Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Is the market environment turning favorable for active equity managers? It seems a strange question to ask in the midst of a pandemic and heightened market volatility, but history tells us that it is during just such turbulent times that active managers excel. There is accumulating evidence that market conditions are growing more attractive for showcasing stock-picking skills.

Active versus Passive

It is well established that active equity mutual funds have underperformed their passive counterparts over the last 10 years or so. A significant portion of this underperformance can be attributed to the large percentage of closet indexers included in the “active” equity universe. Later on, I will discuss the impact of true indexing versus closet indexing on the performance of active equity funds.

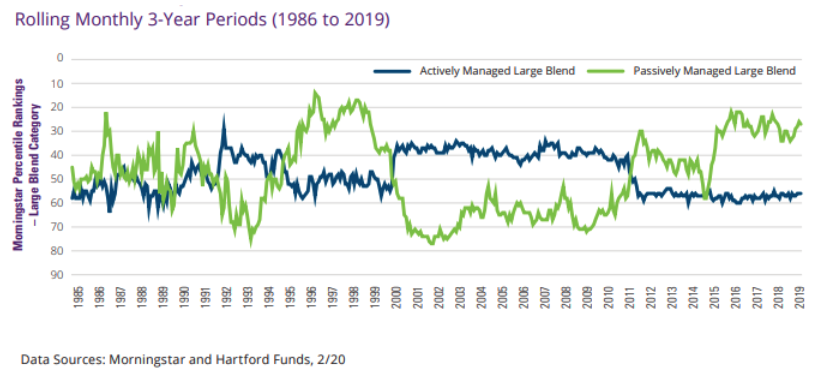

What is not well known is that active funds have gone through extended periods of under- and out-performance. The graph below, from a recent Hartford Funds study, reveals the cyclical nature of this performance. Since 2010, active funds, as measured by what is thought to be the most highly efficient market segment, Morningstar’s large-blend funds, underperformed their passively managed counterparts. However, for the 10 years prior to that, active funds outperformed. Looking back to 1985, there have been extend periods of both under- and out-performance.

The authors also found that, over the last 30 years, active bested passive in 19 of the 26 corrections (a 10% or greater market drop). The recent coronavirus market crash has been dramatic, resulting in a drop of more than 30%, producing the fastest descent into a bear market ever experienced.

Does the dramatic market turmoil of the last few months presage an extended period of active equity out-performance, similar to what we saw after the Dotcom bust and the 2008 Great Recession? There is good reason to believe so.

In recent years, we have not seen this level of uncertainty regarding individual stock valuations. The partial economic worldwide shutdown and massive governmental financial stopgap measures are historically unprecedented. They create difficult-to-decipher crosscurrents that will dominate the forthcoming economic and market recoveries.

It is in just such situations that skilled investment teams shine. It will be sometime before normal valuation ranges return. The resulting wide range of individual-stock returns will provide fertile ground for active equity.

Active equity opportunity

Recent academic research sheds light on the market characteristics that favor stock picking. Three studies (conducted by Gorman, Sapra, and Weigand; Petajisto; and von Reibnitz) show both increasing cross-sectional stock dispersion (the cross sectional standard deviation of returns from either individual stocks or a portfolio of stocks) and increasing volatility (VIX) are predictive of higher returns to stock picking. In addition, Bessembinder shows that high positive skewness (the asymmetry of a probability distribution in which the curve appears distorted or skewed to the right) plays a major role in portfolio and market performance.

In order to estimate the impact of market conditions on stock picking returns, I have proposed active equity opportunity (AEO), a measure of how investors are driving individual stock-return dispersion and skewness. Active equity managers prefer a higher level of AEO, since it is more likely their high-conviction picks will outperform. On the other hand, a low AEO foretells a period in which it will be difficult for even the most talented managers to beat their benchmark.

AEO is estimated using four components, listed here from most to least important.1

- Individual stock cross-sectional standard deviation;

- Individual stock cross-sectional skewness;

