Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Providing income and preserving economic security subsequent to retirement is an important issue for an aging population. Decumulation, living off one’s assets, requires a tradeoff between preserving capital and obtaining income. This article generalizes some simple decumulation strategies and explains the strengths and weaknesses of an inverted approach.

The 4% rule, originated by Bill Bengen, is the first and most commonly studied retirement-income plan. Based on historical data, he found that if one spent 4% of the initial capital annually, adjusted for inflation, one could safely support a 30-year retirement period. The 4% rule continues to be the standard for comparing other methods for retirement-income planning.

The major problem with the 4% rule is that, since the percentage is determined by initial capital rather than ongoing portfolio value, spending does not respond to changes in value of the portfolio over time. Given the same amount of spending each year, a fraction of the current portfolio value greater than 4% is taken when the portfolio is down and less than 4% is taken when the portfolio is up. Under unfavorable markets this will rapidly deplete the portfolio and introduce sequence of returns risk. Without corrective action, a retiree using the strategy has a non-zero probability of going broke.

Another simple option is to withdraw a constant fraction of the current value of the portfolio each year, typically 4% or 5% per year, called the endowment method. In this case the portfolio never reaches zero value and the sequence of returns risk goes away.

Consider that in one case (4% rule) the annual withdrawal rate is greater than 4% when the portfolio declines and less than 4% when it increases, whereas the endowment method always uses the same constant withdrawal rate, let’s assume 4%. More generally, we can examine the spectrum of decumulation possibilities by changing the direction (“tilt”) and magnitude of how the withdrawal rate varies with changes in the portfolio balance over a range of values and examine the implications. The concept of tilt is that each year the withdrawal rate is changed (tilted) based on the value of the portfolio. Table 1 has examples of a range of tilts.

Table 1. Annual withdrawal rate options for initial $1,000,000 portfolio.

|

Capital

|

4% rule

|

-2% tilt

|

-1% tilt

|

Endowment (0% tilt)

|

+1% tilt

|

+2% tilt

|

+3% tilt

|

|

> $1M

|

$40,000

|

2%

|

3%

|

4%

|

5%

|

6%

|

7%

|

|

< $1M

|

$40,000

|

6%

|

5%

|

4%

|

3%

|

2%

|

1%

|

The -2 percent tilt means that, when the portfolio balance goes above $1,000,000 (the assumed starting value), the annual withdrawal rate is decreased by 2% (from 4% to 2%) to compensate, thereby moving the annual income closer to 4% of the initial balance target. When the portfolio goes below $1,000,000, the withdrawal rate is increased from 4 to 6%, thereby stabilizing income toward the planned 4% of initial balance. The +2% tilt represents an inverted approach where, when the portfolio rises above $1,000,000, a greater portion is taken out (6% when the portfolio is greater than $1,000,000, 2% when below $1,000,000). Zero tilt is the classic endowment model where 4% of current balance is taken out each year irrespective of the balance.

The positive tilts are a mathematical formalization of how most people behave. When our portfolio has risen, we spend more (remodel the bathroom, replace the car); when the portfolio falls, we spend less (e.g., spend dividends and interest only). This makes the income more variable but tends to maintain assets near the desired level ($1,000,000 in this example). The negative tilts are closer to the 4% rule, providing a more constant income but greater risk of losing more assets. They also are similar to “floor with upside potential” withdrawal schemes. The positive tilts invert the 4% rule and other negative tilts.

The following figures represent Monte-Carlo simulations of seven different retirement-income plans with three different investment options. The investment options are labeled high, medium and low volatility (and risk). High-volatility portfolios typically have a greater fraction of stocks versus bonds, but with modern portfolios it is more complex than stocks versus bonds. The model portfolios were taken from the Research Affiliates asset allocation site, because they have a great educational treatment on the website and publish their methodologies. I neither agree nor disagree with their estimates. I merely used them as plausible numbers for my simulations. The model portfolios are (mean, annual standard deviation), (5.9, 13), (4.9, 10), (3.3, 6.5) percent.

