The Myths and Fallacies about Diversified Portfolios

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFor many years “alpha” – outperformance of the market on a risk-adjusted basis – was the Holy Grail of investment. Almost all money managers claimed they could produce it. Then, under the weight of an Everest-high mountain of evidence that no investment manager – not mutual funds, not hedge funds – could reliably produce alpha, at long last, a significant minority of investment managers have stopped laying claims to it. For many of these there is now a new Holy Grail: diversification. But there is little agreement as to what it means.

“‘When I use a word,’ Humpty Dumpty said, in rather a scornful tone, ‘it means just what I choose it to mean – neither more nor less.’ “The question is,” said Alice, ‘whether you can make words mean so many different things.’ ‘The question is,’ said Humpty Dumpty, ‘which is to be master – that’s all.’ ” [1]

To try to understand what the new advocates of diversification mean by their versions of it, let’s dissect diversification, first focusing on what most of them agree on. Then we’ll go on to consider the cacophony of new claims – no longer to “alpha,” but to “diversification.”

The only free lunch in investing

The phrase above, applying to diversification, is often attributed to Harry Markowitz’s 1952 paper, “Portfolio Selection” – but it isn’t actually there. Whoever did originate this phrase, there is truth to it. If it is expected volatility that takes away your lunch, and expected return that gives it to you, then combining two assets or securities with the same return and less than perfect correlation reduces your expected volatility without reducing expected return; a free lunch – at least if you are risk-averse.

That’s two assets or securities. What if you add more? It keeps on giving you a free lunch – up to a point. What that point is, and how to find it, are the subject of a long chain of theorizing.

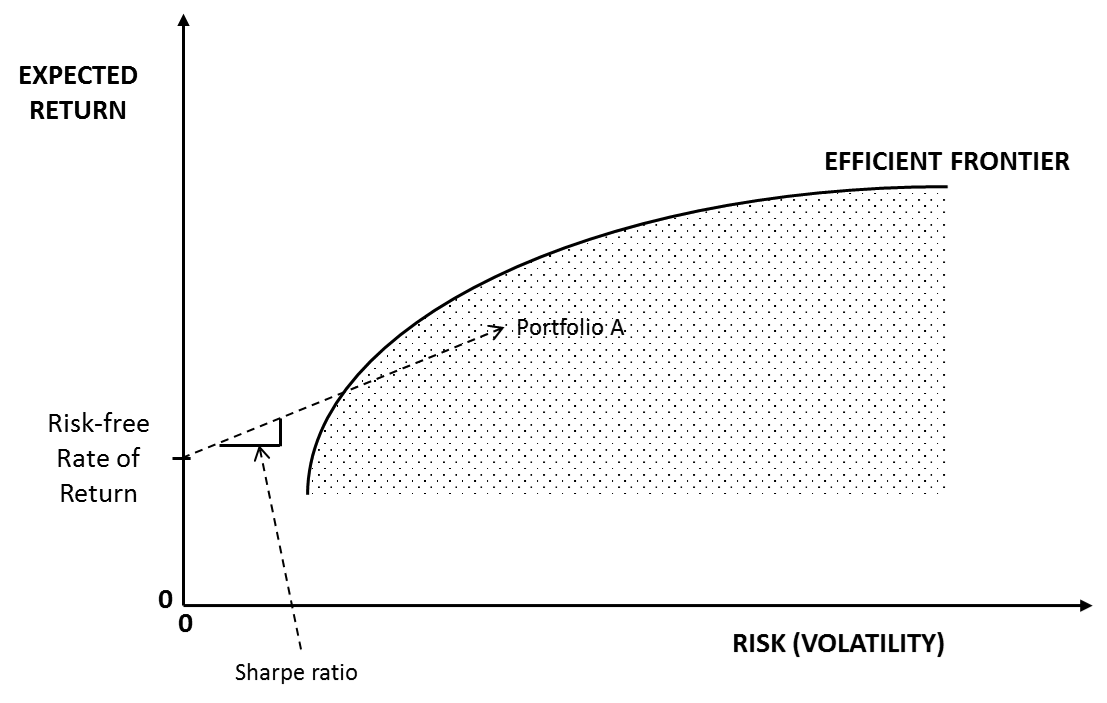

Markowitz traveled that route a good part of the way. I find it amazing that his paper has been the touchstone of investment theory and has been discussed extensively for 65 years, yet the man himself is still younger than my spry 90-year-old uncle. Markowitz’s construction is well known, and can be portrayed as in Figure 1.

Figure 1. Efficient frontier

The dots under the curve in Figure 1 represent “inefficient” portfolios – some are even single stocks. Each one can be diversified further, either to reduce volatility without reducing expected return, or to increase expected return without increasing volatility. The ones that can’t be so diversified any further lie on the efficient frontier.

