Investor confidence in the global outlook for monetary policy, economic growth and inflation has kept volatility contained. Can it continue? We think the risk of a destabilizing policy error is low if central banks remain cognizant of global financial conditions.

Growth and Inflation to Remain Stable Moving into 2018

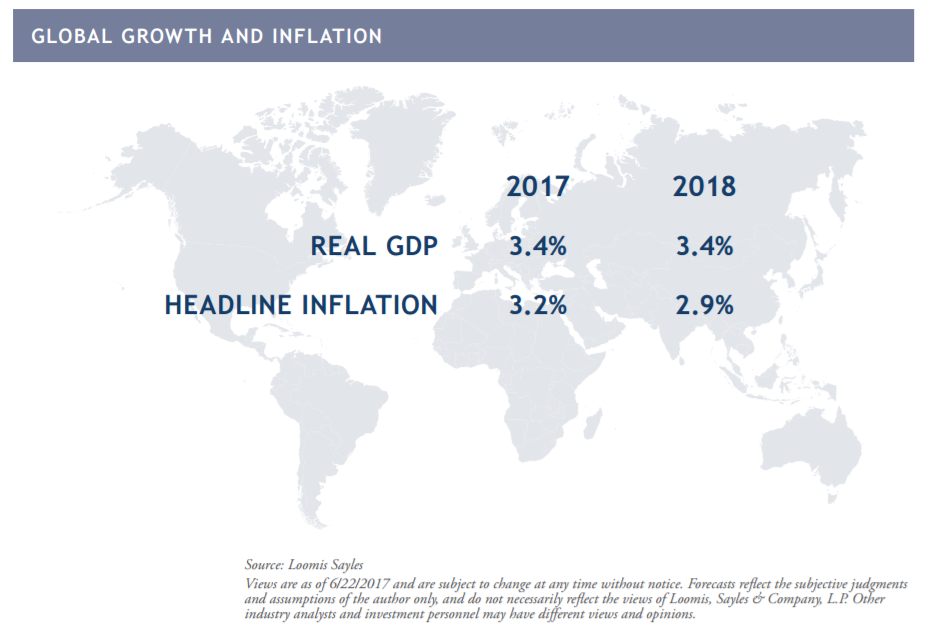

When we look around the world, we see very few catalysts that could significantly increase the pace of global real economic growth, which has ranged from 3.1% to 3.5% in the past five years. The weakest point within that range was last year, when a collapse in oil prices crushed the energy sector and related industries. Looking out through year-end, we see global real GDP climbing to 3.4% annual growth and stabilizing at that level through 2018. This year and next, emerging market (EM) growth is expected to outpace developed market (DM) growth at 4.8% versus 1.8% annually.

Long-Term Path for Stable Growth and Inflation Remains Intact

Headline inflation is expected to increase in 2017, mostly due to the year-over-year rebound in oil prices. We expect nearly flat crude oil prices heading into next year, which should allow global headline inflation to settle back into the 2.9% range next year. Certain high frequency economic indicators, such as manufacturing PMIs, look a bit vulnerable, so a patch of temporary weakness should not be completely ruled out in the near term. However, the longer-term path for stable growth and inflation remains intact, which suggests this fairly slow but steady global expansion can continue. DM monetary policymakers have been removing accommodation much slower than in past cycles, remembering full well the measures it took to get the current synchronized global recovery on track.

As the credit cycle progresses, we expect only modest upward pressure on long-term US yields. A flatter US Treasury curve is expected as yields at the front end of the curve rise faster and by more than those at the long end. In this environment, we believe return prospects for risk assets will continue to look favorable relative to DM government bonds.

Central Banks Remain Data-Dependent, Assessing Global Financial Conditions

The Federal Reserve (Fed) has been the first mover among central banks, tapering quantitative easing measures and raising short-term policy rates in response to the strengthening US economy. We believe the Fed will continue raising interest rates and begin to allow set amounts of US Treasurys and agency mortgage-backed securities to roll off the balance sheet each month, but at a pace and level that do not disrupt financial conditions or derail the economic expansion. The Fed has only hiked four times in the past 18 months, including the June 2017 hike. We believe the pace of US hikes could pick up a bit this year and next since the domestic economy is on firmer footing, but the pace should still be slower than past expansions. Globally, other major central banks are also inching toward less accommodative policies, an indication that economic conditions have improved; however, if the Fed, the European Central Bank (ECB), Bank of Japan and Bank of England remove accommodation too aggressively, they could disrupt the current goldilocks economic scenario and global financial market stability. But central bank communication with market participants has rarely been more transparent or frequent, which helps investors feel confident that surprises are unlikely. The ECB looks next in line to further limit monetary accommodation. Real GDP has rebounded nicely in Europe over recent quarters and inflation has come closer to the ECB’s 2.0% objective. Despite these improvements, we believe changes to the current ECB policy mix will play out over time, not in the short term.

