When equity investors want to compare their performance to a broad U.S. index, they use one representing the whole equity market like the Wilshire 5000, or the S&P 500, which is a little less broad. When they want to compare fixed income performance to a benchmark, they usually use a bond index like the Barclays Aggregate.

Several criticisms – I counted three – have been leveled at the bond index recently. I explored these critiques in a wide-ranging conversation with John C. Bogle, renowned founder of The Vanguard Group. My conclusion is that two of these three criticisms are inconsequential or mistaken while the third is meaningful and significant. And yet, one of the discarded criticisms highlights a question I have been curious to answer – and even Bogle himself, one of our most important big-picture thinkers, was not steeped enough in the minute details of index fund investing to answer it.

The three criticisms of the bond index

Inquiries made to people with long experience in the investment field identified three criticisms that have been leveled at the bond index:

- It overweights heavily indebted issuers.

- It may be double-counting some fixed income securities.

- It is not representative of most investors’ fixed income portfolios; this was expressed by Bogle himself in two conversations with Morningstar.com interviewer Christine Benz.

Let us consider these criticisms in turn.

Does the bond index overweight heavily indebted issuers?

This sounds at first like an extension to fixed income of the canard that a capitalization-weighted equity index overweights large companies – that is, those companies with larger amounts of stock outstanding.

However, perhaps it is a little different in the bond case. Dan diBartolomeo of Northfield Information Services said it was related to the concern that many bonds are relatively illiquid and therefore are not priced regularly. As a result their returns tend to be autocorrelated – a consequence, presumably, of the fact that when a current market price is unavailable the default price is the last price the bond was traded at, whenever that was.

If this is true, then the size-weighting of the bond in the index may be inaccurate; those companies with overpriced bonds may be able to force additional debt on indexers who are obliged to accept it at an excessive price.

Bogle thought that such substantial mispricing of bonds in, for example, Vanguard bond index funds was extremely unlikely. If a bond were substantially mispriced it would be obvious from its yield, which would be out of line with that of similar bonds. Vanguard would pursue the pricing source to get to the bottom of the discrepancy. (This pursuit might, in the end, result in a bond price that was re-marked not to market but to model, perhaps a less-than-ideal solution but one that would be less likely to result in a price distortion.)

If the bonds are all efficiently priced – or at least as close to efficient as possible – then there would be no reason to believe that larger issuers are cutting a better deal from index investors or are more risky than smaller issuers (as there is also no reason to believe the same for equities). If an issuer becomes more risky then the process of issuing bonds would become self-limiting. The bonds would have to be issued at higher and higher interest rates and would eventually become unattractive for the issuer, or wouldn’t be bought. In other words, an efficient market would ensure that an issuer wouldn’t issue so many bonds that they would become an unattractive investment. And when the market is inefficient the issue is as likely to be underpriced as overpriced.

Does the bond index double-count?

This criticism is that the bond index could contain a bond while also containing the same bond as part of an asset-backed security. It seems highly unlikely – though possible – that this could be true.

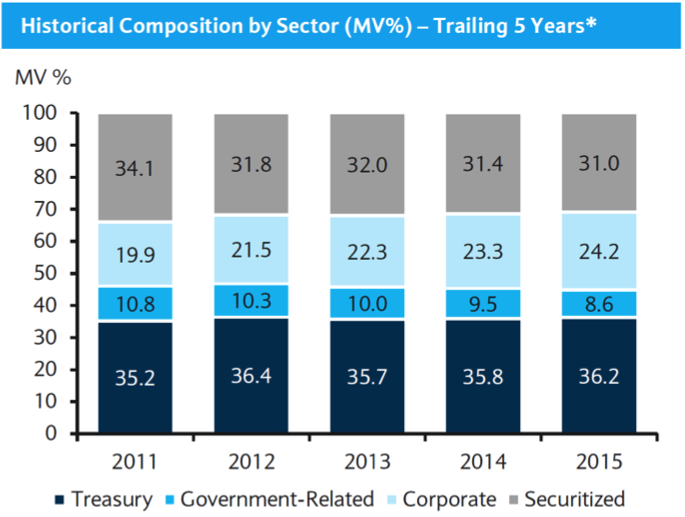

The Barclays U.S. Aggregate Index composition is shown in the following chart:

Source: Barclays Risk Analytics and Index Solutions

The securitized portion consists, according to Barclays, of “MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).”

