Income annuities provide payments precisely matched to a client’s longevity while stocks provide opportunities for greater investment growth. The question remains whether clients should hold bond funds in their retirement income portfolio.

To answer that question, I will first look at the role income annuities play in a retirement plan and then see whether bond funds can fulfill that need equally well.

I will use the term income annuities to include single-premium immediate annuities (SPIAs) and other similar products, some of which provide inflation protection.

Managing retirement risks with income annuities

Income annuities can be viewed as a type of coupon-paying bond that provides income for an uncertain length of time and does not repay the principal value upon death. Much like a defined-benefit pension plan, income annuities provide value to their owners by pooling risks across a large base of participants. Longevity risk is one of the key risks that can be managed effectively by an income annuity. Investment and sequence risks are also alleviated through the more conservative investing approach for the underlying annuitized assets. Income annuities support longevity through risk pooling and mortality credits rather than through seeking outsized investment returns.

Longevity risk relates to not knowing how long a given individual will live. But while we do not know the longevity for a particular individual, actuaries can accurately estimate the longevity patterns for a large cohort of individuals. The “special sauce” of the income annuity is that it can provide payouts linked to the average longevity of the participants, because those who die early will subsidize the payments to those who live longer.

Meanwhile, sequence risk relates to the amplified impact that investment volatility has on a retirement-income plan sustaining withdrawals from a volatile investment portfolio. Even though we may expect stocks to outperform bonds, this amplified investment risk also forces a conservative individual to spend less at the outset of retirement in case their early retirement years are hit by a sequence of poor investment returns. As I discussed in an earlier column, many retirement plans are based on Monte Carlo simulations that produce a high probability of success, which implicitly assumes lower investment returns. An income annuity also avoids sequence risk because the underlying assets are invested by the annuity provider mostly into individual bonds, which create income that matches the company’s expenses in covering annuity payments.

In hindsight, those who experienced either shorter lifespans or who benefited from retiring at a time with strong market returns would have preferred if they had not purchased an income annuity. But income annuities are a form of insurance. They provide insurance against outliving one’s assets. In the same vein, someone who purchased automobile insurance might wish they had gone without if they never had an accident. But this misses the point of insurance. We use insurance to protect against low-probability but costly events. In this case, an income annuity provides insurance against outliving assets and not having sufficient remaining income sources.

There is still an important benefit from income annuities even to those who do not survive long into retirement, especially for those who are particularly worried about outliving their assets. That benefit can be seen by comparing it to the alternative of basing retirement spending strictly on a systematic withdrawal strategy from an investment portfolio. In order to “self-annuitize,” a retiree has to spend more conservatively to account for the small possibility of living to age 95 or beyond while also being hit with a poor sequence of market returns in early retirement.

The income annuity supports a higher spending rate and a license to spend more from the outset of retirement.

With regard to sequence risk, those seeking to “self-annuitize” have two options for deciding how to spend from their investments. They could spend at the same rate as the annuity with the hope either of dying before they run out of money or that their investments earn strong enough returns to sustain the higher spending rate indefinitely. This approach requires acceptance of the possibility that one’s standard of living may need to be cut substantially later in retirement should the hopes for sustained investment growth not pan out. The alternative is to spend less early on and increase spending later if good market returns materialize. The problem with this intention to increase spending over time is that it is the reverse of what most people generally wish to do: spend more early in retirement.

Earmarking assets to fund spending with income annuities

The four financial goals for retirement are lifestyle, longevity, liquidity and legacy. I have just discussed how an income annuity potentially enhances lifestyle from the starting point of retirement. As well, longevity is the fundamental reason to partially annuitize assets. But what about liquidity and legacy?

Income annuities do not provide liquidity or legacy without adding costly provisions that reduce the value of the mortality credits. Intuitively, if you are not willing to subsidize the payments to others in the event you die early, then you have no right to earn the subsidies from others in the event you live long. But there is more to the story about liquidity and legacy. This relates to how an income annuity fits into an overall plan. Often the discussion around income annuities frames the matter incorrectly as an all-or-nothing decision. Partial annuitization lets us think about how we allocate assets toward meeting different goals.