Markowitz created an algorithm to calculate the weights of assets within portfolios on the efficient frontier. It requires myriad inputs: expected returns and volatilities (standard deviations of returns) for each of the constituent assets, and a correlation coefficient between each pair of them. Even for only 10 assets this is still a lot of numbers: 65. And these required input numbers, especially expected returns, are notably difficult to obtain or estimate. Furthermore, which portfolios are on the efficient frontier is exquisitely sensitive to these inputs.

Each portfolio has a “Sharpe ratio,” named after Markowitz’s successor in the development of portfolio theory, William F. Sharpe. The Sharpe ratio (see Figure 1) is the ratio of expected return (over and above the risk-free rate) to “risk,” i.e. volatility (standard deviation of returns). Note that the inefficient Portfolio A’s Sharpe ratio is lower than that of a portfolio on the efficient frontier above it.

The next step in the development of the theory

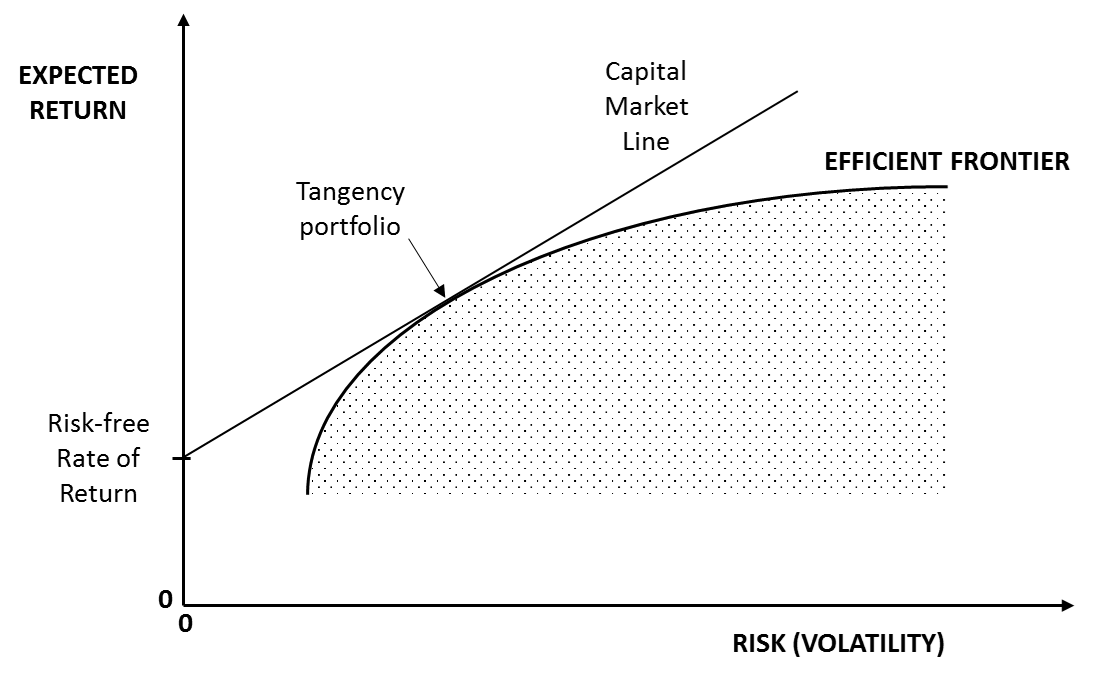

The next step in the theory was to realize that the portfolio with the highest Sharpe ratio is the “tangency portfolio” – see Figure 2. The tangency portfolio is the portfolio at the intersection of a line drawn from the risk-free security that is tangent to the efficient frontier. This line is called the capital market line.

Figure 2. The capital market line

Any portfolio on the capital market line can be obtained by combining the risk-free asset with the tangency portfolio. Therefore, a portfolio on that line is more efficient than a portfolio on the efficient frontier. (For the upper right-hand part of that line, you have to assume that not only can you invest at the risk-free rate, you can also borrow at it.)

So it matters what the tangency portfolio is. If you make the assumption that all publicly available information is known to all investors, and that markets are in equilibrium, this leads to the conclusion that the tangency portfolio is the capitalization-weighted market portfolio. This is not in the least surprising – indeed it is trivial – since in equilibrium all investors, all with the same knowledge, will invest their risk assets in the same portfolio. And the only way they can all do that is if it is the market portfolio. It was this insight that originally brought forth the idea of creating capitalization-weighted index funds to mimic the market.

What is agreed on by the claimants to optimal diversification

Virtually all claimants to the Holy Grail of diversification pay obeisance to the model in Figure 1. They all appear to agree that the most diversified portfolio – for a given level of return or risk – is the one that lies on the efficient frontier.

