Reducing Downside Risk through Multi-Indicator Trend-Following Strategies

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Avoiding large market declines is crucial to not only managing an investor’s risk tolerance but to enhancing their long-term compounded investment returns.

Avoiding large market declines is crucial to not only managing an investor’s risk tolerance but to enhancing their long-term compounded investment returns.

Applying a relatively simple single indicator trend-following strategy as an overlay to a market index exchange traded fund, such as the SPDR S&P 500 Index ETF (SPY), is an excellent way to obtain meaningful exposure to the overall market with significantly lower downside risk and higher long-term risk-adjusted returns.

However, the simplicity associated with a single indicator trend-following strategy can cause it to underperform the market on an absolute basis during protracted up markets. A single-indicator strategy also can be significantly less tax efficient compared to a buy-and-hold index investment.

By adopting a multi-indicator trend following strategy, investors can overcome many of the disadvantages associated with a single-indicator strategy, and thus achieve better long-term absolute and risk-adjusted returns during both up and down markets.

The importance of downside risk reduction

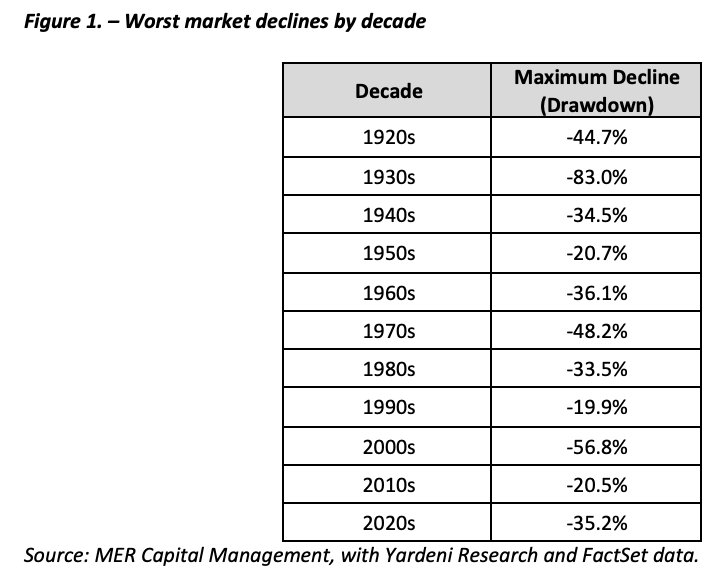

To achieve their long-term investment objectives, most investors are required to maintain a significant allocation to stocks. Unfortunately, a heavy allocation to stocks comes with the risk of large drawdowns or peak-to-bottom declines in portfolio value as a result of protracted market corrections and periodic crashes. For example, as set forth in Figure 1, since the 1920s, every decade except for the 1990s has had at least one market decline worse than -20%; the two largest declines of -83.0% and -56.8% occurred during the great crash of 1929 and the financial crisis of 2007-2008. Even the newly established current decade already has seen a decline of more than -35%.

Avoiding those large market declines is crucial to not only managing an investor’s risk-tolerance but also to enhancing their long-term compounded investment returns. Although most investors instinctually focus on their portfolio’s upside performance, it is their ability to mitigate downside risk that defines their long-term investment success. This is because steep market declines create large holes from which investors must recover. As losses grow ever larger, so too does the subsequent return needed to get back to the pre-decline starting point.

For example, if a portfolio loses a modest 10% of its value, it will need only a subsequent 11% gain to recover the loss. However, a 50% loss would require a 100% subsequent gain and a 60% loss would require a staggering 150% subsequent gain to get back to even. Consequently, as a result of compounding, if an investment strategy can significantly outperform in down periods, it will not have to keep up with the market in up periods in order to produce superior long-term returns. Thus, by managing downside risk, an investor can substantially enhance the long-term performance of their investment portfolio, so as to “win by not losing.”

Mitigating downside risk with trend-following

One of the most effective ways to reduce portfolio downside risk is by using a trend-following strategy as a portfolio overlay. In its most basic form, this involves looking at a market trend indicator, such as a market’s recent past performance or current value in relation to its simple-moving average over a specific time period, to determine when to be invested in the market. Accordingly, a trend-following hedge is a market-timing strategy that seeks to reduce portfolio risk by moving the portfolio out of the market and into safer assets such as cash or government bonds. It does this when the market trend suggests that the risk of owning stocks is high and seeks to keep the portfolio principally invested in stocks when the current market trend suggests that the risk of owning stocks is moderate to low.

