Strategy Based Framework Improves on Style Grid

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

A simple question was asked 30 years ago: “How should we group and evaluate active equity fund managers?” The answer to that question is the widely accepted style grid of market capitalization and value-growth. It was arbitrary, lacking research or academic foundation. Regardless, the widespread adoption of the style box has had pernicious, unintended consequences as managers are incented to adhere to it and track arbitrary benchmarks.

A powerful alternative is to organize managers by the investment strategy that a fund pursues. Once constructed, these statistically valid peer groups provide a comprehensive framework for portfolio construction, manager evaluation, fund selection, and benchmarking, and, quite surprisingly, can be used for stock selection and for managing market exposure or, in short, strategy-based investing (SBI).

Investment strategy as a new framework

Investment strategy – or process, or methodology – is the actual way a manager goes about analyzing, buying and selling investments. Strategy encompasses the manager’s general approach to stock picking as well as the specific elements upon which the manager focuses. This concept also applies to other asset classes.

As an example, a valuation manager (one of the 10 equity strategies to be introduced shortly) identifies and invests in undervalued stocks. The elements used by the manager to implement the valuation strategy might include P/E ratios, valuing future cash flows, or being a contrarian. Drilling down further, the specific criteria used by the manager, such as purchasing stocks with a P/E of less than 15, are the manager’s “secret sauce” and are not part of strategy categorization.

Armed with this basic, yet essential understanding of how professionals manage portfolios, organization around investment strategy is a powerful approach to investment management. Anyone who has looked at a large universe of managers quickly realizes there is a broad spectrum of investment strategies and a wide range of specific investment elements.

Identifying the strategy of U.S. and international active equity mutual funds is accomplished by gathering “principal investment strategies” information from each fund’s prospectus (SEC-mandated since 1998), which is input into a strategy-identification algorithm. This algorithm has been fine tuned using an iterative process involving manager interviews, gathering principal strategy information, eliminating keywords that generate false signals, and settling on a manageable number of strategies.

Over the last 10 years, our firm has gathered tens of thousands of pieces of strategy information for the 3,000 or so (ignoring share classes) U.S.-based active U.S. and international equity mutual funds. The identification algorithm assigns specific strategy information to one of 40 elements (i.e. the specific things managers do to implement their strategy), which are then assigned to one of 10 equity strategies. The 10 equity strategies are listed below.