Claimants to the Holy Grail of diversification summarily dismiss the extension of this theory to Figure 2 and the conclusion that the most-efficient portfolios are combinations of the risk-free asset and a total market index fund. Their reasons for this dismissal are vague. Some cite the Roll critique set forth in a 1977 article, which simply says there is no such thing as the “total market portfolio,” because it would have to include all global assets – including a vast amount of local real estate, and perhaps even such intangibles as human capital. Some cite other articles and arguments. However, one suspects the motivation for this dismissal also includes the fact that it is hard to become a billionaire or a hundred-millionaire, or even a ten-millionaire, just peddling total market index funds. John Bogle, who started the whole extraordinarily successful index fund movement, reportedly has not even achieved hundred-millionairehood (not that he cares).

The motivation for the new emphasis on the search for diversification

Articles on diversification often begin by motivating their goal of maximizing diversification by first nodding, with evident approval, toward the Markowitz construct. Then, they focus on the difficulty of putting this construct into practice, because while it is very hard – as noted earlier – to estimate expected returns, their estimated values make a huge difference in the result.

But, because you can’t estimate expected returns and therefore you can’t carry out the Markowitz project, you need to focus on something else if you’re going to optimize something. And diversification is the obvious candidate, since it is, after all, “the only free lunch in investing.” And this leads the proponents to tout the benefits of “true diversification” – which is presumably an expected-returns-estimate-free way of getting to Markowitz’s efficient frontier.

The buzzing fly in the ointment is as follows. It turns out that when they argue that their method leads you to that golden efficient frontier, their argument is not expected-returns-free as they at first imply it is. They all assume the expected returns that they need in order to prove the optimality of their respective methods. And some of those assumptions are rather strange. In fact, they come down to assuming that all Sharpe ratios for all assets used to construct portfolios are the same. That is, they assume that all of the assets have expected returns that are proportional to their volatilities.

Having established these basic similarities among the approaches to diversification, I will review three candidates for “maximum diversification.” These include: (1) equal-weighting; (2) maximizing the “diversification ratio” proposed by Choueifaty and Coignard (2008); and (3) the risk-parity or equal-risk portfolio. I’ll leave aside in this discussion the alternative cited above (but dismissed by most of the proponents discussed here), that of maximizing closeness to the total market portfolio.

The equal-weighted portfolio

An equal-weighted stock portfolio has equal numbers of dollars in each stock. I don’t think anyone seriously argues that such a portfolio is the most diversified one. It would mean holding – in the name of diversification – the same amount of a large diversified company like the $400 billion market-cap Berkshire Hathaway, and a $70 million market-cap company like NeurogesX, which “develops and commercializes therapies for chronic peripheral neuropathic pain.”

Nonetheless the idea that an equal-weighted portfolio is the most diversified has crept into the official running. For example, an FTSE Russell discussion of diversification lists equal-weighted indexes as the first in a list of alternatives to “address concentration risk” (i.e. to increase diversification). And an academic study that lamentably made it into the pages of The Economist magazine generated “random portfolios” that together added up to an equal-weighted market portfolio. Since all actual portfolios put together add up to the cap-weighted market portfolio not the equal-weighted version, all randomly-generated portfolios – properly constructed – should add up to that too.

And there is, too, the fact that even the equal-weighted portfolio can be shown to lie on the efficient frontier – but only if you make the assumption that all of the securities have the same Sharpe ratio, the same volatilities, the same expected returns and the same pairwise correlations.

Maximizing the diversification ratio

Choueifaty and Coignard (2008) defined a measure of diversification by forming the ratio of the weighted average of the standard deviations of assets in a portfolio to the standard deviation of the portfolio itself. Then they call the portfolio that maximizes this ratio the “most-diversified portfolio.”

This might be okay, but their most-diversified portfolio lies in the cloud of inefficient portfolios below the efficient frontier – unless you make the assumption that all of the Sharpe ratios of the securities in the portfolio are the same. Hence, the most-diversified portfolio of Choueifaty and Coignard is most diversified in the Markowitz sense only on the highly unlikely assumption that all the securities in it have the same Sharpe ratio. Therefore, either Choueifaty and Coignard must reject Markowitz’s construct that awards additional expected return only through diversification, or they really believe that all securities have the same Sharpe ratio.

It is hard to see how a portfolio can be the most diversified if it lies below the efficient frontier. Lying below the efficient frontier means that by adding other securities or by altering the weighting of the securities the portfolio could move vertically upward in Figure 1 to receive the free lunch of a higher expected return at the same level of volatility. What could this upward move be called if not “more diversified”? This is the most basic element of the underlying theory, contested by virtually no one.

