Investors Do Not Underperform their Investments

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDALBAR’s response to this article appears at the end of this article.

For 23 years DALBAR, Inc. has been publishing a research report reaching the conclusion, year after year, that investors underperform the investment vehicles that they invest in due to “poor investor decision making.” Wade Pfau recently discovered, however, that this conclusion is the result of a serious calculation error. Now, using Pfau’s results, I will prove that the evidence actually shows that investors do not underperform their investments.

I will first explain DALBAR’s error and then show, using two examples, how serious the error is. Second, I will describe the conventional wisdom that DALBAR’s error created, and how deeply entrenched it is. Third, I will explain why this received wisdom should have been the subject of skepticism in the first place. Fourth, I will show why Morningstar’s apparent confirmation of the conventional wisdom is mistaken. Finally, I will discuss another interpretation of poor investment decision making, and what it may mean.

DALBAR’s error

A little over a year ago, I sent an email to DALBAR asking for documentation about how their “investor return” is calculated. A DALBAR representative named Cory Clark sent back a two-page pdf file titled, “QAIB Methodology_2016.” I have since discovered that these same two pages are also included in DALBAR’s Quantitative Analysis of Investor Behavior (QAIB) report, under the heading “Investor Return Calculation: An Example.”

These two pages provide a very simple description of a calculation in six steps: (1) compute monthly change in assets; (2) compute change in market value; (3) calculate totals for period (summing the months); (4) determine cost basis; (5) calculate investor return percentage; and (6) find annualized rate of return.

I thought that this write-up was much too simple and was obviously not the whole specification of their calculation methodology. So I wrote back to Clark asking if he could provide me with more precise formulas. He replied, “This is the most detailed description that is available to the public. Anything beyond what is in this document we consider proprietary in nature.”

I am always wary of “proprietary” calculations; therefore, this just raised my level of suspicion. But I did not pursue the matter further at the time.

Then, in March of this year, Pfau published his article in which he reverse-engineered DALBAR’s calculation, based on the results in a section of their QAIB report titled “Systematic Investing.”

Soon after, I realized that the calculation that Pfau discovered DALBAR was using was actually the same as the calculation in their simple two-page write-up. Nobody with any knowledge, however, would believe they were really using that formula, because it is so far off base.

The fatal flaw in the formula lies in step 5, “Calculated Investor Return Percentage.” This step is described as follows: “Dividing the investor return dollars calculated in Step 3 by the cost basis in Step 4 give the total investor return percentage.”

In other words, the sum of market changes in assets is divided by the sum of the cost basis of those assets to get investor return.

This formula is correct only if all of the net contributions were made at the beginning of the period. Otherwise, in almost all cases, it will result in a percentage return that is much too low.

Two examples of DALBAR’s incorrect calculation

Example 1: Suppose you invest $1,000 on day one of a two-year period and let it ride for a year. You are lucky enough that your investment vehicle achieves a 20% return in that year; so at the end of the year you have $1,200.

Then at the beginning of year two, you contribute another $1,000. Now you have $2,200. You let that ride for all of year two. Once more you are lucky because your investment vehicle again returns 20% for the year. Your $2,200 therefore increases by $440. At the end of year two you have $2,640.

Your investment vehicle clearly had a 20% annualized return – and so did you.

But DALBAR’s calculation says your investor return was 14.9%, not 20%. DALBAR would therefore conclude that you underperformed your investment vehicle because of your poor decision making.

Here’s how the 14.9% return is calculated using DALBAR’s methodology. They take your market gains of $200 in the first year and $440 in the second year and add them, getting $640. Then (Step 5) they divide the $640 market gains by the $2,000 cost basis to get 32%, your un-annualized “investor return.” They then annualize this to get a 14.9% annualized investor return – which is much less than the 20% annual return achieved by your investment vehicle.

Example 2: I include this example over a 20-year period because DALBAR’s results are often reported over a 20-year period. Suppose an investor saves $1,000 at the beginning of each month for 20 years, and suppose that the investment vehicle the investor invests in realizes a steady 10% annual return (about 0.8% monthly).

The amount contributed over the 20 years – 240 months – is therefore $240,000. A simple spreadsheet calculation shows that the sum of the gains due to market increases over those 240 months is $483,987.

Dividing $483,987 (the sum of the changes in market value) by $240,000 (the sum of the cost bases) yields an un-annualized “investor return” for the 20 years of 101.66%. This annualizes to 3.57% annually.

DALBAR would conclude from this that the investor underperformed her investment vehicles’ return of 10% by 6.43% – the difference between 10% and the “investor return” of 3.57%.

This is obviously deeply wrong. The investor did nothing but invest the same monthly amount during a 20-year period, and receive the same monthly return every month.