- CBOE Volatility Index (VIX); and

- Expected small stock premium.2

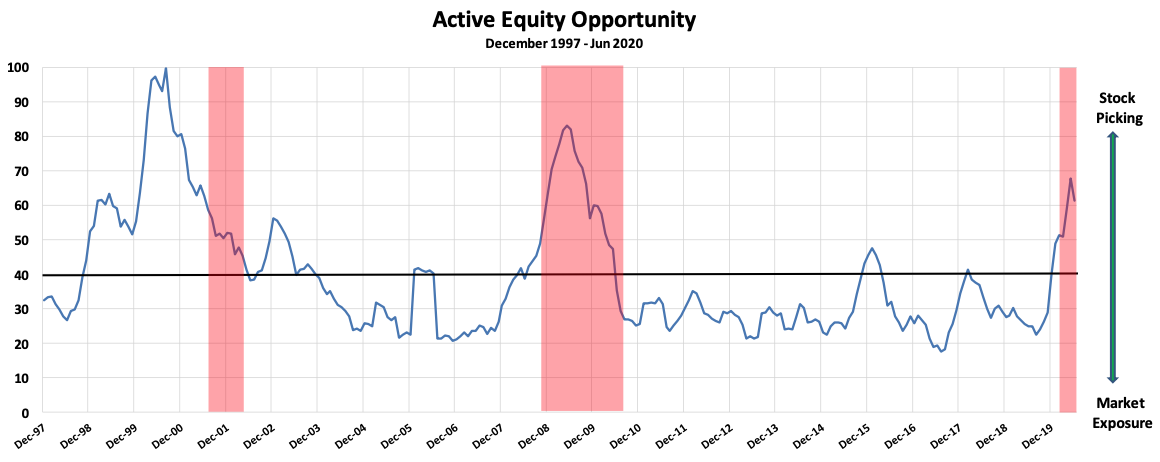

The beginning-of-the-month AEOs for December 1998 through June 2020 are presented in the figure below. The average over this time was 40, which means values greater than 40 signal a better environment for stock picking while lower values signal a worse environment.

During this 20+ year period, 1998 through 2006 and 2008 through 2010 favored stock picking. Of particular interest is that 2010 through 2019, AEO has mostly been below average, declining to a low of 18 in mid-2017.

This von Reibnitz study, based on cross-sectional dispersion going back nearly 50 years, reveals that the mid-2017 AEOs were among the lowest in a half century. Going on 10 years, stock pickers have faced a difficult environment in which to succeed. These results reinforce the active versus passive results discussed earlier.

Sources: Morningstar and AthenaInvest

Since the beginning of 2020, AEO has risen significantly and is well above 40 and strongly into favorable stock-picking territory. The red shaded areas in the figure above represent National Bureau of Economic Research (NBER, the official arbitrator of business-cycle turning points) recessions. The von Reibnitz study, based on a longer 1972 through 2013 fund sample, concludes that, “Overall, these results suggest that periods of elevated dispersion have a positive effect on alpha for the fund sample as a whole, beyond that coming from recessions.” The fact that we are currently in a recession, accompanied by higher AEO values, supports the emergence of a favorable active-equity environment.

2020 equity performance

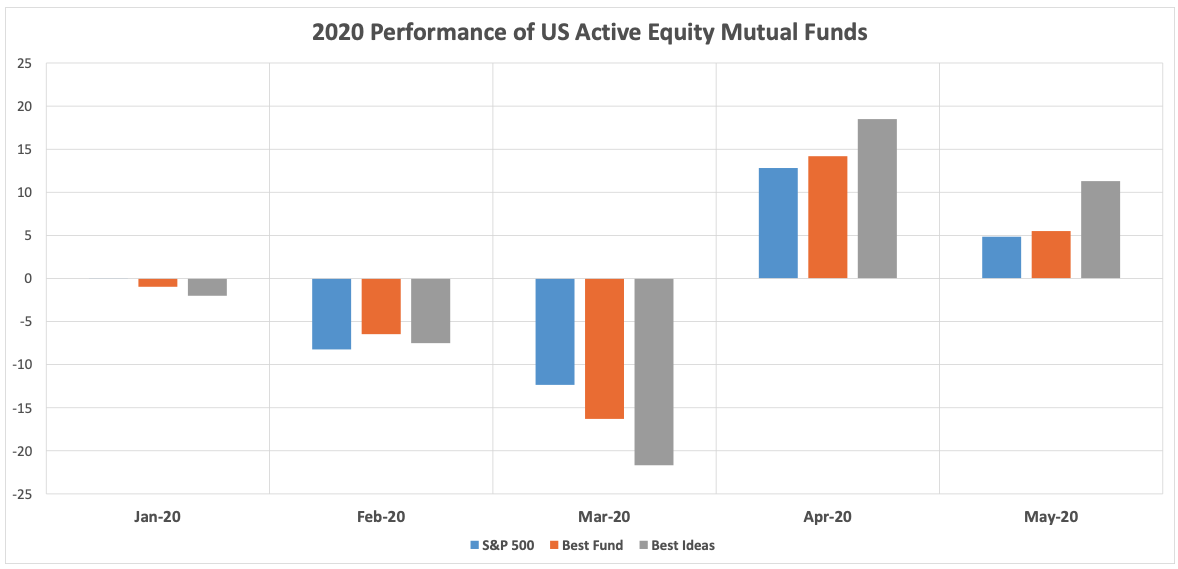

As reported earlier, active-equity funds underperformed for the 10 years ending 2019. How have they done so far this year? The figure below reports the performance of the best active equity funds along with their best tocks (high-conviction stocks) as compared to the S&P 500.