An example of a straightforward trend-following hedge strategy is to compare the market value of the SPDR S&P 500 Index ETF (SPY) to its trailing 12-month simple moving average at the beginning of each week. If the current value of SPY is greater than or equal to its trailing 12-month simple moving average, an investor should stay invested in SPY. However, if the current value of SPY is lower than its trialing 12-month simple moving average, an investor should sell out of SPY and invest in cash as the hedge asset.1

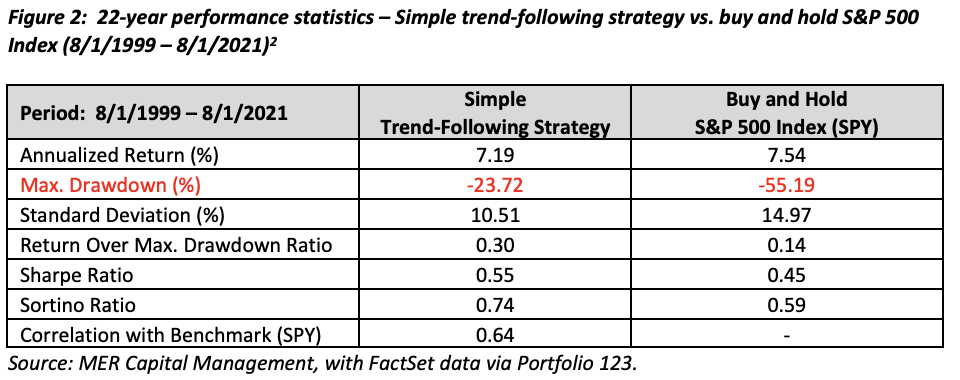

As you can see from Figure 2, over the last 22 years this simple trend-following strategy produced an annualized return comparable to that of the buy-and-hold S&P 500 Index but with substantially lower volatility (i.e., standard deviation) and downside risk (i.e., maximum drawdown). It also produced higher risk-adjusted returns as measured by the return over max. drawdown, and Sharpe and Sortino ratios. The trend-following strategy also had a modest 0.64 correlation with the overall market, suggesting that the strategy can be used as a stand-alone investment or as solid diversifier within a broader investment portfolio.

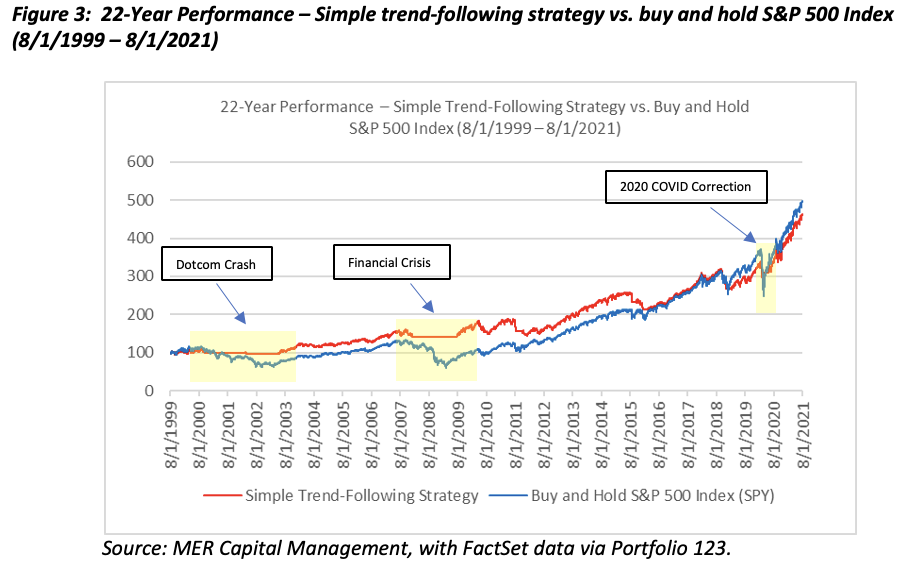

Figure 3 provides a graphical representation of the comparative performance of the simple trend-following strategy versus the buy and hold S&P 500 Index over the entire 22-year performance period. From this graph, you can see how the trend-following hedge significantly reduced portfolio drawdowns during the dotcom crash, the financial crisis and last year’s COVID correction.

