In this December 2018 article, I called attention to the challenges of aiming for a savings target at retirement while taking stock market risk. The prevalent approach of saving a fixed percentage of income every year can miss the retirement target by a wide margin, but adjusting annual savings contributions can run into problems as well. Here, I’ll introduce new ways to measure the performance of pre-retirement strategies, test two new strategies and discuss the potential for more sophisticated approaches.

I’ll use an example similar to the one from the previous article – a 45-year old with current savings of $340,000 who wishes to retire in 20 years. This individual needs to determine how much to save each year until a retirement that will last 30 years. I’ll also assume that, after paying for basic living expenses, $60,000 is left over each year that can be split between discretionary spending and retirement-savings contributions. I’ll further assume that this individual will have enough sources of post-retirement income from Social Security, pensions, or annuities so that withdrawals from savings can all be used for discretionary spending. One of the goals will be to have similar amounts available for discretionary spending pre- and post-retirement – what economists refer to as consumption smoothing, or simply maintaining the same lifestyle.

As before, I’ll use Monte Carlo simulations to project outcomes based on historical returns adjusted downward to produce arithmetic average real returns of 5% for stocks and 1% for bonds. I’ll assume a 60% stock allocation prior to retirement and 30% after retirement as a target-date approach.

Goal setting

We need to first ask the question: How much should this individual save each year to be consistent with maintaining the same pre- and post-retirement lifestyle? We know the initial savings and expected returns pre-and post-retirement. Using Excel or an HP calculator, we can calculate factors for the future value at retirement of $1 per year in savings and the present value of $1 per year in retirement withdrawals. With some algebra we can determine that savings contributions of $13,385 per year will produce equal discretionary spending pre- and post-retirement. We can also estimate savings at retirement of $1,038,221. These amounts and all amounts that follow will be stated in constant 2019 dollars.

Previous strategies

In my previous article, I showed results for strategies of: (1) fixed real savings contributions and (2) adjusting annual savings contributions to hit a retirement target. Below I show results of repeating this exercise and introduce new performance measures.

|

Performance measures for pre-retirement strategies

|

|

Performance measures

|

Fixed contributions

|

Fixed retirement target

|

|

Retirement value at age 65

|

|

|

|

Average

|

$999,032

|

$1,038,221

|

|

Range 25th to 75th percentile

|

$499,367

|

$0

|

| |

|

|

|

Pre-retirement contributions

|

|

|

|

Average

|

$13,385

|

$14,150

|

|

Range 25th to 75th percentile

|

$0

|

$43,295

|

|

Annual volatility

|

$0

|

$22,653

|

| |

|

|

|

Withdrawals during retirement

|

|

|

|

Average

|

$45,248

|

$47,173

|

|

Range 25th to 75th percentile

|

$27,640

|

$19,932

|

|

Annual volatility

|

$2,615

|

$2,828

|

| |

|

|

|

Consumption disruption

|

$12,200

|

$101,664

|

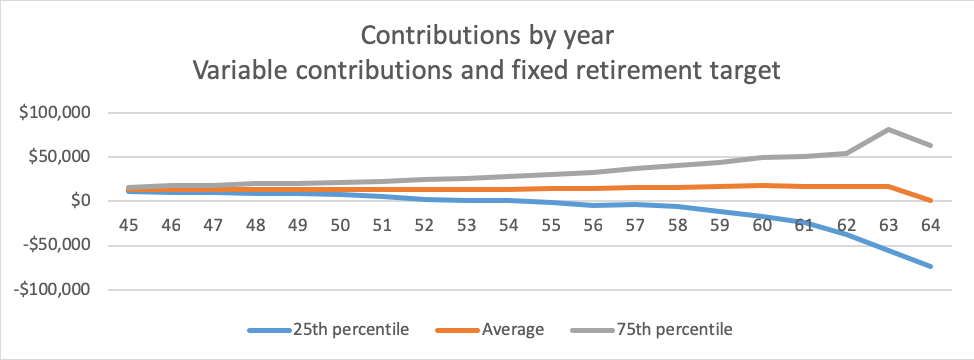

The top block shows average savings amounts at retirement from the Monte Carlo simulations for the two strategies and also the range from the 25th to the 75th percentile. For fixed contributions this highlights the problem cited in my previous article – the wide range of outcomes – half the amounts at retirement fall in a $500,000 span and the remainder are spread even more widely. With the fixed retirement target, we can reduce this span to zero, but encounter different problems as shown in block below.

