The Role of Money in Financial Crises

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAdvisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

What causes financial crises? Unfortunately, as I wrote elsewhere (see here), mainstream macroeconomists have very little to say about the subject, given their decision to ignore the role of money, credit and finance. This error has a long history that can be traced back to the works of Adam Smith, Jean Baptiste Say and John Stuart Mill.

In its current incarnation, money is treated as a “veil” over the real economy and is thus viewed as irrelevant based on the belief that it is a commodity and banks are only intermediaries between savers and borrowers. However, as the Bank of England (2014) and others have recognized, this view is factually incorrect. In the real world, banks create credit (and, given double-entry bookkeeping, deposits, which are money).

As a result of this error, mainstream macroeconomics (as espoused by Krugman, Bernanke, et al.) did not anticipate the crisis in 2008. Here is a disturbing comment issued by Robert Lucas, a Nobel Prize winner and former president of the American Economics Association in defense of mainstream macroeconomic models in The Economist Magazine in 2009:

The charge is that the forecasting model failed to predict the events of September 2008. Yet the simulations were not presented as assurance that no crisis would occur, but as a forecast of what could be expected conditional on a crisis not occurring.

Andrew Haldane, with the Bank of England, responded that:

This is no defense. Economics is important because of the social costs of extreme events. Economic policy matters precisely because of these events. If our models are silent about these events, this jeopardizes the very thing that makes economics interesting and economic policy important.

Yet, little has been (or can be) done to rectify mainstream models, known as dynamic stochastic general equilibrium (DSGE) models. As Paul Roomer, former professor of economics at New York University, who now works as chief economist at the World Bank (and is therefore, in his own words, liberated from the constraints imposed by the academy) stated in an article entitled “The Trouble with Macroeconomics,” “For more than three decades, macroeconomics has gone backward.” We will have to look elsewhere for answers.

Fortunately, some economists did see the crisis coming, including (to name two) Richard Werner and Steve Keen. Yet, their work has been largely ignored by mainstream macroeconomics, which even today continues to argue that money and credit do not matter. Is this simply another inside battle of ideas among economists? Not quite – in fact, the mainstream view has had significant real-world consequences, as we discovered in 2008. The question from the Queen of England resonates: “Why did no one see it coming?”

How does this discussion impact investment strategies?

Investors have twice lost 40% of the value of their portfolios since 2000. One loss of 40% necessitates a gain of 67% just to get back to even. This has happened twice in less than twenty years! Mainstream macroeconomic theorists (and many financial market practitioners) justify these losses based on the mischievous “black swan.” I disagree. In fact, these losses could have been averted, or at least reduced, had macroeconomic and financial stability risk been properly integrated. Unfortunately, mainstream economic theory is trapped – its foundation (belief system) in equilibrium, and its decision to ignore money and credit, makes adaptation to the messy real world complicated. And so it maintains its factually incorrect belief that banks are simply intermediaries between borrowers and lenders, as opposed to what they truly are, which are creators of credit and money.

Credit creation: Productive versus financial capital

In 1997, more than 10 years ahead of the crisis, in an extraordinary article entitled “Towards a New Monetary Paradigm: A Quantity Theorem of Disaggregated Credit, with Evidence from Japan,” Richard Werner described an alternative approach that responded to a series of anomalies, including the cause of the crisis in Japan. His research defined a new version of the quantity theory of money that differed in several important ways from the mainstream approach.

- First, his version correctly focused on credit, not the monetary aggregates, for several reasons. For one, credit represents effective purchasing power (money that has been spent) while the more traditional monetary aggregates represent potential purchasing power (money that has not been spent).

- Second, credit can be disaggregated by sector, distinguishing its allocations to productive economic activity versus asset prices. This is an important distinction with clear implications for financial stability.

Werner’s theory recognizes the important distinction between the use of credit to foster production of goods and services (productive circuit) versus its use to finance the purchase of existing assets (financial circuit), as described below:

- Productive circuit – when capital is invested in production of goods and services, it contributes directly to GDP growth. Over time, credit creation for the real economy and GDP closely parallel one another.

- Financial circuit – when credit is used to finance the purchase of existing assets, this may cause these assets to appreciate (generating capital gains), but with no direct impact on GDP growth.

