So far in my series on selecting superior active fund managers, I’ve broken the most promising research into two very different areas of focus: 1) identifying which segments of the market, or which types of funds, are most promising; and 2) what characteristics to look at in the funds themselves. The most interesting research in category 1 was the “active share” analyses by Antti Petajisto, which concluded that closet index funds (which happen to hold a near-majority of assets in the fund industry) tend to be consistent losers on an after-fee basis, while high-active-share funds with a stock-picking mentality tended to beat their benchmarks by 126 basis points a year.

So far in my series on selecting superior active fund managers, I’ve broken the most promising research into two very different areas of focus: 1) identifying which segments of the market, or which types of funds, are most promising; and 2) what characteristics to look at in the funds themselves. The most interesting research in category 1 was the “active share” analyses by Antti Petajisto, which concluded that closet index funds (which happen to hold a near-majority of assets in the fund industry) tend to be consistent losers on an after-fee basis, while high-active-share funds with a stock-picking mentality tended to beat their benchmarks by 126 basis points a year.

But of course not all the stock-pickers were winners, and the winning funds tended to be scattered all over the various sectors of the market. Is there a way to analyze the different segments of the global opportunity set, and determine the best places to look for those outperforming managers?

As it happens, this is exactly the research that is being conducted by Dan Kern, president of Advisor Partners in Walnut Creek, CA. Kern has an unusual background; he spent eight years as a portfolio manager on the U.S. Growth Equity team at Montgomery Asset Management in San Francisco, and then moved over to researching funds as the managing director of Charles Schwab Investment Management.

“Having worn both hats,” he says, “I’ve learned that investment success is frequently a temporary state of affairs. Today’s high flier is tomorrow’s loser.”

Today, before he looks for potential outperforming funds, Kern subjects different sectors of the market to three basic tests, which tell him whether he’ll even bother to look at the funds that operate in that space.

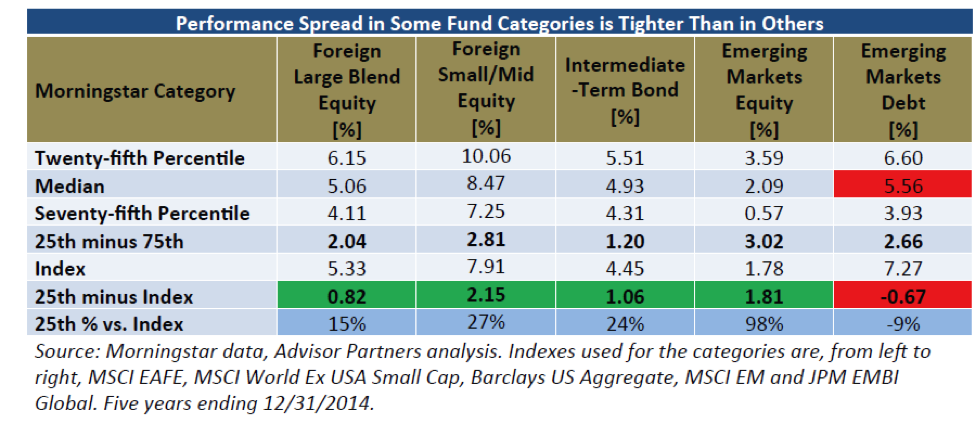

Payoff: the performance spread

Test one is something he calls “payoff.” Is the potential excess return (payoff) worth the risk you would be taking if you decided to invest with an active manager in that sector? Another way to describe this factor is the “performance spread”: Where is it tightest, and least tight?

To answer that question, Kern identified the percentage return that would qualify a fund for the upper quadrant (25th percentile) in different asset sectors, and compared it to the return that a fund would have to achieve to fall into the upper 75th percentile. He also looked at the index return. This allowed him to calculate three derivative figures: the 25th percentile return minus the 75th percentile return, the 25th percentile return minus the index return, and the percentage difference between the 25th quartile fund return and the index.

Figure 1 shows the results for certain foreign stock and bond sectors, plus one U.S. bond sector, for the five years ending December 31, 2014. As you can see, the highest 25th-minus-75th spreads can be found in the emerging markets equity funds sector (3.02% a year), followed by foreign small/midcap equity funds (2.81%). The spread is tightest in the intermediate-term bond category. In reverse order, those two asset classes also have the highest spread between the 25th percentile returns minus the index, and the emerging-markets equity funds have by far the highest percentage difference between the highest 25% of the funds and the index.

Figure 1 – Active-Passive Payoff Analysis

At the other end of the spectrum, the average emerging-markets bond fund loses to the index. The other lowest payoff categories are foreign large-blend equity funds and intermediate-term bonds.

