The motivation for a transaction tax is rooted in the belief that high-speed traders profit at the expense of the “little guy” – anyone from a Robinhood investor to an advisor acting on behalf of a client. A new book provides an excellent education on high-frequency trading that can help us to evaluate that proposition.

The motivation for a transaction tax is rooted in the belief that high-speed traders profit at the expense of the “little guy” – anyone from a Robinhood investor to an advisor acting on behalf of a client. A new book provides an excellent education on high-frequency trading that can help us to evaluate that proposition.

Donald MacKenzie, a professor of sociology at the University of Edinburgh, has produced a prolific body of literature on the study of finance. His contributions are not, however, so much in what we would think of as sociology as in the study of the political economy of finance.1 By studying finance from this angle, he becomes a “fly on the wall,” observing and chronicling the history and application of developments in finance such as the option-pricing model and high-frequency trading. One significant result is that he delivers a clearer picture of these developments than you could get in any other way – even, perhaps, by being a direct participant in them. This extends to his explanations of the mathematics of modern financial theory, which are as crisp and clear and free of unnecessary complications as any I have seen (MacKenzie has an undergraduate degree in mathematics).

“An engine, not a camera”

I first became intimately familiar with MacKenzie’s work very belatedly, by reading his book “An Engine, Not a Camera” only last year, in 2020. I had heard about it and read reviews when it was published in 2006 but never read it.

I was stunned. It had an amazing number of crossovers with experiences I had had in the field, even though I have deliberately kept mostly on the periphery of the field of finance. For example, when I started reading in the book about the Chicago Board Options Exchange’s trading floor in the early 1970s when options started trading, I flashed back to an afternoon’s experience I had in 1973 or 1974 watching at the invitation of a friend at that time, Joe Doherty, who spent his days trading on that floor. I then turned the page of the book – and there was Joe Doherty, being quoted from a MacKenzie interview with him.

MacKenzie provided outstanding coverage of the October 19, 1987 stock market crash, which was in large part precipitated by the too-successful marketing of “portfolio insurance” by the firm Leland O’Brien Rubinstein. (I played a subsidiary role as a consultant on the mathematics to LOR.) For example, having contrasted “mild” randomness as that which “could be treated by standard statistical techniques” (i.e. assuming standard Brownian motion) with “wild” randomness as that which was “not susceptible to those techniques” (i.e. involving Mandelbrotian/Lévy “fat-tailed” distributions or discontinuous jumps), MacKenzie then pronounces as follows, with keen insight, on both the portfolio insurance and Long Term Capital Management disasters: “In both 1987 and 1998, practical action involving models that incorporated the assumption that randomness is ‘mild’ may thus have helped to generate ‘wild’ randomness.”

Not to over-elaborate MacKenzie’s lapidary and important inference, here is an explanation. LOR’s practice of “replicating” a put option by using stock market index futures required assuming that prices moved continuously, as in a Brownian motion model of the stock market. But it failed when prices took wildly discontinuous jumps, a result that was caused by too many market participants using portfolio insurance and other automated trading rules.

When I read the book, I decided I wanted to interview MacKenzie and write about it. But he was in the process of putting the finishing touches on a new book, on high-frequency trading (HFT), and put off an interview until after completing that.

I decided to review his new book instead.

Trading at the Speed of Light

There are fewer crossovers to my own experience in his book on high-frequency trading, Trading at the Speed of Light, than there were in An Engine, Not a Camera – but that meant that I learned more from it.

MacKenzie comes from an academic discipline, sociology, and writes for it. That means his writing is couched to a certain extent in a slightly jargonized language. This does not get in the way, though it tends at times to flatten the prose a bit.

Trading at the Speed of Light is about the history and practice of automated trading, culminating in the computer-driven high-frequency trading that now comprises half of all stock market trades, and was the subject of Michael Lewis’s best-selling 2015 book Flash Boys as well as Scott Patterson’s earlier book Dark Pools, which I reviewed in 2012.