The simulations last for 30 years; all of them are in constant (inflation-adjusted) dollars and use 4% as a basis for the tilts. The 4% rule is included in the graphics for reference. With Monte-Carlo simulations, one obtains thousands of potential future paths; each of these futures is called a realization. Statistical summaries of Monte-Carlo results have weird descriptions if one is not a statistician or practitioner of numerical uncertainty analysis. When I speak of the 10% lower results, I refer to examining all of the hypothetical future 30-year realizations and taking the worst 10%. The median of the average income means that, for all of the thousands of future 30-year realizations, I locate the point where half of the realizations are better and half are worse.

The portfolio at retirement is assumed to be $1,000,000, an easily scalable unit value. Results are shown in units of thousands of dollars. The results presented are from linear equations, meaning that the results can be directly scaled up or down based on the value of the initial portfolio of interest relative to the $1,000,000 assumed herein.

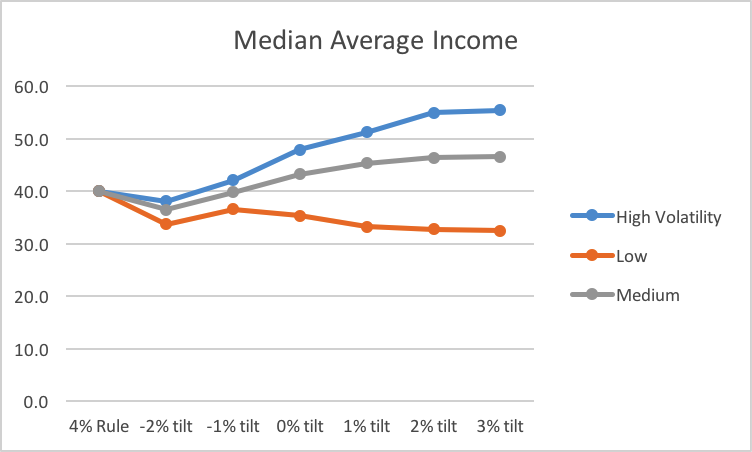

Figures 1 and 2 are projected average income from the median realization and the lower 10% realization, respectively. For the high- and medium-volatility portfolios, the positive tilt (spend proportionally more when the market is up, less when it is down) leads to a higher expected income. The low-volatility portfolio results don’t change much with how the income is withdrawn.

Figure 1. 50 percent (median) average income in thousands of dollars per year.

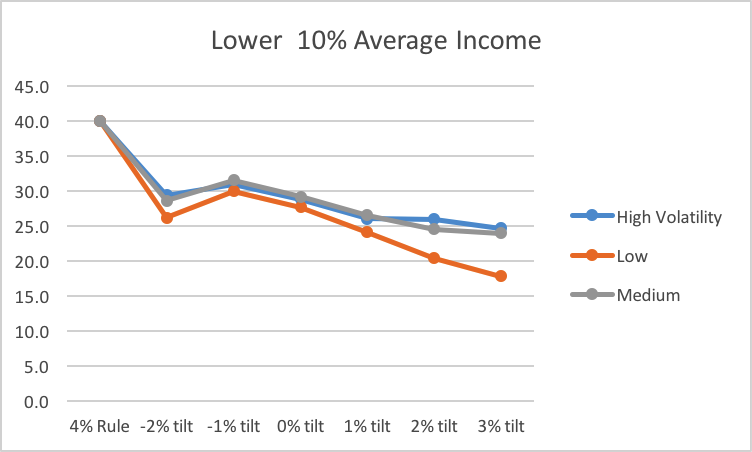

Figure 2 is a reflection of poor market results, the lower 10%. Here we see that a slight negative tilt (withdraw a greater portion of assets when the market is down) does stabilize income when the market is down. The surprising result is that the income under unfavorable market conditions does not depend strongly on the portfolio volatility. This is because low volatility is also associated with lower anticipated returns.

Figure 2. Lower 10% of realizations for income in thousands of dollars per year.

