Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

How should clients use tax-advantaged accounts? By quantifying the tax benefits of those accounts, we can refine recommendations on asset location and the traditional-versus-Roth decision. Specifically, low-return assets, even if otherwise taxed at high rates, may not benefit much from being placed in tax-advantaged accounts. Also, the choice between traditional and Roth contributions is asymmetric: Traditional accounts provide an opportunity for a higher tax benefit, but risk incurring a tax cost. Roth contributions provide greater certainty of a positive tax benefit.

The value of tax benefits

The basic structure of tax-advantaged accounts can be summarized as follows:

The table highlights that avoiding tax on investment income (including capital gains) is a key source of the tax benefit.

What is the value of this benefit? I compare the tax-advantaged account accumulation with a (counterfactual) taxable account accumulation. This is the trade-off faced by clients who must decide whether to contribute to a tax-advantaged account, what type of account to choose, and which investments to place in the account.

Per dollar, the prospective value of the tax benefit is given by:

From this equation, we can see that the tax benefit will equal zero if the return (r), the tax rate (t), or the investment period (n) are zero. The value of the benefit will increase exponentially as r or n increase. Not so with the tax rate. The maximum tax rate is 100% (confiscation) at which point the value of the benefit is once again zero.

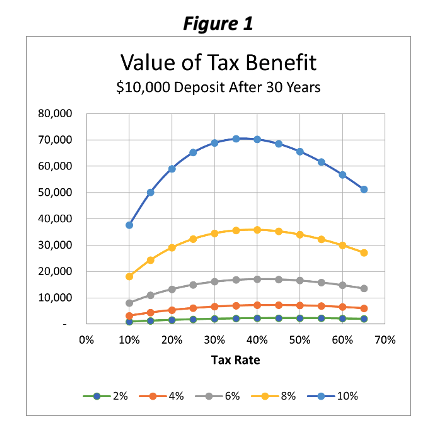

The tax benefit can be significant. Figure 1 illustrates how it varies with the tax rate and return over a 30-year period. The value shown is in addition to accumulation that would occur in a taxable account. The benefit is maximized at a tax rate of about 39%, at which point it accounts for about a fifth to two thirds of the total tax-advantaged account accumulation, depending on the investment return. The optimal (maximum benefit) tax rate varies by investment period as well: between five and 40 years, the maximum benefit is obtained at tax rates between 50% and 35%.

The value of the tax benefit is small for low rates of return. Figure 2 shows how long an investment must compound to achieve an equivalent tax benefit at various rates of return. For example, the tax benefit that accumulates in 40 years at a 2% rate of return takes only about 10 years to achieve at an 8% return.

The implication of this trade-off is that placing low-return assets (e.g., bonds) in tax-advantaged accounts provides limited benefit even if the “tax drag” on the return is higher. Put another way, avoiding a 25% tax on bond income of 2% is less valuable than avoiding even a low 5% tax on an equity return of 8%.

Multiple tax rates

Using a single tax rate is unrealistic. Consider the above formula with three different tax rates,

where tc, td, and ti are the tax rates on contributions, distributions, and investment income, respectively.

The formula is shown using a traditional retirement account, which is taxed at the time of distribution. If tc equals td, the choice between a traditional or Roth account does not matter.i The investor “keeps” the same proportion of the account: (1 + r)n(1 – td=c). The value of the tax benefit obtained on that proportion depends entirely on the tax avoided on investment income. At the extreme, an investor who is able to achieve a zero-tax rate on investment income in their taxable account would receive no tax benefit from using a tax-advantaged account.ii

What if tc does not equal td? Then the tax impact breaks down into two components: 1) the difference between the tax on contributions versus distributions; and 2) the benefit from tax-free investment income. The former effect is powerful and overwhelms the latter over short periods.

For example, assume tc =25%, td =20%, and ti = 10%. There is a five-point difference between the rate at the time of contribution compared with the rate when a distribution is taken, making a traditional account superior to a Roth account. At a 6% annual return, after five years, 70% of the tax benefit is due to this difference, 30% is due to the tax avoided on investment income. After 30 years, the mix has flipped. The tc - td difference now accounts for about 30% of the benefit. Figure 3 illustrates this shift.

The reverse is not true. If we assume tc =20%, td =25%, and ti = 10% there is a five-point difference in favor of the Roth contribution. However, because the tax benefit is measured relative to a regular taxable account there is no additional tax benefit. Both Roth accounts and regular taxable accounts are funded with after-tax dollars (subject to tc.) The tax benefit is purely a function of the tax-free investment income. The higher td only comes into play with a traditional contribution. In that case, it creates a tax cost rather than a benefit – a cost that the investor would have avoided had they opted for a taxable or Roth account. As shown in Figure 4, over time this cost may be overcome by the benefit of tax-free investment income.

Since td is unknown when the decision to contribute is made, this analysis highlights and quantifies one of the benefits of Roth contributions that is sometimes under-appreciated: certainty that a tax benefit will in fact be realized.iii Electing a traditional contribution that, in hindsight, is subject to a higher td will offset any benefit from avoiding taxation of investment income. “Growing out” of this hole can take a long time.

In sum, quantifying the potential tax benefit and its components along the key dimensions of return, time horizon, and tax rates let clients maximize the benefit from tax-advantaged accounts. A future article will explore in more detail how the tax rate on investment income can affect the asset location decision.

Peter Hofmann, CFA, is with Fieldmark Advisors, a registered investment advisor based in North Salem, N.Y.

i It may matter for other reasons, such as uncertainty about future tax rates, liquidity, and estate planning considerations.

ii For example, a zero tax rate on investment income may be achieved by remaining in the 0% capital gains bracket or by holding the account until death.

iii Of course I mean certainty in the context of existing tax law.

Read more articles by Peter Hofmann