To achieve a fixed retirement target, we see wild swings in the amounts needed to be saved each year. The range between the 25th and 75th percentiles is $43,000, which is extreme in relation to an average of about $14,000. I also provide a measure of the annual volatility of savings contributions – the average absolute value of annual changes – and this is close to $23,000 per year. This is obviously not a feasible strategy.

I assume that withdrawals during retirement adjust each year aiming to be level over the remainder of retirement, which is basically the ARVA method proposed by Laurence Siegel and Barton Waring. For the fixed contributions strategy, the percentile range reflects both the variability in savings amounts at retirement and variability from investment performance during retirement, while, for the fixed retirement target only the latter source of variability has an impact. The annual volatility of withdrawals reflects the variability of investment returns.

Finally, I include a measure called “consumption disruption.” This is the average absolute value of the change in discretionary spending from the year prior to retirement to the first year of retirement. Attempting to hit a fixed retirement target would involve major disruption. This is further highlighted the graph below (similar to one from the previous article), showing the percentile range for year-by-year contributions:

Bounded contributions

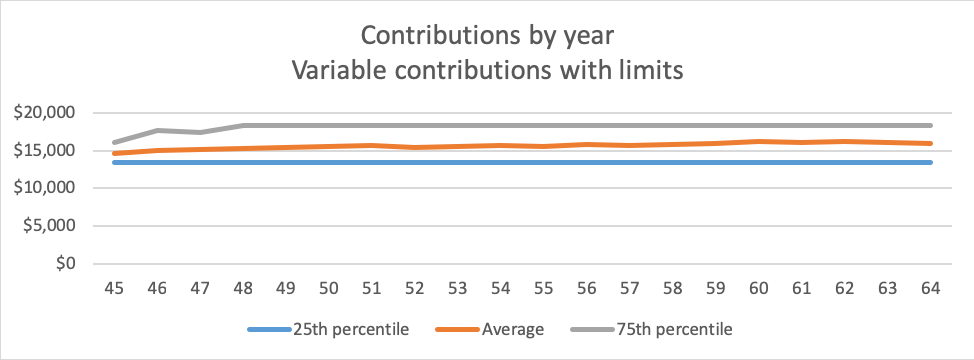

One of the APViewpoint suggestions from the prior article was to aim for a retirement target without decreasing contributions from the initial level. This would prevent reducing or eliminating contributions when investments do well and then having to distress clients with increases when investment markets hit a rough patch. In the chart below I’ve added a column to show results for such a strategy. I aim for the $1,038,221 retirement target as before, but set the minimum contribution at $13,385 – the amount used in the fixed contribution strategy. It also seems reasonable to set an upper bound and I have arbitrarily chosen $18,385, which establishes a $5,000 range on annual contributions.

|

Performance measures for pre-retirement strategies

|

|

|

Performance measures

|

Fixed contributions

|

Fixed retirement target

|

Contributions with lower and upper bound

|

|

Retirement value at age 65

|

|

|

|

|

Average

|

$999,032

|

$1,038,221

|

$1,054,669

|

|

Range 25th to 75th percentile

|

$499,367

|

$0

|

$449,597

|

| |

|

|

|

|

Pre-retirement contributions

|

|

|

|

|

Average

|

$13,385

|

$14,150

|

$15,627

|

|

Range 25th to 75th percentile

|

$0

|

$43,295

|

$4,794

|

|

Annual volatility

|

$0

|

$22,653

|

$663

|

| |

|

|

|

|

Withdrawals during retirement

|

|

|

|

|

Average

|

$45,248

|

$47,173

|

$47,732

|

|

Range 25th to 75th percentile

|

$27,640

|

$19,932

|

$27,933

|

|

Annual volatility

|

$2,615

|

$2,828

|

$2,942

|

| |

|

|

|

|

Consumption disruption

|

$12,200

|

$101,664

|

$10,362

|

Unfortunately, even though this approach seems to make good sense, the performance measures do not differ much from just using fixed contributions. The following graph shows the paths of contributions under this approach.