An important point to understand about the assets in a liquid financial portfolio is that a retiree may overstate the degree of control that they have for these assets. Retirees do not really maintain full control over their financial assets because they have a stream of lifestyle spending goals which must be financed in order to have a successful retirement. Those spending goals represent a liability that must be financed by assets on the household balance sheet. Certain assets must be earmarked to fund these liabilities and this has implications for how those assets should be managed. Many retirees end up earmarking more assets than necessary to support income. They therefore spend less than possible because there is no guarantee component with their income and they worry about outliving their assets. The possibility to consider is whether an income annuity provides an explicit way to earmark the assets needed for income in such a way that it frees up others assets for meaningful liquidity.

Iowa-based financial planner Curtis Cloke refers to the non-annuitized assets as “unfettered assets” as they are no longer tied down to cover the spending needs that are met by the income annuity. This opens more flexibility for the unfettered assets to support a liquid reserve to cover unexpected expenses, other surprises to the financial plan or to otherwise support legacy goals. Allocating other assets in a way that accounts for a more secure spending floor can allow a spending goal to be met more cheaply, even with guarantees included, than a pure systematic withdrawal strategy based only on volatile investments. With each retirement income plan, it is important to investigate how to support spending goals most cheaply and efficiently.

Efficient frontier for retirement income

Rather than being tied down by the need to support lifestyle spending goals, the unfettered assets can be invested for growth and legacy. This is the basis of my research on mathematical optimization. In the February 2013 Journal of Financial Planning article, “A Broader Framework for Determining an Efficient Frontier for Retirement Income,” I focused on how to best meet two competing financial objectives for retirement: satisfying lifetime spending goals and preserving financial assets.

Among the assets I considered in the article were stock funds, bond funds and income annuities. The article built on earlier work by Moshe Milevsky and Peng Chen on the efficient frontier for retirement income, which extended the efficient frontier of Modern Portfolio Theory from a single-period to a lifetime focus. There can be a trade-off between these objectives, as locking in spending or reducing portfolio volatility to protect on the downside generally means sacrificing some of the potential growth on the upside. Product allocation considers how different combinations of stocks, bonds and annuities perform in meeting these two objectives. Efficient allocations will do a better job at meeting both of the lifetime objectives.

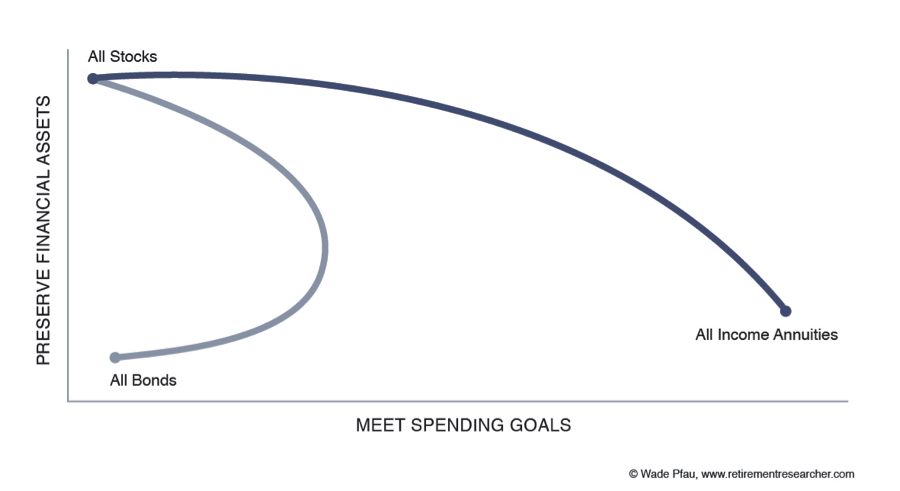

My simulations showed that the efficient frontier for retirement income generally consists of combinations of stocks and income annuities. Perhaps surprisingly, bond funds did not make it to the frontier; they do not serve a useful role in the optimal retirement income portfolio. This result is illustrated in Figure 1.