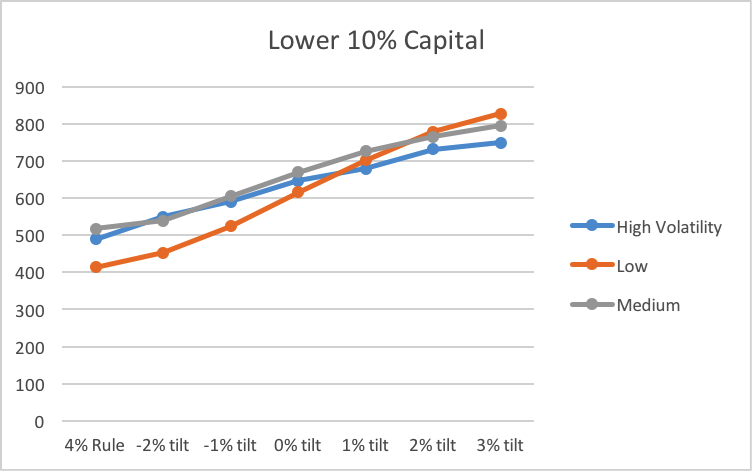

Capital preservation is another concern. In addition to the human tendency to not want to see our assets decline, maintaining assets is important for a rainy day, long-term care, inheritance and philanthropy. Here the results are very clear. A positive tilt to spending tends to preserve capital even with poor market results and the conclusion doesn’t depend strongly on portfolio volatility (risk).

Figure 3. Lower 10% of realizations, average capital in thousands of dollars.

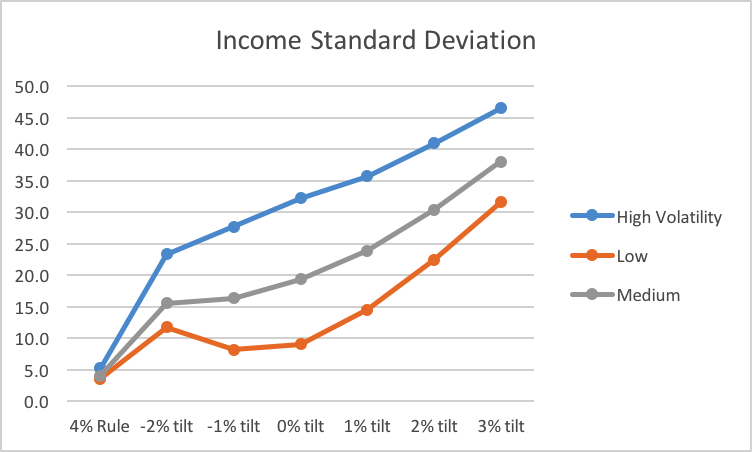

Additional insight into the results comes from examining the variability of income and capital. A low standard deviation means income (or capital) is relatively constant. Notice how the standard deviation of income increases with withdrawal-rate tilt and portfolio volatility. If nearly constant income is the goal, a low-volatility/ low-risk portfolio combined with a zero or slightly negative tilt is preferable. High-tilt and high-volatility investments lead to dramatic fluctuations in annual income.

Figure 4. Standard deviation of annual income in thousands of dollars per year.

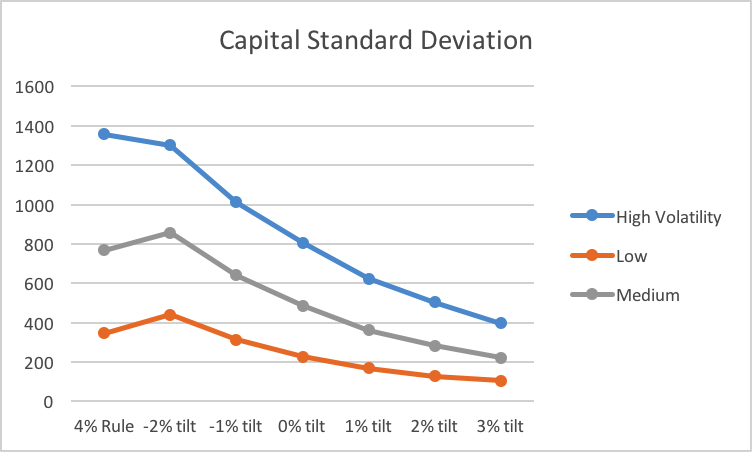

The standard deviation of capital (Figure 5) is also dependent on portfolio volatility and the spending tilt. If one is able to withstand large fluctuations in annual income, a high positive tilt preserves capital while increasing anticipated (average) income, keeping one more prepared for the vicissitudes of life.

