through Multi-Indicator Trend-Following Strategies.” As described in that article, this trend-following strategy looks at a combination of long and short-term moving averages, volatility and time series market timing indicators to determine when, or when not, to be invested in stocks. By operation, this trend-following strategy seeks to reduce portfolio risk by moving the portfolio out of stocks and into safer assets, such as cash or government bonds, when the current market trend suggests that the risk of owning stocks is high. It also seeks to keep the portfolio principally invested in stocks when the current market trend suggests that the risk of owning stocks is moderate to low. However, instead of applying this multi-indicator trend-following strategy as an overlay to a passive S&P 500 stock market index ETF investment as I did in my prior article, here I apply it as an overlay to each factor portfolio. I also have chosen to use an intermediate term government bond fund, as opposed to cash, as the hedge asset for each factor strategy.

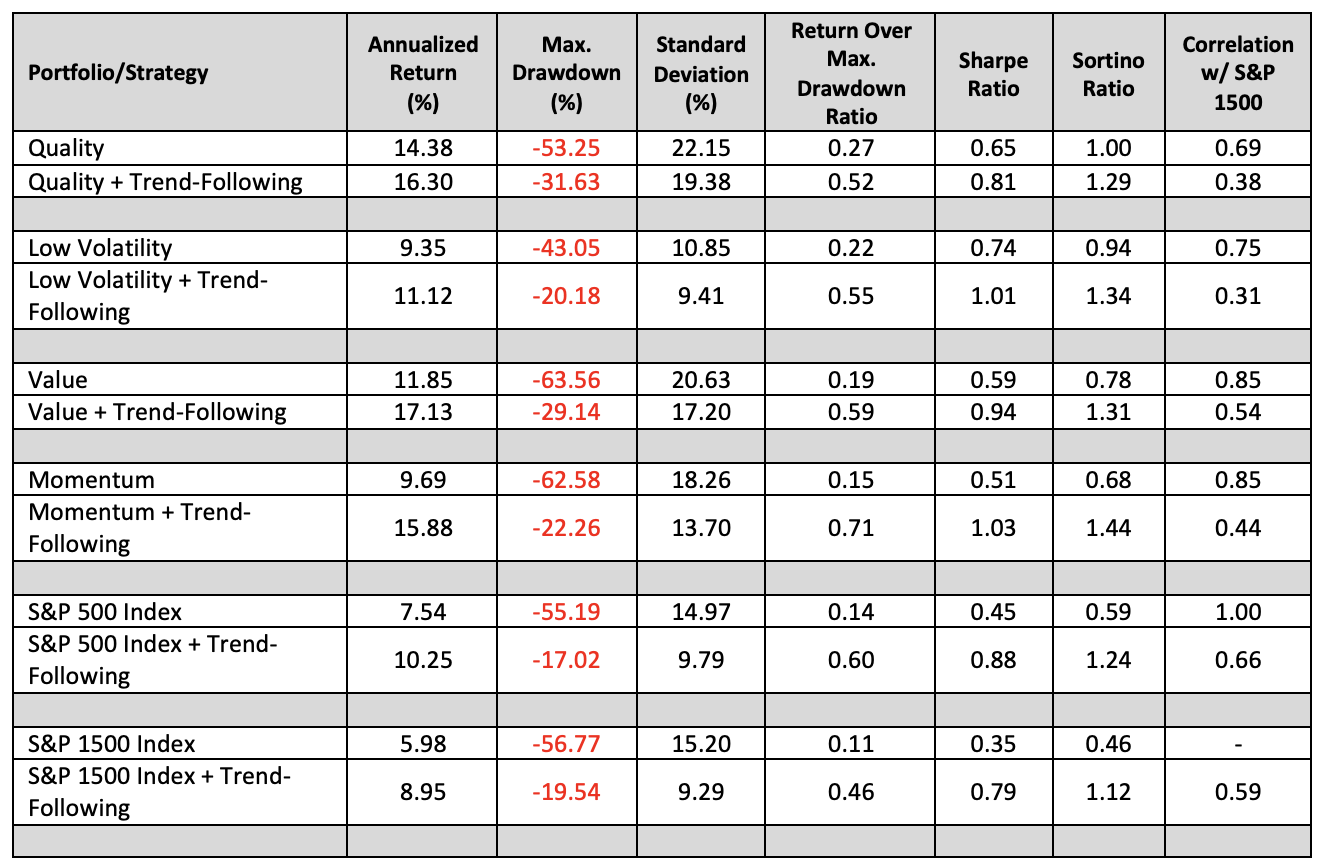

As you can see from Figure 2, over the last 22 years, the application of this multi-indicator trend-following strategy to each factor portfolio significantly enhances the absolute and risk-adjusted performance of each factor strategy. Not only does each trend-following factor portfolio have a higher annualized return compared to its unhedged version, they also achieved this higher return with substantially lower volatility and maximum drawdown. As a result, the return over maximum. drawdown, Sharpe and Sortino ratios for each trend-following factor portfolio are much higher than those for their respective unhedged versions.

