Should retirees place greater faith in stocks’ ability to outperform bonds over reasonable holding periods or in insurance companies and bond issuers’ ability to meet their contractual guarantees? Your position on this fundamental question will determine how you choose to build retirement income strategies for your clients.

Instead of taking a side in this debate, I will illustrate how sequence of returns risk can derail a cohort of retirees. Indeed, that can happen without an economic catastrophe wiping out large financial institutions.

You may believe that any situation where stocks underperform bonds would make it impossible for contractual guarantees to be met. As I will explain, that belief is not fully justified.

The relevance of risk pooling

In contrast with defined-contribution pensions, a defined-benefit pension provides benefits more closely aligned with the amount of spending one could support given appropriate investment return and mortality assumptions. This is possible because the pension manager can pool two types of risks that individuals cannot pool on their own. The first of these is longevity risk. This risk is less relevant for today's discussion, but it reflects the idea that the pension manager can make payments to participants assuming they will live to their life expectancy. Those who die earlier will subsidize the payments to those who live longer.

The more relevant issue is that investment risks can be pooled across different cohorts of individuals who work and retire at different points in time. When individuals manage their own retirement investments, some will experience good sequences that would allow them to spend at a much greater rate than the defined-benefit pension could offer. But others will not be as fortunate; the sequence of returns they experience will lead to a lower level of sustainable income than the defined-benefit pension could have provided. The pension is able to pool these investment risks, giving everyone the same average benefit for the same contributions, by sharing this market risk across cohorts.

Some would have been better off on their own, while others would have been worse off. But things work out on average.

Investment risk and sequence risk

Retirees face market risk, which concerns how market volatility causes average investment returns to vary over time. Sequence of returns risk adds to the uncertainty related to overall investment returns. The financial market returns experienced near one’s retirement date matter a great deal more than most people realize. Even with the same average returns over a long period of time, retiring at the start of a bear market is very dangerous; wealth can be depleted quite rapidly as withdrawals are made from a diminishing portfolio and little may be left to benefit from a subsequent market recovery.

Sequence of returns risk relates to the heightened vulnerability individuals face regarding the realized investment portfolio returns in the years around their retirement date. Though this risk is related to general investment risk and market volatility, it differs from general investment risk. The average market return over a 30-year period could be quite generous. But if negative returns are experienced when someone has just started to spend from their portfolio, it creates a subsequent hurdle that cannot be overcome even if the market offers higher returns later in retirement.

The dynamics of sequence risk suggest that a prolonged recessionary environment early in retirement could jeopardize the retirement prospects for a particular cohort of retirees. That scenario does not imply a large-scale economic catastrophe. This is a subtle but important point. Particular retiree cohorts could experience very poor retirement outcomes relative to those retiring a few years earlier or later; devastation for one cohort does not necessarily imply overall devastation for the economy or for institutions that pool financial-market risk across different cohorts.

To illustrate this, we will first look at the rolling compounded returns over 30-year periods for a 50/50 portfolio of large-capitalization stocks and short-term fixed income assets, using the dataset available on Robert Shiller’s webpage.

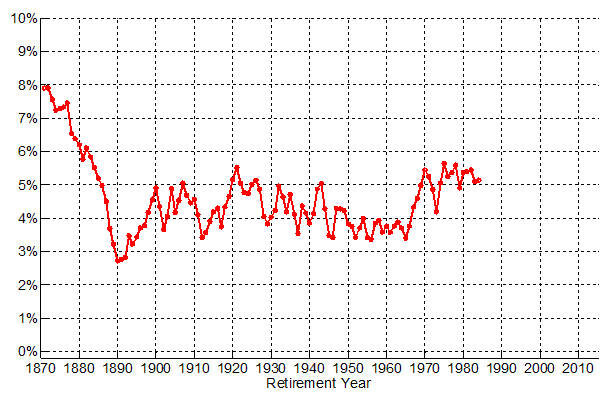

Figure 1

Compounded 30-Year Real Portfolio Returns for 50/50 Asset Allocation

Figure 1 represents investment or market risk, as distinct from sequence of returns risk. Average returns over different 30-year rolling periods are not always the same; they fluctuate. While there was more volatility and extremes in both directions before 1900, I focus the discussion on the post-1900 period. (A number of legitimate questions could be asked about the applicability and accuracy of 19th century financial market data.)

Since 1900, rolling compounded 30-year returns have generally stayed within the 3.4% to 5.7% range. Changes to these numbers have happened quickly. For instance, the compounded return from 1973 through 2002 was 4.18%, while the compounded returns from 1975 through 2004 was 5.65%. That difference is due to a two-year lag in the starting point for calculating returns; the 1973 and 1974 returns were switched for the 2003 and 2004 returns. We can think about this volatility for compounded returns over a 30-year period of time as the general investment risk facing retirees. However, this is not the whole story since sequence of returns risk has not been factored in yet.