An examination of individual simulations indicates that almost all the cases move quickly to the upper or lower bound and remain there until retirement. We end up with a combination of fixed contributions at two different levels. We could widen the upper and lower bounds, but then we would encounter the same performance issues as with a fixed retirement target.

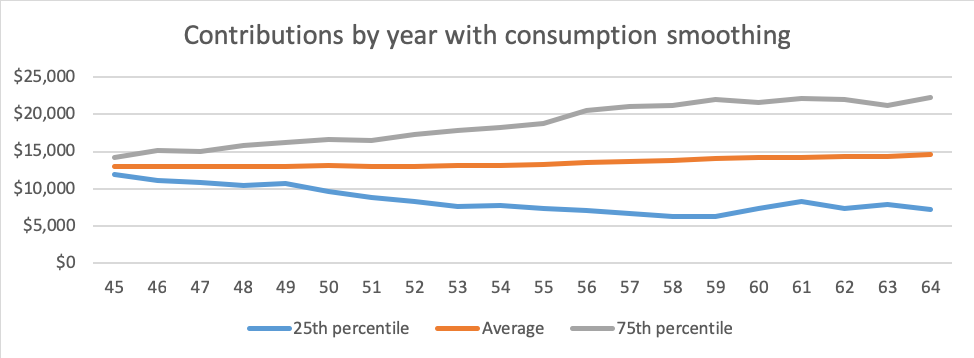

Consumption smoothing

Finally, I attempted a strategy where I abandon a retirement savings target, and focus on smoothing discretionary spending pre- and post- retirement. During the pre-retirement period, this involves annual recalculations of the savings contribution amount based on the same approach that resulted in the starting contribution of $13,385. For example, after a year of poor investment performance, the likely result of such a recalculation would be the combination of lowering of prospective retirement withdrawals, lowering the estimated savings amount at retirement and increasing retirement savings contributions. The increase in savings contributions will lower pre-retirement discretionary spending to match lower prospective retirement withdrawals. This process will be less disruptive than aiming for a retirement saving target, particularly in the years near retirement, because adjustments are spread over both the remaining years of pre-retirement and the full retirement period. The exhibit below provides and additional consumption smoothing column:

|

Performance measures for pre-retirement strategies

|

|

|

|

Performance measures

|

Fixed contributions

|

Fixed retirement target

|

Contributions with lower and upper bound

|

Consumption smoothing

|

|

Retirement value at age 65

|

|

|

|

|

|

Average

|

$999,032

|

$1,038,221

|

$1,054,669

|

$1,009,625

|

|

Range 25th to 75th percentile

|

$499,367

|

$0

|

$449,597

|

$334,195

|

| |

|

|

|

|

|

Pre-retirement contributions

|

|

|

|

|

|

Average

|

$13,385

|

$14,150

|

$15,627

|

$13,521

|

|

Range 25th to 75th percentile

|

$0

|

$43,295

|

$4,794

|

$10,344

|

|

Annual volatility

|

$0

|

$22,653

|

$663

|

$2,564

|

| |

|

|

|

|

|

Withdrawals during retirement

|

|

|

|

|

|

Average

|

$45,248

|

$47,173

|

$47,732

|

$45,901

|

|

Range 25th to 75th percentile

|

$27,640

|

$19,932

|

$27,933

|

$24,316

|

|

Annual volatility

|

$2,615

|

$2,828

|

$2,942

|

$2,884

|

| |

|

|

|

|

|

Consumption disruption

|

$12,200

|

$101,664

|

$10,362

|

$25

|

Under this approach, the ranges are tamed somewhat, and what is particularly striking is the elimination of the disruption in discretionary spending at retirement. However, even under this approach, there will still be a range of contributions and a range of withdrawals as is shown in the graph below – an inevitable result of generating retirement income with volatile investments.