The mistaken but deeply entrenched conventional wisdom that DALBAR created

As incredible as it is, or should be, this error was undetected for 23 years. The results reported by DALBAR based on this error have become the conventional wisdom. Almost everybody in the financial world believes that investors underperform because they behave irrationally, getting in and out of the market at the wrong times – panicking after a drop and getting out, and becoming greedy and envious after a rise and getting in.

This has even been taken to the extreme in Carl Richards’s cute drawing shown below.

In this drawing, the investor not only gets into the market after a rise and out of it after a drop, the investor somehow manages to do these things at precisely the worst times. Most of the financial advice community has convinced itself – and has convinced most other people – that investor irrationality has this insidious effect.

Why that conventional wisdom should have been a subject of skepticism in the first place

But this should never have been so easily believed. The wonderful Upton Sinclair quote, which began to circulate widely after the 2007-2009 financial crisis, “It is difficult to get a man to understand something when his salary depends on his not understanding it,” has a corollary: “It is difficult to get a man not to believe something when his salary depends on his believing it.”

This corollary has done wonders for DALBAR’s business, which is based on a grossly incorrect calculation, and for DALBAR’s clients, financial advisors. Advisors can use it to “prove” that investors behave irrationally and need help.

There are two reasons why this should have been questioned right from the beginning, when DALBAR released its first report.

The first derives from efficient market theory, specifically its random walk implications. Even without efficient market theory, the patterns of price movements so closely resemble a random walk, and their unpredictability so fits the mathematical characteristics of a random walk, that price changes would still have been hypothesized to follow a random walk.

But if prices follow a random walk, then it is about equally likely that after a sharp drop in market price the price will continue to drop as that it will rise; and about equally likely after a sharp rise that the price will continue to rise as that it will reverse.

Therefore, if an investor gets out of the market after a drop for fear that it will drop some more, about half of the time that investor will be right. And if an investor gets into the market after a rise in the belief that it will rise some more, again, about half the time that investor will be right.

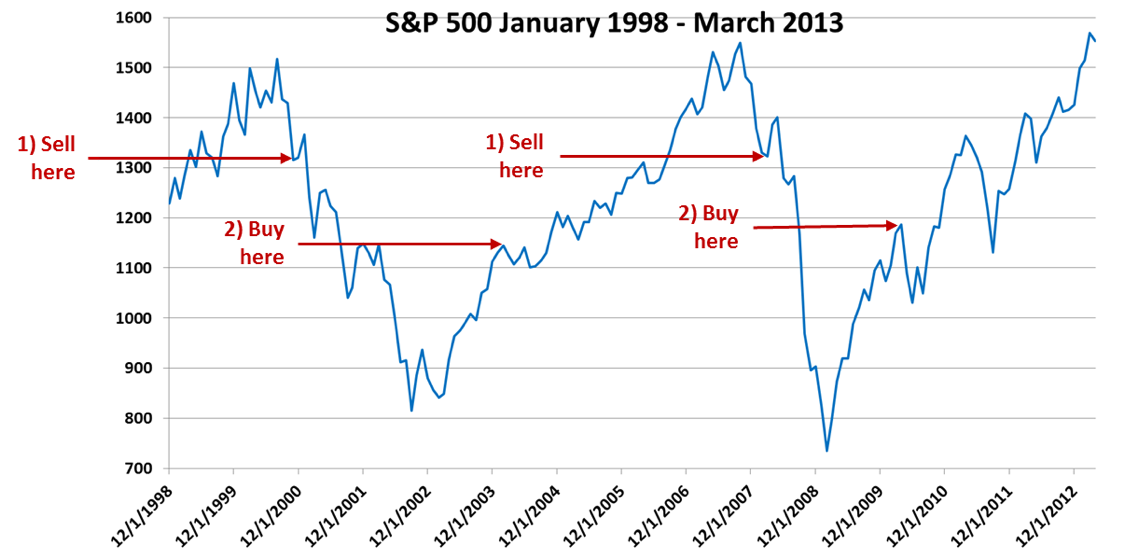

The scenario depicted in the following graph of S&P 500 levels from January 1998 to March 2013 is, in fact, much more likely than the one in Richards’s drawing.

In this scenario, the investor sells in a panic twice after sharp drops in 2000 and 2007, and reenters the market after sharp rises in 2003 and 2009 – classically irrational behavior, according to modern conventional wisdom. And yet this investor sold at higher prices than she bought and therefore made out well – because in both cases after she sold, the market went down more, and after she bought, the market went up more.