Both types of credit creation generate liabilities for the borrower – the main difference is that when credit is used for productive purposes, the income it generates can be used to pay down the debt. In this sense it is self-amortizing. However, credit creation to support asset prices has different implications. Credit growth can cause asset prices to appreciate (prompting more credit growth, etc.), but a continuous stream of credit is required to perpetuate this process. If and when credit growth slows, asset prices fall, at times precipitously. Debt-induced asset price appreciation inevitably is a zero-sum game. For every winner, there must be a loser in equal amount, since nothing has been produced!

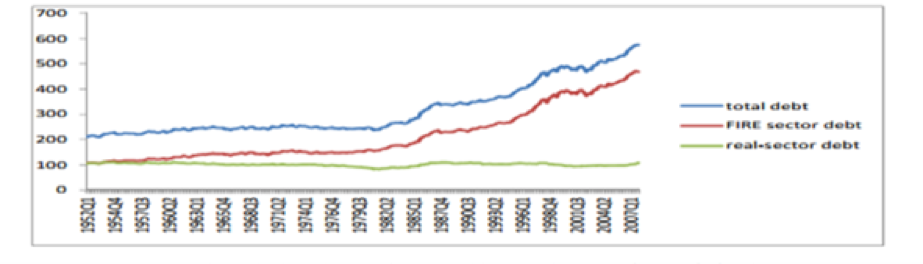

This qualitative distinction between different uses of credit is the key to understanding financial crises. One way to track this growth is to follow the Federal Reserve’s flow of funds. Dirk Bezemer (2012) has generated the following chart, which distinguishes credit to the productive circuit (which has moved in a range from 80% to 110% of GDP) from credit to the financial circuit (which has grown significantly over the past three decades).

Source: Dirk Bezemer (2012) and Federal Reserve Flow of Funds

Financial crises in the 21st century

What prompted the shift toward greater use of credit in the financial circuit? For several decades following World War II, a number of structural regulations, including the Glass Steagall, McFadden Act and Regulation Q (interest-rate regulations), constrained credit growth and thus, financial instability. From 1945 to 1965 or so, the financial system (primarily banks) provided credit to help foster global economic recovery. This was a period of remarkable economic stability, sometimes referred to (in economic terms) as the Golden Age of Capitalism. There were a handful of bank failures, no noticeable financial crises and the distribution of incomes was relatively balanced, given strong institutional support for labor wages.

In the 1970s, the collapse of Bretton Woods, rising inflation and other factors pushed the U.S. government to deregulate various industries, including airlines, trucking and finance. The lifting of quantitative restrictions on credit unleashed rapid growth in credit that was then targeted at asset markets. Serial asset boom-bust cycles occurred after 1980 in real estate, equities, bonds, etc., as private sector debt growth rose rapidly relative to GDP (see chart below), increasing financial instability. In fact, Continental Illinois Bank represented the first case of “Too Big to Fail” in the US in 1984.

Throughout this period, central banks focused exclusively on containing inflation, while generally ignoring the surge in private sector debt and asset prices (despite periodic crises). When crises erupted, the central bank would step in, as monetary policy became increasingly asymmetric (“Greenspan/Bernanke/Yellen Put”). The virtual floor on asset prices encouraged investors to increase risk-taking, which they did, fueling the upward movement in asset prices.

Regulators demonstrated very little understanding during this period about what it is that makes finance different from other sectors of the economy. Mostly, they were concerned about the trees (institution-specific risk) and managed to miss the forest (financial crises and systemic risk) altogether. In truth, positive feedback between credit creation and asset prices in a liberalized market environment sets in motion a dangerous boom-bust dynamic, which fuels speculative tendencies (e.g., carry trades).

