Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Fears of rising interest rates have become background radiation, exposing everyone. A recent Eaton Vance survey, Advisors’ 4 Biggest Concerns: Eaton Vance, of 1,006 advisors concluded that, “nearly three-quarters of advisors report at least some concern about a near-term increase in rates, and one in five say they are very concerned.”

The distress runs so deep that some advisors call for completely abandoning bonds. At a recent investment conference in Manhattan, I witnessed a senior executive of a major real estate syndicator tell 1,000 advisors that he believes that investors should hold 0% of their portfolios in bonds. “I don’t see why they should hold any bonds,” he chirped to applause and laughter when answering a question of what percentages investors should hold in various assets. What should investors buy instead? REITs of course, he said. I won’t tell you which real estate syndicator he represents, but its underlying stock value is down 97% since that speech.

Later, in Denver, at an alternative investing conference sponsored by Financial Advisor magazine, the audience survived similar fusillades against bonds.

Even the venerable Barron’s ran a cover story with the warning “Trouble Ahead for Bond Funds.” The pull quote from the article read: “There is a real, real risk in bond funds.” In Advisor Perspectives, I read with surprise an article titled “Why Bond Funds Don’t Belong in Retirement Portfolios.”

Here is the investment-conference formula. The speaker directs the audience, “Raise your hand if you’ve survived a bear market in bonds.” The audience looks around bewildered; after all, the last bond bear market ended over 30 years ago. No one raises a hand. “Proof,” he booms, “this is what I am talking about folks – you have no idea what to expect in a bear market. Be warned, it’s not pretty.” Then he offers up as evidence investing your entire IRA in a 30-year Treasury bond the day before interest rates shoot up 4%. “In a flash 48% of your net worth instantly vanishes, forever--in a U.S. Treasury Bond! Do I have your attention yet?” The audience shrinks in horror.

My research challenges these hysterics. Rising interest rates are nothing to fear. Total returns could be positive, not negative, if we have a similar rate trajectory that we had in the last bear market in bonds. I believe that bonds should continue to be a staple in investors’ portfolios – and in greater, not lesser percentages as our population ages and interest rates increase.

Additionally, Blackrock found that from 1929-2014 stocks were negative in 24 years. In 92% of those years, bond returns were positive. [Source: Morningstar. As of 12/31/14. Past performance does not guarantee or indicate future results. Bond Returns represented by IA SBBI IT Govt Index from 1929 to 1975 and the Barclays U.S. Aggregate Index from 1976 to 2014. Stocks are represented by IA SBBI Large Stock Index from 1929 to 1970 and the S&P 500 from 1970 to 2014]

The numbers

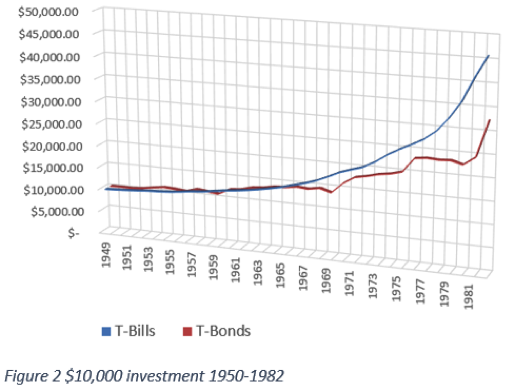

The last secular bear market in bonds lasted from roughly 1950 to 1982. Let’s start with a picture – Figure 1. This is what a bear market in bonds looks like. A 5.58% average annual return for 32 years.

Figure 1 – Thomson US: Corp - High Yield – MF Index, 12/31/49-12/31/81, Hypothetical $10,000 investment.

This is a high-yield index – so, yes, it threw off higher returns than investment-grade corporates or Treasury bonds.