Thus, the bulk of the securitized portion of the index apparently consists of mortgage-backed securities. Since no mortgages are included elsewhere in the index, these could not be a source of double-counting. The only other possibility is the ABS. It is conceivable that these could include packages consisting, at least partially, of securitized corporate debt, some of which is also included in the index as individual corporate bonds. Nothing specified in Barclays’ document describing the U.S. Aggregate Index (downloadable here) explicitly rules out this possibility. Nevertheless, it is likely that the effect would be negligible even if Barclays had not made an adequate effort to avoid double-counting.

The bond index portfolio is not representative of the vast majority of fixed income investors

Here, the criticisms are those leveled by Bogle himself, and they do bite. About 70% of the U.S. Aggregate Index, according to Bogle, consists of U.S. federal government-issued securities. The total of those securities, according to Bogle, is about $16 trillion. Of that amount, however, at least half is owned by national governments – notably China, Japan, the UK, and, in fact, the United States itself. These securities are held by national governments not so much for their investment potential, but – especially in cases like China – for macroeconomic reasons, for example as dollar reserves to be used to help stabilize currencies and to smooth international credit crises. The United States holds federal securities to fund programs like Social Security and more recently, as a consequence of quantitative easing.

The demand for U.S. federal debt for such purposes has pushed up its price relative to less highly-rated corporate bonds. Hence, funds that replicate the Barclays U.S. Aggregate Index have substantially lower yields than U.S. corporate bond funds.

For example, Vanguard’s Total Bond Market Index mutual fund (VBTLX), which is invested, according to Vanguard’s web site, “about 30% in corporate bonds and 70% in U.S. government bonds of all maturities,” currently has a yield of 2.3% while its Intermediate-Term Corporate Bond Index fund (VICSX) has a yield of 3.5% – a difference of 1.2%.

Bogle argues that the small additional risk of default and slightly longer durations in the corporate bond fund (6.4 years for VICSX versus 5.8 years for VBTLX) does not justify forgoing 1.2% of yield, especially when – in the current interest rate environment – that 1.2% represents a reduction of yield of more than a third. To the extent that standard deviation measures risk, for example, the Total Bond Market Index fund VBTLX has a standard deviation of about 3.0% while the standard deviation of VICSX is 4% to 4.5%. Bogle questions whether this is enough difference in risk to justify a 1.2% premium for corporates.

Bogle believes that we need to fix the bond index. He thinks that a corporate-only index would be the right benchmark, or a mix of perhaps one-fourth governments and three-fourths corporates. That would be representative of the typical investor’s portfolio rather than being representative of the apples-and-oranges combination of the typical investor’s portfolio with those of the Treasuries of China, Japan, the UK and the U.S.

Will the index be changed? Due to the power of inertial forces, Bogle is not sanguine about the possibility of actually changing the most widely followed bond index. He merely recommends that a U.S. fixed income investor hold corporate bonds or perhaps a combination of about three-fourths corporates and one-fourth U.S. government securities. He also points out, unsurprisingly, that average bond fund expenses are about 0.9%, which – again in the current interest rate environment – eats up nearly a third of the typical corporate bond fund’s yield and half that of the aggregate bond index.

Is there a possible index fund scam?

This comes back to the issue I mentioned above.

John Kay, in his book “Other People’s Money: The Real Business of Finance” (which I reviewed here), identified “the problem, evident on the London Stock Exchange, in which companies of doubtful reputation seek listings in order to force holders of passive funds to buy their stock.”