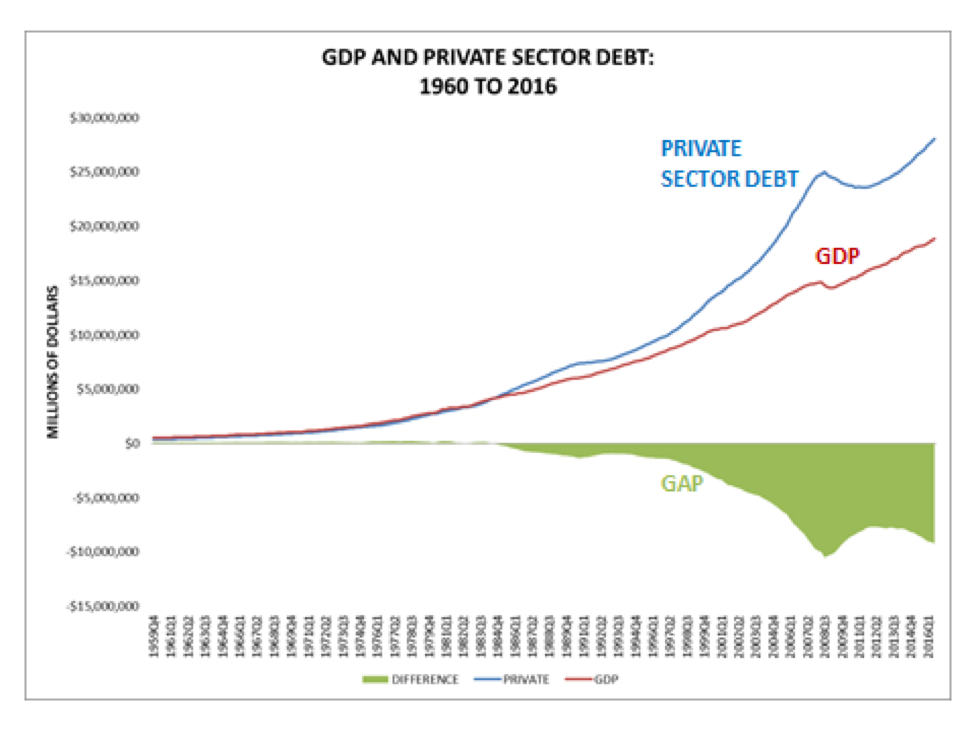

From 1980 to 2007, more than 70% of credit creation was allocated to financial and real assets (“finance mostly finances finance”). Currently, private sector debts equal 150% of GDP, up from 94% in 1980, yet the vast majority of credit that has been created has not supported productive activity. Wages have remained stagnant for the bottom 50% of the income distribution since the early 1980s, as its share of overall income has declined from 20% in 1980 to 12% in 2014 (most recent figure available), while the share of the top 1% increased from 12% to 20%. Reportedly, the top 1% now owns more than the bottom 90%.

The shifting nature of economic activity and credit creation introduces at least four macro challenges.

- The sizable private sector debt load, at 150% of GDP, will encumber future consumption by the bottom 90% of the income distribution, slowing future rates of economic growth.

- Continued use of debt to finance increasingly over valued asset prices make additional disruptions in the financial sector more likely than not, even absent a recession.

- With an aging expansion, there is a strong likelihood of a recession (potentially accompanied by a financial crisis) within the next two to three years.

- Finally, from the perspective of economic stability and public policy, the consequences for income distribution are seriously out-of-whack with the past fifty years of U.S. history, which has contributed to the tense political atmosphere in the U.S. We intend to address this issue in a separate article.

Investors in general are sanguine about short-term investment return prospects, though most appear concerned about the longer term. This cycle cannot end well. Even today, with all the attention paid to macroprudential policies, the new focus on top-down risk, etc., there is still very good reason to be skeptical that things will be all that different in the next crisis, especially given the current deregulatory configuration of political forces.

In response, there is a need for a top-down investment framework that integrates macroeconomic and financial stability risk (for more see here and here). These events are definitely not black swans – once equilibrium is abandoned and money and credit are incorporated, development of real world portfolio solutions becomes possible.

John Balder is a co-founder and CIO at Investment Cycle Engine, Inc. His experience combines more than 25 years of work building innovative investment strategies at firms that included GMO and SSgA. He previously worked with the U.S. Treasury and Federal Reserve Bank of New York after beginning his career with the House Banking Committee on Capitol Hill. His research focuses on the financial stability and the real world relationship between macroeconomics and finance. More information is available at www.icycleengine.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All