MacKenzie spends a large part of the book relating the history of trading in stocks, options, futures, sovereign bonds, and currencies, and the politics of the gradual transition from the person-to-person and dealer-client trading models to computerized trading. For some of these securities, such as stocks and options, the trading transformed almost completely from person-to-person in the early 1970s to computer-to-computer in the present day.

MacKenzie’s account of the floor trading on the CBOE in the early 1970s is hilarious. Traders were packed in so tightly that sometimes they were squeezed between other traders and their feet didn’t touch the floor. They had to suffer spittle from shouting traders next to them.

Being tall was an advantage because you could yell or gesture over the heads of your neighbors. To rise above them, some traders took to wearing elevated shoes. But finally, MacKenzie says, the exchange “had to impose a limit on the extent to which traders could add to their bodily height by wearing platform heels.”

One interesting story in the book – an example of its mission as a study of the political economy of finance – relates to how Leo Melamed, then-chair of the Chicago Mercantile Exchange, won approval for financial futures trading even though it was perceived as gambling, which was illegal in Illinois where the CME was headquartered. This was achieved by using the political process to establish a new regulator, the Commodity Futures Trading Commission (CFTC), which would have jurisdiction over financial futures and thus legitimize them. At one point, the Securities and Exchange Commission (the SEC) was offered the oversight function instead, but its commissioners declined it, with comments such as, “Why would we mess around with pork bellies?”

Thus, as a result of an ill-considered offhand comment, was an enormous securities market born.

The high-frequency trading game

My greatest interest in the book was engaged by Chapter 6, “How HFT Algorithms Interact, and How Exchanges Seek to Influence It.” Anyone who wants to know the basics of HFT should read this chapter. MacKenzie conducted 358 interviews with 337 people – high-frequency traders, exchange staff, etc. – mostly in Chicago, New York, Amsterdam and London, over a period of 10 years. He admits to not understanding much of what he heard at the beginning, but he went back over and over to interview again the same or different people until it became clear to him.

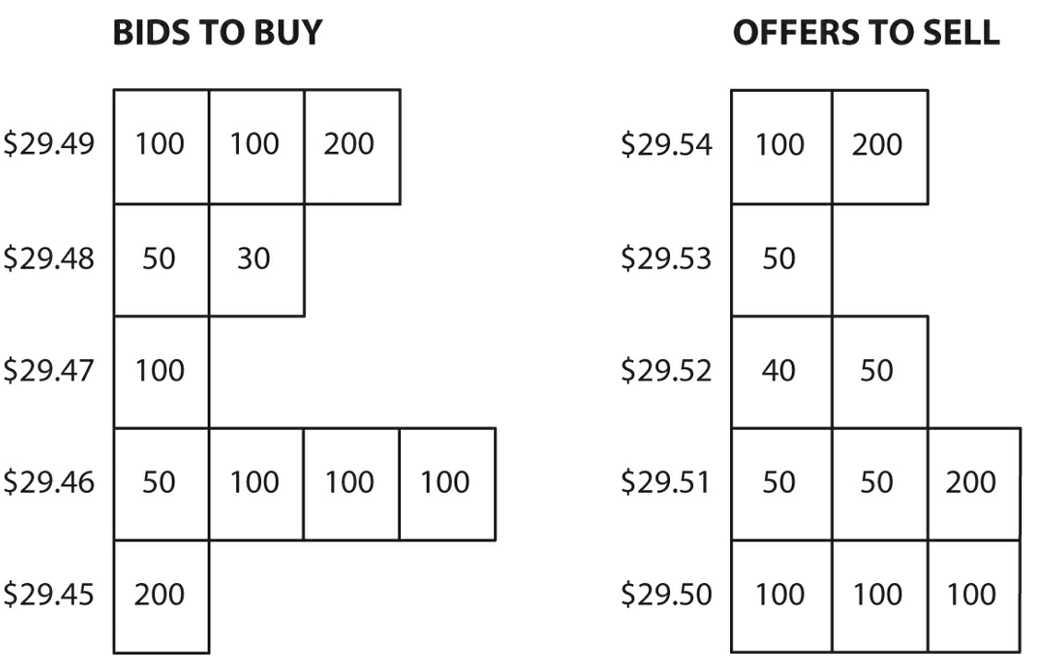

The trading game is determined by a deceptively simple layout, as depicted by MacKenzie below.

