What is the risk that equity investments won’t turn out as well in the long run as we would like them to? This is obviously a very important question. We are often assured that stock investments will eventually pan out because of “mean-reversion.” However, mean-reversion in securities prices is ill-defined, oversimplified and little more than a physics metaphor. Moreover, some of its presumed effect might be explainable by other means. Reassurances of superior long-term equity performance must, therefore, either derive from less technical justifications, or investors must maintain a secure safety net to guard against poor long-term performance.

Can we rest easy with our equity investments, or do we need to be unceasingly vigilant?

With equity investments, as opposed to fixed income, there is no contractual assurance of receiving any of one’s investment back at all, let alone a positive return. This in itself suggests good reason to be nervous. And yet, we tell each other constantly that we should not be nervous.

We have become accustomed to assuming that diversified investments in equities will do well in the long run. If a time comes when equities drop in value and the sentiment of the market is dark, we assume the “rational” response is not to sell but to hang on because the market will recover in due time.

There are two seemingly very good reasons for making that assumption. One is that if equities don’t provide a good return over 30 years, then something must have gone disastrously wrong. We assume that either this will not happen, or if it does, then no investment strategy will work.

The second reason for making that assumption is that the equity market has recovered again and again from bleak periods in the past – at least the global market did, even if occasionally a national market didn’t.

The Bodie-Siegel debate

Responses to the question of whether equities will perform well in the long-run have ranged from very reassuring to not very reassuring at all. As David Blanchett, Michael Finke and Wade Pfau point out in a Sept. 23 Advisor Perspectives article, the reassuring end of the spectrum has been associated with Wharton Professor Jeremy Siegel, while the not-very-reassuring end has been represented by Boston University Professor Zvi Bodie.

The two professors present completely different types of evidence. Siegel, in the 5th edition of his book Stocks for the Long Run, makes his argument based on the fact that although stock prices have fluctuated wildly at times from year to year, real returns on stocks were remarkably consistent and very attractive over three long periods of years (1802-1870, 1871-1925 and 1926-2012) – around 6.5% each period, give or take about a tenth of a percent.

Bodie, on the other hand, invokes modern portfolio theory to show that the risk to the value of one’s assets when investing in stocks compared with investing in bonds increases the longer they are owned. This is because the cost of insuring against a shortfall in equity investments relative to bond investments increases over time.

Reasons to doubt Siegel’s view

One reason to be skeptical of Siegel’s data is the time period that it covers. The period since 1800 has been unique in human history. During that period, growth of real global economic product has averaged about 2.7% annually. Prior to that time, for hundreds of years, according to economist Brad DeLong – indeed for millennia – growth averaged between zero and less than two-tenths of a percent per year.

Suppose that in the future, the pace of economic growth went back to the levels of the past, prior to the last 200 years. We assume this cannot possibly happen because we can’t turn the clock backward to pre-technology times. Yet prominent figures such as Northwestern University economist Robert J. Gordon have speculated that economic growth may be much lower in the future. Even GMO founder Jeremy Grantham, a long-time exponent of reversion to the mean, has warned that growth will abate dramatically in coming decades.

What would be the effect of that abatement – or more to the point, of the expectation of that abatement? A drop in the expectation of economic growth from the 2.7% of the last 200 years to well below 1% would have an immediate catastrophic effect on stock prices, causing them to fall by more than half. Indeed, when they did fall by half between 2007 and 2009, it could have been attributed to a sudden drop in the expectation of long-term economic growth. If that low expectation persists, stocks will remain depressed, as they did for many years in Japan.

Siegel’s history of stock-market returns is not enough by itself to ensure that future returns will be as good as in the past. In fact, there is ample reason to worry that they won’t. And if they are much worse because economic growth will be lower, then fixed income will be a safer haven.

Reasons to doubt Bodie’s view

Bodie’s view is also open to question. It is important to note what model Bodie used to calculate the cost of insurance: geometric Brownian motion.1 It is the basis for the vast majority of Monte Carlo simulations, and it is the fundamental assumption of most of Modern Portfolio Theory (MPT), including option-pricing theory.

But doubts have been aired for decades as to whether geometric Brownian motion correctly models real-world price changes. The first questions were raised by Benoit Mandelbrot more than 50 years ago, when the model was in its nascent stages. Mandelbrot observed that distributions of percentage price changes had “fatter tails” than the distribution2 assumed by geometric Brownian motion. That is, extreme price movements are more common than geometric Brownian motion assumes them to be. It is theoretically possible to alter the model slightly to incorporate these fat tails, but it is much easier mathematically to use geometric Brownian motion. That is why it continues to be used.

More recently, the focus of attention has been on a core assumption of the standard geometric Brownian motion model: that returns over different time periods are “independent and identically distributed” (IID).That is to say, the rate of return that actually occurs in one time period, no matter how high or low, cannot alter the probabilities of rates of return in subsequent periods.3

Recent objections to that assumption have often referred to “mean-reversion.” Mean-reversion of rates of return is the financial analog of the physics truism “what goes up must come down.” It implies that if a high rate of return occurs, then the likelihood increases that lower returns will follow, and vice versa. Indeed, mean-reversion would seem, on the face of it, to invalidate Bodie’s result.