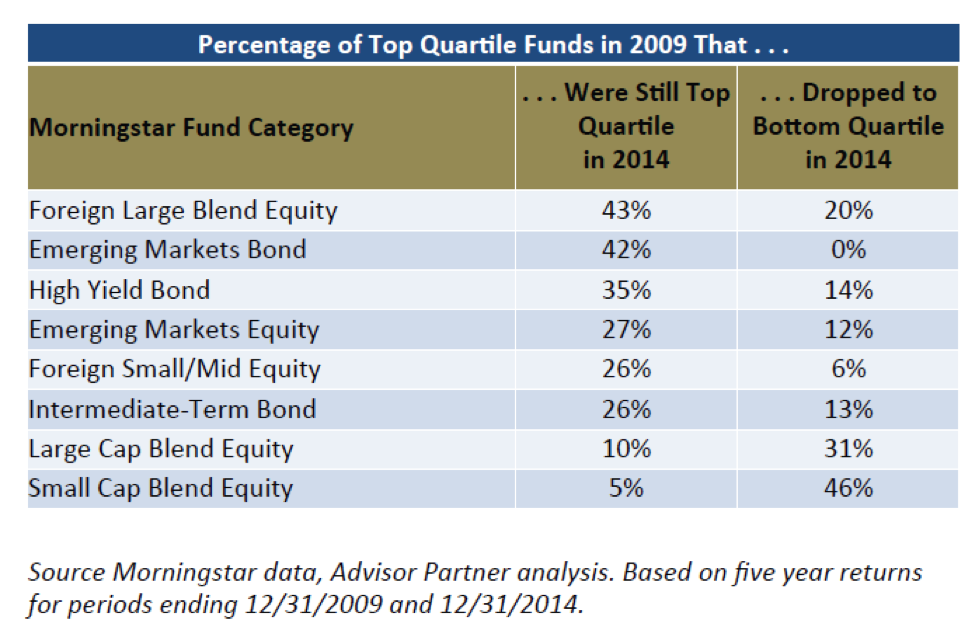

Persistence: luck versus skill

Test two, the second dimension of the analysis, measures what Kern calls “persistence.” The relevant question here is: How often has outperformance been repeatable in this sector? This analysis offers clues as to how much of the success of outperforming funds in the past could be attributable to luck or timing versus skill. If a high percentage of the outperformers are beating their peers on a consistent basis, then your bets on active managers would have a higher chance of succeeding over the next market cycle.

Looking at the data set for five-year periods ending December 31, 2009 and December 31, 2014 (see Figure 2), Kern calculated two figures. First: how many of the top quartile funds in the first time period were also ranked in the top quartile in the second? And: how many first-quartile funds in the first five years had dropped to the bottom quartile during the second period?

Figure 2 – Active-Passive Analysis – Persistence

In Kern’s shop, the analysis covers many time periods. But even if we confine our search to just these two, the results are dramatic. Look at the emerging-markets bond sector, which came out dead last in the previous analysis, because so many of the top-quartile funds were underperforming the index. Of the top quartile emerging-markets bond funds, 42% remained in the top quartile from one time period to the next, and none them had slid to the bottom quartile. Meanwhile, foreign large-blend equity funds, high-yield bond funds, emerging-markets equity funds, foreign small/midcap equity funds and intermediate-term bond funds all had high ratios of consistently outperforming funds vs. funds that slid to the lower ends of the rankings.

At the other end of the scale, only 10% of the large-cap blend equity funds that outperformed in the first time period were able to stay in the upper quadrant during the second, while 31% of the outperformers fell down into the last quadrant. Interestingly, there was far more luck than skill in the small-cap blend equity category; only 5% of the winners persisted, while 46% of the winners in one time period fell into the bottom quadrant in the second.