Economic Backdrop and Prudent Monetary Policy Support Equities

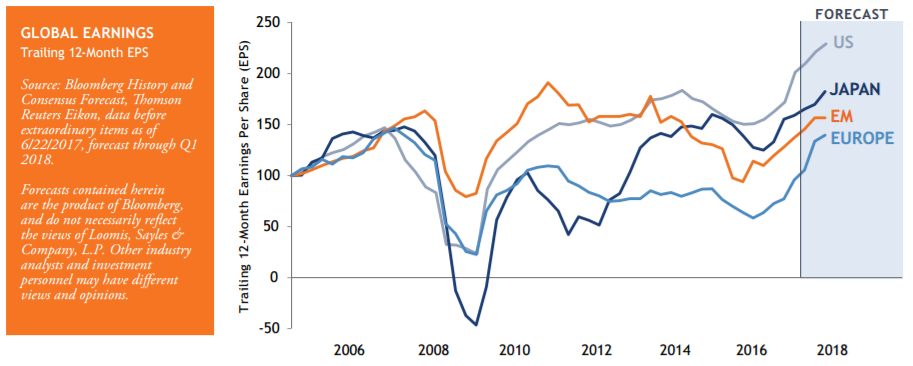

The major central banks have indicated monetary policy decisions will continue to be data-dependent, allowing policy to ebb and flow with economic activity. This degree of caution on the policy front paired with improving corporate fundamentals has led to a favorable environment for risk assets, which we believe can continue. Corporate profits rebounded globally earlier this year and have since broadly exceeded market expectations. The continued profits recovery is an important supporting factor for current equity market valuations, which are not inexpensive, but not overly stretched either. In what is still a fairly low-growth environment, we have seen the information technology sector show global performance leadership year to date and over the past quarter. Energy and financial earnings, which were depressed one year ago, also showed impressive year-over-year growth for many companies. Commodity prices have been under pressure recently and we do not expect a strong rebound, which should boost profit margins for companies that use commodities as inputs to their manufacturing process. However, if oil prices fall back below $40 per barrel, we could once again see contagion sweep through energy and related sectors, including financials, which is a key risk to our positive view.

The S&P 500® Index had been alone in making new 52-week highs earlier this year, but the MCSI Emerging Markets, Japan and Europe indices recently followed suit. Many global equity indices are now trending upward, which indicates a global bull market with technical and fundamental backing. The continued earnings recovery is supporting higher index levels, and we could see equities advance further without an increase in price-to-earnings multiples. The S&P 500 has significantly outperformed global peers over the past five years; however, global equities have outperformed year to date now that global earnings have bested US earnings in some cases. We think that trend may continue if the fundamental improvement we expect comes through for global companies.

Fixed Income Buoyed by Fairly Benign Rate Outlook and Profit Rebound

Based on our moderate outlook for global growth and inflation, we see a benign path for interest rates in most countries. Although yields are generally headed higher, we do not expect a material repricing of the global government bond market. As a result, we believe global and domestic investment grade credit indices with relatively longer duration can still achieve modest excess returns over the next 12 months. The rebound in corporate profitability since the start of the year has been another catalyst for investment grade and high yield credit markets. Fundamental improvement in corporate health and stable economic conditions have kept credit spreads near historic lows and volatility in most risk markets subdued.

We believe credit spreads can remain tight and profits can continue to recover as long as the global economy continues to chug along. Tighter financial conditions in China may slow growth a bit, which could lead to additional capital flight, but the world’s second-largest economy seems to be on fairly solid footing overall. EM economies, a key driver of global growth, are also benefiting from the stable economic environment and still-easy financial conditions. EM hard currency US-dollar-denominated sovereign bond spreads have tightened much like other credit indices but still provide a higher yield than many DM government bonds. The spread between EM inflation and DM inflation is at the lowest level in more than 30 years, a sign of the strides EM countries have made in terms of improving economic stability. With further progress expected, albeit at a slow pace, EM local currency government bonds have a favorable return profile and remain one of the highest-yielding asset classes. All things considered, the current global economic and monetary policy backdrop is creating a favorable environment for risk taking and although expected forward returns are not high, we believe modestly positive outcomes can be achieved.

Disclosure

This commentary is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis do not represent the actual or expected future performance of any investment product. Information, including that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This information is subject to change at any time without notice.

Past performance is no guarantee of future results.

Indices are unmanaged and do not incur fees. It is not possible to invest directly in an index.

This document may contain references to third-party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with Loomis Sayles & Co., L.P. and does not sponsor, endorse or participate in the provision of any Loomis Sayles services, funds or other financial products. LS Loomis | Sayles is a trademark of Loomis, Sayles & Company, L.P. registered in the US Patent and Trademark Office.

MALR019449