At this point in the year, we believe developed and emerging economies should continue to drive solid global growth. Corporate earnings estimates for the remainder of 2018 look strong, particularly in the United States, where tax reform looks set to add to an already durable outlook. Potential risks we are monitoring include changes in Federal Reserve (Fed) policy as well as modifications to global trade rules.

Economic Activity Has Been Improving for Years

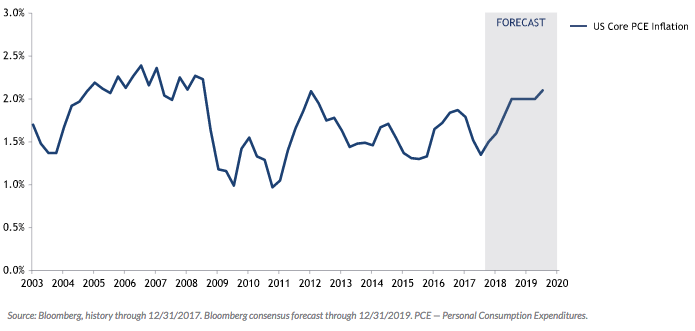

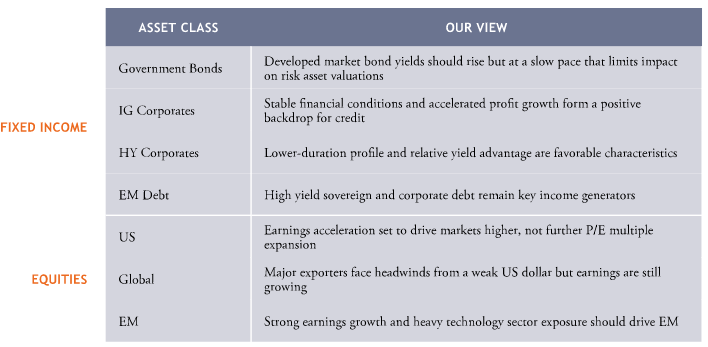

Manufacturing activity has been recovering since 2016, when a low in oil prices coincided with the end of a corporate profit recession. Looking forward, economic indicators are expected to continue strengthening. GDP growth estimates are rising and consumer confidence has continued to improve across the world. In addition, US core PCE inflation is expected to trend up steadily toward the Fed’s 2.0% target. So far, better domestic economic activity has been met with rate hikes. The US has some of the highest interest rates among developed economies and they are expected to rise further (along with those in other developed economies), albeit at a fairly slow pace that should not materially alter demand for risk assets.

INFLATION EXPECTED TO TREND TOWARD 2.0%

Narrow Credit Spreads Can Hold Steady with Stable Financial Conditions

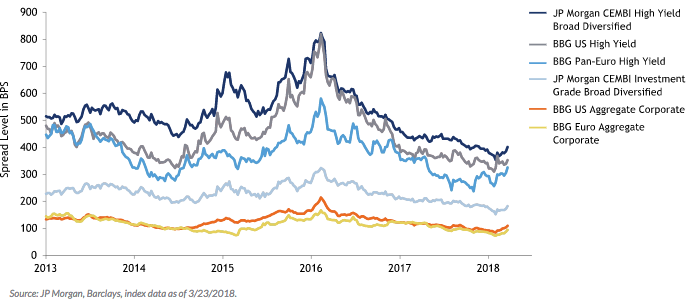

Global growth and rising profits remain key to keeping credit spreads at multi-year lows. We recognize that as the cycle advances and interest rates move higher, spreads are less likely to tighten further. However, as long as financial conditions remain stable, credit should continue to perform favorably. In a rising rate environment, lower-duration sectors of the credit market, such as high yield and asset-backed securities (ABS), may perform better than their longer-duration counterparts. Bank loans, with rates that adjust as short-term rates change, should also continue to attract investor demand in anticipation of Fed rate hikes throughout the year.