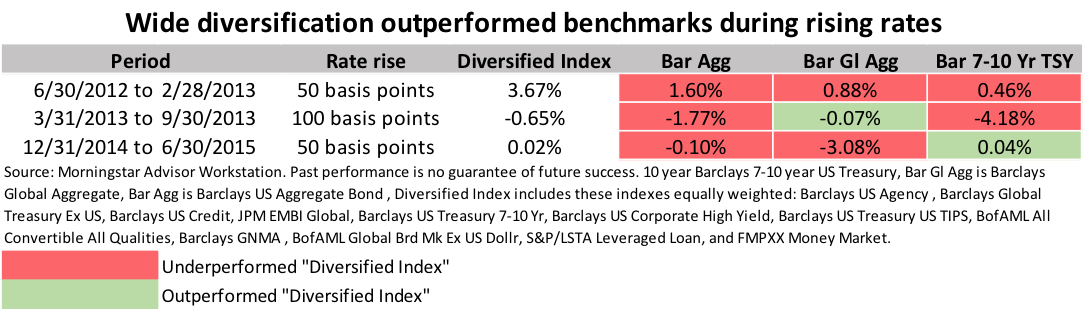

However, Treasury Bills and Bonds earned positive returns as well – Figure 2. Note that shorter maturity T-Bills outperformed longer maturity T-Bonds. First lesson – with rising rates, shorten maturities.

When you realize that rising rates are nothing to fear, you can avoid, if you wish, complex or volatile active management solutions like hedging, optimization, tactical maneuvering, asset concentration or depending on equities to shore up your value. I say “if you wish” because I am not entirely sure the industry wishes to avoid complex and higher risk solutions. Quite the opposite. The industry seems to be leveraging these fears so they can make a more persuasive case for esoterica like adding equities, long-short, hedging, zero-beta, negative-duration, etc.

Equity fund managers are studious about limiting their fixed-income holdings so they can reduce “cash drag.” Likewise, why should fixed-income managers add equities? When they do, with the hope of increasing yields or returns, they introduce a disproportionate level of risk. In 2008, MLPs, REITs and high-dividend stocks (the three favorite bond fund substitutes) were each down over 30%. When you substitute MLPs and REITS for bonds you are adding volatility to the Barclays U.S. AGG by six-fold and eight-fold respectively. [Source: The trailing 10-year standard deviations, as of September 30, 2015: MLP: Alerian MLP TR Index 18.55, REIT: MSCI US Real Estate Invst GTRust Price 27.88, US AGG: Barclays U.S. Aggregate Index 3.23, Thomson Reuters]

What’s happened lately?

In 2012, I argued in Advisor Perspectives that the bear market in bonds that lasted from roughly 1950-1982 produced positive (not negative) total returns in bonds. In 2013, I revisited the topic and attempted to show that shorter maturities and wider diversification were a better risk-adjusted return strategy than adding high-yielding equities.

What about now? Since January 2012, 10-year Treasury bond yields have risen more than 50 basis points in less than one year, three times. In these periods (below) a hypothetical fully-diversified, equally-weighted, fixed-income portfolio almost always out-performed the Barclays U.S. AGG, Barclays Global AGG and Barclays 7-10 year Treasury indices. (Note: these are index returns, not fund returns. Indexes are not investable.)

I believe that the “diversified index” (or what I call 3Twelve™) out-performed for three reasons: wider diversification, shorter-duration and equal-weighting. (No fees were assumed for any of the above indexes)

The benefits (and pitfalls) of equal-weighting stocks is well known. In the last 25 years the S&P 500 equal-weighted Index has outperformed the S&P 500 index by 1.25% annually. [Source: Morningstar, Inc., S&P 500 TR vs S&P 500 Equal-Weighted TR, 9/30/1990 through 9/30/2015, past performance is not indicative of future results.] The reason may be because equal-weighting corrects for the large-cap growth bias in the S&P 500 by boosting small-cap value, which has historically outperformed. (A pitfall is concentration risk – relatively tiny companies have as much leverage over your portfolio as trusted giants.)

Can fixed-income benefit from the same advantage? Market-weighting in equities assures that larger companies dominate. This is a good fiduciary move. Although one can argue whether market-weighting or equal-weighting equities will outperform, market-weighting equities biases to quality.

However, the opposite is true for market-weighting fixed income. Market-weighting fixed income over-weights heavy borrowers, which is not the kind of exposure investors may want. And when you equal-weight, you raise percentages in asset classes like senior-loans, convertible/preferred, TIPS and high yields, none of which are found in the Barclays Global AGG. The net result is potential higher returns. However, higher returns are not free – you also are exposed to more concentration risk and a slightly lower average credit quality. My research suggests that this risk-reward trade-off is worth it.

