In the first edition of my book, Reverse Mortgages: How to Use Reverse Mortgages to Secure Your Retirement, I did not analyze using a reverse mortgage to support the short-term costs of delaying Social Security. But a faulty report issued by the Consumer Financial Protection Bureau (CFPB) in August 2017 claimed that using a reverse mortgage to delay Social Security is a bad idea. This report gained a lot of press coverage and is likely serving as the primary resource for people seeking to learn more about the matter. I will provide the analysis that shows why the CFPB is wrong about reverse mortgages and Social Security.

I am not philosophically opposed to the CFPB’s mandate or the regulations it has advocated. I believe in effective regulation, and have served as an intern at the Social Security Administration. My original career goal, before finding my place in academics, was to become a U.S. government economist.

But I am disappointed that this report was issued and heralded with a press release and other promotion by the CFPB.

There is a sentence in the conclusion of the report that makes sense, “For consumers who have the option, working past age sixty-two is usually a less costly way to increase their monthly Social Security benefit than borrowing from a reverse mortgage.” This is true. Delaying retirement is usually the best possible way to build stronger finances for retirement. But for those who have retired at sixty-two, what is the best way to coordinate Social Security claiming, home equity, and the investment portfolio to build an efficient overall retirement income plan?

The report failed to answer this adequately; its conclusion that the reverse mortgage is too costly was incomplete.

What the report does is to estimate the increase in total Social Security benefits (ignoring cost-of-living adjustments) obtained (assuming a life expectancy at 85) by waiting from age 62 to age 67 before claiming Social Security benefits. Technically, this is not a delay of Social Security, but just claiming at the article’s assumed full retirement age rather than claiming early. The additional benefits are compared to the costs of replacing those five years of missing age-62 benefits by taking distributions from a HECM line of credit. Reverse-mortgage costs are reflected through the upfront fees, insurance premiums, servicing costs and interest accumulated at the age-85 life expectancy. These costs are shown to be substantially higher than the net gain in Social Security benefits, leading the authors to conclude:

We find that borrowing a reverse mortgage loan to get an increased Social Security benefit carries significant costs that generally exceed the additional lifetime amount gained from delaying Social Security. In addition, the amount that a consumer will need to borrow from a reverse mortgage loan to delay claiming Social Security benefits could negatively affect the consumer’s ability to move or use their home equity to meet a large expense later in life.

These conclusions violate two of the tenets of my Retirement Researcher Manifesto. Tenet one is to play the long game. Do not base your decisions about what happens at life expectancy, but rather what happens if we live well beyond life expectancy. Delaying Social Security is a form of insurance that supports the increasing costs associated with living a long life. It provides inflation-adjusted lifetime benefits for a retiree and a surviving spouse, and these lifetime benefits will be 76% larger in inflation-adjusted terms for those who claim at 70 instead of at 62. The value of this insurance is missed when analysis only considers the impacts through life expectancy.

Second, and more importantly, the CFPB report authors have violated tenet seven, which mandates working with the entire retirement balance sheet and matching assets to liabilities. We do not know the liabilities to be funded in the CFPB report; there is no spending goal to be achieved. The report also completely ignores the possible existence of an investment portfolio to help fund retirement. If retirees have expenses to meet, they must draw from their assets. For someone retired at 62, how will expenses be met? Should retirees claim Social Security early? Or build a bridge to delay Social Security using a reverse mortgage? Or delay Social Security, but fund the delay instead through distributions from an investment portfolio? The CFPB report does not address this at all.

The report merely says that it is better to work longer and to not retire at 62. This allows expenses to be covered by labor income. Fair enough if this is the best decision to bolster finances, but it does not address what a person should do when they stop working before 70. Their notion that the costs of a reverse mortgage exceed the benefits of Social Security delay is incomplete because it does not address how to fund the spending need, other than to assume the person is still working. If retired, distributions from an investment portfolio also have a cost in terms of the lost compounding growth potential for those funds if they are spent instead of remaining in the portfolio.