Figure 2: 22-year performance statistics – Single factor portfolios with trend-following vs. unhedged single factor portfolios and the S&P 500 and S&P Composite 1500 Indexes with and without trend-following (8/1/1999 – 8/1/2021)

Source: MER Capital Management, with FactSet data via Portfolio 123.

Source: MER Capital Management, with FactSet data via Portfolio 123.

The trend-following factor portfolios also produced better annualized returns compared to both trend-following and buy and hold market index portfolios. They also outperformed the market index portfolios on a risk-adjusted basis as seen by their higher Sortino Ratio. However, each trend-following factor portfolio experienced a larger maximum drawdown compared to both market index trend-following portfolios. And, except for the low volatility trend-following strategy, the trend-following factor strategies also were more volatile. Nevertheless, for investors who are willing to accept a slightly higher level of portfolio volatility and downside risk, the trend-following factor strategies exhibit a clear advantage over both market index trend-following strategies.

Combining strategies for superior risk-adjusted performance

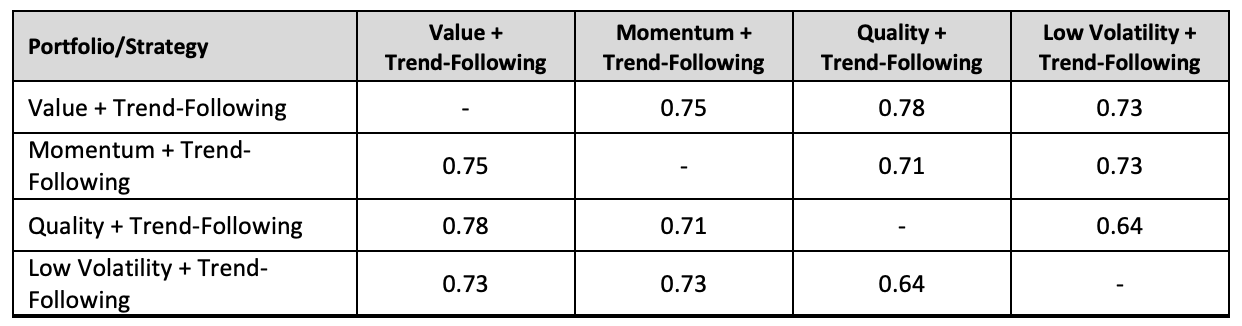

As shown in Figure 3, the modest cross-correlation between the trend-following factor strategies suggests that a combined strategy, made-up of an equal allocation to all four trend-following factor portfolios, can produce significantly better risk-adjusted performance compared to any single trend-following factor strategy.

Figure 3: Trend-following factor strategies – Cross-correlation matrix (8/1/1999 – 8/1/2021)

Source: MER Capital Management, with FactSet data via Portfolio 123.

Source: MER Capital Management, with FactSet data via Portfolio 123.