In the early 1980s, in an activity centered largely in Denver for some reason, it was possible to form a company and launch a public offering of around $5 million just by assembling an MBA, an engineer and someone with a marketing or finance resume and preparing the requisite papers. Many vaporous firms were funded this way, resulting in a number of “penny stocks” that sold for pennies per share. Some of these were then utilized by even-more-shady market participants for so-called pump-and-dump schemes. These were the companies that were actually the subject of the recent but somewhat anachronistic movie, “The Wolf of Wall Street.” One of the most notorious pump-and-dump companies was a firm named Blinder, Robinson – sometimes referred to as “blind ’em and rob ’em.”

These pump-and-dump companies consisted of an office with a bank of telephones, which employees with little or no securities experience – or other experience – were trained to staff. These employees were issued directions to open the phone book and call people one at a time and hype certain of these penny stocks. The owners of the pump-and-dump company would have already invested in the hyped stocks. Many of the people called actually invested, helping to drive up the price that the employees quoted, until the company’s employees were suddenly issued new orders to call those people back and tell them, “Now sell!”

Through this trick, the owners of the calling companies earned substantial gains on the stocks that they pumped at low prices and then sold on the manipulated upswings. Some of those owners, however, were subsequently charged with stock price manipulation and dispatched swiftly to jail.

Is there some possibility that similar schemes could swindle index fund investors? I’m not sure I can see how this could be done, but it is something worth thinking about. Innovations in the securities markets are created constantly. Most of them are merely we-win-you-lose plays, but some are outright scams. One way to downplay the risk would be to be less slavish about adhering precisely to the index; that is, to minimizing tracking error.

What does an index fund do about new issues?

This brings me to the question I would like to ask index fund managers. What do they do about new issues? For example, what do they do when there is an IPO or a secondary offering by a company that is already public? Bogle didn’t know the answer and suggested I ask others at Vanguard who would know, which I may do in good time.

My understanding of the IPO process – admittedly not a particularly well-informed understanding – is that the investment bankers who manage the IPO initially call large institutional investors whom they know and offer each of them specified numbers of shares at a specified price (or, they record the investors’ requests for specified numbers of shares at specified prices). Depending on the pushback they receive from those institutional investors and the resulting subscriptions to the IPO, the managers determine the appropriate offering price and sign up the institutional investors to receive their shares.

Are index fund managers among those institutional investors who participate in this process? If so, they would not be quite the passive investors that they ordinarily are – simply accepting the market price – because they would be actively involved in expressing their price preference. Or do they just wait until after the IPO and buy the appropriate numbers of shares on the secondary market?

The same question would apply for bonds. Does the index fund investor participate in the process of setting the coupon and other features of a new bond issue, or does the investor take the passive route by waiting and simply buying a portion of it at the secondary market price?

Some employees at an index fund investment management firm surely know the answers to these questions. I haven’t happened to encounter them yet, but I haven’t made a deliberate search. This could be a topic for discussion of this article. Who is there among readers who knows the answer?

Given the answer to the question, is it possible that it could uncover something that index fund investors should be aware of – some hidden danger?

In a paraphrase of the motto of the American Civil Liberties Union: eternal vigilance is a price of investing. Passive as an investor and the investor’s investments may be, the investor still needs to trust the investment manager to be on the lookout for pitfalls.

Michael Edesess, a mathematician and economist, is a visiting fellow with the Centre for Systems Informatics Engineering at City University of Hong Kong, a principal and chief strategist of Compendium Finance and a research associate at EDHEC-Risk Institute. In 2007, he authored a book about the investment services industry titled The Big Investment Lie, published by Berrett-Koehler. His new book, The Three Simple Rules of Investing, co-authored with Kwok L. Tsui, Carol Fabbri and George Peacock, has just been published by Berrett-Koehler.

Read more articles by Michael Edesess