The best funds are those consistently pursing a narrowly defined equity strategy while focusing on their best idea stocks. My firm, AthenaInvest, uses a fund’s self-declared strategy to assigns each fund to one of 10 strategy groupings. The best funds in each strategy are determined using objective measures of strategy consistency and high conviction equity holdings.3

Sources: Morningstar and AthenaInvest

In January and February, the best funds and best stocks performed about the same as the S&P 500. However, in March, when the market moved dramatically down and then back up, both underperformed. As the market rebound continued into the second quarter, both have dramatically outperformed, with best stocks outperforming best funds as one would expect. Even the best funds are not fully invested in best stocks, so by eliminating non-best-idea stocks, the remaining best stocks outperform both the best funds and the market.

For additional evidence, AthenaInvest’s stock-picking portfolios have done very well so far this quarter, generating high returns, strongly outperforming their respective benchmarks. These results, along with the just-reported broader measures, represent short-period returns. But they illustrate the impressive performance of active equity since the market bounce back of late March. These results, combined with the previous observations, provide further support for the emergence of a new era of active equity success.

A broader perspective4

Earlier this year, passive equity mutual fund AUM exceeded active equity AUM for the first time ever. An overriding question is how long this transition from active to passive will last. Will passive funds be the only ones standing at the end of the day? I do not believe this to be the case for the simple reason that as uninformed passive AUM grows, the stock market will become more informationally inefficient.

This means information-gathering active funds have an excellent opportunity to outperform in the face of growing passive AUM. Grossman and Stiglitz made the argument 40 years ago that some degree of information inefficiency must remain in order to incent active investors to pursue the costly process of gathering information they need to make profitable investment decisions. In other words, the current passive revolution is sowing the seeds for an active-equity renaissance.

Wermers surveyed a vast body of empirical results and concluded that the more stocks are held by passive investors, the more informationally inefficient markets become and, in turn, the greater are the opportunities for active managers. In another study, Wermers and Yao find that passive fund trades add little to market efficiency, since they are driven by investor flows, while information gathering active funds trade in stocks that are not efficiently priced.

Cremers and others examined the relation between indexing and active management in the mutual fund industry worldwide. Explicit and closet indexing by active funds were associated with a countries’ regulatory and financial market environments. They found that actively managed funds are more active and charge lower fees when they face more competitive pressure from low-cost, explicitly indexed funds.

Moreover, the average alpha generated by active management was higher in countries with more explicit indexing and lower in countries with more closet indexing. Overall, their evidence suggests that explicit indexing improves competition in the mutual fund industry. The current flow of funds out of closet indexing, even though it means smaller active versus passive AUM, bodes well for those equity managers who consistently pursue a narrowly defined strategy while focusing on high-conviction positions.

With continuing large passive inflows, stocks will be increasingly mispriced. From the current roughly 50/50 split, the forces driving flows into passive funds will eventually be neutralized by the offsetting increase in the attractiveness of stock picking, resulting in a roughly 70% passive/30% truly active split. An attractive equilibrium for successfully pursing active equity strategies is approaching.

Its time has come

Market conditions have turned favorable for active equity funds. Individual stock dispersion and positive skewness, market volatility, and the small-firm premium all have increased in recent months, setting the stage for stock pickers to demonstrate their skill. Given the scale of the economic and market disruptions, an extended period of heightened uncertainty is expected. This makes determining a stock’s fundamental value very difficult, favoring heavily resourced and skilled, professional equity teams.

The active-passive fund flows also bode well. As more money is being managed by passive funds, the more inefficient becomes the stock market, while, in parallel, the more competitive and less closet-index-like become the surviving active managers.

Since the late March market turnaround, active equity has significantly outperformed, the initial indications of what could be a long running period of outperformance. We are witnessing the dawn of a new active-equity era.

C. Thomas Howard is emeritus professor of finance at the University of Denver and CEO and chief investment officer at AthenaInvest, Inc.

1 AEO is calculated using the following methodology: Each component is measured as a 6-month trailing average; Each is converted to a standard normal deviate; These are combined using average correlations with fund and stock alphas; Scaled to range between 0 and 100.

2 Calculated as the difference between the small and large stock expected returns.

See Howard for more details.

3 Neither of these measures are based on past or current performance, but instead on objective measures of fund manager behavior. For more information on how funds are strategy identified and strategy groups are formed see Howard. Best Stocks are those most held by the Best Funds.

4 Some material in this section drawn from Return of the Active Manager, authored by Jason Voss and me, published by Harriman House in 2019.

More ETF Topics >

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.