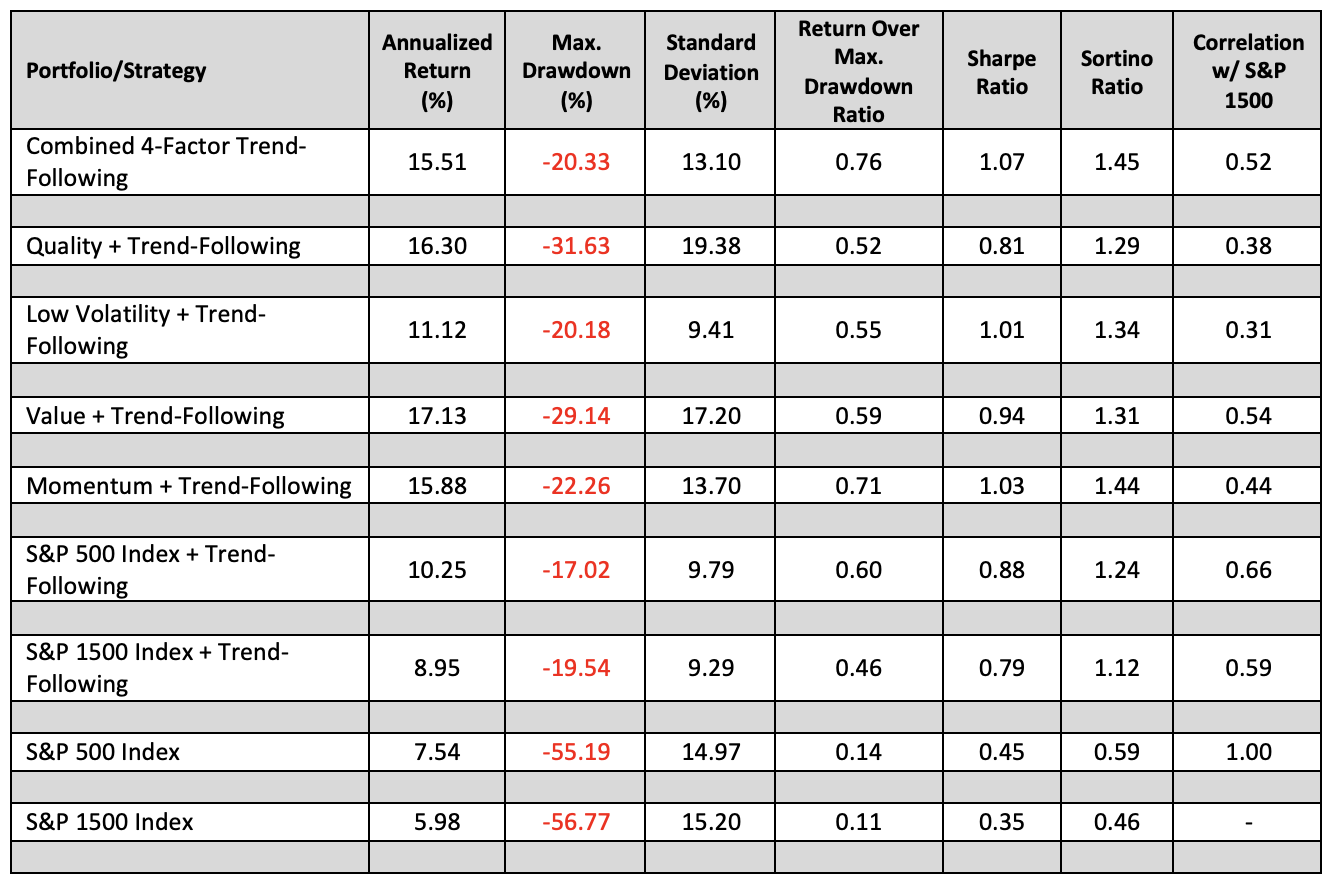

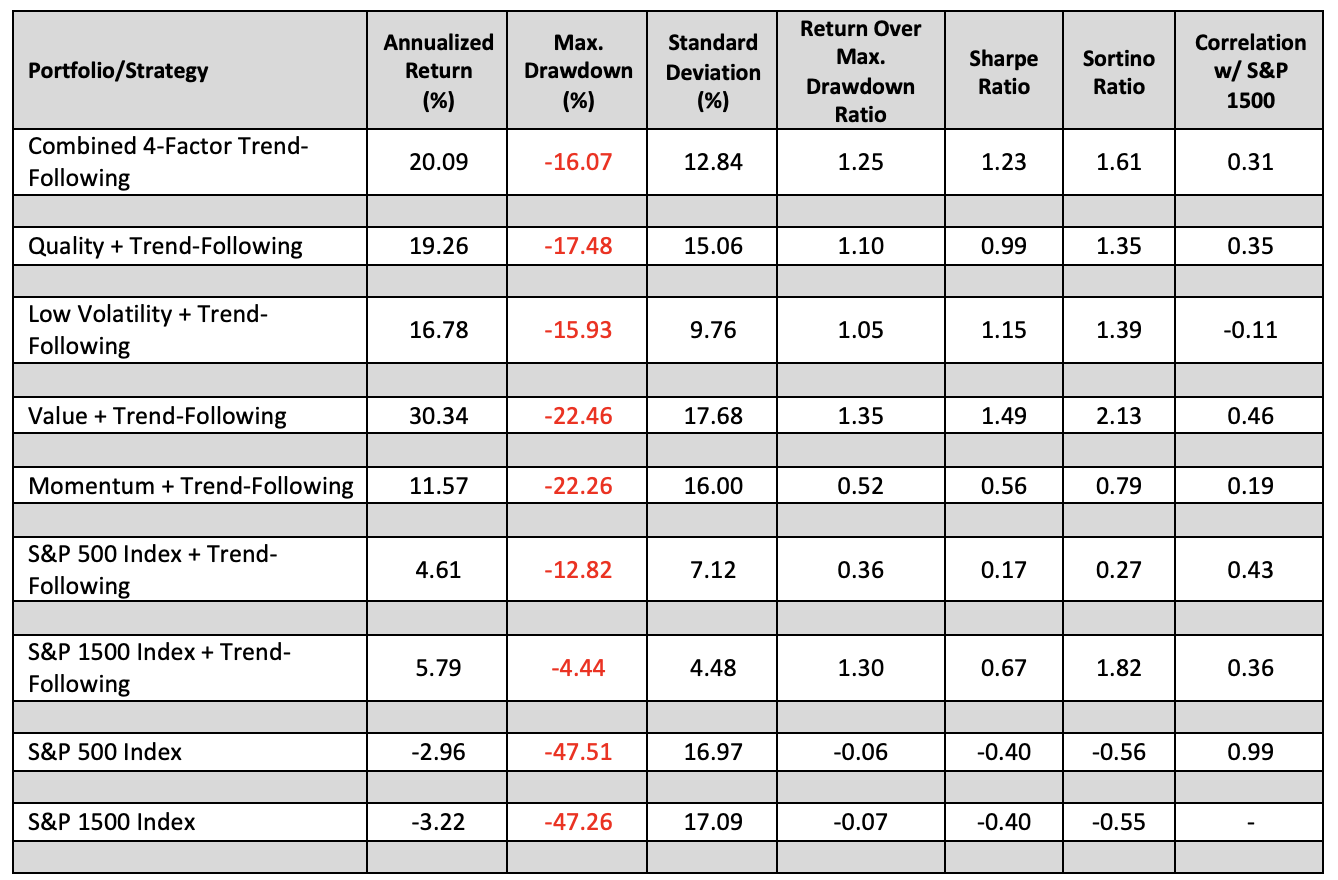

Figure 4 provides a detailed examination of the comparative long-term performance of such a combined trend-following factor strategy versus each single factor trend-following strategy and the two market index trend-following strategies. Here you can see that the combined 4-factor trend-following portfolio produced the fourth highest annualized return (i.e., 15.51%), the fourth lowest maximum drawdown (i.e., -20.33%) and the fourth lowest volatility (i.e., 13.10% standard deviation) among the seven portfolios. Nevertheless, despite not having placed first in any of the aforementioned statistics, the balanced performance of the combined 4-factor trend-following portfolio enabled it to achieve the highest return over max. drawdown, Sharpe and Sortino ratios, and thus, the best overall risk-adjusted performance of any portfolio during the 22-year period.

Figure 4: 22-year performance statistics – Combined 4-factor trend-following portfolio vs. single trend-following factor portfolios and the S&P 500 and S&P Composite 1500 Indexes with and without trend-following (8/1/1999 – 8/1/2021)

Source: MER Capital Management, with FactSet data via Portfolio 123.

Source: MER Capital Management, with FactSet data via Portfolio 123.