Thus, the decisions to buy and sell may have been motivated by irrational greed and fear, but thanks to the market’s random patterns, the investor may have been as likely to get lucky by buying low and selling high as the opposite.

The second reason why DALBAR’s conclusions should have been challenged from the get-go is the “aggregation” argument. If investors make bad decisions by buying at the wrong times and selling at the wrong times, who are the investors on the other side of their trades? For every investor that buys at the “wrong” time there is an investor on the other side of the trade who sells at the “right” time, and for every investor that sells at the “wrong” time there must be an investor on the other side of the trade that buys at the “right” time.

It is not possible that all investors underperform their investments by buying and selling at the wrong times. In fact, about half the well- or poorly-timed trades must be at the “right” time and half at the “wrong” time.

Then if – let us say – all individual investors in mutual funds in aggregate (the ones evaluated by DALBAR and Morningstar) are poor decision makers, who are the good decision makers that are always on the other side?

There is no evidence that there is such a group of consistently good decision makers. As is well known, for example, institutional investors in aggregate beat the market no more frequently than individual investors in aggregate. So this consideration alone should have been enough to cast doubt on DALBAR’s conclusions.

Why Morningstar’s confirmation of the conventional wisdom is mistaken

Morningstar, Inc., has for some time been making its own calculations to measure the “gap” between investment return and investor return. To its credit, Morningstar publishes its calculation methodology for anyone to see. Its approach is to calculate the usual time-weighted return for the investment vehicles that investors invest in, but to use the dollar-weighted return (also called internal rate of return, or IRR) to calculate investor return.

The dollar-weighted return is believed to combine the evaluation of an investor’s investments with that of the timing of cash flows into and out of those investments. This is why time-weighted return was recommended over dollar-weighted return as the means of evaluating pension fund managers’ performance, in a study by the Bank Administration Institute in 1968 – because it was assumed that pension fund managers should be evaluated based on the performance of their investments alone, not on the timing of the cash flows into and out of the funds they manage.

Hence, it would seem to make sense to assume that since the time-weighted return evaluates the performance of the investments alone, while the dollar-weighted return evaluates the performance of the investments and the fortuitousness of the timing of cash flows combined, therefore the difference between dollar-weighted return and time-weighted return constitutes an evaluation of the timing of the cash flows alone.

But this inference is too swiftly made, as we shall see in a moment.

Morningstar’s results do in fact show a shortfall of investor return defined by dollar-weighted return, as compared with investment return defined by time-weighted return. Where Morningstar goes too far, however, is in implying that bad investor behavior causes it.

In its “Mind the Gap 2016” report (requires registration), Morningstar found that for U.S. equity mutual funds over the 10 years ended December 2015, the gap between investment return and investor return was 74 basis points, or 0.74%. Morningstar inferred from this that “investor returns fall short of a fund's stated time-weighted returns because, in the aggregate, people tend to buy after a fund has gained value and sell after it has lost value.”

But Pfau, in his paper, also calculated what investor return would have been if an investor in the S&P 500 had merely added the same amount to her investment portfolio every year. His finding was that for 20-year periods in the last 32 years, the S&P’s return beat the investor return by an average of 1.81% – more than one percent greater than Morningstar’s 2016 “gap.”

This was merely historical happenstance, due to the sequences of returns in those time periods. In many, earlier, periods, Pfau found that the investor return would have beaten the investment’s return. But it is enough to invalidate Morningstar’s interpretation, which is based on data for the recent time periods.

What about the poor decision simply to be out of the market?

There is a slightly different reason to blame investors for underperformance. When they panic and bail out of the stock market after a decline, they usually invest in low-yielding assets instead. This means that over time, they are less than 100% invested in the asset that has the superior long-run expected return.

This is not a critique of their “poor decision making” by getting in and out of the market at the wrong times, but of their poor decision making by getting out at all. If the stock market truly is a random walk, then you’ll maximize your expected return by being in it 100% of the time – any less than that produces a lower expected return, no matter when you get in or out.

But what if the investor doesn’t want to take the risk of being 100% in the market 100% of the time? Typical asset allocation advice doesn’t recommend that for most investors; it recommends a mix of stocks and lower-expected-return fixed income, such as a 60/40 mix. It is then assumed that the investor adheres to that mix by rebalancing periodically.

Why would it not be an equally good strategy to be 100% in the market 60% of the time, and 100% in fixed income 40% of the time? Let us suppose that this did not mean jumping back and forth constantly, but, say, staying six years 100% invested in stocks and then four years 100% invested in fixed income.

My random walk intuition causes me to conjecture that a Monte Carlo simulation of such a strategy would yield the same probability distribution of ending wealth, or nearly the same, as would a 60/40 constant mix.