Figure 1: Retirement Income Efficient Frontier

Bond funds are still volatile and subject to sequence risk. For a retiree meeting spending needs with portfolio withdrawals, bond funds might have to be sold at a loss if interest rates rise. Income annuities sidestep this possibility (as, it should be noted, do individual bonds held to maturity). Interest rate risk becomes inconsequential, because spending amounts have been securely funded.

More importantly, income annuities outperform bond funds as a retirement income tool because they offer mortality credits. For someone wishing to spend at a rate beyond what interest rates can support, bond investments will essentially ensure that the plan fails. For example, someone who is spending at a 5% real rate from a bond fund earning a 0% real rate will run out of assets after 20 years. This is clearly a problem for anyone making it into year 21 of their retirement. Supporting this higher spending rate for longer can be done with income annuities or with more volatile investments that introduce downside risks for meeting the spending goal.

Income annuities are “actuarial bonds” that provide longevity protection unavailable with traditional bonds. Trying to meet a spending objective from a bond fund will inevitably lead to portfolio depletion while income annuities provide income for life. Income annuities are like a bond with a maturity date that is unknown in advance but is calibrated and hedged specifically to cover the amount of spending needed by retirees when they are alive to enjoy it.

More income and potentially more legacy

Since the insurance company providing the annuity is investing those funds primarily in a fixed income portfolio, we should view income annuities as part of the retiree’s bond allocation. There is less of a need for bonds for those non-annuitized “unfettered” assets.

This leads to a counterintuitive result. Liquid financial assets can be larger later in retirement with partial annuitization. Legacy is not irreversibly harmed.

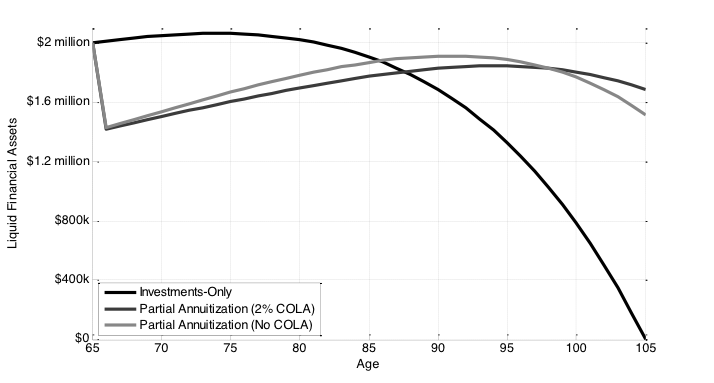

This point will be clearer with a simple example, in which I compare an investments-only retirement strategy with two strategies including partial annuitization. Consider a 65-year old opposite-sex couple who have both just turned 65 and are ready to retire. With a nest egg of $2 million, they budget for $83,255 of spending from their portfolio – with a planned 2% annual spending increase to cover inflation – for the rest of their lives. This represents a 4.16% withdrawal rate from their retirement date portfolio balance. I assume a fixed inflation rate of 2% and real compounded returns of 6% for stocks and 1% for bonds. This ignores sequence risk since these returns are based on my idea of “expected” compounded returns, which would result in a 50% chance that returns actually end up less. In other words, these are not conservative market expectations.

The couple can spend $82,255 with these market assumptions because they worry about outliving their assets. Despite not using conservative investment assumptions, they want to ensure that their retirement plan can be sustained for a 40-year planning horizon. With these market assumptions and their desired retirement asset allocation of 40% stocks and 60% bonds (rebalanced annually), this is precisely how long their wealth will last in the investments-only case.

The other possibility they consider is to annuitize 30% of their financial assets. Treating the income annuity as part of their fixed income allocation, they shift half of their bond holdings ($600,000) into the income annuity while preserving the same amount of stocks as before. With the remaining $1.4 million financial portfolio, their new asset allocation is 57% stocks and 43% bonds, rebalanced annually. While I argue that bond funds are not needed in retirement, the couple was not willing to take my advice to this extreme, so they are still keeping some bonds.

Based on the numbers at my Retirement Dashboard, the payout rate for a life-only joint and 100% survivor’s income annuity with a 2% annual cost-of-living adjustment is 4.24%. The payout rate is 5.37% for a fixed payout with no cost-of-living adjustment. With the COLA, the annuity income grows annually by 2% from an initial base of $25,440. Without the COLA, the annuity provides a fixed $32,220 for each year of retirement. The remainder of the couple’s spending goal is covered through systematic withdrawals from their investment portfolio.

