Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In our 2019 book, Return of the Active Manager, Jason Voss and I declared that active equity management was alive and well in spite of the movement to index investing. We provided numerous suggestions to improve the evaluation of investment opportunities as well as manage equity portfolios, from the perspective of behavioral finance.

Little did we know that a golden era of active equity management would commence shortly after our book was published.

Active versus passive

This article is an update of my 2020 Advisor Perspectives article, The Dawn of a New Active Equity Era. In that article, I discussed the surprisingly positive impact of the active to passive flows on the prospects for active equity outperformance. The flows out of closet indexers and into true indexers is creating an attractive active equity environment. I will not repeat the evidence supporting this argument.

Active equity opportunity

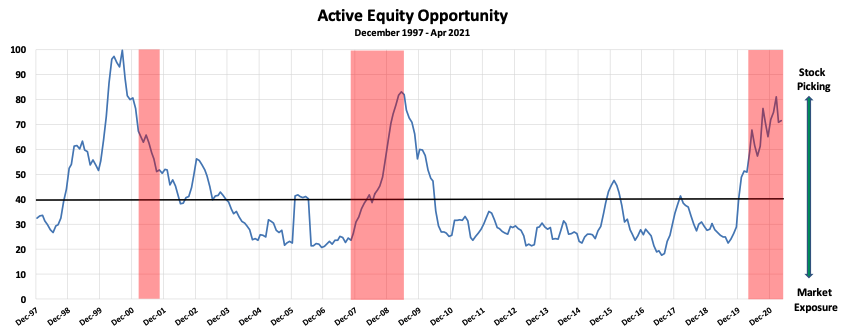

In the previous article, I described a measure, dubbed active equity opportunity (AEO), which reveals how favorable markets are for stock picking. Markets characterized by high individual stock dispersion and high positive skewness, high market volatility, and small cap outperforming large cap set the stage for stock picking success. Active equity managers prefer a higher AEO since it indicates their high-conviction picks are more likely to outperform. On the other hand, a low AEO implies that even the most talented managers will struggle to beat their benchmark.

The figure below shows AEO from 1997 through last month. A value above 40 signals a favorable stock picking environment, while it is less favorable when it is below 40. As has been extensively reported, 2011–2019 was a bad stretch for active equity. Over those nine years, AEO was mostly below average, reaching a low of 18 in mid-2017. Anna Helen von Reibnitz, in a study going back nearly 50 years, found that mid-2017 return dispersion was the lowest in a half century. For those nine years, stock pickers faced strong headwinds, which in part explains passive’s growth at active’s expense.

Since late 2019, however, AEO has spiked and is now at twice its average. The red-shaded areas in the figure represent National Bureau of Economic Research (NBER) recessions. The U.S. is currently in a recession, until NBER says otherwise, that is accompanied by high AEOs. This combination of high AEO and recession represents an ideal situation for stock pickers.

Sources: Morningstar and AthenaInvest

Empirical evidence demonstrating the compelling opportunity

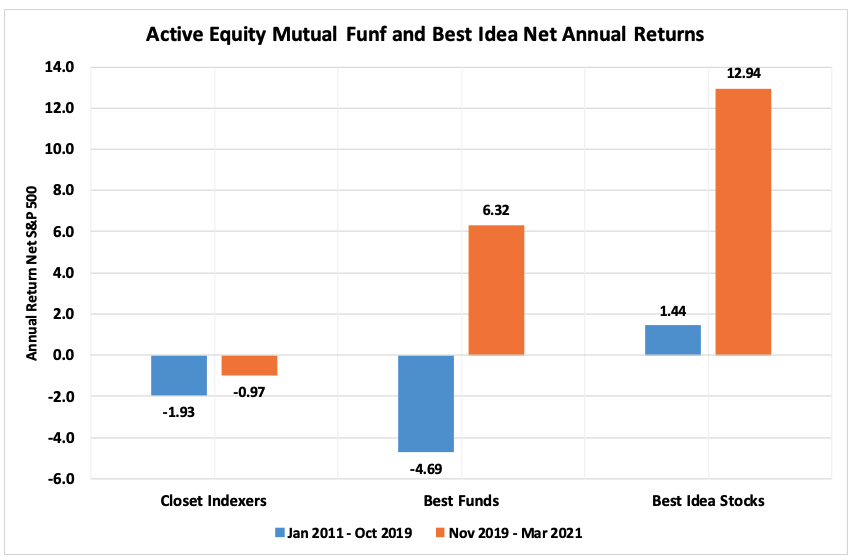

How have active mutual funds fared since late 2019 as AEO increased dramatically, accompanied by the pandemic driven recession? The annual returns, net of S&P 500 returns, for closet indexers and best active equity funds, along with the returns for best idea or high-conviction stocks are presented below.

Sources: Morningstar and AthenaInvest

My firm, AthenaInvest, assigns a fund to one of 10 strategy groupings based on its self-declared strategy. The best funds in each strategy, those pursuing a narrowly defined equity strategy while focusing on their best-idea stocks,

are determined each month using objective measures of strategy consistency and high-conviction equity holdings. These measures are not past performance-based but are gauges of fund manager behavior

The reported annual returns are derived from a simple average of the 200 or so best-fund subsequent-month net returns for each time period. Closet index returns are calculated in a similar manner. Best idea stocks are those most held by the best funds. Each month features between 250 and 300 best-idea stocks.

Monthly compounded annual best idea stock returns are calculated using a simple average of the subsequent monthly stock returns. This means that a small number of large-cap stocks – the FAANGS, for example – do not disproportionately influence reported returns. In fact, small stocks generally make up half of the best idea universe.

As the preceding figure shows, both closet indexers and best funds underperformed the S&P 500 from 2011 through late 2019. Best-idea stocks slightly outperformed, but if typical mutual fund fees are deducted, they generated returns comparable to the S&P 500. So, if an active equity fund had focused exclusively on best-idea stocks during this period, it would have matched the market return. Thus, even the best funds must hold low-conviction stocks along with their high-conviction counterparts.

The earlier period, during which AEO was well below its average value, shows how difficult it is for active equity funds to outperform in such markets. A high-AEO environment, however, in which emotional investing crowds are pushing stocks away from their fundamental value, sets the stage for stock-picking success.

The November 2019 to March 2021 period, when AEO was well above average, demonstrates this. Again, closet indexers underperformed the market roughly by their fees, as to be expected. Yet both best funds and best-idea stocks eclipsed the S&P 500 on an annual basis by 6.32% and 12.94%, respectively, as AEO reached levels not seen since 2009. Best-idea stocks outperformed best funds by a stunning 6.62% annually, which offers further evidence that best funds hold many low-conviction stocks.

This recent performance shines a light on the extraordinary skill of active equity managers when market conditions favor stock picking.

The home run derby is here

Since late 2019, market conditions have turned favorable for active equity funds. Individual-stock dispersion and positive skewness, market volatility, and the small-firm premium have all increased in recent months. Stock pickers have the opportunity to demonstrate their skill.

Given the scale of recent economic and market disruptions, we can expect heightened uncertainty for some time. This makes determining a stock’s fundamental value a challenge that favors expert, heavily resourced professional equity teams.

The current high-AEO period is driven by the increased trading activity of emotional crowds pushing stock prices away from fundamental values. The GameStop short squeeze frenzy was the most visible example of these market-roiling trades. This stock picking opportunity could stretch many months into the future. Professional managers and investors should embrace this opportunity for as long as it lasts.

C. Thomas Howard is emeritus professor of finance at the University of Denver and CEO and chief investment officer at AthenaInvest, Inc.

Read more articles by C. Thomas Howard