Owning a large number of stocks reduces risk. Less widely known is that it also increases expected returns.

There is a tendency to think that owning a handful of stocks may be a bit riskier but have an equal likelihood of outperforming the market as a whole. This is wrong for two reasons:

- Higher standard deviations lead to lower returns; and

- A portfolio that is smaller but has a standard deviation equal to the market’s is still expected to underperform the market.

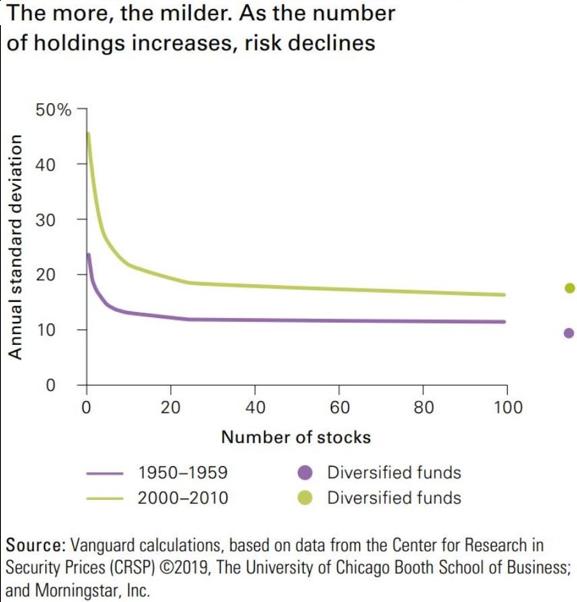

A recent Vanguard paper, What’s a Mutual Fund Worth?, demonstrated that U.S. stocks are more volatile than in the past. The authors (Andrew Clarke, Michael Nolan, and Tyrone Sampson) showed a portfolio of one stock has an annualized standard deviation of 45.3%, while 100 stocks reduce the standard deviation to 16.3%. Yet the investor is not compensated for diversifiable (idiosyncratic) risk, as we know.

Lower standard deviations can equate to higher returns

That lower standard deviation can increase returns is less well known. To explain this simply, a stock that increases 30% in one year and declines by 10% in the second year has a 10% simple average annual return but a geometric return of only 8.17%. A portfolio that increases 10% each year for two years also has a 10% simple average annual return but a higher 10% geometric. What this means is that lower standard deviations lead to geometric returns much closer to the arithmetic returns. In the first case, a $10,000 investment grew by $1,700 while in the second gained $2,100.

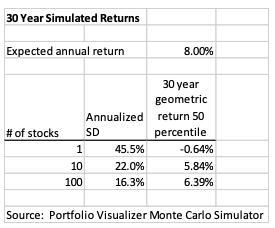

Let’s simulate 30 years of returns using Portfolio Visualizer’s Monte Carlo Simulation tool, with standard deviations calculated by Vanguard using data from CRSP and Morningstar. Further, let’s assume that any stock has an expected 8% return in any one year. This is the arithmetic return.

In the results below, a portfolio of 100 stocks has an expected long-run annualized geometric return of 6.39% but one stock has an expected loss of 0.64% annually. Ten stocks reduce the standard deviation significantly but still produce a long-run geometric return 0.55 percentage points less than the 100-stock portfolio.

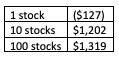

Over a two-year period with a $10,000 investment this translates to the following gains:

Over 30 years, the differences are far more dramatic. But, don’t generalize this math into a belief that lower standard deviation portfolios, such as minimum-volatility funds, reduce risk and increase returns. That is not necessarily true.

Standard deviation is an imperfect measure of risk

Portfolios of more than 30-50 positions essentially have the same standard deviations. One doesn’t significantly reduce standard deviation by having thousands of stocks. This leads to the perception that having too many stocks is “overdiversified” and doesn’t decrease risk. Reality trumps perception, however, as it does decrease risk, even with the same standard deviation.

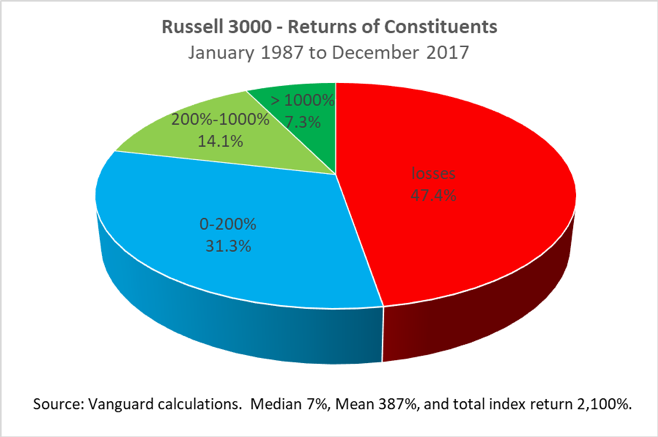

To understand this point, let’s look at what a typical stock in the Russell 3000 earned between 1987 and 2017. This is a surrogate for the U.S. stock market, excluding microcap companies. According to a Vanguard paper in The Journal of Investing, the return of the median stock was 7% or a tiny 0.22% annually, including dividends. This means half of the constituents did better and half worse. So, more than half underperformed a Treasury Bill. The mean return was 387% or 5.24% annually.

The paper, How to Increase the Odds of Owning the Few Stocks that Drive Returns, also estimated the probabilities of randomly selected portfolios besting the return of the market. The authors, Chris Tidmore, Francis Kinniry, Giulio Renzi-Ricci, and Edoardo Cilla, examine the returns of the individual stocks of the Russell 3000. They found that 47.4% of those individual stocks had negative returns over the 31-year period with some having a negative 100% return. The return of the Russell 3000 was driven by about 7.3% of those stocks that delivered a return greater than 1,000%. In fact, the total return of the Russell 3,000 was 2,100% or 10.48% annually. Miss out on some of those relatively few high flyers and portfolio returns are far lower.

While the standard deviation of a 30-stock portfolio may not be significantly higher than the entire market, the study shows that the probability of it earning the market return is only 40.3% and the average expected shortfall is about 0.4% annually. Even at 500 stocks, there is only about a 48.4% probability of getting the return of the entire market. Tracking error averages 8.2% with 30 stocks and 1.8% with 500 stocks.

My take

I agree with Mark Twain that, “there are lies, damned lies, and statistics.” A portfolio of a few dozen stocks may have virtually the same standard deviation as the market and even a near perfect positive correlation, but have dramatically different and typically lower returns. Those lower returns are real money in our clients’ pockets and will have a dramatic impact on their financial goals. Telling your clients that they had the same market standard deviation and correlation won’t be very satisfying if they have underperformed the market and have to push back financial independence.

Owning the entire market is consistent with modern portfolio theory (MPT). Doing so increases the odds of getting the market return and is, in no way, overdiversified. Beyond theory, since expenses and taxes are real, stick to broad, low-cost index funds that don’t push through capital gains. I’ve never been a fan of factor investing. Market-cap weighted index funds like the iShares Core S&P Total U.S. Stock Market ETF (ITOT) or the Vanguard Total Stock Market ETF (VTI) fit the bill just fine. And this math works for international stocks as well.

I embrace dumb beta — getting the entire market return without taking on more risk than necessary.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisor. He has been working in the investment world with 25 years of corporate finance. Allan has served as corporate finance officer of two multi-billion dollar companies, and consulted with many others while at McKinsey & Company.

Read more articles by Allan Roth