An Actuarial Process for Better Decisions in Retirement

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

Incorporating actuarial methodology and the popular floor-and-upside approach to financial planning, I show how advisors can help their retired (or soon-to-be retired) clients make better financial decisions.

This article is a follow-up to my previous Advisor Perspectives articles, Think Like an Actuary to Become a Better Advisor and Better Budgeting with an Actuarial Approach, which encouraged financial advisors to use the actuarial approach to help clients determine how much they can afford to spend each year in retirement and to make other personal financial decisions. If you are unfamiliar with the actuarial approach, I suggest that you read one (or more) of my prior Advisor Perspectives articles or visit my website. I provide free education about the application of the same basic actuarial principles I used as a consulting pension actuary to help plan sponsors determine plan contributions to help individuals, couples and their financial advisors develop reasonable annual spending budgets. I also provide (free) Excel workbooks that may be downloaded for this purpose.

Inspiration for this article comes from the sage advice contained in two Forbes articles by Dirk Cotton, Negotiating the Fog of Retirement Uncertainty and Honey, What’s Our Retirement Plan? In those articles, Cotton discussed how much of one’s retirement resources might be allocated to what he refers to as “floor” and “upside” portfolios. According to Cotton, a floor portfolio is funded primarily by non-risky assets (i.e., Social Security, pensions, annuities and bond ladders) and is designed to provide a safe lifetime income to fund essential expenses, while the remaining assets (the “upside” portfolio) are funded primarily by risky assets to support future discretionary expenses.

Cotton stated, “The most important decision you will make in retirement planning is how much of your resources to allocate to the upside and floor portfolios.” He noted, “The correct balance will depend on how willing you are to risk losing your standard of living for the chance of having an even higher one.” His advice: “The less confident we are in our upside portfolio's ability to deliver on its promises, the more we should allocate to the safe floor portfolio. Finally, he concluded, “Many retirees and even some planners seem to be massively overconfident in upside-portfolio spending rules.”

In this article, I propose a seven-step financial planning process using basic actuarial principles and results from my workbooks to estimate amounts needed to fund a client’s essential and discretionary recurring and non-recurring expenses. Comparing the present value of the client’s assets with the amounts needed to fund those categories of expenses enables retired clients to make better spending and investment strategy decisions and enables those considering retirement to make better retirement timing decisions. I will illustrate this process and apply it to a hypothetical individual, who decides, as a result of going through this process, to increase the size of his floor portfolio by purchasing a combination of single-premium immediate (SPIA) and deferred-income (DIA) annuities. By incorporating this process into her consulting toolkit, our hypothetical financial advisor is able to develop a robust plan that is expected to preserve her client’s standard of living, maximize his expected near-term spending and reduce his investment and longevity risks in retirement.

Seven-step financial planning process for retirees

I recommend that financial advisors add the following financial planning process to their consulting toolkit.

- Estimate the client’s future annual recurring expenses

- Estimate the client’s future non-recurring expenses

- Categorize each expense in steps 1 and 2 as "essential" or "discretionary"

- Using one of our Actuarial Budget Calculator workbooks for retirees (single or married as applicable), determine the actuarial reserves needed to fund future expected recurring and non-recurring essential expenses and future expected recurring and non-recurring discretionary expenses

- Compare the total current (or present) value of the client’s assets with total actuarial reserves needed as calculated in Step 4. If the total current value of assets is greater than the total actuarial reserves needed, then suggest increasing one of the following:

- the client’s current and future spending budgets,

- the client’s rainy-day fund or

- some combination of the two.

If the total current value of the client’s assets is less than total actuarial reserves needed, then suggest one of the following:

- increasing assets (for example through part-time employment),

- decreasing current and future spending budgets (presumably starting with discretionary spending items),

- applying a reasonable smoothing to the current spending budget, or

- some combination of these alternatives.

- Use the “essential expenses” vs. “discretionary expenses” calculations in Step 4 as a guide for developing or modifying the client’s investment strategy

- Repeat above steps at least once a year

Example

Let’s see how Jane, our hypothetical financial advisor, can use the above process, the ABC workbooks and her models to help her hypothetical client, John, better manage his investment and longevity risks, meet his spending goals and protect his standard of living in retirement.

Data

As of January 1, 2019, John is age 65, unmarried and retired. He has previously elected to start his Social Security benefit of $20,000 per annum. He has $1,000,000 in accumulated savings, with about half in his 401(k) plan and the other half in an after-tax account. His current overall investment allocation for these assets is 40% in bonds and 60% in equities. He also has equity in his home, but plans to use his home equity to cover his future long-term care expenses, so for budget determination purposes, he will assume that these two items net out. He has no other sources of retirement income and has no plans at this time to work for pay in retirement.

