Eight key messages and themes have underscored my writing and research. Those guidelines serve as a manifesto for my approach to retirement income planning:

-

Play the long game. A retirement income plan should be based on planning to live, rather than planning to die. A long life will be expensive to support, and it should be the focus. Fight the impatience that would lead one to choose short-term expediencies carrying greater long-term cost. This does not mean, however, that one sacrifices short-term satisfactions to plan for the long-term. There are many efficiencies that can be gained from a long-term focus that can support a higher sustained standard of living for as long as one lives. One still has to plan for a long life, even when rejecting strategies that only help in the event of a long life. Remember, planning to live to life expectancy is quite risky; half of the population will live longer than this. Planning to live longer means spending less than otherwise. Developing a plan that incorporates efficiencies that will not be realized until later can allow for more spending today in anticipation of those efficiencies. Not taking such long-term efficiency-improving actions will lead to a permanently reduced standard of living. The implication is more conservative lifetime spending in order to preserve assets for the long-term as a fix for the planning inefficiencies.

Some strategies I have discussed that focus on building a long-term plan over accepting short-term expediencies include the following: delaying the start of Social Security benefits, purchasing a single-premium immediate annuity (SPIA), paying a bit more taxes today in order to enjoy more substantial tax reductions in the future, making home renovations and living arrangements with the idea of supporting aging in place, setting up a plan that accounts for the risk of later cognitive decline that makes it harder to manage one’s finances with age and opening a line of credit on a reverse mortgage. These strategies may not make much sense if the planning horizon is only a couple of years, but they make a great deal of sense for someone building a sustainable long-term retirement income plan.

-

Do not leave money on the table. The holy grail of retirement income planning is finding strategies that enhance retirement efficiency. I define efficiency such that if one strategy simultaneously allows for more lifetime spending and/or a greater legacy value for assets relative to another strategy, then it is more efficient. Efficiency does have to be defined from the perspective of how long one lives. Related to point (1), there can be a number of strategies that enhance efficiency over the long-term (but not necessarily over the short term) with more spending and more legacy. One simple example for tax planning is taking IRA distributions or harvesting capital gains to the point that the marginal tax rate leaves the 0% tax bracket could help to reduce future taxes without any present cost.

-

Use reasonable expectations for portfolio returns. A key lesson for long-term financial planning is that you should not expect to earn the average historical market returns for your portfolio. The average is just that; half the time it is more and half the time less. Beyond this, we have been experiencing a period of historically low interest rates, which unfortunately provides a clear suggestion that at least bond returns are going to be lower in the future. This has important implications for those who have retired (these implications are relevant for those far from retirement as well, but the harm of ignoring them is less than for retirees). At the very least, dismiss any retirement projection based on 8% or 12% returns, as the reality is likely much less when we account for portfolio volatility, inflation, a desire to develop a plan that will work more than half the time and today’s low interest rates. As a corollary to this point, while low interest rates generally make retirement more expensive, there are some strategies that are made more attractive by low interest rates, such as delaying Social Security or opening a reverse mortgage.

4.

Be careful about plans that only work with high market returns. A natural mathematical formula that applies to retirement planning is that higher assumed future market returns imply higher sustainable spending rates. Bonds provide a fixed rate of return when held to maturity, and stocks potentially offer a higher return than bonds as a reward for their additional risk. But this ”risk premium” is not guaranteed and it may not materialize; it is risky. Retirees who spend more today because they are planning for higher market returns than available for bonds are essentially “amortizing their upside.” They are spending more today than justified by bond investments, based on an assumption that higher returns in the future will make up the difference and justify the higher spending rate.

For retirees, the fundamental nature of risk is the threat that poor market returns triggers a permanently lower standard of living. Retirees must decide how much risk to their lifestyle they are willing to accept. Assuming that a risk premium on stocks will be earned, spending more today is risky behavior. It may be reasonable behavior for the more risk tolerant among us, but it is not a behavior that will be appropriate for everyone, and it is important to think through the consequences of this in advance.

5.

Build an integrated strategy to manage various retirement risks. Building a retirement income strategy is a process that requires a determination for how to best combine available retirement income tools in order to meet retirement goals and to effectively protect against the risks standing in the way of those goals. Retirement risks include longevity and an unknown planning horizon, market volatility and macroeconomic risks, inflation and spending shocks that can derail a budget. Each of these risks must be managed by combining different income tools with different relative strengths and weaknesses for addressing each of the risks. There is no single solution that can cover every risk, though some financial products have been marketed as such.

6.

Approach retirement income tools with an agnostic view. The financial services profession is generally divided between two camps: those focusing on investment solutions and those focusing on insurance solutions. Both sides have their adherents who see little role for the other side. But my research shows that the most efficient retirement strategies require an integration of both investments and insurance. It is potentially harmful to dismiss subsets of retirement income tools without a thorough investigation of their purported role. In this regard, it is wrong to describe the stock market as a casino, to lump SPIAs together with every other type of annuity, to not have a better understanding of different annuity products and to dismiss reverse mortgages without any further consideration.

