Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

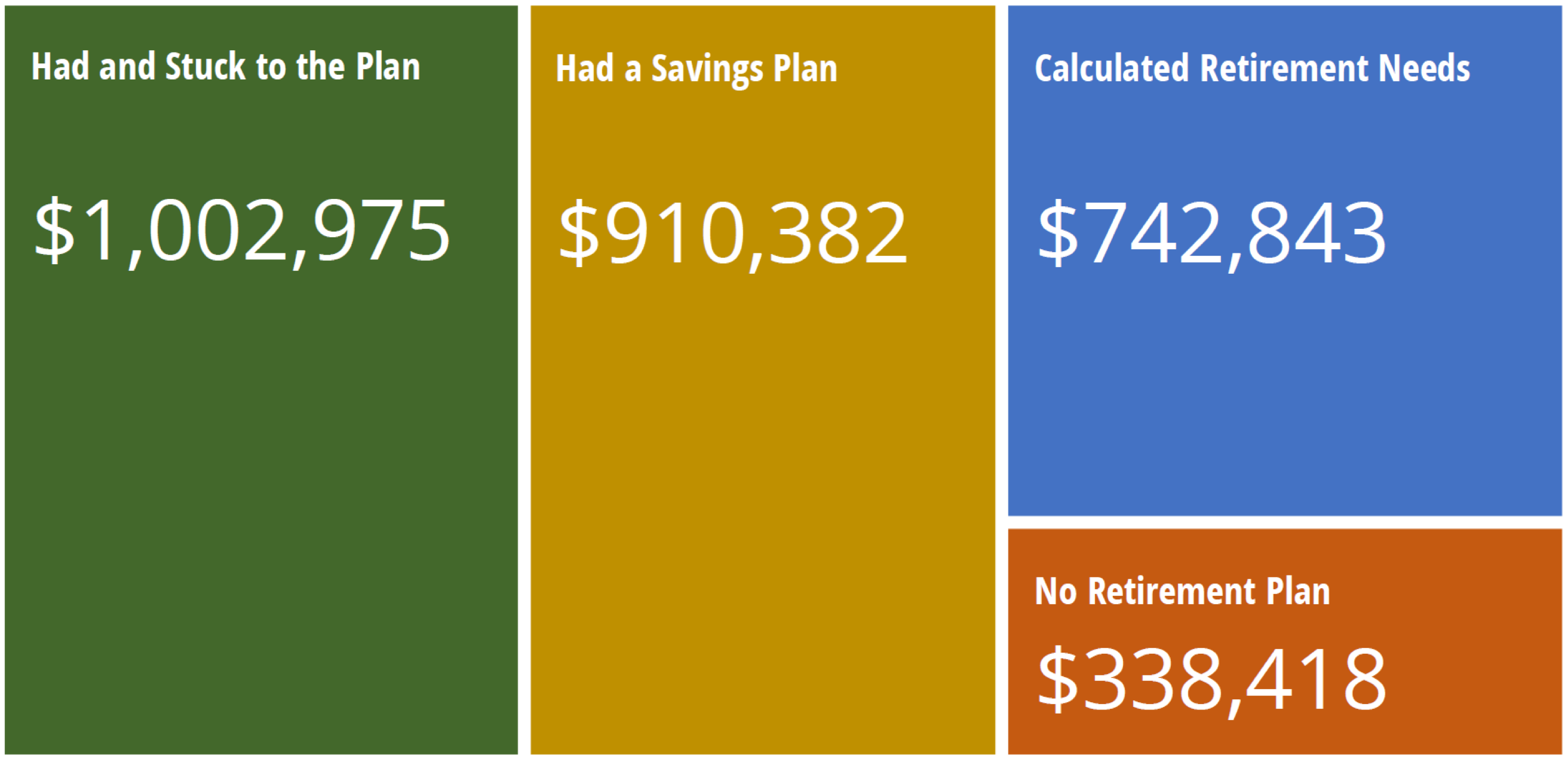

Planning is a powerful tool to help investors succeed and achieve better outcomes. The table below highlights the benefits of planning taken from a study on retirement planning among Americans over age 50. The results show that having and sticking to a plan results in three times the net worth when compared to those who don’t have a plan.

Total net worth across different planning types

Source: Lusardi, Annamaria, and Mitchell, Olivia S., “Financial Literacy and Planning: Implications for Retirement Wellbeing,” May 2011

The study analyzed the following four categories of planning and their impact on net worth:

- Those who had no plan.

- Those who thought about planning by calculating how much they needed for retirement.

- Those that had a plan for how to save the money needed.

- Those that had a plan and stuck to it.

Not surprising, having and sticking to a plan generates the best outcome. What may be surprising is the magnitude of the impact of planning and that any amount of planning results in two to three times the wealth. Even just calculating the amount of money needed for retirement improves results dramatically.

Having a plan simplifies investing and allows investors to focus on things they can control. Contributions, withdrawals and the amount of time invested are all drivers of long-term wealth. These actions are enabled by planning which creates awareness and encourages long-term thinking along with consistent action over time. These practices in turn can help investors avoid many common and costly behavioral bias and mistakes. So, make a plan and stick to it!.

From the behavioral viewpoint

What is going on?

- We are naturally averse to acting in order to avoid loss, punctuated by our two-for-one loss aversion, where we feel twice as bad about a loss as an equivalent gain. We don’t want to make a mistake and suffer the associated regret. Loss and regret are powerful emotional drivers. Daniel Crosby calls this psychological pattern conservatism.

- We are prone to emotional overreaction when under stress because our cognitive functions are diminished by our emotions. This can lead to poor decisions at precisely the wrong time and often results in costly mistakes.

- Building wealth requires delayed gratification, where current benefits are traded off for long-term benefits. We are unlikely to engage in this trade off without systems-two thinking, requiring a conscious process that identifies future value and a method for obtaining it.

What can we do?

- Develop a needs-based plan as a financial roadmap and to help Illustrate the value of following the plan.

- Be realistic, review and update the plan regularly as life circumstances change.

- Focus on what you can control with predetermined courses of action to build discipline.

- Learn to understand that progress toward goals is often more important than short-term investment performance.

- Work with a financial advisor who can provide valuable perspective and guidance to help you stick to the plan.

C. Thomas Howard, PhD, is the CEO and chief investment officer at AthenaInvest, Inc., a Colorado-based investment manager. Tom oversees Athena’s ongoing research which has led to a number of patents, industry publications and conference presentations. He is a professor emeritus at the Reiman School of Finance, Daniels College of Business, University of Denver where he taught courses and published articles for over 30 years in the areas of investment man

More Factor-Based Investing Topics >

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives Source: Lusardi, Annamaria, and Mitchell, Olivia S., “Financial Literacy and Planning: Implications for Retirement Wellbeing,” May 2011

Source: Lusardi, Annamaria, and Mitchell, Olivia S., “Financial Literacy and Planning: Implications for Retirement Wellbeing,” May 2011