Jane and John sit down for their initial planning meeting. They discuss John’s current annual expenses based on average amounts over the past few years and John’s expectations for future non-recurring expenses. The amounts are summarized in the table below.

John’s annual recurring and non-recurring expenses

|

Annual Expense Category |

Recurring |

First Year Non-Recurring |

|

Taxes |

$15,600 |

|

|

Work-Related Expenses |

0 |

|

|

Housing |

5,200 |

$29,400* |

|

Food |

7,500 |

|

|

Clothing |

2,900 |

|

|

Healthcare |

6,000 |

|

|

Transportation |

3,900 |

|

|

Entertainment |

2,600 |

|

|

Travel |

2,000 |

$10,000** |

|

Charity |

1,700 |

|

|

Other |

2,730 |

|

|

Total |

$50,130 |

$39,400 |

*The sum of his mortgage payment of $14,400 and anticipated home improvement cost for 2019

**Assumed extra travel expenses for 2019

With respect to his expected non-recurring expenses, John tells Jane that he:

- Expects his current annual home mortgage payments of $14,400 per year will cease on January 1, 2023 (four more years)

- Anticipates spending $15,000 this year and $15,000 next year (in today’s dollars) on home improvements.

- Would like to travel until he reaches age 80 and would like to budget an additional $10,000 per year (increasing at inflation minus 1% each year) for the next 15 years

Jane enters his 2019 data into the ABC for single retiree workbook. He has no heirs that he plans to leave money to upon his demise, so he and Jane agree to input a desired estate at the end of John’s lifetime planning period of $10,000 in today’s dollars in the ABC workbook to cover funeral expenses. They also agree to input $50,000 (about one year’s recurring expenses) for the present value of his future unexpected non-recurring expenses.