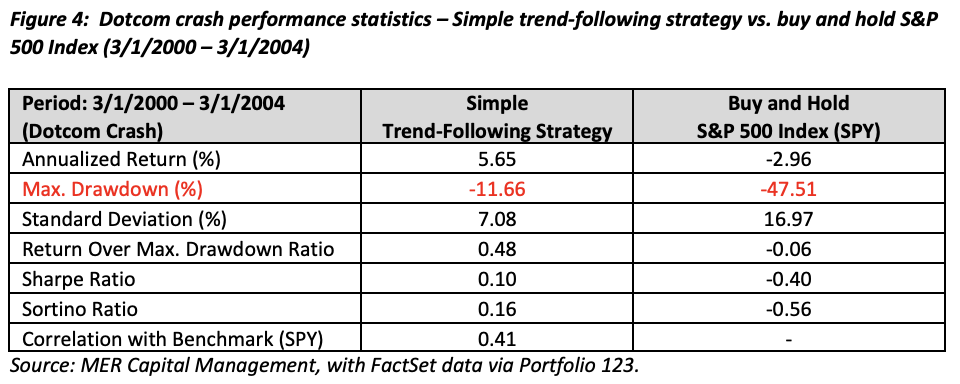

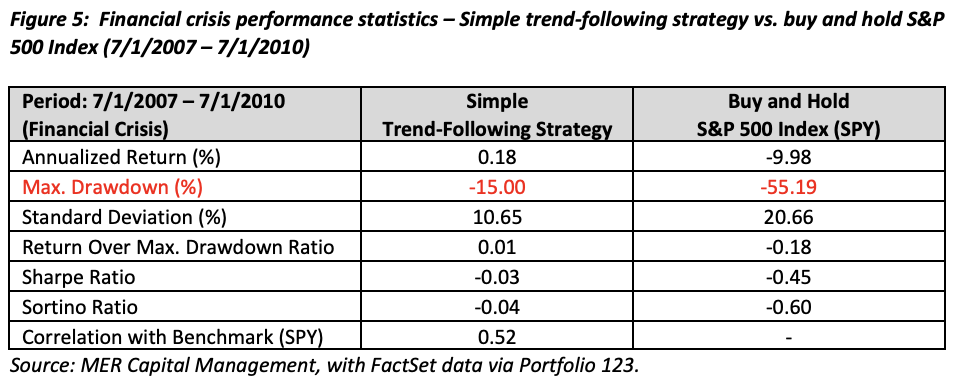

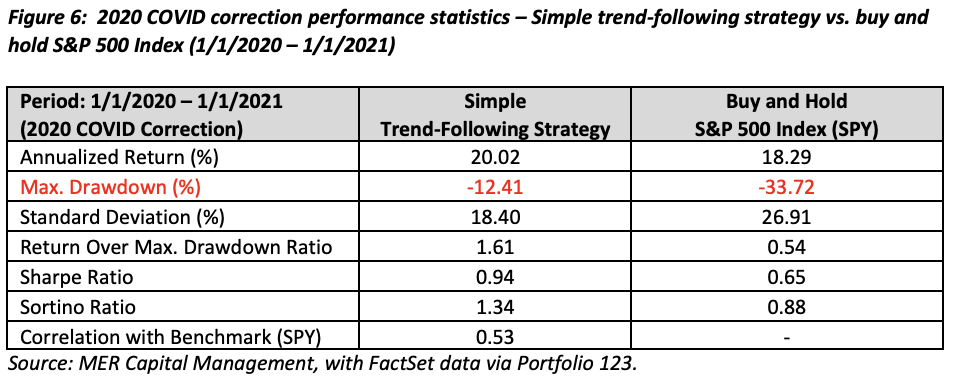

Figures 4-6 provide a more detailed examination of the trend-following strategy’s performance versus the buy-and-hold S&P 500 Index during each of these three crisis periods and their immediate recovery.

As Figures 4-6 show, for each of these three large stock market drawdown periods, the trend-following strategy did its job by protecting the portfolio from experiencing large declines. As a result, the absolute and risk-adjusted returns for the trend-following strategy during each crisis period significantly exceed those of the buy-and-hold S&P 500 Index.