There are 304 fixed-income ETFs and not one is equally-weighted in all major fixed-income assets. Instead of doing the most obvious – equal-weight the universe – the industry has 304 ways to say “no” to diversification.

Why do we treat bonds differently than stocks?

Something strange happens when advisors talk about bonds. They discard everything they know about investing, as if the laws of fixed-income investing are outside of the established norms we use for other asset classes. They forget about market cycles, buy and hold, dollar cost averaging and the benefits of diversification.

Why should the owners’ manual for investing in bonds read differently than that of stocks? Most advisors recommended that clients hold stocks even when the market fell 37% in 2008. We rarely recommend that clients shun stocks just because a bear market might be around the corner – cut back, perhaps, but not avoid completely. So why do we advise clients to avoid bonds if rates increase?

Additionally, advisors misdiagnose the average fixed-income investor. We imagine that bond investors are spending their monthly income on a house note, the electric bill, groceries, etc., when actually 86% of bond fund dividends are reinvested (ICI Fact Book 2015, Table 29, page 301). Many bond fund investors are total-return investors – not income investors. So, the yield chase is led by the advisor, not the investor.

The remedy is simple and low risk. In a rising-rate environment, investors need to widely diversify, shorten maturities and equally weight. If widely diversified equal-weighted indexing works for stocks, it can work for bonds as well. This is how bond investors may have the opportunity to succeed no matter what Janet Yellen does.

Andy Martin, is president of 7Twelve Advisors, LLC, registered securities principal for Girard Securities, Inc., creator of the 3Twelve™ Total Bond Portfolio, and author of Dollarlogic: A Six-Day Plan to Achieving Higher Returns by Conquering Risk.

Thomson US: Corp - High Yield - MF is an equal weighted index of mutual funds within the stated investment category. Funds in this category seek high current income by investing a minimum of 65% of its assets in generally low-quality corporate debt issues. The funds represented by this index involve investment risks which may include the loss of principal invested. This index represents the component funds at closing net asset value and includes all annual asset-based fees and expenses charged to those funds, including management and 12b-1 fees.

Index performance charts and data displayed depict hypothetical investment for illustrative purposes only. It does not include any deduction for fees, expenses, or taxes.

It is not possible to invest directly in an unmanaged index.

The information included in this report is based upon data obtained from public sources believed to be reliable; however, Thomson Reuters does not guarantee the completeness or accuracy thereof.

Thomson Reuters, an independent information services firm, has been the leading provider of information and analytical services on investment products to financial professionals for more than 55 years. Thomson Reuters information and software is used by more than 140 financial institutions nationwide, representing more than 200,000 investment professionals.

Andy Martin is not affiliated with Thomson Reuters or any of its subsidiaries.

The information contained herein, while not guaranteed, has been obtained from sources which we believe to be reliable and accurate. This material is not to be considered an offer or solicitation regarding the sale of any security.

Barclays Aggregate Bond - The Barclays Aggregate Bond Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment-grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

Barclays Global Aggregate Index - The Barclays Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. There are four regional aggregate benchmarks that largely comprise the Global Aggregate Index: the US Aggregate (USD300mn), the Pan-European Aggregate, the Asian-Pacific Aggregate, and the Canadian Aggregate Indices. The Global Aggregate Index also includes Eurodollar, Euro-Yen, and 144A Index-eligible securities, and debt from five local currency markets not tracked by the regional aggregate benchmarks (CLP, MXN, ZAR, ILS and TRY).

Barclays Capital 7-10 U.S. Treasury Index - The Barclays Capital 7-10 Year U.S. Treasury Index includes all publicly issued, U.S. Treasury securities that have a remaining maturity from 7 up to (but not including) 10 years, are rated investment grade, and have $250 million or more of outstanding face value. In addition, the securities must be denominated in U.S. dollars and must be fixed rate and non-convertible.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. Investing in mutual funds involves risk, including the potential loss of principal invested. Risks vary depending upon the strategy used by the fund as well as the sectors in which the fund invests. When redeemed, shares may be worth more or less than the original amount invested. Diversification cannot assure success or protect against loss in periods of declining values.

Read more articles by Andy Martin