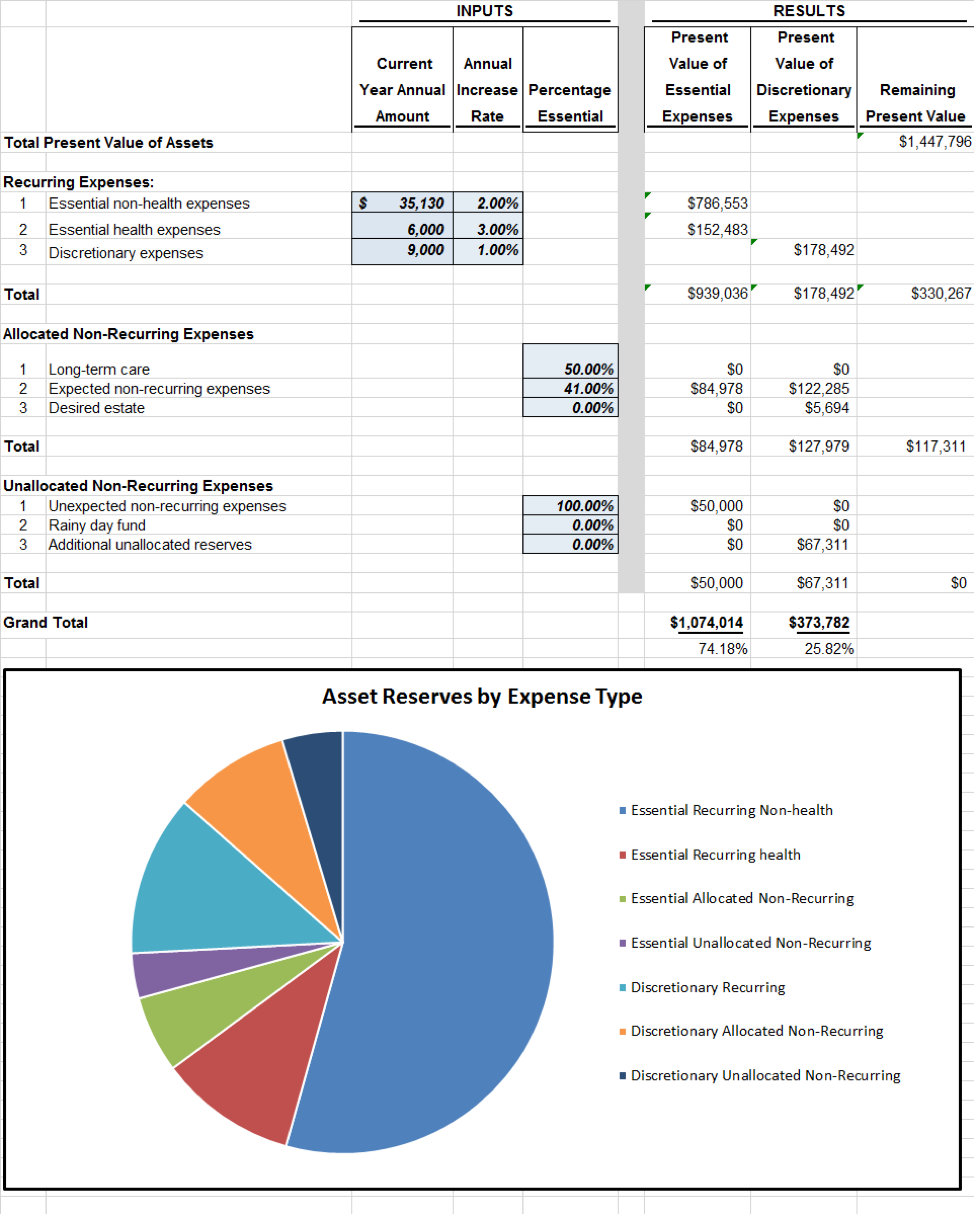

They agree to use the ABC workbook default assumptions (approximately consistent with current inflation-adjusted annuity purchase rates) to develop a total present value of his assets of $1,447,796 ($1,000,000 in accumulated savings and $447,796 from Social Security). Under these assumptions, the present value of John’s non-recurring expenses totals $207,263 ($29,712 for home renovation, $54,361 for home mortgage payments and $123,190 for his future travel plans), his recurring spending budget for 2019 is $52,919 and his total spending budget (including expected non-recurring expenses) is $92,319.

Jane and John go through each recurring and non-recurring expense item from the above table to determine which of his expenses are essential to John and which may be categorized as discretionary. For example, John decides that while all of his extra travel plans are discretionary expenses, he categorizes his future mortgage payments and home renovations as essential. They then use the “Asset Reserves by Expense Type” tab of our workbook and their categorizations to determine the present values of John’s expected future essential expenses and discretionary expenses. A screen shot of this tab for John is shown below.

As shown in this screen shot, about 74% of the present value of John’s resources will be required to fund his expected future essential expenses under the assumptions used in the workbook. The remaining 26% will be required to fund his estimated future discretionary expenses (and leave an unallocated reserve of about $67,000).

Jane and John discuss the implications of these calculations. While John is pleased that his current assets appear to be sufficient to fund his future recurring and non-recurring expenses, he is concerned that his current investment strategy may be too aggressive, and it may make sense to increase the size of his floor portfolio.

He asks Jane what his options are. Jane uses her Monte Carlo model to discuss the probable outcomes of investment in alternative less risky assets. Jane and John discuss John’s bond portfolio and note that while bonds are generally less risky than equities they are not guaranteed for life. If John’s bond holdings are considered as “floor assets”, his floor portfolio is only $847,796 ($447,796 plus $400,000). If his bond holdings are not considered as floor assets, his floor portfolio is only $447,796.

As a result of Jane’s modeling, John expresses interest in purchasing annuity products. Jane obtains several quotes for immediate and deferred annuities. She indicates that a $100,000 premium will purchase a QLAC providing a fixed-dollar lifetime income of $3,110 per month, or $37,320 per annum, starting at John’s age 85 (with nothing paid if he dies prior to that age). She also indicates that a $200,000 premium will purchase a SPIA with a lifetime annual income of $12,972.

To see how the purchase of these annuities would affect his current year spending budget and the present value of his assets, Jane makes three changes to in input/results tab of his 2019 ABC workbook: 1) she changes his accumulated savings from $1,000,000 to $700,000, 2) she adds the expected annual QLAC income of $37,320 with 20-year deferral and 3) she adds annual SPIA income of $12,972 starting immediately. The first thing John sees after these changes is that his annual recurring spending budget would increase by about 5% from $52,919 to $55,636. He also sees that the present value of his assets will increase from $1,447,796 to $1,508,628 ($700,000 of accumulated savings plus $447,796 from Social Security plus $131,707 from the QLAC plus $229,125 from the SPIA).