But the six-year / four-year strategy might be more comfortable for the investor. For example, the investor might stay in the market for six years as long as things seemed on an even keel, then get out for four years as soon as she got nervous.

Those indoctrinated by the fallacious DALBAR results will think this is the very worst possible strategy. But if you believe that market prices follow a random walk – and if you believe the Monte Carlo simulation that I have little doubt would produce the results that I have conjectured – then the strategy will not seem so bad.

This opens up avenues for future research, both behavioral (are investors more comfortable with this risk-hedging strategy?) and quantitative. It should be taken seriously.

Economist and mathematician Michael Edesess is adjunct associate professor and visiting faculty at the Hong Kong University of Science and Technology, chief investment strategist of Compendium Finance, adviser to mobile financial planning software company Plynty, and a research associate of the Edhec-Risk Institute. In 2007, he authored a book about the investment services industry titled The Big Investment Lie, published by Berrett-Koehler. His new book, The Three Simple Rules of Investing, co-authored with Kwok L. Tsui, Carol Fabbri and George Peacock, was published by Berrett-Koehler in June 2014.

DALBAR’s Response

On October 9, 2017, Advisor Perspectives received the following response from Louis S. Harvey, the CEO of DALBAR:

Response to Edesess Article in Advisor Perspectives

If this was a first offense and had no visibility, I would laugh it off as uninformed rambling. But this is not the first offense and the article has gained some credibility by being carried in a respected publication.

This is not a laughing matter, but a serious threat to all who seek to act in the best interest of investors.

The underlying premise of the article as carried in its headline is that “Investors do not underperform their investments”. The article promotes the notion that investor performance is as good as it can be and gives an absurd reason for any belief to the contrary… a fictional error in a DALBAR calculation.

All who champion the cause of improving investor returns must rise up to challenge this nonsensical conclusion and the preposterous and false argument on which it is based. The facts of underperformance are published on DALBAR’s Website, www.DALBAR.com/QAIB .

The conclusion that “Investors do not underperform their investments” flies in the face of the basics of mutual funds. These basics make it impossible for any more than 1% of investors to ever outperform an applicable index and causes the average investor to lag that index by several percentage points. The author and anyone who chooses to believe this absurd conclusion should understand the myriad of performance limiting factors that guarantees that over 99% of investors have and will underperform indices:

- Non-uniform acquisition and withdrawal dates… performance is measured over specific time periods but investors transact on every business day

- Sales charges (loads, 12-1 fees, redemption fees, etc.) are not included in the calculation of benchmark returns

- Operating expenses that pay for the management, operations and distribution of investments are not factored

- Portfolio trading costs that are incurred every time a fund buys or sells a security are absent from indices that trade “free”

- Asset allocations into low performing asset classes such as cash and other defensive investments

- Dividends and capital gains taken in cash are excluded since indices assume that all distributions are reinvested

- Leakage from loans, margin interest, fees or other deductions never occur in an index

- Opportunity cost of being out of the market during periods of appreciation is never experienced by an index which is assumed to always be fully “invested”

- Investor trading activity ebbs and flows unlike an index that reflects a buy and hold posture

- Psychological factors such as loss aversion, herding and excessive optimism do not influence the benchmarks

- The irrational belief that higher prices (expenses) will yield better investments is derived from consumerism where the expectation is that prices in some way reflect value

The theory that most investors actually earn benchmark level returns is in contradiction to the fact that the balances in their individual accounts show underperformance.

If investors did earn index level returns, there would be no point in educating and advising them or creating solutions that improve performance. In other words, the work that the investment community and DALBAR have done to bring investor performance closer to index level returns would have been pointless since “investors do not underperform”. This supposition is contradicted by the fact that investor performance has significantly improved over the two decades since DALBAR’s analysis has been published.

Furthermore, there is the economic absurdity that the revenue generated within the financial community is created without a net loss of investor returns. Compensation received by the entire financial community is derived from investors.

Claiming to have discovered a (non-existent) calculation error in DALBAR’s methodology and blaming this for the general acceptance that investors underperform applicable indices is ridiculous on its face, in addition to being false.

The author goes on to accuse Morningstar of being a co-conspirator in this alleged massive fraud. Morningstar stands accused of quantifying one of the causes of investor underperformance. This implausible theory of a conspiracy underscores the absurdity of the article.

For the record, QAIB uses the actual balances in investor accounts each month to calculate investor profits or loss after all performance limiting factors are considered. This reflects the personal return that the average investor would see on a statement. Representations to the contrary are false. Additional research is used to identify solutions that reduce the underperformance. A compendium entitled Managing Investor Behavior that covers two decades of such solutions was recently published and is available from DALBAR.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All