I got my MBA at Kellogg nearly four decades ago and have been teaching investing for the last 20 years. Though not much has changed in the curriculum, over time I’ve realized that some things are downright wrong. Here are the big six.

I got my MBA at Kellogg nearly four decades ago and have been teaching investing for the last 20 years. Though not much has changed in the curriculum, over time I’ve realized that some things are downright wrong. Here are the big six.

1. There is a negative time value of money. A dollar today is worth more than a dollar tomorrow is the simple lesson taught in business school. That, along with the lesson that we want a greater return for taking on more risk are the two most important lessons in finance. They are the basis of developing a discount rate to evaluate investments.

But a dollar in the future is worth less than a dollar today. That’s because real returns for high-quality bonds are negative. With the 10-year Treasury Bond yielding 1.33% as of September 3, 2021, and the Fed target for inflation at 2%, you will likely be able to buy less 10 years from now than more. This is especially true after paying taxes on the interest.

In Germany, the nominal rate is -0.37% annually as of September 3, 2021. In the U.S. and Europe, a dollar today is worth more (not less) than a dollar in the future. A positive real return comes as compensation for taking on more risk, not from the time value of money.

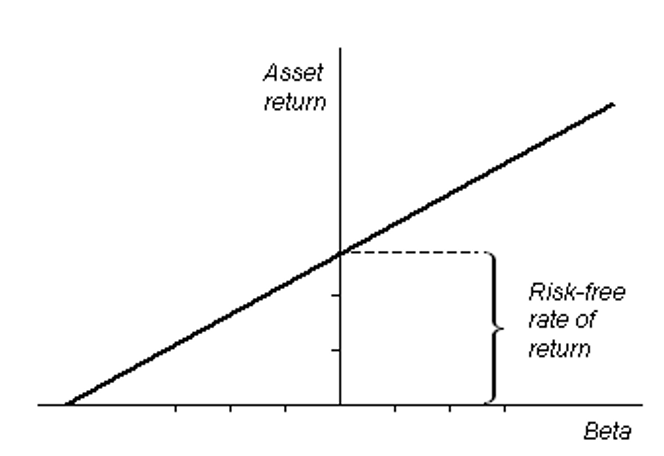

2. There is no risk-free rate. The capital asset pricing model (CAPM) states that the expected return of a stock = risk-free rate + market risk premium x beta of the stock or portfolio. But there is no risk-free rate. As mentioned, a U.S. Treasury bond is yielding 1.35%; after taxes, it is quite a risky investment in the long-run.

In 1997, the government began issuing Treasury Inflation Protected Securities (TIPS), which provide inflation protection. As of September 2, 2021, their annualized yield was a negative 1.03%. That is also guaranteed to lose spending power. In addition, my personal inflation is much higher than the CPI-U, mostly driven by healthcare and healthcare insurance.

3. Microeconomics is wrong. Microeconomics predicts the behavior of individuals and businesses. We all learned the supply and demand curve concepts. If prices drop, people will buy more. This is based upon the belief that people are logical beings who behave consistently to maximize their wealth.

Daniel Kahneman was the first psychologist to win the Nobel Prize in economics to show how false this was, as he helped launched the field of behavioral finance. I completely believed that I was a rational being with consistent opinions and beliefs, who used all available information and was not influenced by the herd. Looking back, I wonder how I could have been that deluded, which Kahneman would say is hindsight bias.

We are emotional beings. When the price of stocks drop, loss-aversion causes us to want to protect what’s left. But my instinct is to sell. I have to push myself to rebalance.

Another example came from a Stanford Business School professor who told me to raise my hourly rate for my financial planning practice, explaining that I’d be busier as the perceived value would be greater. As irrational as this was, he was absolutely right.

4. Macroeconomics is also wrong. Macroeconomics predicts what will happen based upon decisions of governments. The lesson I most remember is that when a government prints more money, and its citizens buy the same quantity of goods and services, inflation will follow. To me this sounded like an obvious conclusion that I certainly never questioned for many years. Yet, in the U.S., we’ve been printing money for a long time with very little inflation until just recently. Japan has been running its printing press even faster for the past three decades and fighting deflation.

How did reality prove macroeconomics wrong? Perhaps because servicing the debt slows down the economy. Or perhaps it’s because we live in a world that is hard to predict.

5. Markets are not always efficient. I selfishly went to business school to get rich by learning how to beat the market. However, Burton Malkiel’s Random Walk Down Wall Street convinced me otherwise. And all of that was before the internet gave everyone virtually equal access to the same information at the same time.

Yet inefficiencies exist in at least two ways. Emotions lead us to chase performance as well as buy high and sell low. By my calculations, a global 60% stock and 40% bond portfolio earned 219.7% from December 31, 1999 to December 31, 2020, but one that simply rebalanced every six months earned 240.1%. Yes, investors are predictably irrational and chase performance. We also chase parts of the market that have been hot as well chasing factors that worked in the past.

The second way markets are inefficient is in fixed income. A Treasury money market is yielding 0.01%, but I have a credit union money market paying 1.0% that is backed by a U.S. agency, the NCUA. A four-year Treasury bond is yielding about 0.62%, though I just opened a four-year CD yielding 2.02%, also backed by the NCUA. The Treasury interest is state tax exempt, but the after-tax difference is still huge. The government creates inefficiencies by giving guarantees that only smaller investors can harness as the insurance limits are meaningless to institutional investors with billions to put in fixed income.

6. You can’t diversify with a few dozen stocks. One stock has a much higher standard deviation than owning 60, yet the standard deviation declines very little afterwards as can be seen by the chart below.

But standard deviation doesn’t mean you’ll get the same return. Because long-run market returns are driven by a relatively small number of stocks, one must own hundreds or thousands of companies. Even owning 100 companies only gives a 44.7% chance of earning the total market returns. You Increase the odds of getting the market return by owning everything. Though that was virtually impossible decades ago, it is now child’s play with total stock index funds.