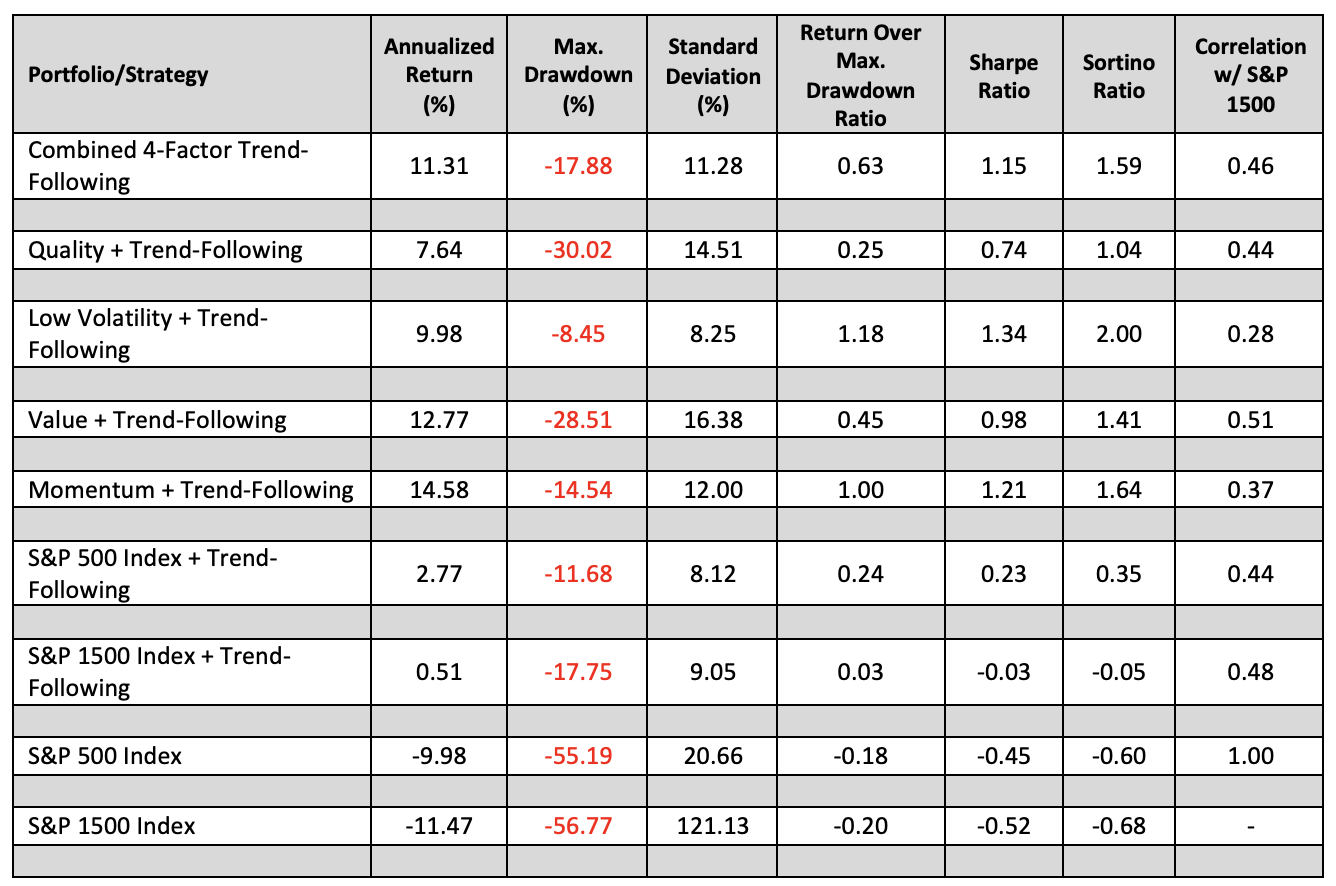

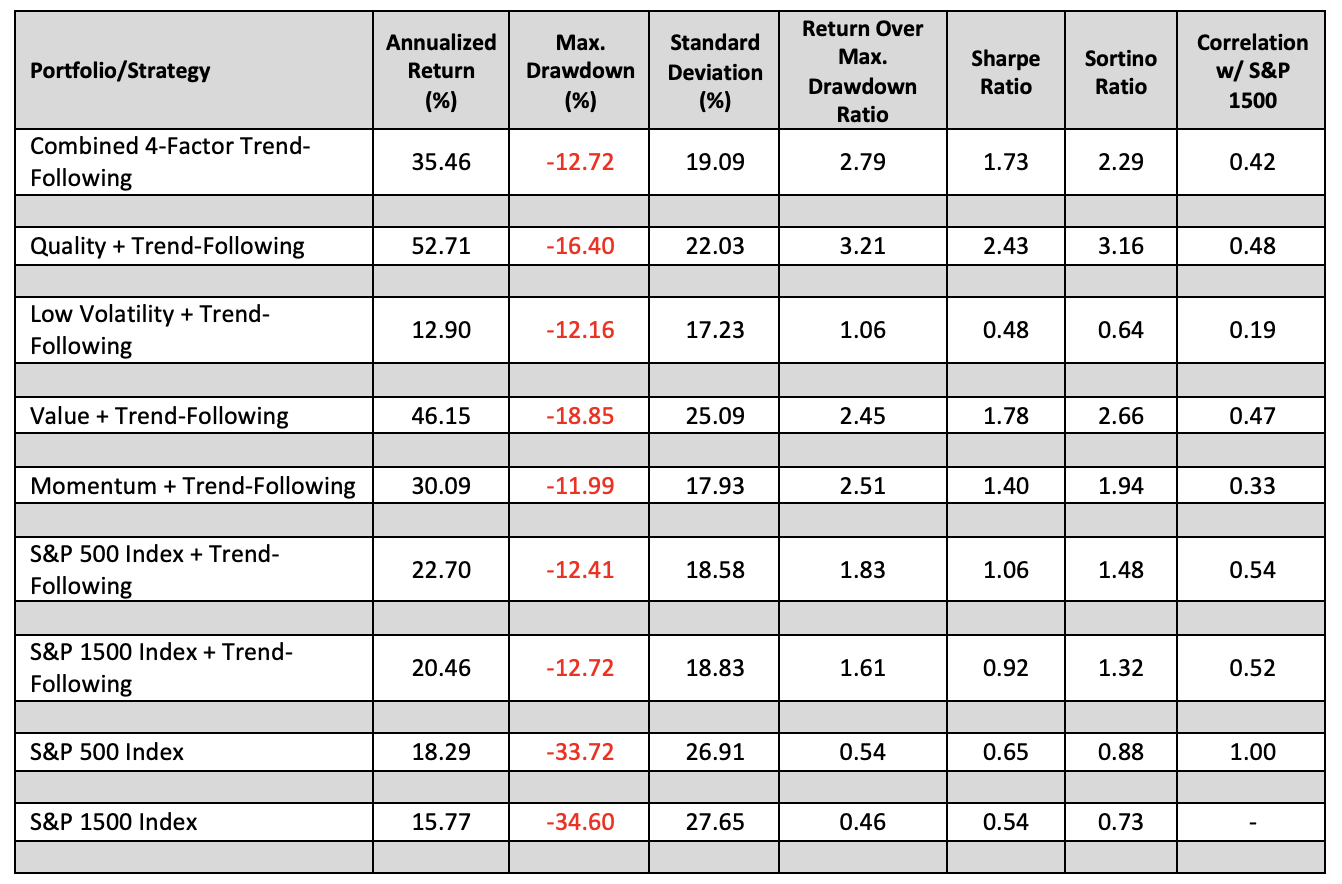

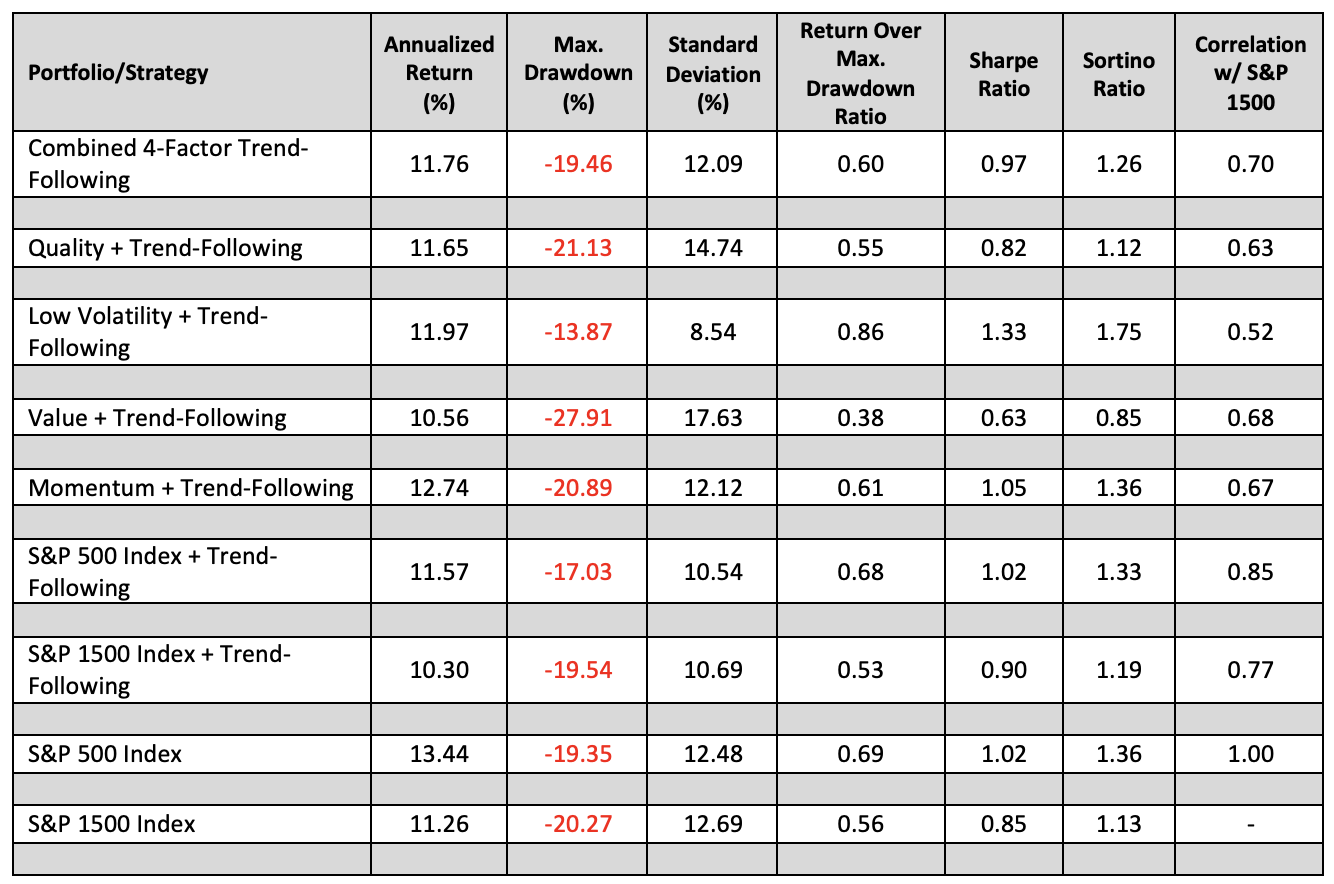

Moreover, as seen in Figures 5-8, the combined 4-factor trend following strategy produced the most consistent absolute and risk-adjusted performance during each of the three most recent market crisis periods as well as during the post-financial crisis bull market. Although the combined 4-factor trend following strategy’s performance did not place first in any of these periods, its consistent middle to top-half absolute and risk-adjusted performance during these bull and bear markets suggests that it’s the best strategy to deal with a multitude of market environments. Consequently, by combining multiple trend-following factor strategies into a single portfolio, investors are more likely to achieve significantly better long-term, absolute and risk-adjusted performance compared to any single strategy.

Figure 5: Dotcom crash performance statistics – Combined 4-factor trend-following portfolio vs. single trend-following factor portfolios and the S&P 500 and S&P Composite 1500 Indexes with and without trend-following (3/1/2000 – 3/1/2004)

Source: MER Capital Management, with FactSet data via Portfolio 123.

Source: MER Capital Management, with FactSet data via Portfolio 123.

Figure 6: Financial crisis performance statistics – Combined 4-factor trend-following portfolio vs. single trend-following factor portfolios and the S&P 500 and S&P Composite 1500 Indexes with and without trend-following (7/1/2007 – 7/1/2010)

Source: MER Capital Management, with FactSet data via Portfolio 123

Source: MER Capital Management, with FactSet data via Portfolio 123

Figure 7: 2020 COVID correction performance statistics – Combined 4-factor trend-following portfolio vs. single trend-following factor portfolios and the S&P 500 and S&P Composite 1500 Indexes with and without trend-following (1/1/2020 – 1/1/2021)

Source: MER Capital Management, with FactSet data via Portfolio 123.