The equal-risk portfolio

The equal-risk concept seems to have caught on among those who, unable as a group to show that they can get return, wish to change the subject by shifting the focus of investing from return to risk. And of course you need to have diversification because that is the new Holy Grail. So what could be better than diversifying risk?

The idea is that, to take the simplest example given in Qian (2011), if stocks’ standard deviation is three times that of bonds – e.g. 15% versus 5% – why would you want a 60/40 stock-bond portfolio when that means that 92% of the volatility is contributed by the stocks? (0.6 squared times 15% squared as compared to 0.4 squared times 5% squared.)

Instead, advocates of the equal-risk approach, also called risk parity, argue that you should allocate the portfolio so that the risk contributions of the constituent assets are the same. In the example just mentioned, that would be a 25% stock / 75% bond portfolio.

There are two problems with this approach. First, like Choueifaty and Coignard’s most-diversified portfolio, it lies below the efficient frontier if your portfolio has more than two assets, unless you assume that the Sharpe ratios of the constituent assets are all the same. Second, as Choueifaty et al (2011) have pointed out, the equal-risk portfolio can be arbitrarily changed by dividing up the assets differently. For example, if you form a risk-parity portfolio from short-term, intermediate-term, and long-term bonds and stocks, then form another portfolio by merely adding an aggregate bond index fund to the mix that itself contains those same bonds, you’ll get a different portfolio. Lohre et al (2013) acknowledge this problem and propose a fix for it based on the interesting “principal portfolios” approach (Partovi and Caputo 2004), but it doesn’t address the efficiency shortfall.

Bottom line

None of these approaches to maximizing diversification has much theoretical merit. They are part of that combination of fuzzy math and suggestive language that is peculiar to the investment finance field. Their proofs that they are maximally diversified in the Markowitz sense depend on the assumption that the Sharpe ratios of a portfolio’s constituent assets are all equal. But if all assets that go into constructing a portfolio have the same Sharpe ratio, then they will all fall on a straight line running through the risk-free rate and lying somewhere in the middle of the cloud of inefficient portfolios in Figure 1. There’s no reason to believe this. Furthermore, even if it were true of one decomposition into constituent assets – such as intermediate bonds, long-term bonds, and stocks – then it could not also be true of a different but equivalent decomposition – such as stocks plus a bond aggregate comprising both intermediate and long-term bonds. Thus, the assumption itself is internally inconsistent.

This leaves it unclear as to exactly what should be the measure of maximum diversification. Yes, all can agree, it’s whatever portfolios are on the efficient frontier, but the errors in solving for that are so massive that the results can be ignored.

The answer is simply that there is no such thing in practice as maximum diversification. It’s no more than a theoretical concept. You can get a rough sense of the diversification of a portfolio by looking simultaneously at tracking error to an index, Choueifaty and Coignard’s diversification ratio, and even just the number of securities in a portfolio. (Personally I would ignore the equal-risk approach.) But attempts to “maximize” diversification have no place in the practical world. Even in the theoretical world the attempts should do better than these; perhaps they will in subsequent efforts.

Michael Edesess is a mathematician and economist, a senior research fellow with the Centre for Systems Informatics Engineering at City University of Hong Kong, chief investment strategist of Compendium Finance and a research associate at EDHEC-Risk Institute. In 2007, he authored a book about the investment services industry titled The Big Investment Lie, published by Berrett-Koehler. His new book, The Three Simple Rules of Investing, co-authored with Kwok L. Tsui, Carol Fabbri and George Peacock, was published by Berrett-Koehler in June 2014.

References

Choueifaty Y. and Coignard Y. (2008), Towards maximum diversification, Journal of Portfolio Management, 34(4), pp. 40-51.

Choueifaty, Yves, Tristan Froidure, and Julien Reynier. "Properties of the most diversified portfolio." Journal of Investment Strategies 2.2 (2013): 49-70.

Lohre, Harald, Heiko Opfer, and Gabor Orszag. "Diversifying risk parity." Journal of Risk 16.5 (2014): 53-79.

Maillard, Sébastien, Thierry Roncalli, and Jérôme Teïletche. "On the properties of equally-weighted risk contributions portfolios." Available at SSRN 1271972 (2008).

Partovi, M. Hossein, and Michael Caputo. "Principal portfolios: recasting the efficient frontier." Economics Bulletin 7.3 (2004): 1-10.

Qian, Edward. "Risk parity and diversification." Journal of Investing 20.1 (2011): 119.

Roncalli, Thierry, and Guillaume Weisang. "Risk parity portfolios with risk factors." Quantitative Finance 16.3 (2016): 377-388.

[1] Lewis Carroll (Charles L. Dodgson), Through the Looking-Glass, chapter 6. First published in 1872.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All