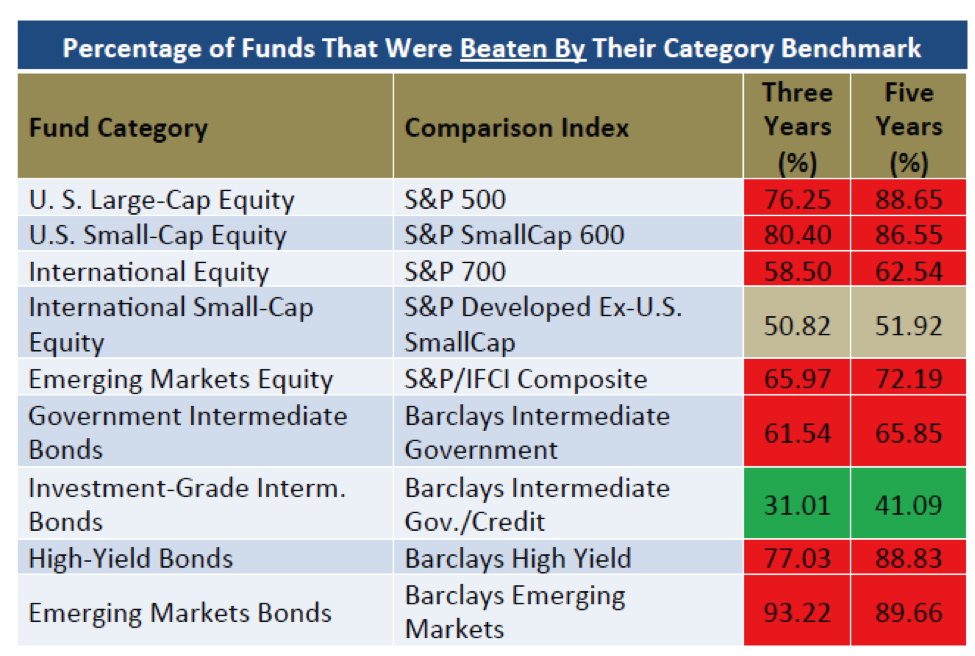

Predictability: the percentage of outperformers

Kern’s third analysis attempts to measure “predictability.” The relevant question here is: What percentage of managers beat a particular index over different periods of time? The theory there is that you would be better off looking for outperforming managers in a sector where they’re relatively plentiful. On the other hand, you want to stay away from picking active managers in markets where they’re rare and therefore harder to find.

Figure 3 looks at the five years ending December 31, 2014. It lists the investment category and the benchmark that Kern believes most closely matches the asset class. From there, he simply calculates the percentage of funds that were beaten by their benchmark index in each category. The fund categories that had the fewest winners (or, calculated this way, the most losers) compared to the index are color-coded red, and efficient-market believers will be cheered to see how much the chart is dominated by this color. The biggest loser is emerging-markets bonds, where more than 93% of the funds failed to beat the index over the past three years, and almost 90% underperformed over five years.

Figure 3 – Active-Passive Analysis – Predictability

But there are a couple of important anomalies in this analysis. Roughly half of all international small-cap equity funds defeated their benchmark, and a majority of investment-grade intermediate bond funds were winners.

Inefficient benchmarks

Advisor Partners is in the business of creating model investment portfolios for advisors. When I talked with Kern, his firm had interpreted this messy dataset in an interesting way. It was investing passively in the large-cap U.S. stocks, international equities and commodities. U.S. small-cap equity and emerging-markets equity are mixed; Kern was blending active and passive approaches with the former, and making tactical active allocations in the latter.

Meanwhile, Kern was hiring active management in the international small-cap, international fixed-income, and in the investment-grade and below-investment grade U.S. bond sectors. “Our active bets in fixed income,” Kern adds, “are partially a function of our discomfort with the fixed-income indices.”

Indeed, Kern does not attribute the favorable active versus passive numbers to consistently brilliant management in the mutual fund arena, but to serious flaws in the indices. That same reasoning also explains why Advisor Partners is using active managers in the emerging-markets realm. “It's a function of us thinking that in the current environment, the indices don’t represent the opportunity set in emerging markets,” Kern explains. “The popular indices are focused on commodity producers and banks, and are underweighted to emerging industries.”

He also wonders how a true reflection of emerging markets could be so heavily weighted in such developed economies as Korea and Taiwan. “Certain countries may be considered ‘developing’ from a political and social perspective,” says Kern, “but they’re as developed as the U.S. and the U.K in economic terms. I think some of the benchmark providers have left that factor out of their equations.”

Global-bond indices offer a different set of issues. “In the global bond benchmarks, the weightings are based on volume of debt issuance,” says Kern. “Building a fixed-income benchmark based on greater amounts of debt issuance leads you into an adverse selection problem – which is how you had big countries like Spain, Italy and Portugal make up such a big portion of the global ex-U.S. bond indices.”

Kern thinks you could say the same thing about U.S. high-yield indices, which currently have a meaningful concentration in energy companies. “They’ve issued an awful lot of debt to fund their capital expenditures,” he says. (Think: fracking.)

Sustainability and diversification

Having inefficient benchmarks is one characteristic of an asset class that favors active managers. Another is whether there are a lot of analysts stepping all over each other with overlapping reports or, on the other side, where there happens to be very little analyst coverage.

“The classic example of the former, of course, would be U.S. large-cap,” says Kern. “Wall Street has analysts closely following all the U.S. large-cap stocks, to the point where you see public debates in the press about individual company valuations and immediate analyses whenever there’s an announcement. Everybody has a pretty good idea what’s going on with each company.”

He says the role of luck versus skill in that sector may be higher than in some of the less well-traveled asset classes. Hence the low persistence and predictability scores.