Source: MER Capital Management, with FactSet data via Portfolio 123.

Figure 8: Post-financial crisis bull market performance statistics – Combined 4-factor trend-following portfolio vs. single trend-following factor portfolios and the S&P 500 and S&P Composite 1500 Indexes with and without trend-following (1/1/2010 – 1/1/2020)

Source: MER Capital Management, with FactSet data via Portfolio 123.

Source: MER Capital Management, with FactSet data via Portfolio 123.

Conclusion

To achieve superior, long-term investment performance investors should adopt a strategy that includes both good offense and good defense.

An offense-oriented investment strategy that invests in stocks that have significant quality, value, momentum or low-volatility factor advantages is an excellent way to produce long-term market-beating returns. Unfortunately, these factor-based strategies can be volatile and subject to large drawdowns which may make them poorly suited for risk-adverse investors. However, by combining factor-based stock selection with a defense-focused, multi-indicator trend-following strategy as a portfolio overlay, investors can significantly reduce the risks associated with this form of stock selection, and achieve better long-term absolute and risk adjusted returns. For the best long-term, risk-adjusted performance, investors should consider combining multiple trend-following factor strategies into a single portfolio.

Key Definitions

Maximum Drawdown means the largest drop from peak to bottom during a certain time period, expressed in percentage from the peak.

Standard Deviation is a statistical measure that shows the historical volatility of an investment’s return. The greater the standard deviation, the greater the volatility.

Return Over Max. Drawdown Ratio is a risk-adjusted performance measure which shows the relationship between an investment’s return and its maximum loss for a specific time period. It divides the average annualized return of an investment by its maximum drawdown. The investment with the highest Return Over Max. Drawdown ratio is deemed to have the best risk-adjusted return (i.e., the highest return per unit of downside risk).

Sharpe Ratio is a measure of an investment’s risk-adjusted performance. It divides the average of an investment’s return by the standard deviation (i.e., volatility) of returns. The investment with the highest Sharpe ratio is deemed to have the best risk-adjusted return.

Sortino Ratio is a measure of an investment’s downside risk-adjusted performance. It divides the average of an investment’s return by the downside standard deviation (i.e., negative volatility) of returns.

Like the Return Over Max. Drawdown and Sharpe ratios, the investment with the highest Sortino ratio is deemed to have the best risk-adjusted return. However, this measure of risk-adjusted return typically is considered superior to the Sharpe ratio because it measures an investment’s performance in relation to only its volatility of negative returns or downside volatility.

Correlation is a measure of the statistical similarity of a strategy’s return with that of another strategy or market index for a specific time period. The higher the correlation, the more similar the returns. For example, a correlation of 1.0 means that the pattern of historical returns between two strategies is exactly the same, with a correlation of -1.0 meaning that the pattern of historical returns between two strategies is exactly in opposite. Accordingly, strategies that have a low or negative return correlation with each other tend to be good diversifiers.

Mark E. Ricardo, JD, LLM, AAMS®, is president and chief investment officer of MER Capital Management, a quantitative money management firm specializing in providing risk-managed equity portfolios to individuals, institutions, and other investment advisory firms through separately managed accounts and model portfolios. Additional information about Mr. Ricardo and MER Capital Management can be obtained at www.mercapitalmanagement.com. Mr. Ricardo can be contacted at [email protected].

1See, F. Goltz and B. Luyten, The Risks of Deviating from Academically-Validated Factors, Scientific Beta Report (February 2019); A. Perrins, Factor Investing: An Academic Source of Excess Returns, Savvy Investor Special Report (March 2018); J. Huij, Factor Investing Case Studies, Robeco Whitepaper (September 2016); and D. Blitz, J. Huij, S. Lansdorp and P. van Vliet, Efficient Factor Investing Strategies, Robeco Whitepaper (May 2016).

2To test the robustness of each factor strategy, I also used the Russell 3000 Index as the beginning stock universe. The results for each factor strategy were substantially similar to those achieved when using the S&P Composite 1500 Index as the beginning stock universe.

3All strategy returns are back-tested annualized total returns for the applicable period net of a $5.00 per trade brokerage commission and a 0.05% slippage charge.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All