In this depiction of an order book, there are three bids to buy (a security) at $29.49, in lots of 100, 100, and 200; two “asks” offering to sell at $29.54; and so on.

Deceptively simple, and yet it leads to such complications.

Michael Lewis’s book brought to everyone’s attention the fact that the HFT industry will go to extraordinary lengths and expense to try to reduce by milliseconds the length of time it takes for an order to be executed.

One simple example of a HFT practice, called “quote matching,” shows why.

Quote matching is believed to work well when the “tick size” between bid or ask (offer) prices is small. The tick size is the minimum price difference allowed on the exchange between neighboring bid or ask prices.

Suppose the highest bid to buy a share of a security is $30. A quote matcher might place a bid at $30.01, making it likely that the bid would be executed before the $30 bid.

The principle is that if the price of the share goes up, the quote matcher will have made a profit. But if the price goes down then the quote matcher can limit her loss to a single cent by immediately accepting the $30 bid.

If, that is, the $30 bid still exists.

If the $30 bidder is on her toes – or rather, her computer is – it won’t exist anymore. It will have been canceled because the market price of the security went down, so it has become a “stale” bid at too high a price. This can all happen almost instantaneously.

The result is a cat-and-mouse game between high-frequency traders who try a gambit like quote matching, and other high-frequency traders who cancel their placed orders in the nick of time.