Saying that reverse-mortgage use is too costly because it could hurt the ability to move or to use home equity for another expense ignores asset-liability matching for the retirement-spending goal. Meeting spending needs from the investment portfolio instead could drain net worth faster than meeting spending needs from the reverse mortgage. We have to test this to see which strategy can best preserve net worth after retirement expenses are met, so that more liquidity is available later in retirement to fund a move or other expensive shock. The CFPB report ignores both the spending goal and the investment portfolio, so it does not provide a meaningful conclusion about what a retiree at 62 should do.

Fixing the CFPB’s methodology

Properly addressing this requires a more complete analysis than the CFPB report provided. I can analyze these complexities with regard to long-term impacts and asset-liability matching by using my standard approach by developing Monte Carlo simulations that allow interest rates to start at their lower current levels, but to gradually fluctuate toward their historical numbers, on average, over time. When it comes to the Social Security-claiming decision, I consider four options for those entering retirement at age 62:

- Delay claiming Social Security benefits until age 70. Open a home-equity conversion mortgage (HECM) at age 62 and draw the equivalent amount of the age 62 Social Security benefit (without cost-of-living adjustments) from the line of credit to replace these missing benefits. Once Social Security begins at age 70, stop distributions from the HECM. In order to reduce the loan balance and transfer more of the principal limit back to the line of credit for use if the investment portfolio later depletes, make a voluntary repayment to reduce the loan balance by the amount of the original age-62 benefit without cost-of-living adjustments in years after positive market returns and when at least two years’ worth of the retirement-spending goal remains in the investment portfolio.

- Delay claiming Social Security benefits until age 70. Open a HECM at age 62 and draw the equivalent amount of the age 62 Social Security benefit (without cost-of-living adjustments) from the line of credit to replace these missing benefits. Once Social Security begins at age 70, stop distributions from the HECM. Do not voluntarily pay down the HECM loan balance. Use any remaining line of credit as a spending source if the investment portfolio depletes later in retirement.

- Delay claiming Social Security benefits until age 70. Draw the full amount of the retirement-spending goal from the investment portfolio. This requires greater distributions for the first eight years of retirement, but distributions reduce by the amount of the Social Security benefit once it begins at age 70. Only open a HECM as a last resort option to meet the spending goal if the investment portfolio depletes later in retirement.

For a case study analyzing these strategies, I shall consider a 62-year-old single individual entering retirement. She owns a home appraised at $400,000 as well as a tax-deferred retirement account with $1 million of assets. The investment portfolio uses a 50/50 asset allocation for stocks and bonds.

Her full retirement age for Social Security is 66 and at that age she is eligible for a benefit equal to $2,000 per month, or $24,000 per year. If she claims early at 62, her lifetime benefit is reduced to $18,000 per year, and if she delays Social Security to 70, her yearly benefit increases to $31,880 in inflation-adjusted terms. Without including inflation-adjustments, eight years of her age 62 Social Security benefit sum to $144,000.

Her spending goal to be covered by her investment portfolio, home equity and Social Security is $50,000 per year before taxes, and this grows with inflation. She has other pension income such that we assume for this portion of assets she is in the 25% marginal tax bracket and 85% of her Social Security benefits as well as any investment portfolio distributions will count as taxable income. I do not consider required minimum distributions from the qualified plan, which may accelerate the need to pay taxes and force some of her assets into a taxable account in simulations where markets perform well.

At retirement, she considers a HECM with a lender’s margin of 2.25% when the 10-year LIBOR swap rate is 2.25%. This analysis is based on the updated HECM rules that went into effect on October 2, 2017. For a 62-year old, these details translate into an initial principal limit factor of 43.9%, with the expected rate of 4.5%. Upfront costs include a $6,000 origination fee, an initial mortgage insurance premium of 2% of the home value, plus another $2,500 for other closing costs. These costs total $16,500, and it should be clear that this represents the full retail price in order to avoid biasing the results in favor of the reverse mortgage. For this scenario, with some shopping around, potential borrowers should be able to find opportunities to have the origination fee waived and perhaps even receive credits for a portion of the other costs. The up-front costs will be financed within the loan. This leaves a net-initial principal limit of $159,100 (400,000 x 0.439 - 16,500). In cases where the reverse mortgage is opened later, I assume the maximum eligible home value (currently $636,150) and the closing costs rise with inflation.