CREDIT SPREADS

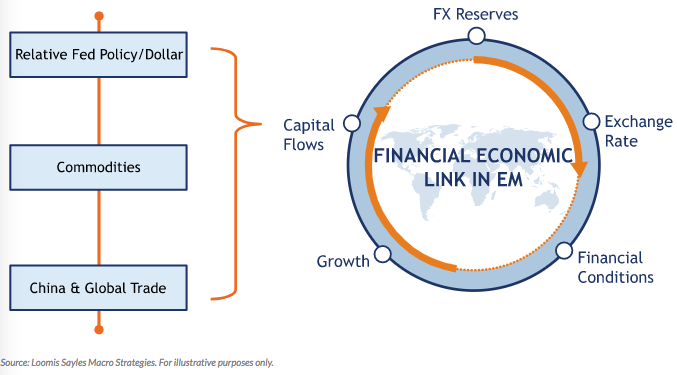

US Dollar Likely Range Bound to Weaker, Supporting EM

Investors have been moving capital into non-US assets as they seek opportunities in countries with higher economic growth than found in the US and investments with greater total return potential. This environment has fostered a weaker US dollar that generally benefits emerging markets (EM) particularly from a funding perspective. As the US dollar weakens and EM governments and companies have greater access to capital markets, they can issue debt more readily. Capital flows into emerging countries can advance fundamental improvement, which then reinforces the case for investment. With catalysts for a US dollar bull market largely absent, we find local-currency EM debt attractive given its yield advantage over other fixed income sectors. With fundamental improvement on tap in regions like Asia and Central and Eastern Europe, certain EM currencies are positioned to outperform the US dollar.

Global Equity Total Return Potential Remains Solid

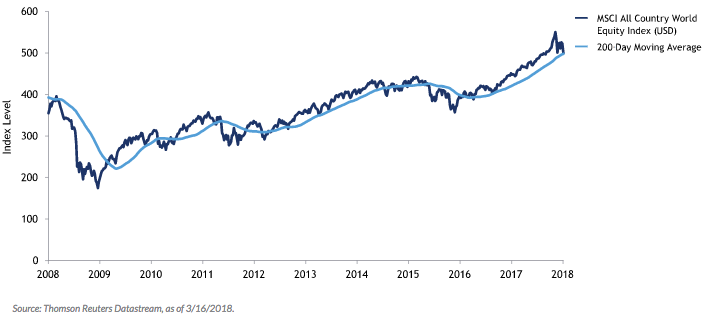

Equity markets may have gotten a little ahead of themselves in January as optimism about synchronized global growth and supportive financial conditions led to outsized gains to start the year. In January alone, the MSCI All Country World Index rallied 5.7% while the MSCI Emerging Markets Index posted an 8.3% total return. While volatility picked up recently, prospects for global equities in the quarters ahead also improved. From an earnings-per-share standpoint, we believe the S&P 500® Index is likely to show year-on-year growth of nearly 20% for 2018. Other US indices are also expected to show strong double-digit growth, boosted in part by corporate tax cuts. We expect EM earnings to grow approximately 16% this year, nearly on pace with the US. With the earnings story broadly positive, equities should find valuation support as well as a basis for potential gains. Advances fueled by price-to-earnings multiple expansion are less likely.

EARNINGS SHOULD SUPPORT EQUITY VALUATIONS

Keeping an Eye on the Risks

Looking ahead, we anticipate a fairly benign environment where many asset classes could potentially achieve modest total returns. Naturally, there are risks. If US inflation and interest rates move higher and faster than we expect, aggressive Fed tightening could lead to a flat or inverted yield curve and a premature end to the cycle. Globally, financial tightening and regulatory clampdown in China could reverse the virtuous cycle in EM and spark disinflationary pressure. Global trade wars and tariffs could disrupt technology supply chains and other import/export relationships. A case could also be made for upside surprises. For example, fiscal stimulus and generous monetary policy could contribute to a growth boom and steady reflation. Another potential source of higher-than-expected growth could result from Chinese policymakers if they effectively manage the country’s excess leverage and financial imbalances. While an environment supporting demand for risk assets should prevail, we remain vigilant in assessing the overall outlook.

Disclosure

This commentary is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis do not represent the actual or expected future performance of any investment product. Information, including that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This information is subject to change at any time without notice.

Past performance is no guarantee of future results.

Indices are unmanaged and do not incur fees. It is not possible to invest directly in an index.

LS Loomis | Sayles is a trademark of Loomis, Sayles & Company, L.P. registered in the US Patent and Trademark Office.

MALR021596