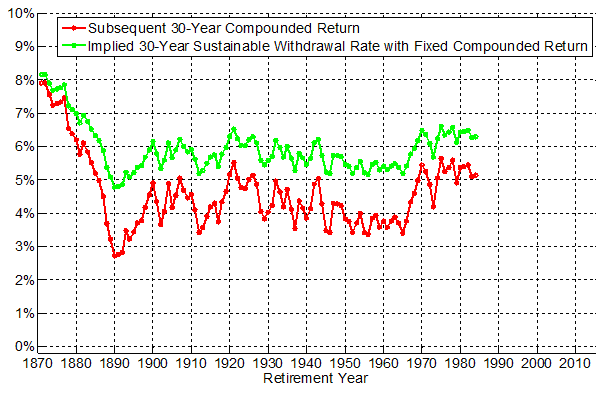

But let’s consider another calculation before incorporating sequence risk. Figure 2 uses the historical data to show the hypothetical sustainable withdrawal rates implied by a fixed compounded return equal to the calculated numbers shown in Figure 1. These numbers represent a simple annuity calculation: with withdrawals taken at the start of the year and a fixed compounded portfolio return for the next 30 years, what is the spending rate that would deplete the portfolio in the 30th year? The answer is in green in Figure 2.

Because investment returns fluctuate, these hypothetical sustainable withdrawal rates also fluctuate. Nonetheless, since 1900 they remain within a range of about 1.5 percentage points. They do not fall below 5%, and they are a little above 6.5% at their highest. These would be sustainable withdrawal rates if there were only investment risk to worry about, in which the compounded returns over 30 years were all that mattered.

Figure 2

Compounded 30-Year Real Portfolio Returns for 50/50 Asset Allocation

And Sustainable Withdrawal Rate Implied by the Fixed Real Compounded Return

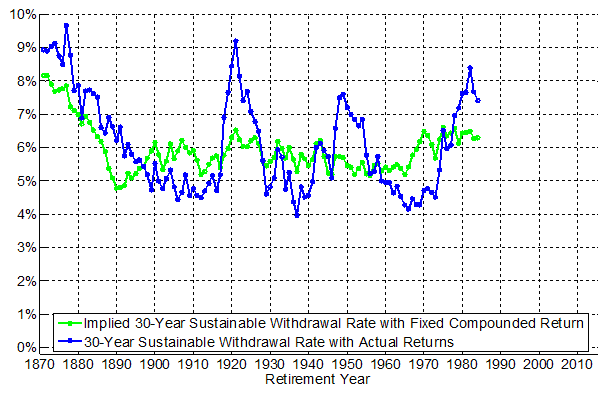

Finally, Figure 3 demonstrates the specific impact of sequence risk compared to the more general market risk. The green points again represent implied withdrawal rates for compounded average return over the subsequent 30 years. Meanwhile, the blue curve represents the actual sustainable withdrawal rates over those 30-year periods. What matters for calculating the actual withdrawal rates is not just an average portfolio return, but also the specific sequence of returns.

Actual withdrawal rates are much more volatile after accounting for sequence risk. There is greater downside risk; the withdrawal rate fell as low as 3.95% for a 1937 retiree and 4.16% for a 1966 retiree. On the other hand, there is greater upside potential as well; a 1982 retiree could have used an 8.39% withdrawal rate, and a 1921 retiree could have used a 9.19% withdrawal rate.

The differences have been stark. For instance, the average portfolio return from 1937 to 1956 would have implied a 5.28% sustainable withdrawal rate, but it was only 3.95% in reality. Likewise, for a 1969 retiree the sustainable withdrawal rate was 4.71%, while the average portfolio return would have supported a 6.49% withdrawal rate. Retirees can indeed be adversely affected in ways that dig deeper than the investment risk associated with the average return experienced over retirement. This is important because this risk can be alleviated through pooling.

Figure 3

Comparing Sustainable Withdrawal Rates Implied by the Fixed Real Compounded Returns

With Actual Sustainable Withdrawal Rates Supported by the Sequence of Returns

The bottom line

William Bengen’s 1994 research provided us with the initial formulation of the 4% rule for retirement portfolio withdrawals. He investigated sustainable spending for each rolling 30-year period in the historical record. His analysis accounted for the sequence risk in the historical data, and his results reflected what would have worked in the worst-case scenario in history.

However, because of the greater volatility of actual withdrawal rates relative to those implied by average market returns, we should not place too much comfort in the idea that the worst-case scenario in U.S. history represents how bad things may get for particular cohorts of returns.

The volatility of actual sustainable withdrawal rates, compared to the withdrawal rates implied by compounded average returns over 30-year periods, demonstrates sequence of returns risk. In the withdrawal phase of retirement, the specific sequence of market returns matters greatly. Individuals drawing off their own investments have no way to manage this risk except to spend at a very conservative rate and hope for the best. More often than not this will require being overly conservative and leaving assets on the table at death. It’s an important factor for retirees to consider relative to the higher spending rates available through risk pooling.

Wade D. Pfau, Ph.D., CFA, is a professor of retirement income in the Ph.D. program in financial services and retirement planning at the American College in Bryn Mawr, PA. He is also the director of retirement research for McLean Asset Management and inStream Solutions. He maintains the Retirement Researcher website. See his Google+ profile for more information.

Read more articles by Wade Pfau