No free lunch

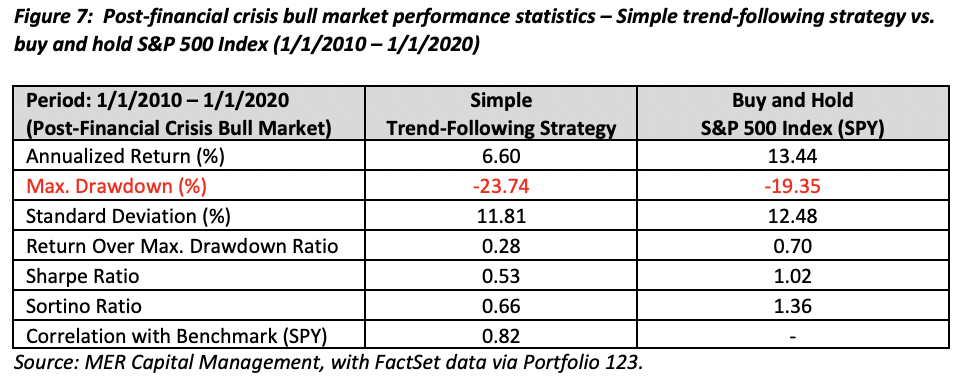

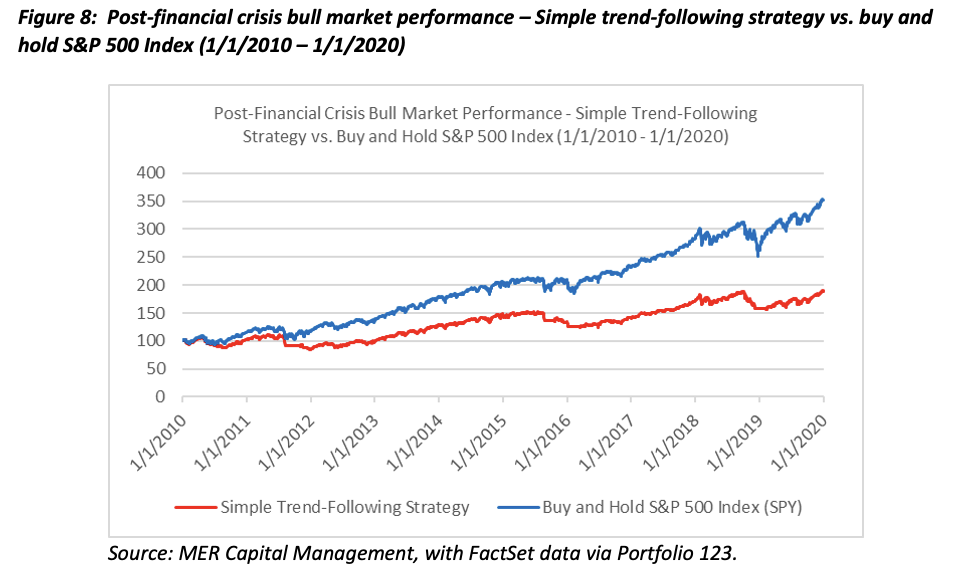

The above data shows a simple trend-following strategy can be remarkably effective in reducing portfolio volatility and losses, leading to significantly better long-term risk-adjusted returns compared to the buy-and-hold benchmark index. However, such performance likely will not always be as strong since, as shown in Figures 7 and 8, trend-following strategies can significantly lag the performance of the buy-and-hold index during protracted bull markets. This underperformance typically is caused by the strategy’s reaction to false positive trend indicators, which prompt the strategy to move to cash when market volatility picks up and short-term market declines are followed by swift rallies.

The good news, however, is that these periods of underperformance occur when the overall market is going up, and the strategy largely makes up for this lower absolute performance by providing the portfolio with better long-term downside protection. Thus, the value associated with a trend-following strategy can be difficult to appreciate when the stock market is on a roll and traditional portfolios are doing well. In this way, the hedging benefits associated with a trend-following strategy are similar to those of an insurance policy, since the true value of each risk mitigation measure is not fully appreciated until a crisis has occurred.

Another drawback associated with trend-following strategies is their lower tax efficiency compared to a buy-and-hold market index investment. This lower tax efficiency is caused by the periodic trades necessitated by the operation of the strategy’s market-timing hedge rule. However, the downside protection associated with a trend-following strategy usually will more than compensate for this higher tax burden. Moreover, this disadvantage can be avoided by holding such a strategy in a tax free or tax deferred account.

Combing multiple trend indicators for better results

Now that I have discussed the pros and cons associated with a simple, single-indicator trend-following strategy, the next question is whether such a strategy can be improved to address the disadvantages previously discussed. Fortunately, the answer is “yes.”