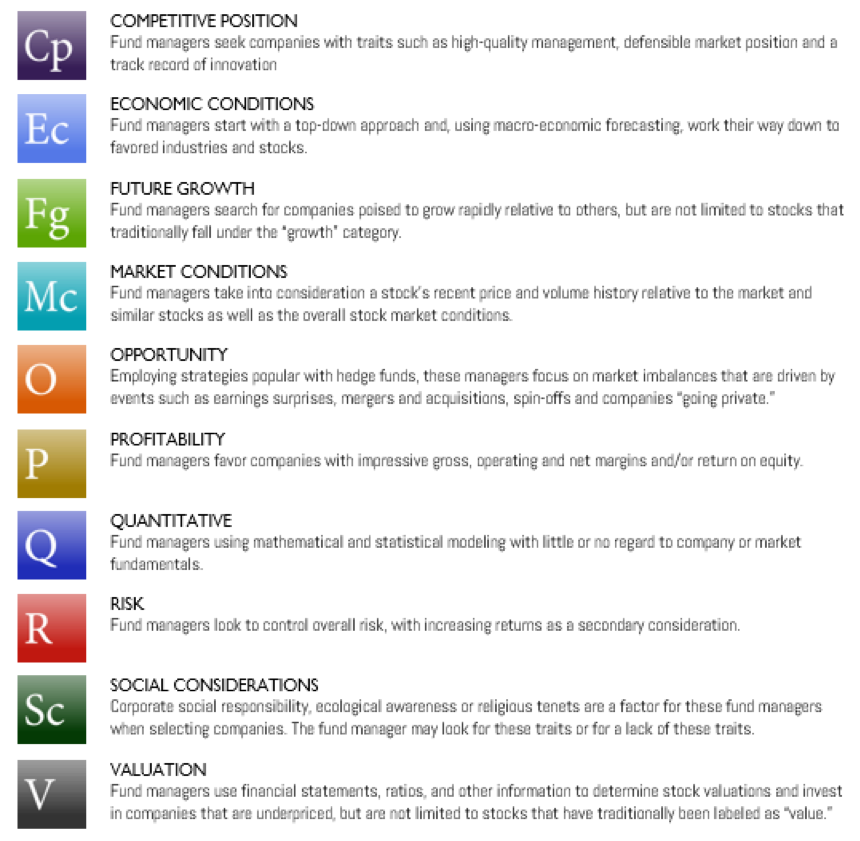

Active equity strategy descriptions

For example, competitive position managers focus on business principles, including quality of management, market power, product reputation, competitive advantage, sustainability of the business model and history of adapting to market changes. Economic conditions managers take a top-down approach based on economic fundamentals, and so forth for the other eight strategies. Those that believe equity managers deviate from their stated investment approach and therefore question the value of self-declared strategy should review my study that summarizes the initial test results.

The strategy database is updated monthly and has captured some data as far back as 1980. This is a self-identification process, so the number of funds varies across strategies. Summary strategy benchmark statistics are provided in Table 1 later in this article.

Advantages of the strategy framework

Clustering managers based on their self-declared strategy helps avoid the problem of comparing funds that are actually pursuing very different investment approaches. Other benefits include:

- Managers are free to pursue their stated investment strategy.

- Managers following similar investment processes are grouped together.

- Strategy based peer groups remain stable over time, allowing for long-term comparisons.

- Returns are more correlated within strategies and less correlated across strategies.

Once the universe is organized this way, useful applications begin to appear.

- Strategic and tactical portfolio construction based on strategy can be implemented.

- Managers can be ranked by their consistency and conviction.

- Stocks held by strategy peer groups can be identified.

- Expected returns based on market preferences for strategies can be calculated.

Superior diversification relative to style boxes

A popular approach for active equity portfolio construction is to diversify across the style grid by investing in a small-cap value fund, a large-cap growth fund and so on for the nine or more style boxes. Strategy diversification is a similar concept in that you invest in funds pursuing different strategies.

Strategies provide superior diversification relative to style boxes as demonstrated in this study, which details a series of tests comparing the two frameworks. A successful formation of active equity fund peer groups should have the lowest across-group-return correlations and the highest-within-group correlations, which leads to:

- the greatest diversification when investing in funds from different groups, and

- funds within a peer group all employing a similar investment strategy.

The cross-fund correlation tests conducted demonstrate that forming peer groups based on self-declared strategy outperforms style box peer groups on both dimensions. That is, when classifying funds by strategies there is higher correlation within each strategy (reflecting commonality) and lower correlation between each strategy (reflecting differences) relative to the correlation data within and between style box categories.

Strategy-based portfolio construction

Evaluating funds in terms of self-declared strategy provides a powerful framework for constructing and managing equity portfolios. A straightforward way to build a strategy-diverse portfolio is to select a fund from each of the 10 strategies, but this approach can be improved upon by examining each strategy’s historical performance as summarized in Table 1.

Table 1: U.S. strategy statistics (1980-2017)

* As of March 2018, ignoring share classes. Sources: Morningstar and AthenaInvest

As shown, strategies have performed quite differently over time, with future growth delivering the best returns at 13% annually and risk the worst, underperforming future growth by 6%. Based on these return differences, it does not make sense to invest in all 10 strategies. I recommend limiting fund portfolios to the top six strategies: future growth and competitive position, which are the two that have outperformed the S&P 500, along with opportunity, quantitative valuation and profitability, each performing within 1% of the market.

This leaves out social considerations, market conditions, economic conditions and risk, which have all unperformed by more than 2%. Some may prefer social-impact investing, and if something other than returns is a criterion, then a social considerations fund could be included.

Market and economic conditions funds are not attractive because the information upon which these are managed is likely already captured in equity prices. Consistent with this notion, their underperformance roughly equals the average fees charged by funds.

Risk is puzzling. These funds state that they manage short-term volatility and drawdown, with return as a secondary consideration. In the latter sense, they have succeeded as they underperform the market by nearly 5%. More perplexing is that Risk is 30% more volatile than the market and earns a substantially lower return. While Risk has a strong negative rank correlation with most other strategies, it is unlikely that this diversification benefit is enough to offset the undesirable combination of higher volatility and lower return.

Performance of strategies over the business cycle

How have strategies performed over the business cycle? The strategy performance is ranked from best to worst in Table 2 based on the phase of the business cycle.

