Should those further from retirement safely allocate more to stocks? I’ll use an example to challenge the popular notion that those with many years left until retirement can safely allocate heavily to stocks. I’ll then demonstrate that pre-retirement investment challenges are more difficult to deal with than generating income after retirement.

The motivation for this article came from the recent stock market swoon, which predictably gave rise to a bevy of articles and posts with suggestions about how investors should react. A recurring theme was that those close to retirement had good reason to be nervous, while those with many years of work and investing ahead had less reason to worry. Of course, the important takeaway from such discussions is not whether to be nervous, but instead to focus on appropriate asset allocations at different stages in the retirement-savings lifecycle.

Time is not the great diversifier

I’ll use an example of a 45-year old who wishes to retire in 20 years with a savings target of $1 million (in 2018 dollars). I’ll assume that he or she currently has $340,000 in retirement savings and will be saving $15,000 per year increasing with inflation. This individual will maintain a 60/40 stock/bond portfolio.

I’ll use Monte Carlo simulations to project the range of possible outcomes. But, instead of generating random yearly returns, I’ll employ a technique called “bootstrapping.” This uses randomly selecting 20-year blocks of stock and bond returns from Ibbotson data that covers the years 1926-2017. The objective is to capture historical relationships between stock and bond returns and year-to-year correlations within each asset class. However, I believe that historical returns paint too rosy a picture going forward, so I will scale down the historical returns to produce an average annual arithmetic real return for stocks of 5% and 1% for bonds.

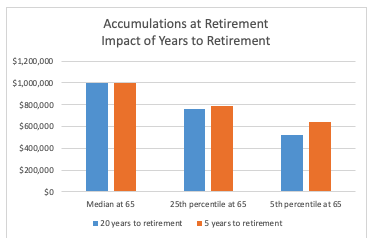

In the chart below I provide downside risk measures showing the 25th and 5th percentiles of amounts saved at retirement in 2018 dollars. For comparison, I also provide the results for a client five years from retirement with $770,000 in savings who is also saving an inflation-adjusted $15,000 per year with a retirement-age target of $1 million.

As for the question, “Who should be worried?” the answer turns out to be both.

Conventional wisdom might decree that the client with 20 years remaining should not be worried because stock market ups and downs will balance out over time, and additional stability will be provided by 20 years of future savings contributions fixed at $15,000 per year in real dollars. (These future savings can be thought of as the “human capital” contribution to retirement.)

But that’s not what the results of this analysis indicate. There’s roughly a one-in-20 chance that savings at retirement will be less than half what is hoped for, and a one-in-four chance savings will be less than three-quarters of the desired amount. The amount of retirement income such savings can generate will be directly proportional to the amount of savings at retirement.

When we compare the client with 20 years remaining to the one with five years, we see that time and future fixed savings have not reduced risk, but instead increased it. So time is not the great diversifier. Although this challenges commonly held beliefs, it is by no means a new finding. In 1995 Professor Zvi Bodie wrote this article challenging the notion of “stocks for the long run,” and later wrote two books on retirement planning that reflected the same theme – Worry Free Investing and Risk Less and Prosper. However, the view (or perhaps hope) still persists that stocks are safe over long enough planning horizons.

Target-date funds are not the answer

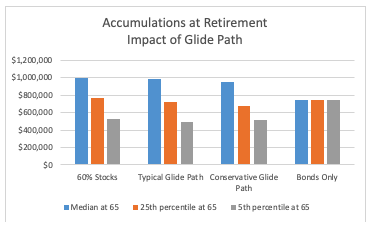

We need to see if there is a way to reduce the range of savings amounts at retirement without losing the benefit of the return premium that stocks provide. As a first step we can examine what happens if we lower the stock allocation as we get closer to retirement. This is the approach target-date funds take through their “glide paths.” The chart below compares our level 60/40 stock/bond allocation with results from two different glide paths derived from Morningstar survey data on target-date funds. The typical glide path has 80% stocks 20 years before retirement gliding down to 40% at retirement, while the conservative glide path decreases from 60% to 20%. For comparison I also include results for hypothetical “bonds only” investing, which assumes a 1% real return and no volatility – equivalent to investing in zero-coupon inflation-protected bonds (TIPS strips) maturing at retirement.

For the target-date glide paths, the disappointing news is that the range of outcomes are not that dissimilar from the level 60/40 allocation. The distributions tighten somewhat, but mostly because the median results decline. The 25th and 5th percentiles are worse than with 60% stocks. As might be expected, the bonds-only median falls below the median outcome where stocks are included in the portfolio, but the variation in outcomes is eliminated.