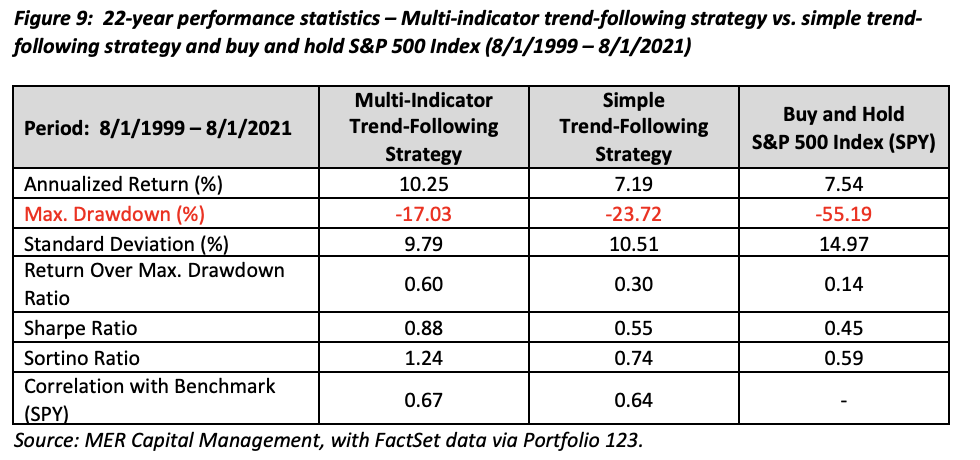

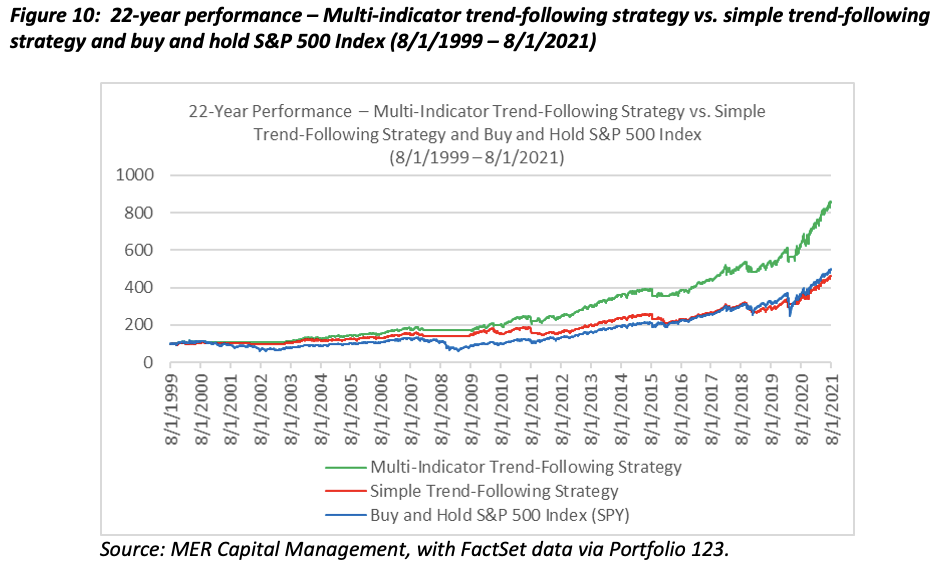

By combining multiple types of trend indicators, we can achieve better absolute and risk-adjusted returns, with greater tax efficiency, compared to the simple trend-following strategy. As shown in Figures 9 and 10, a multi-indicator trend-following strategy that combines long-term and short-term moving average trend indicators with time-series and market volatility indicators, substantially outperforms the simple trend-following strategy and the buy and hold S&P 500 Index on a risk-adjusted basis over the past 22 years. However, the most striking characteristic of the multi-indicator trend-following strategy is that it also significantly outperformed both strategies on an absolute basis (i.e., 10.25% annualized return for the multi-indicator trend-following strategy vs. 7.19% annualized return for the simple trend-following strategy and 7.54% annualized return for the buy and hold index). It also produced this return with significantly lower downside risk (i.e., -17.03% maximum drawdown for the multi-indicator trend-following strategy vs. -23.72% maximum drawdown for the simple trend-following strategy and -55.19% maximum drawdown for the buy and hold index).