Table 2: Business-cycle strategy performance ranks (1980-2017)

Sources: National Bureau of Economic Research, Morningstar, and AthenaInvest.

Over this nearly 40-year time period, the economy expanded 76% of the months and was in one of five recessions 14% of the months. The year before a recession represented 10% of the months. For the expansion months, strategy performance ranks are similar to the long-term ranks reported in Table 1.

Future growth, competitive position, quantitative and valuation are among the top six performers regardless of where we are in the business cycle. There is a case for including these four strategies as core investments in any active equity fund portfolio. One could easily argue for including opportunity and profitability as strategic investments as well. These six strategies make up nearly 90% of U.S. active equity mutual funds, so avoiding the bottom four strategies excludes roughly 10% of available funds.

The four bottom-ranked strategies, shown in red, move up in rank only sparingly. Market conditions and risk are at the top in the year before and recession months, respectively. Economic conditions is the only strategy that never makes it into the top six.

Since it is difficult to forecast an upcoming economic downturn, there is a good argument for not including social considerations, economic conditions, market conditions and risk in a properly diversified active equity portfolio.

Strategy framework identifies best active equity funds

While past performance is not predictive of future performance, fund manager behavior is. The active equity strategies provide a framework that helps reveal important manager behaviors that lead to superior performance.

A critical fund manager behavior is the consistent pursuit of a narrowly-defined strategy. The challenge is how to measure consistency. A common approach is to demand consistent returns over time. But we know that the best funds outperform at times and underperform at others. While this is emotionally difficult for investors, it is an unavoidable fact when investing in successful active funds as strategies don’t perform well in all types of markets.

Another common approach is to demand that funds closely track their style-box benchmarks. Such funds, however, while acting like their benchmarks, underperform as demonstrated in this study. Benchmarks have little to do with a manager’s strategy so asking them to minimize tracking error is tantamount to asking them to deviate from their strategy. This is because they are being required to purchase stocks for the sake of staying in their assigned style box, rather than investing in their preferred stocks.

An alternative is to examine the type of stocks in which a manager invests. For example, is a value fund invested in value stocks or is it chasing an unrelated trend such as favoring growth stocks?

Using a more definitive process, we evaluate consistency of a manager by comparing their holdings to other managers pursuing the same strategy for a pool of stocks upon which to focus. For a manager following a competitive position strategy, for example, the pool is comprised of stocks most held by other competitive position funds.

It makes intuitive sense to use a screen driven by those who are looking for similar stock characteristics. In addition, strategy pools are in constant motion, as managers make buy and sell decisions based on ever- changing economic and market conditions. A stock stays in a particular strategy-pool for 14 months on average. (See this study for details on how strategy stock pools are created.)

Focusing on similar strategy stocks is not only intuitively appealing but it leads to better performance, as shown in this study. Figure 1 below demonstrates that the active equity funds holding the most similar strategy stocks (quintile 5 in Figure 1) outperform those holding the least by 212 basis points. This confirms the advantage of focusing on stocks most held by others following the same strategy. Collective intelligence provides valuable information.

Figure 1: Strategy consistency: 1997-2017

Sources: Morningstar and AthenaInvest

These strategy-consistency results are in stark contrast to what has been uncovered regarding style-box consistency. This study demonstrates that equity funds experiencing the largest style drift outperform those with the least by about 300 basis points. Asking a fund manager to stay style-box consistent hurts performance because it forces them to invest in stocks outside their own strategy simply to track the style benchmark. Style consistency begets strategy inconsistency and, in turn, poor performance.

High-conviction stocks

Beyond strategy consistency, there is an additional performance advantage if a fund invests exclusively in high-conviction stocks. A fund applies its investment strategy to hundreds of its own strategy stocks to come up with a manageable set of high-conviction stocks. Even though two funds might pursue the same strategy, their implementation is unique. Thus, funds pursuing the same strategy can hold quite different high-conviction portfolios.

The benefit of holding only high-conviction stocks is demonstrated in Figure 2 below. Increasing the amount invested in the top 20 high-conviction stocks (captured by the highest 20 relative weights in the portfolio) improves fund alpha, represented by the two green bars in Figure 2. Increased investment in the non-top-20 stocks hurts performance, as represented the single red bar.