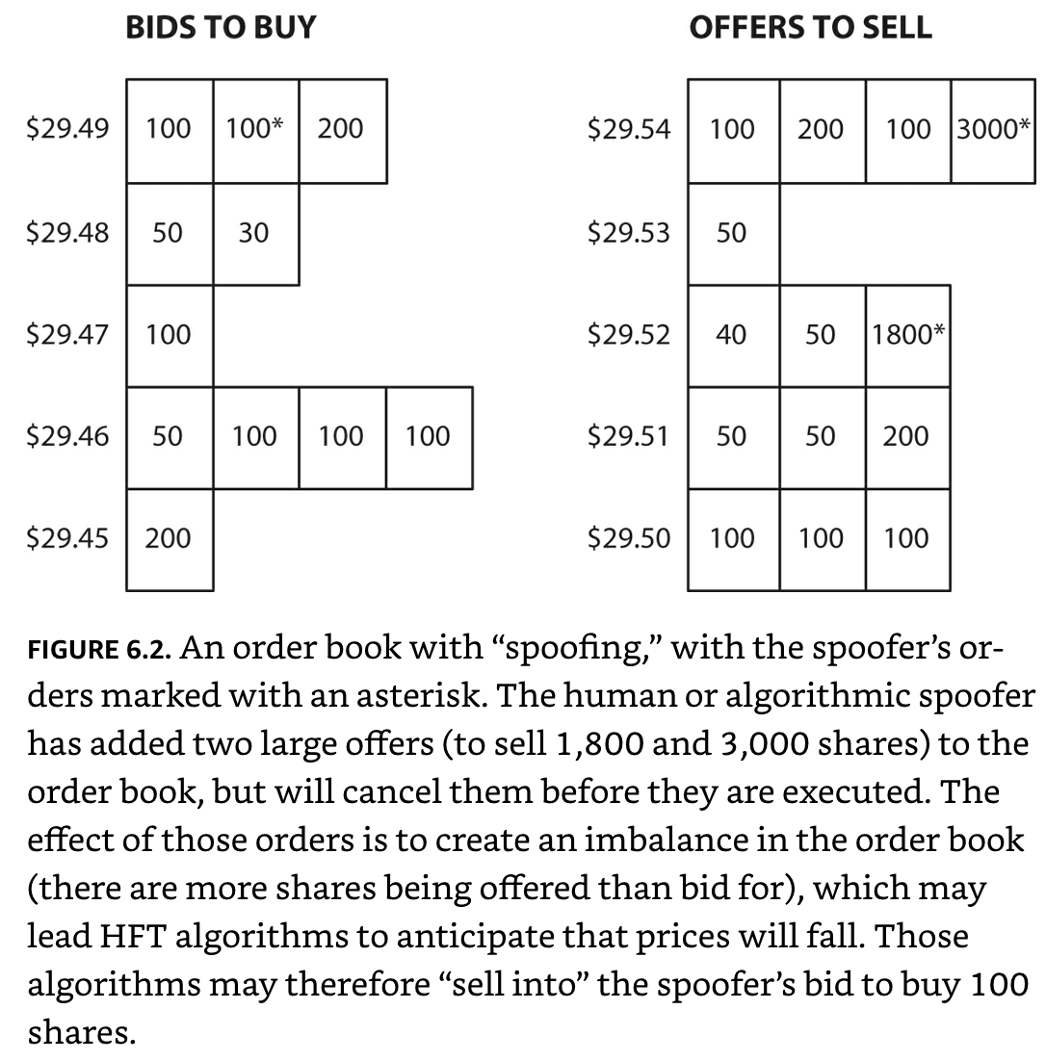

Another example of a high-frequency trading gambit is “spoofing.” Regulators and exchanges look askance at spoofing and sometimes ban it, perhaps because it is considered a form of market manipulation.

The premise of spoofing is that if there are many more offers to buy than to sell, that is evidence that the price of the security is likely to rise; and conversely, if there are many more offers to sell than to buy, that is evidence that the price of the security is likely to fall.

A spoofer who wants to buy at a good price may “stack the order book” to make it look like the price of the security is going to fall. The picture below shows MacKenzie’s example of spoofing, along with his explanation of it.

The spoofer has temporarily (on the order of milliseconds) tilted the order book toward sellers to make it look like the price is going to fall but does not seriously intend to get those orders filled. (Bidders and askers, incidentally, are anonymous; they don’t reveal who the offerer is.) The impression created that the price will fall drives the seller into the arms of the spoofer’s bid to buy 100 shares at a price that the spoofer believes is advantageous.

The professional traders are divided between “makers” and “takers.” “Market makers” operate by posting both a bid price and an ask price that is slightly higher, bracketing the price at which they think a “fair trade” would execute. “Takers” simply accept a posted price, either because their price prediction algorithms suggest it is a good price or because the price is “stale” – that is, the market has moved against it but its poster has inadvertently failed to cancel it.

The focus of MacKenzie’s study is on the high-frequency traders themselves and their interactions with each other. Among them it is a zero-sum game, like a poker game. If the game included only the high-frequency traders then they would not earn a profit in aggregate, in fact they would lose due to their high expenses. Many of them in fact, perhaps most of them, don’t make money, as MacKenzie points out, because their expenses for brokerage, exchange and clearing fees and technology and communications links exceed their gains.

MacKenzie focuses less on the “fish” in this game – the unsophisticated traders, and those who trade merely because their business requires them to2; in other words, the Robinhood-type day traders and active institutional money managers. To the extent that the high-frequency traders make a profit in aggregate these traders must be the source of their profit. But it is difficult to estimate how much. I would like to see MacKenzie do an additional study focusing on this question. There are, of course, academic studies of such questions in finance journals but MacKenzie would do a better job of it.

Does high-frequency trading increase liquidity and decrease transaction costs?

I have written several articles defending proposed financial transaction taxes against what I perceive to be wrongheaded and cynical criticisms.3 One criticism is so transparently cynical that it is hard to believe anyone would accept it: that a financial transaction tax (FTT) mostly hurts “the little guy.”

But there is another criticism that is harder to grapple with: that the practice of HFT, which a FTT would curtail, makes markets more liquid and thus reduces transaction costs.