For the two camps in the profession, it is natural to accuse the opposite camp of having conflicts of interest that bias their advice, but each side must reflect on whether their own conflicts color their advice. On the insurance side, the natural conflict is that an insurance agent receives commissions for selling insurance products and only needs to meet a requirement that their suggestions are suitable for their clients. On the investments side, those charging for a percentage of assets they manage naturally wish to make the investment portfolio as large as possible, which is not necessarily in the best interests of their clients who are seeking sustainable lifetime income. Meanwhile, those charging hourly fees for planning advice naturally do not wish to make their recommendations so simple that it foregoes the need for an ongoing planning relationship. It is important to overcome these hurdles and to rely carefully on what the math and research show. This requires starting from a fundamentally agnostic position.

7.

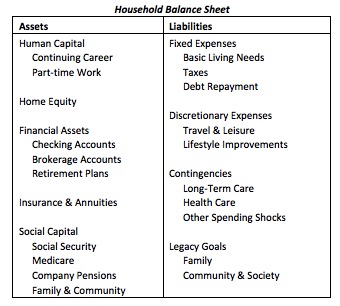

Start with the household balance sheet. A retirement plan involves more than just financial assets. The household balance sheet is the starting point for building a retirement income strategy. This has been a fundamental lesson from various retirement frameworks, such as Jason Branning and M. Ray Grubbs’ Modern Retirement Theory, Russell Investments’ Funded Ratio approach and the Household Balance Sheet view of the Retirement Income Industry Association. At the core of these different methodologies is a desire to treat the household retirement problem in the same way that pension funds treat their obligations. Assets should be matched to liabilities with comparable levels of risk. This matching can either be done on a balance sheet level, using the present values of asset and liability streams, or it can be accomplished on a period-by-period basis to match assets to ongoing spending needs. Structuring the retirement income problem in this way makes it easier to keep track of the different aspects of the plan and to make sure that each liability has a funding source. This also allows a retiree to more easily determine whether they have sufficient assets to meet their retirement needs, or if they may be underfunded with respect to their goals. This organizational framework also serves as a foundation for deciding on an appropriate asset allocation and for seeing clearly how different retirement income tools fit into an overall plan.

The following table provides a basic overview of potential assets and liabilities on the household balance sheet.

8.

Distinguish between technical liquidity and true liquidity. An important implication from the household balance sheet view is that the nature of liquidity in a retirement income plan must be carefully considered. In a sense, an investment portfolio is a liquid asset, but some of its liquidity may be only an illusion. Assets must be matched to liabilities. Some, or even all, of the investment portfolio may be earmarked to meet future lifestyle spending goals. Curtis Cloke describes this in his Thrive University program as allocation liquidity. A client is free to reallocate their assets in any way they wish, but the assets are not truly liquid because they must be preserved to meet the spending goal. This is different from free-spending liquidity, in which assets could be spent in any desired way because they are not earmarked to meet existing liabilities. While a retiree could decide to use these assets for another purpose, doing so would jeopardize the ability to meet future spending. In this sense, these assets are not as liquid as they appear.

True liquidity emerges when there are excess assets remaining after specifically setting aside what is needed to meet all of the household liabilities. This distinction is important because there could be cases when tying up part of one’s assets in something illiquid, such as a SPIA, may allow for the household liabilities to be covered more cheaply than could be done when all assets are positioned to provide technical liquidity. In simple terms, a SPIA which pools longevity risk may allow lifetime spending to be met at a cost of 20 years of the spending objective, while self-funding for longevity may require setting aside enough from an investment portfolio to cover 30-40 years of expenses. Because risk pooling and mortality credits allow for less to be set aside to cover the spending goal, there is now greater true liquidity and therefore more to cover other unexpected contingencies without jeopardizing core-spending needs. Liquidity, as it is traditionally defined in securities markets, is of little value as a distinct goal in a long-term retirement income plan.

The bottom line

Retirement income planning is a relatively new field that differs from traditional wealth accumulation. The combined impact of retirement risks is that retirees experience reduced capacity to bear financial market risk once they have retired. They also must meet spending goals by taking distributions from their asset base. This calls for more integrated strategies that take into consideration the eight key ideas I have presented.

Wade D. Pfau, Ph.D., CFA, is a professor of retirement income in the Ph.D. program in financial services and retirement planning at The American College in Bryn Mawr, PA. He is also a principal and director at McLean Asset Management, helping to build model investment portfolios that can be integrated into comprehensive retirement income strategies. He actively blogs at RetirementResearcher.com. See his Google+ profile for more information.

Read more articles by Wade D. Pfau