Figure 2: Fund alpha improvement for increasing investment in high-conviction stocks

Based on single variable, subsequent gross fund alpha regressions estimated using a data set of 44 million stock-month equity fund holdings over Jan 2001- Sep 2014. Sources: Morningstar and AthenaInvest

Figure 2 reveals that funds display stock picking skill as evidenced by investing more money in their best idea stocks which subsequently outperform. It also reveals that the typical mutual fund holding 75 stocks (the median number of holdings) is badly over-diversified, investing in three times more alpha destroying stocks than in alpha-building stocks.

Funds that consistently pursue a narrowly defined strategy while taking high conviction positions perform best. Past performance is not part of this fund-selection process because it is not a reliable predictor. Fund behavior, in terms of consistency and conviction, however, is predictive.

Strategies can indicate expected stock market return

One of the more surprising results flowing out of our strategy research is the ability to intelligently organize the return factors driving overall market returns. It turns out that how investors are responding to the strategies provides a measure of the current expected stock market return. In turn, this information can be used for managing a portfolio’s equity exposure.

Aggregate stock market returns are driven by the collective buy and sell decisions of individual and institutional investors. Many market factors enter into investor decisions, and the relative importance of each factor evolves over time. At various times, investors will place more importance on economy-wide data, stock market activity or specific industry sectors or stocks.

When estimating overall market expected returns, it is important to know the current mix of factors favored by investors. Each of the 10 strategies introduced earlier captures a specific set of market factors. For example, competitive position (CP) fund managers focus on innovative companies, building an investment process around factors such as strong management and defensible market positions.

A strategy’s recent return rank relative to other strategies varies over time because investors collectively focus on a changing mix of factors. However, investment managers usually pursue their investment strategies regardless of whether they are in favor with investors or not. Managers keep doing the same thing while investors change their focus, which provides a stable prism for viewing what is being favored by investors at a given time.

Strategy market barometer (SMB) captures the factors currently being rewarded by investors. A high SMB means that market participants favor a high-return factor mix, while a low SMB means a low-return mix is in favor. Consequently, a high SMB implies a high expected market return, and a low SMB a low expected return.

Instead of revealing whether recent market returns have been positive or negative, SMB focuses on relative strategy return ranks. The SMB can be high or low regardless of recent market performance.

Additionally, SMB is not a traditional measure of market sentiment. Instead, it captures actual investor behavior. Strategy return ranks are the result of collective investment activity, so they reflect what investors do rather than how they feel about current market conditions. The SMB is a “put your money where your mouth is” type of measure.

Calculating a strategy market barometer

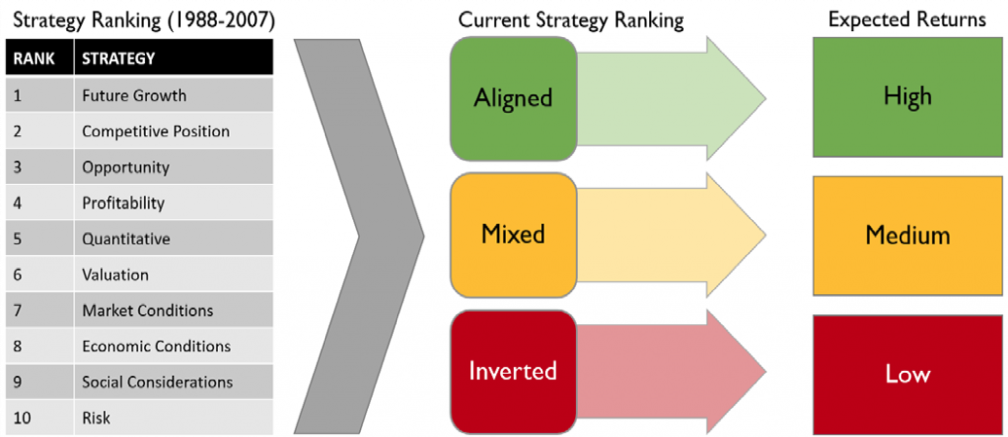

Monthly strategy index returns are calculated by averaging the monthly returns for all funds in a given strategy. The 2,000 or so US active equity mutual fund monthly returns are net of management, operating, 12b-1 and other automatically deducted fees. SMB is calculated using trailing 12-month strategy return rank absolute deviations from the 1988-2007 ranks shown in the left-hand table in Figure 3.

As can be seen, the top performing U.S. equity strategy over this 20-year period was future growth, while the bottom performer was risk. Risk underperformed future growth by 600 basis points annually over this period, consistent with the strategy performance results reported earlier.