International small-cap presents the opposite dynamic. “There, you have a lot less coverage by Wall Street,” says Kern. “Because of that, there seem to be ample opportunities for active managers to win in that space.” The problem there, he adds, is the difficulty of navigating any small-cap realm effectively when your success is rewarded with billions of dollars of new money. That’s how funds become closet indexers.

Once you identify the areas where you’re buying active management, how would you control for factors like a pileup of new assets or a change in management? Kern looks at the problem in two dimensions.

First, he says, you have to decide whether a fund management team’s competitive advantage is sustainable. “Will what they do be ultimately arbitraged away by new entrants that either do the same thing or do something a bit better?” Kern asks. “In that vein, I think of the early quant managers who had some informational and computational advantages,” he adds. “But gradually, as more and more managers understood the factors and drivers that were creating this advantage in the marketplace, the new participants created a less fertile opportunity set for the quantitatively-oriented managers.”

The other dimension is a recognition that certain styles and approaches will be in favor at certain times, and sometimes out of favor. “We don’t have a good way to know how this will play out in advance,” says Kern. “So you create a diversified portfolio with different risk and return drivers.”

Based on the data, Advisor Partners can change its mind about whether to go active or passive in different sectors, and it will periodically adjust the allocations, ‘leaning ‘ (as Kern puts it) away from higher valuation asset classes. In addition, he’ll look for active management when certain asset classes are traveling through a period of high uncertainty. Today’s bond markets, driven in part by competing and ever-changing central bank interventions in the U.S., Brussels, Japan, China and elsewhere, and by unprecedented issuances, are unpredictable to the point of being chaotic, so he sees value in active management in this unusual time period. As bond issuance returns to normal, as market forces are again given control of rates, he may drop back to a more passive position.

Neglected areas of research

There is, of course, much more to analyze. “Going forward, we want to do some follow-on research on how managers outperform and underperform,” says Kern. “What are the common factors? Right now, we have a flat set of findings, with perhaps a working hypothesis on the findings. But we don’t have a deeper dive into the how and why.”

Specifically, Kern would like to know whether active share is a predictive factor or coincidental with market-beating performance. “I want to structure it by asset class,” he says, “and really isolate whether active share is just a large-cap phenomenon, or whether there is a benefit to the active share metric in other asset classes where the indexes are not as top-heavy as large cap is.”

This would allow him to control for size, volatility, beta, value and momentum, and see where active share managers might be adding their value. And he wants to extend the research time period beyond 2009.

Kern is also curious about underperformance. “Why some managers profoundly and consistently underperform is a neglected area of research,” he says. “It seems to be easier to consistently underperform the market by a wide margin than you would imagine would be possible in a moderately efficient market environment.”

Are the drivers for underperformance the mirror image of the reasons for outperformance, or are there different things going on? Avoiding the losers could, theoretically, be a big success factor in selecting active managers.

And Kern has a socially responsible investing (SRI) research project on his plate for 2015. “I would like to look at that population of managers,” he says, “and identify, from a risk/return perspective, how well that population has done over rolling time periods.” In other words, look at the SRI analytics that managers have employed as additional investment analysis that might prevent certain negative surprises from showing up. (Think: huge cleanup costs for decades of dumping toxins in the nearest river, or being publicly exposed for running sweatshops in emerging Asian nations.)

The bottom line here is the same as it was in parts I and II of this series: Kern’s research suggests that selecting benchmark-beating active managers in certain asset classes is not the impossible task that some believe it to be. By attempting to narrow his search, Kern has discovered inappropriate indices (and a host of index funds tied to them), and segments of the global opportunity set where active managers are more plentiful, more persistent and somewhat more predictable.

Bob Veres' Inside Information service is the best practice management, marketing, client service resource for financial services professionals. Check out his blog at: www.bobveres.com. Or check out his Insider's Forum Conference (for 2016 in San Diego) at www.insidersforum.com.

Read more articles by Bob Veres

So far in my series on selecting superior active fund managers, I’ve broken the most promising research into two very different areas of focus: 1) identifying which segments of the market, or which types of funds, are most promising; and 2) what characteristics to look at in the funds themselves. The most interesting research in category 1 was the “active share” analyses by Antti Petajisto, which concluded that closet index funds (which happen to hold a near-majority of assets in the fund industry) tend to be consistent losers on an after-fee basis, while high-active-share funds with a stock-picking mentality tended to beat their benchmarks by 126 basis points a year.

So far in my series on selecting superior active fund managers, I’ve broken the most promising research into two very different areas of focus: 1) identifying which segments of the market, or which types of funds, are most promising; and 2) what characteristics to look at in the funds themselves. The most interesting research in category 1 was the “active share” analyses by Antti Petajisto, which concluded that closet index funds (which happen to hold a near-majority of assets in the fund industry) tend to be consistent losers on an after-fee basis, while high-active-share funds with a stock-picking mentality tended to beat their benchmarks by 126 basis points a year.