Figure 5. Standard deviation of capital in thousands of dollars.

At one level, the movement from -2 to +3 tilt appears to be a simple tradeoff of income stability versus capital stability. Negative tilts stabilize income but risk capital loss, whereas positive tilts provide a highly variable income while stabilizing capital.

But there’s more.

The positive tilts increase the anticipated income dramatically while only slightly decreasing the lower 10% income and better preserve the capital. A spending plan with a positive tilt (spend more when the market is high, less when low) and a higher stock (higher volatility) portfolio will increase anticipated retirement income while reasonably protecting capital for unanticipated events. As long as capital is preserved, spending plans can change as desired. When capital disappears (a risk with the 4% rule and other negative tilts) options close.

If the assets are to provide most of the retirement income, then a lower stock (lower volatility) portfolio with a zero or slightly negative tilt stabilizes income, with a cost of low longer term growth that limits anticipated income. In this situation purchase of an annuity, such as a single-premium immediate annuity (SPIA), may be a better option.

A positive tilt and high volatility portfolio make sense for clients whenever the stable portion of the income and liability stream (Social Security, pension, annuity and paid-off house) is a large portion of total income (or of the present value of total wealth). Positive tilt and high volatility also work well for relatively affluent clients who can live off of interest and dividends if necessary then take out 5-6%/year when markets rise. In both cases maximizing anticipated income and preserving capital for a rainy day, inheritance or philanthropy are greater concerns than minimum living expenses during market downturns.

The benefit of the positive tilt (inverted withdrawal rate) might be thought to come from a tendency to sell more high and sell less low, but that is not the case. My simple Monte-Carlo simulations do not have mean reversion, although real stock markets may mean revert. Rather, the positive tilt options in the simulations sometimes benefit from a sequence of returns bonus, nearly the opposite of the 4% rule or the negative tilts where a sequence of returns risk exists. Notice that, for positive tilts, the average income is approximately equal to the average portfolio rate of return while portfolio risk (standard deviation) is moderated relative to the endowment model (zero tilt). Both the sequence of returns risk and the herein observed sequence of returns bonus are statistical consequences of how income is subtracted from the randomly varying capital. An improved understanding of the statistical impacts of the withdrawal rate allows for adjusting withdrawal rates so that, on average, the results are superior.

How would this work in practice? The best use of Monte-Carlo analyses is not to predict the future but rather to help us understand the likely consequences of our actions given an uncertain world. Jill and Jack Hill can use this insight to develop a simple, less formulaic, plan.

Jill and Jack have a combined Social Security income of $60,000/year. They purchase a 3%/year annual step-up annuity (SPIA) at retirement to obtain an additional $15,000/year of steady income. The net $75,000/year of (approximately) inflation-adjusted income is enough to meet their basic needs. This leaves them with $1,000,000 of investible assets. They would like to maximize their income while alive, preserve some assets for long-term care if needed, and leave some money at death to assist with college for their six grandchildren and give to their church. The $1,000,000 of assets is invested in 80% world stocks (e.g., Vanguard VT) and 20% bonds, a high-volatility portfolio. When their portfolio declines during market downturns, they take only dividends and interest (assume 2.5% to keep this example simple), putting their income near $100,000. When the market rises and the portfolio is above the initial $1,000,000, they take out 5-6% of the balance each year, raising gross income to greater than $125,000; allowing them to travel around the world looking for their pail of water.

Their anticipated (median average) income from the figure above would be about $130,000 using the positive tilt withdrawal rate versus $115,000 with the 4% rule. At the same time, their assets would be much more stable (standard deviation of asset balance reduced by a factor of 2-3 relative to 4% rule), providing both increased anticipated income and financial security for the Hills and their family. If they wanted to add more stability to their annual income, they could use the higher income during good years to purchase additional aliquots of annuity (SPIA).

The inverted withdrawal rate is worthy of consideration.

John Walton is an Engineering Professor at the University of Texas at El Paso, where he has taught for 24 years. He has a Ph.D. in Chemical Engineering. His interest in financial planning came from considering options for his coming retirement.

Read more articles by John Walton