Figure 3: Strategy Ranks and Expected Market Returns

Image AthenaInvest

Figure 3 provides a graphical representation of the relationship between strategy ranks and expected market returns. If current strategy ranks align with long-term ranks, then expected returns are high. This means investors are currently favoring strategies in the same order they have performed over the long run. More specifically, investors are favoring future rowth stocks and competitive position stocks. This is a positive sign for the market and leads to expected returns well above the 10% long-term average.

On the other hand, if ranks are inverted in relationship to long-term ranks, investors are not favoring future growth and competitive position stocks and instead are rewarding risk, social considerations, economic conditions and market conditions stocks – historically weaker strategies. This is a bad sign for the market because it indicates investors are taking a defensive position rather than focusing on long-term stock market drivers. As a result, the expected market return is weak or even negative. For example, social considerations, risk, and market conditions were top relative strategies in 2008, a bad sign for the market. And we know what happened in 2008.

Strategy ranks most often fall in between aligned and inverted and, as a result, the expected market return is somewhere around the long-term average of 10%.

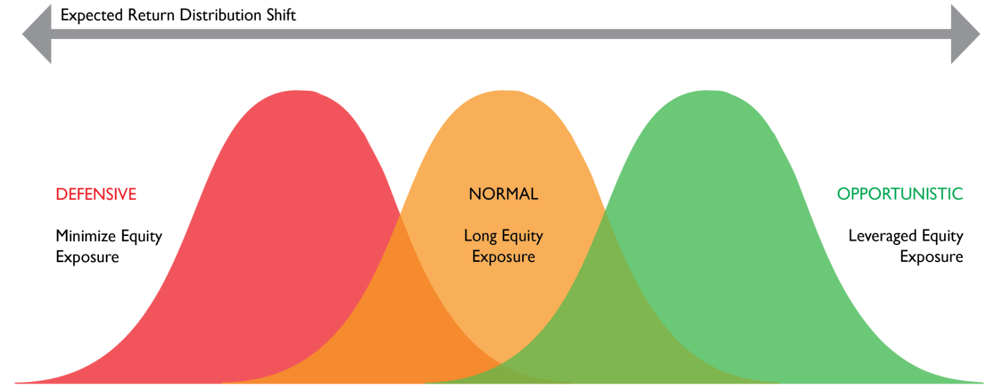

As demonstrated in Figure 4, SMB can be used to vary equity exposure from none to long to leveraged, something AthenaInvest has successfully done since 2010 with the Athena Global Tactical ETFs portfolio.

Figure 4: Return Distribution Shift Based on SMB

Image: AthenaInvest

Strategy-based investing

While the style grid takes a narrow approach to categorizing funds, peer groups based on strategy consider the actual way a manager goes about analyzing, buying and selling stocks. Shifting to a strategy-based categorization of equity managers creates statistically valid peer groups that can be used for a wide variety of applications including benchmarking, manager evaluation, fund selection, portfolio construction and tactical management.

Using this framework, we can analyze investment manager behavior and investor behavior (their preference for the strategies), both which create the building blocks of SBI.

Consider the applications from the SBI research, particularly with portfolio construction. As discussed here, strategies provide superior diversification relative to style boxes so creating a strategy-diverse portfolio should help improve returns. Additionally, the patented research behind Athena’s SMB has proven effective at driving a market rotation strategy for the Athena Global Tactical ETFs portfolio.

The research shows that manager behavior in the form of strategy consistency (measured based on the extent to which the fund holds its own strategy stocks) and high- conviction, is predictive of future performance. If a manager is not strategy-consistent and taking high-conviction positions, investors may not reap the benefits of manager skill. Instead the benefits are captured by the fund by means of growing large and transforming into a closet indexer.

C. Thomas Howard, PhD, is chief investment officer and director of research at AthenaInvest. Building upon the Nobel Prize winning research of Daniel Kahneman, Howard is a pioneer in the application of Behavioral Finance for investment management. He is a professor emeritus at the Reiman School of Finance, Daniels College of Business, University of Denver, where he taught courses and published articles in the areas of investment management and international finance. He is the author of Behavioral Portfolio Management. Howard holds a BS in mechanical engineering from the University of Idaho, an MS in management science from Oregon State University, and a PhD in finance from the University of Washington.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All