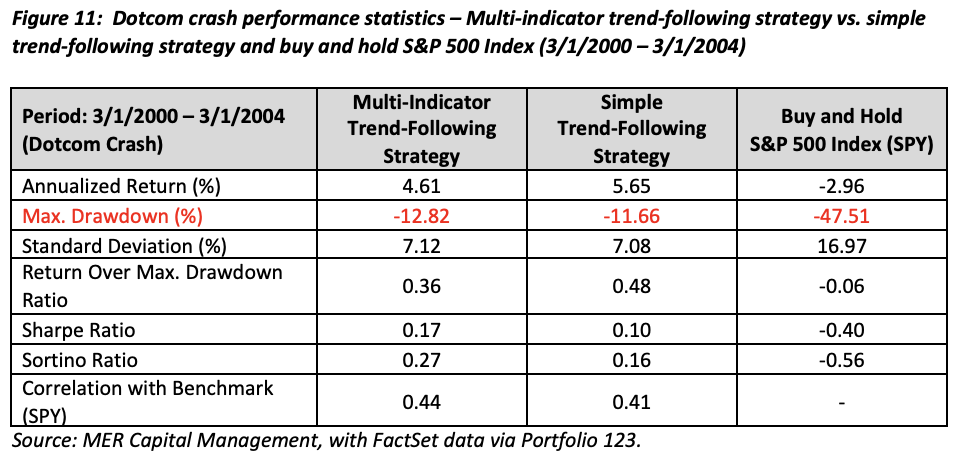

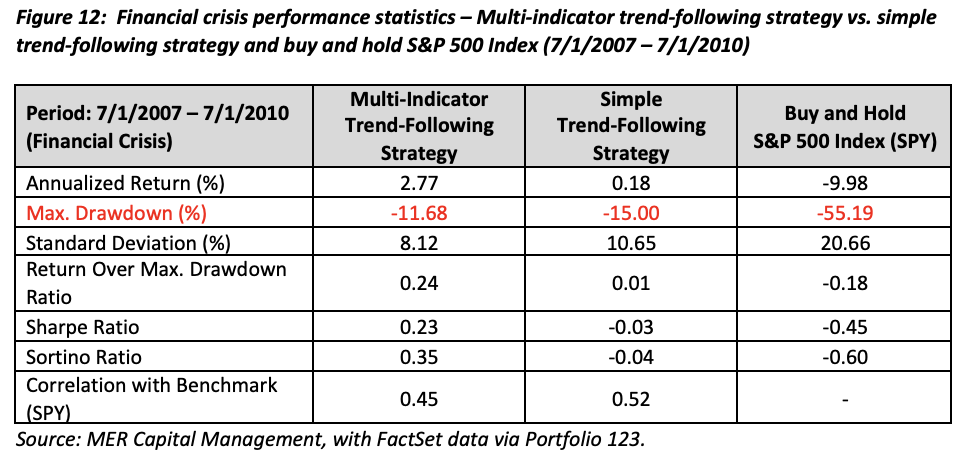

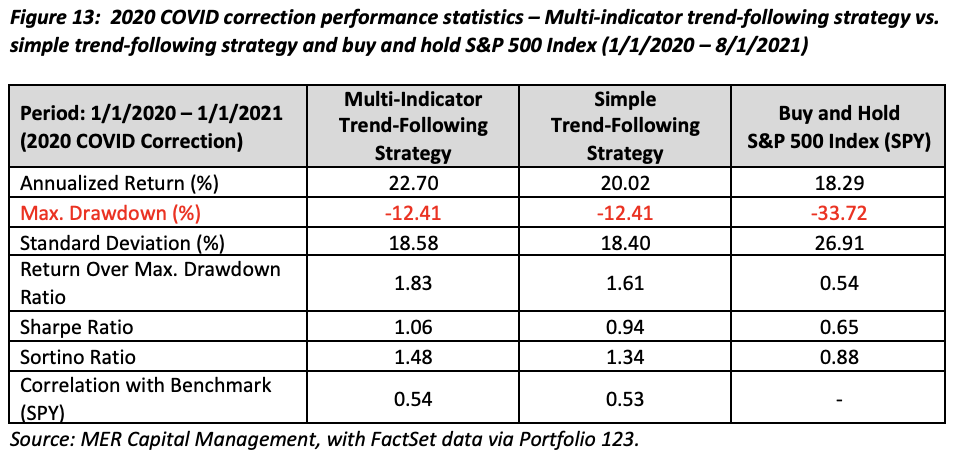

The multi-indicator trend-following strategy also performed well during each of the three most recent market crises. Figures 11-13 show the comparative performance of the multi-indicator trend-following strategy versus the simple trend-following strategy and the buy-and-hold S&P 500 Index during the time periods that include the dotcom crash, the financial crisis and last year’s COVID correction. During both the financial crisis and the 2020 COVID correction periods, the multi-indicator trend-following strategy significantly outperformed both the simple trend-following strategy and the buy-and-hold S&P 500 Index on an absolute and risk-adjusted basis as seen by the multi-indicator strategy’s higher annualized return, lower maximum drawdown and higher return over max. drawdown, and Sharpe and Sortino ratios. Only during the dotcom crash period did the multi-indicator strategy underperform the simple trend-following strategy as seen by its slightly lower annualized return and slightly higher maximum drawdown. However, even during this period, the multi-indicator strategy still significantly outperformed the buy-and-hold market index strategy on an absolute and risk adjusted basis.