If he sells $100,000 of his bonds in his pre-tax account and $200,000 of his equities in his after tax account, his new floor portfolio, not considering his bonds, would be $808,628 ($447,796 from Social Security, $131,707 from the QLAC and $229,125 from the immediate annuity) under the default assumptions, or $1,108,628 if the $300,000 in remaining bonds are considered as floor assets. Irrespective of how he considers his bond investments, he would still have $400,000 left invested in equities for his upside portfolio.

Jane explains the differences between results obtained with her Monte Carlo model and the results obtained by the ABC model. She indicates that the Monte Carlo model uses expected assumptions for equity returns and variances and produces ranges of results and probabilities, while the ABC assumes more conservative estimates of investment returns and longevity. Jane and John discuss these assumptions and decide that for the purposes of this exercise (to increase John’s floor portfolio and mitigate longevity and late-in-life-investment risks), it is more appropriate to use the more conservative budgeting assumptions than the more aggressive expected return and longevity assumptions.

As a result of this exercise, John decides to actually sell $100,000 of the bonds in his pre-tax account and purchase the QLAC. He also decides to sell $200,000 of his equities in his after-tax account and purchase the immediate annuity. John and Jane agree to explore purchasing additional annuities in the future when they both hope annuity purchase rates will become more favorable than in the current economic environment.

What about future budgets?

Jane shows John the inflation-adjusted run-out tab of the ABC workbook to see how current and future withdrawals from his accumulated savings will be coordinated with payments from the QLAC, SPIA and Social Security to keep the expected real dollar recurring spending budget at about $55,636 if all assumptions are realized and recurring expenses increase by assumed inflation of 2% per year. If he spends his annual spending budget each year, he understands that his total expected spending is expected to be front-loaded (starting at about $95,000 in 2019), and withdrawals from his accumulated savings are expected to be much higher prior to his age 85 than after (when the QLAC is expected to kick in).

Of course, future experience won’t be exactly as assumed, so John understands that each year, as part of their annual face-to-face meeting to discuss his investment strategy and financial plan, he and Jane will recalculate a revised spending budget that will automatically coordinate his withdrawals with benefits payable under the QLAC to avoid a discontinuity at age 85 when the QLAC payments are scheduled to commence. Depending on actual experience, future spending budgets may be higher or lower than amounts shown in the run-out tab. Based on the probabilities developed in Jane’s Monte Carlo model, John assumes that actual future experience is more likely than not to be more favorable than the default assumptions used for his budget.

What makes this actuarial approach so effective?

Since it utilizes present values of income streams and expenses to develop a rational spending budget, the actuarial approach automatically handles non-linear payment (and expense) streams. By comparison, the 4% Rule, IRS RMD approach (or any other safe withdrawal plan) don’t work with QLACs (or other non-linear income sources) to provide a reasonable spending budget, as these approaches don’t coordinate spending with other sources of retirement income.

By separately reserving for expected non-recurring expenses, the actuarial approach is more efficient than approaches that don’t distinguish between non-recurring and recurring expenses. The actuarial approach develops a reserve for these expenses over their expected payment period, not over the retiree’s entire remaining lifetime planning period.

While Jane’s Monte Carlo model is able to incorporate non-linear payment streams and indicate how annuity purchases may positively affect the probability of success of meeting a certain spending goal, it will not tell John how to adjust his spending budget each year to keep on track. Her model also provides a probability of meeting a specified spending goal that does not distinguish between recurring and non-recurring expenses and therefore does not provide as meaningful information to John. Finally, her Monte Carlo model doesn’t compare the present value of his essential spending with his floor assets. Therefore, while some individuals may struggle to understand the present value concepts used in the actuarial approach, this approach can help Jane, and other financial advisors, better meet the needs of their clients.

Conclusion

I have shown how you can use the actuarial approach and my recommended process to compare the present value of your client’s assets with the present values of their essential and non-essential expenses for the purpose of determining if the client’s assets are sufficient to fund their expected standard of living and for determining a floor and upside investment strategy. If, as a result of performing this comparison, your client believes that they should increase their floor portfolio, I encourage you to use our ABC workbooks, in addition to your current models, to measure the expected impact on the client’s current spending budget and floor portfolio of potential changes in their investment strategy.

I also encourage you to build annual “valuations” and meetings into your consulting process. By better meeting your client’s planning needs you will be adding value to the consulting relationship and, therefore, you will be more likely to retain your clients and increase your revenue.

Ken Steiner, FSA, is a retired actuary with a website entitled, "How Much Can I Afford to Spend in Retirement."

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All