Switching to a target-date glide path is not the answer. We need to look for another approach.

Variable contributions

So far we have assumed level real contributions of $15,000 per year. We’ll now examine what happens if we allow contributions to vary based on underlying investment performance. If performance is poor we increase contributions and vice versa. This is analogous to a post-retirement switch from fixed withdrawals (e.g., the 4% rule) to a variable or dynamic approach where withdrawals are a function of the current value of remaining savings. A subset of such dynamic methods are those based in the Excel PMT function, which determines an annually-recalculated level withdrawal amount as a function of the expected return, expected remaining years and current savings. The ARVA method proposed by Laurence Siegel and Barton Waring is an example.

We can use this same Excel PMT function to annually recalculate the retirement savings contribution by entering the expected real return, number of years to retirement, current savings and target real savings at retirement. By using real returns and targeting real savings at retirement we calculate a level real contribution amount that will increase with inflation each year. This savings contribution amount will adjust with each year’s recalculation depending on investment performance for the past year. We can model this process using the same bootstrap method that we used with level real contributions.

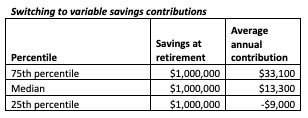

We apply this method based on our initial example of 20 years to retirement and a 60% stock allocation. The chart below provides good and bad news.

If we assume that contributions are either made or trued-up at the end of each year, we see that we hit our $1 million target exactly regardless of investment performance. This is just a mathematical certainty from repeating the PMT function each year until retirement. The bad news is the range of 20-year average contributions that may be required. The median value is about $13,000, slightly less than the $15,000 used previously, but the range varies widely. At the low end, the 25th percentile calls for negative average contributions, indicating that the initial $340,000 20 years before retirement is more than sufficient to grow to $1 million at retirement. But the 75th percentile calls for more than double the median contribution.

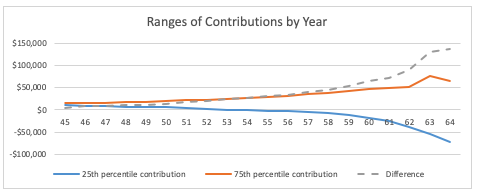

We can gain further insight about what happens with contributions by examining the following chart, which shows the 25th and 75th percentiles year-by-year for the 20 years leading up to retirement.

As we get close to retirement, the range of required contributions widens dramatically. This is quite different than what happens when the PMT method is applied to retirement withdrawals. In that case, as we approach the end of retirement, the remaining savings balance is dwindling. Investment performance has less of an impact even though the remaining period for adjustments is shortening. But with pre-retirement contributions, the savings balance is reaching its highest point just as the years remaining for adjustment approach zero. The result is either lots of variability in the balance at retirement with fixed contributions as was shown earlier, or lots of variability in contributions near retirement with variable contributions.

The balance between accumulation and withdrawal strategies

Unfortunately there are no easy answers. One can try experiments where contributions are limited to a high and low range or place limits on annual changes in contributions. But if such limits are set at reasonable, practical levels, we end up with variable amounts of savings at retirement similar to what we projected based on fixed contributions. Another approach is to ignore the amounts at retirement and rely on variable withdrawals over the course of retirement to self-correct to some degree. There is evidence based on historical returns that mean reversion may reduce the variability of retirement withdrawals, but given that such analysis requires 60-year blocks of return data, we have few independent trials to on which to base our analysis. Wade Pfau has studied the relationship between savings rates and withdrawal rates, and reported his findings in this 2011 blog post.

Of course there is also the option of sacrificing upside and accepting a much larger allocation to fixed income investments – bond funds, individual bonds, CDs, stable-value funds, and various types of annuities designed for accumulation that pay fixed rates of interest. Finally, to the extent there is flexibility about yearly contributions to saving and/or flexibility about when to retire, it can make up for variability in investment performance.

Final word

The pre-retirement challenge of hitting a target number at retirement have not been adequately understood or researched. To some extent this is because of an unjustified faith in self-correcting properties of the stock market. This is a subset of the much more general problem of attempting to use volatile investments to meet fixed obligations, for example, in public pension funding. The pre-retirement phase provides its own unique and daunting challenges.

Joe Tomlinson is an actuary and financial planner, and his work mostly focuses on research related to retirement planning. He previously ran Tomlinson Financial Planning, LLC in Greenville, Maine, but now resides in West Yorkshire, England.

Read more articles by Joe Tomlinson