Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In my previous article, I showed how the value of tax-advantaged accounts depends on the tax-free investment income earned in those accounts. This article digs deeper into this dynamic to further demonstrate why the conventional wisdom of “stocks in taxable, bonds in tax advantaged” is not reliable. Compounding of tax-free investment income, protecting against tax policy changes, and avoiding taxes on inflation are all potential reasons for holding stocks in tax-advantaged accounts.

To reiterate from my prior article, the value of the tax benefit is the difference between the tax-advantaged accumulation and a (counterfactual) accumulation in a taxable account

where r is the periodic return, n the number of periods, and tc, td, and ti are the tax rates on contributions, distributions, and investment income, respectively.

where r is the periodic return, n the number of periods, and tc, td, and ti are the tax rates on contributions, distributions, and investment income, respectively.

While the tax rates on contributions and distributions are as of a point in time, the effective tax on investment income is spread over the investment period. It may be levied yearly on income distributions, at the time of sale as a capital gains tax, or as a combination of the two.

Estimating ti, which we can also think of as the annualized tax drag, involves lots of assumptions. In addition to future tax rates, the magnitude of the return, timing of the tax (annual or at sale), and length of the investment period are critical.

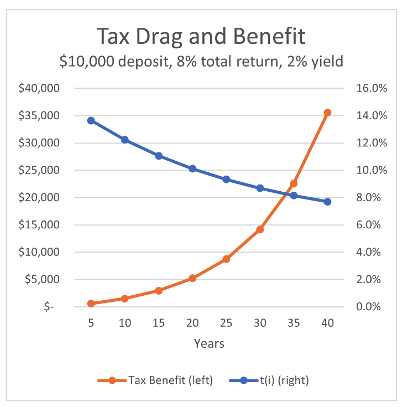

Figure 1 illustrates these factors. I am assuming pretax funds of $10,000. For the remainder of the discussion, the ordinary tax rates, tc, and td, are set at 20%, making us indifferent to a traditional vs Roth contribution. The tax benefit thus varies only with ti. I assume an 8% total return and a 2% dividend yield. I assume that in a taxable account both dividends and capital gains would be taxed at 15%. However, because capital gains are only taxed at the end of the period, ti declines over time. After 30 years it has dropped from the initial 15% to 8.7%.

That is not the whole story, however. While the annualized tax drag is lower, the total tax benefit has grown dramatically. In other words, savings from even a small ti compounded over many years can result in a significant tax benefit. In this example the benefit accounts for over 17% of the total accumulation after 30 years.

The implication of this dynamic is that the conventional wisdom of “stocks in taxable, bonds in tax-advantaged” may break down over long periods. There are at least three reasons to consider stocks in tax advantaged accounts.

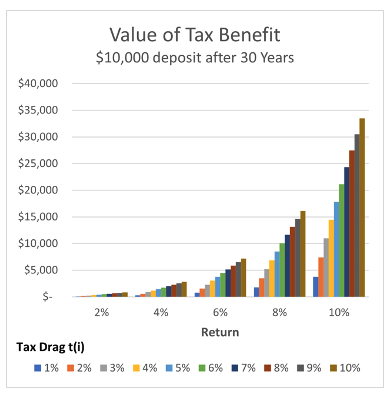

As the example above shows, a small, annualized tax drag can nevertheless result in a large benefit. Figure 2 shows the rapid increase in the tax benefit as the return and ti increases.

To make this concrete, say you have a 30-year horizon and a choice between placing one of two portfolios in a tax advantaged account: a) the above stock portfolio with an 8.7% annual tax drag; or b) a bond portfolio yielding 4% subject to 50% tax. Which should you choose? At first blush you might think that saving 2% (4% return times 50% tax rate) a year is preferable to saving 0.7% a year (8% return times 8.7% tax rate). It turns out, however, that the tax benefit of the stock portfolio after 30 years exceeds that of the bond portfolio by almost 24%. The reason is that the tax savings of the stock portfolio, though smaller on an annual basis, are compounded at a much higher rate.

The sensitivity of the tax benefit to ti means that stocks in tax-advantaged accounts can be a significant hedge against changes in tax policy. This goes well beyond general concerns about future tax rates, although those may be important considerations for some clients. It extends to other proposals that affect the timing and character of taxes. For example, a move toward annual taxation of unrealized capital gains as floated by Secretary of the Treasury Janet Yellen would dramatically increase the tax benefit of holding stocks in tax-advantaged accounts. Tax timing alone, with no increase in the actual tax rate, would increase ti to 15% from 8.7% in the example given earlier. The tax benefit after 30 years would be higher by 62%. Another proposal making the rounds among Democrats – elimination of the step-up in basis at death – would also have a significant impact.

A third and final point is that tax-advantaged accounts hedge against inflation and the value of this hedging capacity should be maximized. Inflation depresses real returns in taxable accounts. This is easily seen in the following example. Assume a pre-tax real return of zero and inflation of 5%. Then the nominal investment return is 5%. Assuming a 15% tax rate, an investment of $10,000 will grow to $10,425 in one year. The constant dollar (real) value after one year will thus be $10,425/1.05, or $9,929, for a real after-tax return of -0.72%.

Because income is tax free in tax-advantaged accounts, it compounds at the full nominal rate or return. The benefit from avoiding the tax drag becomes larger as both inflation and returns increase. It is another reason that locating higher return assets in tax-advantaged accounts can be preferable for some clients, especially if they are concerned about rising inflation.

In sum, tax-advantaged accounts provide clients with valuable opportunities to preserve after-tax wealth in the face of uncertainty about the future. The interrelated effects of return, tax rates, and time horizon are too complex for simple rules of thumb. To take full advantage of these accounts, advisors should quantify the tax benefits under different scenarios.

Peter Hofmann, CFA, is with Fieldmark Advisors, a registered investment advisor based in North Salem, N.Y.

Read more articles by Peter Hofmann