MacKenzie’s stated mission does not include assessing the social value of HFT. The only place in the book where such a consideration is touched on is where MacKenzie cites the work of French economist Thomas Philippon, who showed that in spite of all the technological developments the efficiency of financial intermediation has not increased since the 1880s.

Does HFT increase liquidity? Well yes, in the sense that it increases the number of transactions and therefore increases the likelihood that one’s order will be filled quickly.

Nevertheless, one quote in MacKenzie’s book casts a modicum of doubt on this. In noting that there are critics of quote matching and other algorithms, MacKenzie says, “Bids and offers, these critics alleged, ‘can disappear as quickly as they emerge, making market liquidity illusory.’”

But even if we were to concede that HFT increases “liquidity” – a vaguely-defined concept – does it reduce transaction costs?

That is much more iffy. Philippon’s work is one piece of evidence that it has not done so.

HFT does reduce the bid-ask spread since there are so many more bids and asks at any one time. But does this necessarily mean that the transaction cost to the ordinary (non-HFT) market participant is lowered? There are millions of shares traded a day in the U.S. stock market. Would transaction cost be lowered still more for the ordinary market participant if high-frequency traders traded trillions of shares a day instead of millions? This is unlikely.

I have seen widely-quoted journal articles that simply assume the transaction cost is half the bid-ask spread. The assumption is apparently that this is the profit that the market maker realizes, on average. But there is no good reason for that assumption. When one leg of a bid-ask spread executes, the other leg is unlikely to execute simultaneously – in fact, market makers usually have to change the other leg’s price (even at a loss) to make it more likely to be executed, because the market has moved since the first was executed. Like so many assumptions made in the field of academic finance, this one rests on infirm soil.

MacKenzie illustrates that HFT is a good and challenging game for a small number of eager participants (and their algorithms). But since it is not clear that it provides a benefit to anyone outside of those avid players, there is no reason to favor or exempt it from taxation.

Economist and mathematician Michael Edesess is adjunct associate professor and visiting faculty at the Hong Kong University of Science and Technology, chief investment strategist of Compendium Finance, adviser to mobile financial planning software company Plynty, managing partner and special advisor at M1K LLC, and a research associate of the Edhec-Risk Institute. In 2007, he authored a book about the investment services industry titled The Big Investment Lie, published by Berrett-Koehler. His new book, The Three Simple Rules of Investing, co-authored with Kwok L. Tsui, Carol Fabbri and George Peacock, was published by Berrett-Koehler in June 2014.

1 Britannica defines political economy as the branch of social science that studies the relationships between individuals and society and between markets and the state.

2 A “fish” in a poker game is someone who can’t resist playing but is an inveterate loser.

3 https://www.marketwatch.com/story/heres-a-better-way-than-gamestop-attacks-for-the-little-guy-to-stick-it-to-wall-street-11612765598, https://www.marketwatch.com/story/vanguard-opposes-this-wall-street-tax-its-founder-john-bogle-favored-and-that-says-a-lot-about-mutual-funds-today-2020-09-03, https://www.marketwatch.com/story/how-fund-giant-vanguard-is-misleading-investors-about-a-proposed-tax-on-stock-trades-2020-01-16, https://www.bloomberg.com/opinion/articles/2019-06-20/the-case-for-a-financial-transaction-tax, https://www.marketwatch.com/story/why-a-wall-street-tax-would-have-little-impact-on-main-street-investors-2019-04-01

Read more articles by Michael Edesess

The motivation for a transaction tax is rooted in the belief that high-speed traders profit at the expense of the “little guy” – anyone from a Robinhood investor to an advisor acting on behalf of a client. A new book provides an excellent education on high-frequency trading that can help us to evaluate that proposition.

The motivation for a transaction tax is rooted in the belief that high-speed traders profit at the expense of the “little guy” – anyone from a Robinhood investor to an advisor acting on behalf of a client. A new book provides an excellent education on high-frequency trading that can help us to evaluate that proposition.