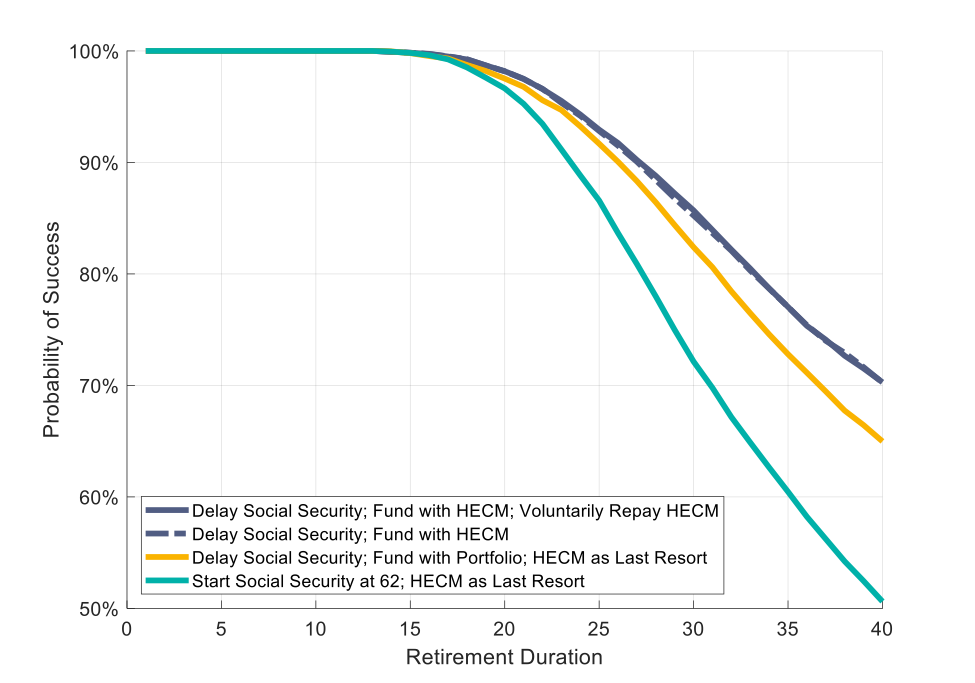

Figure 1 provides the results for this case study in terms of the ongoing probability of success in meeting the spending goal throughout retirement. Claiming Social Security at 62 and only opening the HECM as a last resort option if the portfolio depletes results in the lowest probabilities of success. There is value is spending down other resources (either investments or home equity) during the first eight years of retirement in order to enjoy a permanently higher Social Security benefit after that point.

Figure 1 Probabilities of success for Social Security-claiming strategies

Moving toward better outcomes, the next best strategy is to delay Social Security to 70 and spend from the investment portfolio in the meantime, and to then only open a HECM as a last resort option if the investment portfolio depletes. Thirty years into retirement, delaying Social Security has raised the probability of success from 72% to 82%. Higher distributions needed in the first eight years of retirement are more than offset by the larger benefits subsequently available at age 70, such that the overall probability of success increases.

Next, the two strategies supporting the highest success rates both involve delaying Social Security and funding the delay through distributions from a HECM rather than distributions from the investment portfolio. This affirms that even after accounting for the full retail costs of setting up a reverse mortgage, its ability to help reduce sequence risk for the portfolio by providing a way to delay Social Security without needing to take larger distributions from the portfolio provides greater net advantages. It is interesting that voluntarily paying down reverse mortgage debt after age 70 to transfer a portion of the growing principal limit from loan balance to line of credit does not have a noticeable impact on success rates. After 30 years, both strategies have raised the success rate for this spending goal to about 85%.