The alternative would be to use investments like bond ladders or single-premium income annuities (SPIAs) to generate fixed contributions and withdrawals. A calculation using the consumption smoothing equations and assuming a 1% real return would increase savings contributions to $23,887 and lower discretionary spending to $36,113, both pre- and post-retirement. So the choice would be fixed spending at the $36,000 level, or achieving a $10,000 greater average with more variability, or something in between – but no free lunch in the form of high discretionary spending with no variability.

Having reviewed the various approaches and performance measures, my personal view is that consumption smoothing should take precedence over other considerations. Maintaining a certain lifestyle from the working years through the retirement years makes more sense than a plan that disrupts the lifestyle in either direction at the time of retirement. Boston University professor Laurence Kotlikoff has been a strong advocate for consumption smoothing in financial planning, and founded the company Economic Security Planning, Inc. about 20 years ago. It offers two financial planning software systems, ESPlanner and a newer product MaxiFi Planner, both based on a foundation of consumption smoothing. ESPlanner was profiled in this 2011 Advisor Perspectives article.

More sophisticated approaches

There are more sophisticated approaches that aim for a retirement-age savings target or do consumption soothing, and I’ll provide links to a few examples.

Canadian researchers Graham Westmacott, Peter Forsyth, Kenneth Vetzel have done research on varying the asset allocation during the pre-retirement years when using fixed contributions and aiming for a retirement-age savings target. They advocate a dynamic and adaptive asset allocation strategy rather than one that uses a pre-determined target-date fund glide path. They demonstrate that their strategy can significantly reduce the variability of savings at retirement.

From the UK, Cass Business School Professor and Director of the Pensions Institute David Blake and associates Douglas Wright and Yumeng Zhang, wrote this 2011 paper based on a full economic life-cycle model allowing for variable contributions, spending and asset allocation over the full lifecycle. Optimization involved the use of utility functions and dynamic programming. A plus for this paper is that the optimization techniques are fully explained rather that given a shorthand treatment. Key findings were that optimal asset allocation glide paths came out steeper than for typical target-date funds, e.g. 100% stocks until age 50 and then dropping steeply to around 20%. Optimal savings contributions recognized typical earnings profiles by age, and the optimal consumption smoothing was achieved with no contributions until the mid-30s, increasing contribution rates in the years with peak earnings increases, and a slowing of contributions in the years nearing retirement when earnings typically rise less rapidly.

Gordon Irlam, creator of the AACalc.com software that I discussed in this 2013 article, wrote this paper that uses an approach similar to that used in the Blake et al. paper, but Irlam also includes Social Security as an income source. Again, his optimization favors a 100% stock allocation during most of the working years, but not as much of a cutback for retirement because of the base of income provided by Social Security.

Both the Blake et al. and Irlam approaches rely on utility functions, which unfortunately have not succeeded in crossing over from economic research to financial planning. A remaining challenge is figuring out how best to bring the power of the analytic techniques used by economists into financial planning practice.

Final words

Strategies for both pre- and post-retirement planning will inevitably involve tradeoffs between high and variable consumption versus lower but less variable spending. Optimization means getting the most consumption for a given amount of variability, but not eliminating variability. It comes down to clients working with advisors to make the appropriate assessment of how much variability in spending they are comfortable with pre- and post-retirement.

Joe Tomlinson is an actuary and financial planner, and his work mostly focuses on research related to retirement planning. He previously ran Tomlinson Financial Planning, LLC in Greenville, Maine, but now resides in West Yorkshire, England. He thanks Neal Merbaum, Rick Miller, Graham Westmacott, Gordon Irlam, Dick Purcell, and the APViewpoint discussion of the prior article for valuable input.

More Alternative Investments Topics >