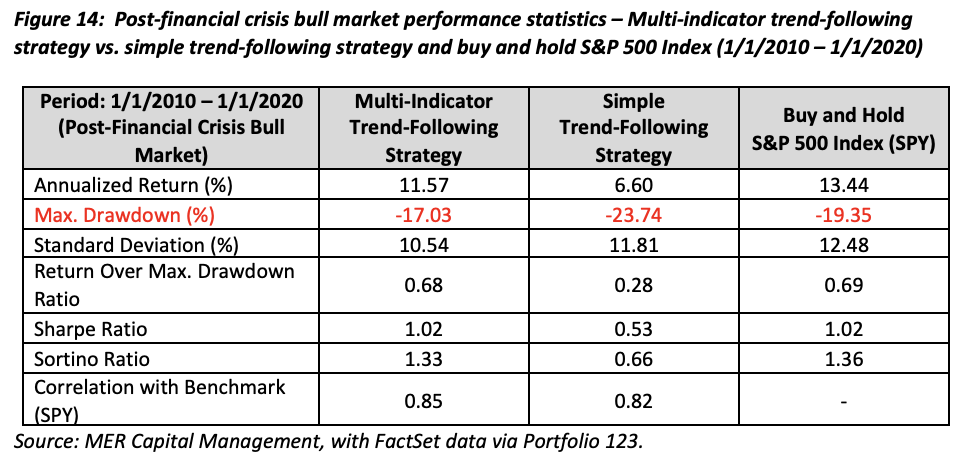

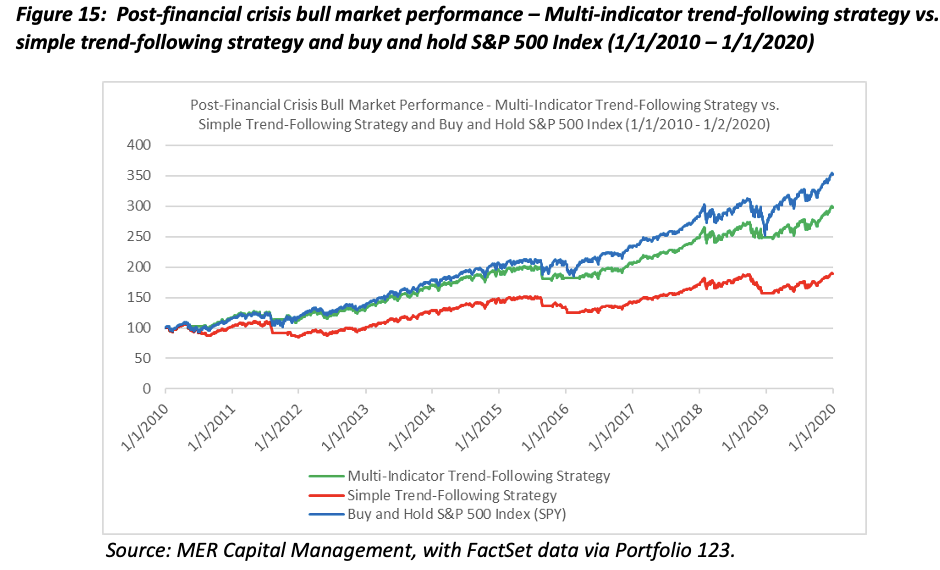

Now let’s see how the multi-indicator trend-following strategy fared during the post-financial crisis bull market. As shown in Figures 14 and 15, the multi-indicator trend-following strategy performed substantially better than the simple trend-following strategy during this up-market period. Its 11.57% annualized return is far greater than that of the 6.60% annualized return for the simple trend-following strategy and significantly closer to the 13.44% annualized return for the buy-and-hold S&P 500 Index. Moreover, it produced this return with a much lower -17.03% maximum drawdown compared to the -23.74% maximum drawdown for the simple trend-following strategy and the -19.35% maximum drawdown for the buy-and-hold S&P 500 Index. As a result, the multi-indicator trend-following strategy generated substantially better absolute and risk-adjusted performance compared to the simple trend-followings strategy and comparable risk-adjusted performance to that of the buy and hold S&P 500 Index during this bull market period.