We can also consider legacy wealth. This is the value of legacy assets (a bequest) available to heirs. It is defined as any remaining portfolio assets after taxes plus any remaining home equity after the reverse mortgage loan balance has been repaid. If spendable assets are depleted (the portfolio and the entire line of credit) such that the full spending goal cannot be met, legacy values are counted as negative by summing the total spending shortfalls that would manifest either as reduced spending or as a need to rely on ones’ heirs for additional support as a form of “reverse legacy.” This addition of a negative legacy makes results more meaningful because it clarifies the magnitude in which a spending goal cannot be achieved. Legacy values are shown on an after-tax basis assuming that the same 25% marginal tax rate applies to portfolio assets, though the possibility of any tax deductions available to heirs upon repaying the HECM loan balance are not considered.

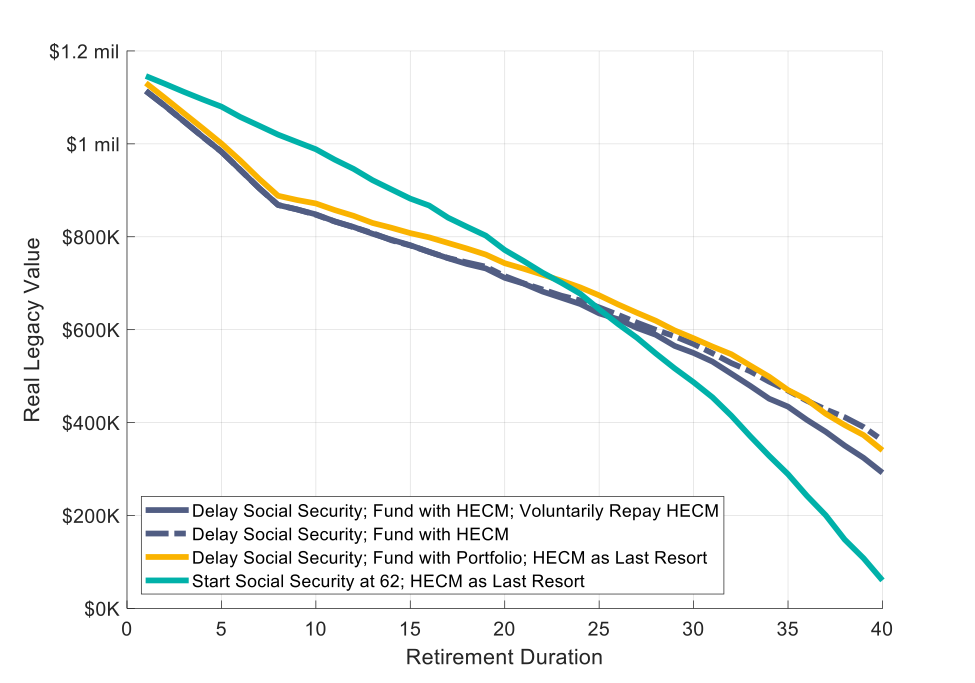

Figure 2 shows the legacy value of assets at the median outcome. This means that in 50% of cases legacy values will be less than shown, while in 50% of cases legacy values will be greater than shown. The median reflects an average or typical outcome. Claiming at age 62 supports a greater legacy until about 20-25 years in retirement (ages 82-87). After that time, delay strategies all help to support greater legacy because the higher Social Security benefits help to dramatically reduce other distribution needs. Using the portfolio to delay does come out slightly ahead, but the reverse mortgage strategies remain competitive. The possibility for lower up-front costs on the reverse mortgage may close much of this gap. Compared to claiming at 62, which the CFPB report seemingly endorses in the absence of a full analysis, Social Security-delay strategies help dramatically to support legacy for longer and costlier retirements when dollars of legacy will have a bigger impact for heirs.

Figure 2 Median real legacy value for Social Security-claiming strategies

An unlucky outcome is represented by the 10th percentile for legacy wealth. Portfolio returns are poor and the financial portfolio is quickly depleted. I have not included an exhibit to show this case, because it looks similar to the median case, except that wealth depletion happens sooner. Claiming at 62 depletes available assets by age 88, along with a smaller Social Security benefit after that point as a remaining source for retirement income. Using a reverse mortgage to fund Social Security delay can help support the full spending goal for another year, and funding delay by spending from the investment portfolio helps support the full spending goal until age 91. With these delay strategies, the Social Security benefit provides 76% more spending power after the investment portfolio and home equity are no longer able to contribute to retirement spending.