In all cases, the couple is able to fund their spending goal equally well for 40 years. Figure 2 tracks the amount of liquid financial assets remaining as they meet their spending objectives over time. In early retirement, liquid financial assets will naturally be less with partial annuitization. The value of financial assets falls by 30% when 30% of assets are annuitized. Financial assets grow and eventually catch-up again by the mid- to late 80s. This age is still less than the life expectancy for the longest living member of the couple, such that the figure indicates there is a greater than 50% chance that the legacy value of assets will be larger with either type of partial annuitization. This places the odds in squarely favor of having more liquid financial assets at death with partial annuitization. Short-term sacrifice provides potential long-term gain.

Because the no-COLA income annuity provides a bigger initial payout, there is less pressure on the portfolio in the early retirement years, letting liquid financial assets grow more quickly. This advantage is eventually lost as income with the 2% COLA surpasses the no-COLA income by age 78. After that point, the income with the COLA annuity is larger. In the final years of the 40-year period, the remaining assets in the investment portfolio drop quickly and reach $0 by age 105 while partial annuitization continues to support liquidity and legacy.

Figure 2: Liquid Financial Assets – Investments Only vs. Partial Annuitization

The point that partial annuitization provides relief for the withdrawals from the financial portfolio can be seen more clearly with Figure 3. This figure shows the annual withdrawal rate from the financial portfolio needed to meet the overall spending goal after subtracting any annuity income as a percentage of remaining portfolio assets. It stays less with partial annuitization than the investments-only case for three reasons.

Initially, the payout rate from the income annuity is higher than the sustainable spending rate from the investment portfolio. Even though the annuitized assets do not benefit from an equity premium, they do benefit from being calibrated to a shorter planning horizon than 40 years.

Second, as retirement continues, the income annuity supports more of the income goal with mortality credits while the bond component of the investment portfolio continues to create a drag on the sustainable amount of spending. Over time, more of the cumulative retirement spending has been funded by the mortality credits from the income annuities, which relieves pressure on the amount of withdrawals needed from the remaining financial assets. As such, even by age 105 when the investments-only strategy has completely depleted remaining assets, the partial annuitization strategies are still going strong with necessary withdrawal rates below 10%.

Third, the partial annuitization approach also supports greater growth for remaining assets through the higher stock allocation, which is justified at the initial retirement date by considering the allocation to the income annuity as part of the fixed income portfolio. In our example, this permanently raises the stock allocation for remaining assets from 40% to 57%. The greater risk capacity afforded through partial annuitization allows remaining assets to be invested more aggressively for the subset of the household balance sheet representing the financial portfolio. Over time, the overall allocation to stocks increases as the present value of remaining annuity income falls. This relates to my joint research with Michael Kitces that discusses how partial annuitization proxies the benefits of a rising equity glide path in retirement.

Figure 3: Ongoing Withdrawal Rates from Remaining Assets – Investments Only vs. Partial Annuitization

The bottom line

When retirement is short, partial annuitization leads to a smaller legacy (though in the case of short retirement, both approaches still support a pretty reasonable legacy). For longer retirements, partial annuitization offers sound spending support while also fortifying a larger legacy. It is a more efficient retirement income strategy, and that is why income annuities serve as a viable replacement for bonds in a retirement income portfolio.

When the income annuities include provisions for cash or installment refunds, an early death may not leave beneficiaries in any worse shape with regard to their inheritance, than a plan excluding income annuities. This would lose some of the “kick” from mortality credits, so it would effectively trade more legacy wealth in early retirement for less in later retirement. But it is an option for clients not fully convinced by the life-only strategy.

Wade D. Pfau, Ph.D., CFA, is a professor of retirement income in the Ph.D. program in financial services and retirement planning at The American College in Bryn Mawr, PA. He is also a principal and director at McLean Asset Management, helping to build model investment portfolios that can be integrated into comprehensive retirement income strategies. He actively blogs at RetirementResearcher.com. See his Google+ profile for more information.

Read more articles by Wade Pfau