The above data clearly shows that the multi-indicator trend-following strategy is a major improvement over the simple, single indicator trend-following strategy. This improvement primarily is due to the multi-indicator strategy’s more accurate interpretation of market trends. By looking at more than one trend indicator, the multi-indicator strategy is better able to determine the true direction of the market, and thus, avoid most false positive trends and their associated drag on performance.

The avoidance of false positive market trends also enhances the tax efficiency associated with the multi-indicator trend-following strategy, as seen by its lower number of taxable trades. For example, over the 22-year period from August 1, 1999, through August 1, 2021, the simple trend-following strategy had a total of 25 sell trades compared to only nine sell trades for the multi-indicator trend-following strategy. Therefore, by more accurately measuring the actual market environment, the multi-indicator trend-following strategy achieves greater tax efficiency due to its less frequent trading.

Conclusion

For both individuals and institutional investors, applying a simple, single indicator trend-following strategy as an overlay to a market index ETF investment is an excellent way to obtain meaningful exposure to the overall market with significantly lower downside risk and higher long-term risk-adjusted returns. However, the simplicity associated with a single indicator strategy can cause it to underperform during protracted bull markets. A single indicator strategy also tends to be significantly less tax efficient compared to a buy-and-hold index investment. By modifying a single indicator trend-following strategy to include multiple trend indicators that more accurately assess the actual market environment, an investor can overcome many of the disadvantages associated with a single indicator trend-following strategy, and thus, achieve better long-term absolute and risk-adjusted returns during both up and down markets. Or in other words, . . . more effectively “win by not losing.”3

Key Definitions

Maximum Drawdown means the largest drop from peak to bottom during a certain time period, expressed in percentage from the peak.

Standard Deviation is a statistical measure that shows the historical volatility of an investment’s return. The greater the standard deviation, the greater the volatility.

Return Over Max. Drawdown Ratio is a risk-adjusted performance measure which shows the relationship between an investments’ return and its maximum loss for a specific time period. It divides the average annualized return of an investment by its maximum drawdown. The investment with the highest Return Over Max. Drawdown ratio is deemed to have the best risk-adjusted return (i.e., the highest return per unit of downside risk).

Sharpe Ratio is a measure of an investment’s risk-adjusted performance. It divides the average of an investment’s return by the standard deviation (i.e., volatility) of returns. The investment with the highest Sharpe ratio is deemed to have the best risk-adjusted return.

Sortino Ratio is a measure of an investment’s downside risk-adjusted performance. It divides the average of an investment’s return by the downside standard deviation (i.e., negative volatility) of returns.

Like the Return Over Max Drawdown and Sharpe ratios, the investment with the highest Sortino ratio is deemed to have the best risk-adjusted return. However, this measure of risk-adjusted return typically is considered superior to the Sharpe ratio because it measures an investment’s performance in relation to only its volatility of negative returns or downside volatility.

Correlation with Benchmark is a measure of the statistical similarity of a strategy’s return with that of the market index for a specific time period. The higher the correlation, the more similar the returns. For example, a correlation of 1.0 means that the pattern of historical returns between a strategy and the market index are exactly the same, with a correlation of -1.0 meaning that the pattern of historical returns between a strategy and the market index are exactly opposite. Accordingly, assets that have a low or negative return correlation with each other tend to be good diversifiers.

Mark E. Ricardo, JD, LLM, AAMS®, is president and chief investment officer of MER Capital Management, a quantitative money management firm specializing in providing risk-managed equity portfolios to individuals, institutions, and other investment advisory firms through separately managed accounts and model portfolios. Additional information about Mr. Ricardo and MER Capital Management can be obtained at www.mercapitalmanagement.com. Mr. Ricardo can be contacted at [email protected].

1Both trend-followings strategies described in this article use cash as the hedge asset for simplicity. However, substituting a hedge asset that has a negative correlation with the overall market, such as a government bond fund, can meaningfully enhance the long-term absolute and risk-adjusted returns associated with both types of trend-following strategies.

2All strategy returns are back-tested annualized total returns for the applicable period net of a $5.00 per trade brokerage commission and a 0.05% slippage charge. Actual strategy net returns may be higher than indicated since most market index ETFs can now be traded on a commission free basis.

3Our research has shown that combining a multi-indicator trend-following strategy with a more active form of stock selection, such as a factor-based model, can further improve absolute and risk-adjusted performance compared to merely applying such as strategy to a passive market index ETF. However, a detailed discussion of this topic is beyond the scope of this article.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All