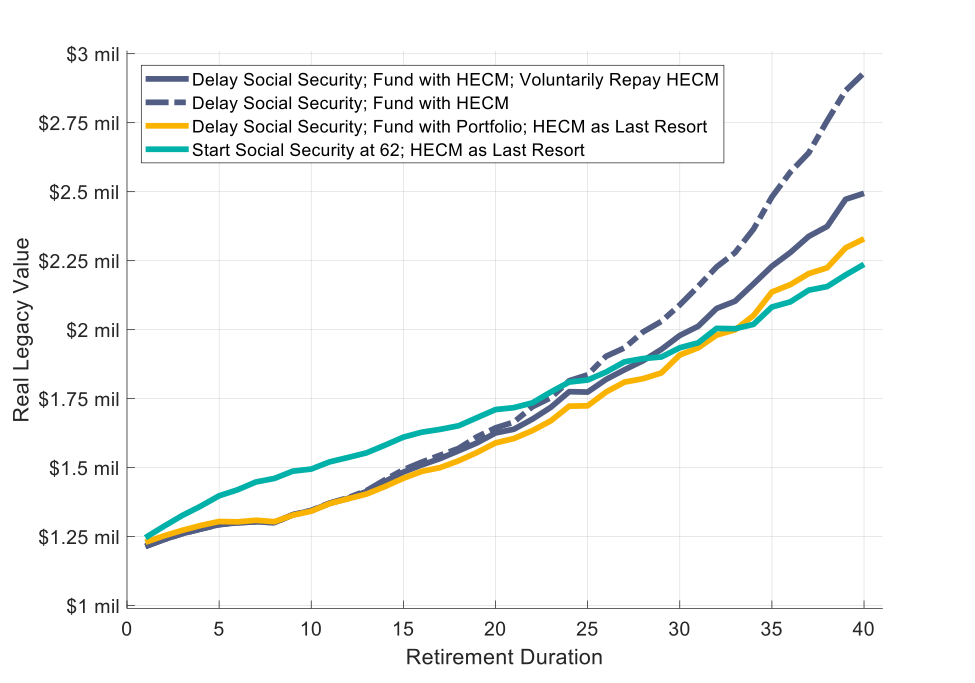

As for the 90th percentile, the investment portfolio performs well and distributions can continue indefinitely without depleting the portfolio. The 90th percentile for legacy values is shown in Figure 3. For these positive outcomes, the investment portfolio is able to grow at a faster rate than the principal limit, and so retirees over the long-term are able to benefit by keeping more assets in their investment portfolio by spending from the HECM more quickly. The higher subsequent portfolio value more than offsets the growing loan balance for the HECM. Claiming at age 62 supports more legacy for about 25 years. Over the long term, funding Social Security delay with the HECM supports greater legacy, followed by funding delay through the investment portfolio.

Figure 3 90th percentile legacy value for Social Security-claiming strategies

The bottom line

Contrary to conclusions made in the CFPB report, there is value in delaying Social Security and spending down other resources in the interim. Spending from a HECM or an investment portfolio are both viable options, and lead to a higher probability of success and a greater legacy value for assets over the long-term. Using a HECM to fund Social Security delay does not create greater risk for retirees experiencing spending shocks or needing to move later in retirement, because reduced distribution needs from the investment portfolio and the subsequent reduction in sequence risk offset the reverse-mortgage costs and preserve overall net worth.

Wade D. Pfau, Ph.D., CFA, is a professor of retirement income in the Ph.D. program in financial services and retirement planning at The American College in Bryn Mawr, PA. He is also a principal and director at McLean Asset Management and the Chief Planning Scientist for inStream Solutions. He actively blogs at RetirementResearcher.com. See his Google+ profile for more information.

Read more articles by Wade D. Pfau