Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

It’s only natural for someone invested in a poorly performing active equity mutual fund to wonder if it’s time to make a change. Should an investor sell a fund if it trails its benchmark for a year? Three years? Five years?

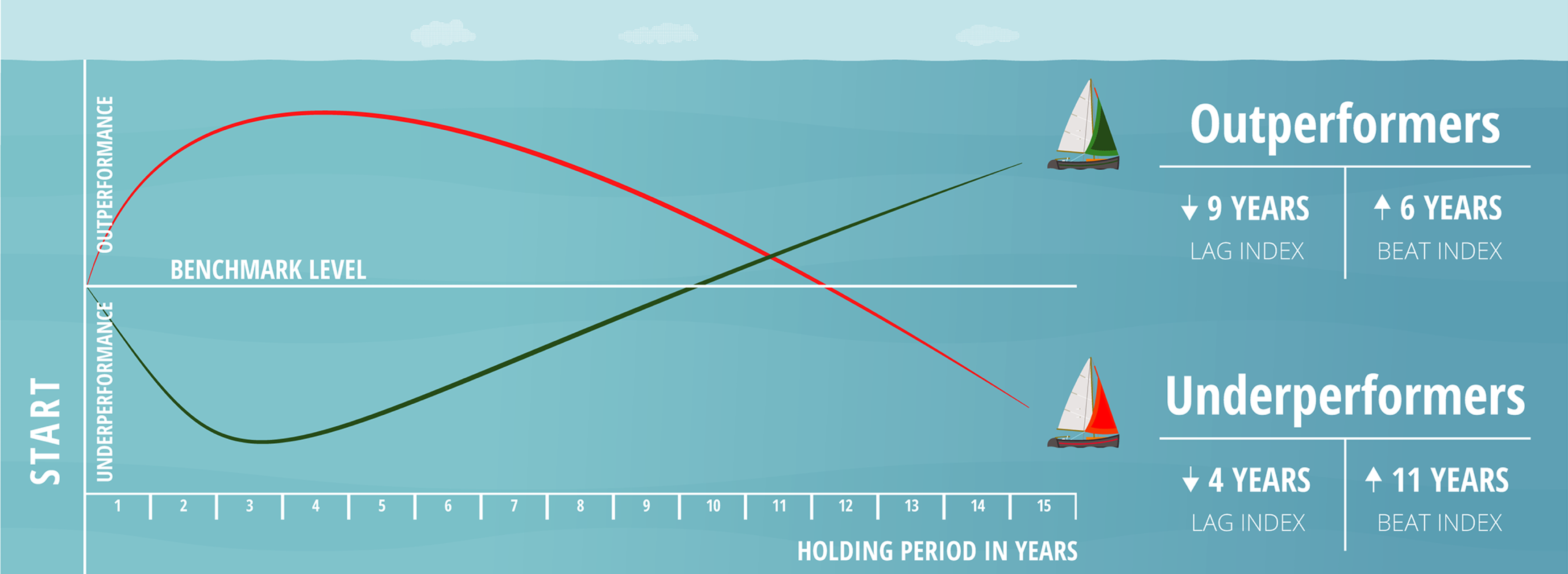

Turns out, active equity mutual funds that beat their benchmark over a 15-year period experience a whopping nine years of cumulative underperformance on average! Conversely, and perhaps even more surprising, funds that ultimately underperform their benchmark over the same 15-year period cumulatively outperform over 11 of those years on average.

Average length of active equity fund underperformance/outperformance (2003-2017)

Source: How Long Can a Good Fund Underperform Its Benchmark, Paul D. Kaplan, Ph.D. and Maciej Kowara, Ph.D., Morningstar Manager Research, March 20, 2018

Source: How Long Can a Good Fund Underperform Its Benchmark, Paul D. Kaplan, Ph.D. and Maciej Kowara, Ph.D., Morningstar Manager Research, March 20, 2018

These insights are illuminated in Kaplan and Kowara’s excellent Morningstar Manager Research piece entitled “How Long Can a Good Fund Underperform Its Benchmark?” But what do these findings mean for investors? One obvious implication is that “Past Performance Does Not Predict Future Performance,” but everyone knows that, right?

The conclusions of this study demonstrate that comparing fund performance versus a benchmark for periods of 10 years or less is not an effective method for deciding when to sell or keep a mutual fund. This long timeframe makes successful active equity mutual fund investing challenging because it requires a different set of behaviors than what instinctively works in other areas of life.

Consider an investor that believes five years is more than long enough to endure a poorly performing fund and replaces it with a fund that has outperformed over the last five years. The investor may feel better by taking action to get rid of the “Bad” fund in favor of a “Good” fund. But the investor has removed the portfolio from the green path on the chart above and placed it on the red path, ultimately compounding the underperformance with an increased likelihood that the new fund will underperform the old one over the next time period. While well-intentioned, this practice results in performance chasing.

If we dig deeper, we find that long-term outperformance is driven by a handful of periodic outsized years accompanied by relatively long periods of underperformance. Investors that want to outperform in the long run need to be prepared to accept substantial periods of underperformance and be willing to hold on to funds for as long as 10-15 years. A mid-course performance evaluation can lead a long-term investor astray more often than not.