However, as I will argue, the concept of mean-reversion in investment returns and most approaches that have been proposed to model it are flawed.

Evidence for “mean-reversion”

Blanchett, Finke and Pfau (BFP) obtain an interesting result in a longer paper that is referenced in their Advisor Perspectives article. In that paper, they construct equity, bond and cash returns for multi-year overlapping periods up to 20 years in length from the 113 years of data for 20 developed countries compiled by London Business School professors Elroy Dimson, Paul Marsh and Mike Staunton (DMS) and reported in a London Business School / Credit Suisse study. They then use a standard risk-averse utility function to find the stock/bond/cash portfolio mix that maximizes expected utility for each multi-year period.

The result is that the equity allocation increases with the number of years in the multi-year period. This suggests that contrary to Bodie, equity risk decreases over time.

I found this result interesting enough to do my own investigation, using the 1926-2013 monthly returns for the CRSP deciles of U.S. stock-market capitalization. This 88-year period is not enough for a statistically significant study of independent (i.e., non-overlapping) 20-year returns, since it contains only four such periods. However, I computed the standard deviations of these returns both for one-year periods and for overlapping monthly rolling multi-year periods.

I then simulated what overlapping multi-year-period standard deviations would be if returns either adhered to an IID process or were serially randomized (i.e., scrambled in time). The result was that standard deviations for the actual multi-year returns were lower than for the randomized returns.

Both the BFP results and my results imply that over the past hundred years or so, the volatility of long-run equity returns – as compared with their short-run volatility – has been less than traditional investment theory would imply.

BFP interpret the result to imply that equity returns “revert to the mean.”

But does it imply that? Does it show that even when equity returns plummet in the short run, we can relax and depend on them to stabilize eventually at a comfortable level? Does it suggest that real equity returns can be reliably counted on to fall within a band of, say, 2-7% in the long run, as they did in the last 100 years,4 whatever may happen in the interim?

No. None of these conclusions are warranted based on BFP’s results or on my results.

The appeal of the mean-reversion interpretation

I believe that two motives cause this leap to a too-easily reached conclusion. The first is that we want to reassure ourselves and others that long-run returns will be what we hope they will be no matter what scary turns they take over shorter time periods. This enables financial advisors to present themselves as stabilizing influences who can reassure investors and prevent them from making rash decisions out of fear and greed, because the advisors know the market’s history (though not its future).

This leads to a second, related motive. We have recently been taught by the faddish behavioral-finance field that investors behave irrationally and make bad decisions. This presumed bad decision-making has all too often been taken to the absurd extreme of assuming that unenlightened investors will always buy at market tops and sell at market bottoms. (Wouldn’t it be great to know someone like that? All you’d have to do is the opposite and you’d get rich quick.)

If equity returns mean-revert predictably but naive investors will mistakenly expect them not to, then there is a reason to advise investors to rebalance their portfolios, and there is a reason to believe the flawed DALBAR studies claiming to show that investors time the market badly because of their irrationality.

The trouble with the mean-reversion interpretation

The mean-reversion interpretation is problematic however, for several reasons.

First, consider the physics analogy, “what goes up must come down.” For an object to come down – to mean-revert – it must earlier have had the momentum to go up. The same goes for securities prices. Before mean-reversion can occur, momentum that persists in carrying prices away from their mean must first occur. Studies of equity returns have in fact found that they exhibit momentum in the short run, from one 3-12 month period to the next. Other studies have found that equity returns exhibit mean-reversion in the longer run, from one 3-5 year period to the next.

Thus, the mean-reversion effect appears to be a momentum-and-mean-reversion effect, not just a mean-reversion effect. The problem with a momentum-and-mean-reversion effect that occurs at vaguely defined, unevenly and randomly spaced time intervals is that it is very difficult to know how to make use of it. If at any moment, momentum can turn into mean-reversion, but you can’t predict when, what use is that knowledge? That is why, for example, periodic rebalancing does not increase returns.

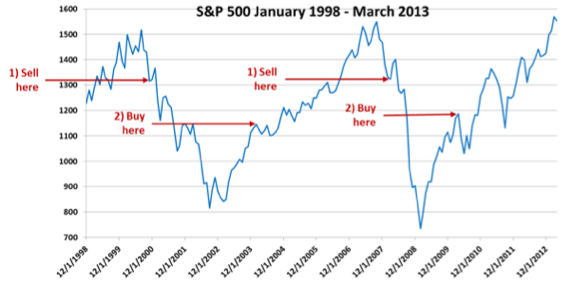

It is also why an irrational investor who buys at market peaks and sells at market troughs will not necessarily do badly, and may even do well. In Figure 1, the investor becomes fearful and panics after a steep drop and sells, then becomes greedy and envious after a steep rise and buys. Note, however, that this investor buys at lower prices than he or she sells. This is more likely to be an accurate picture of an investor driven by fear and greed than one who buys at absolute market tops and sells at absolute bottoms. The simple lesson is that irrational investing is more likely to achieve a random result than a worst-case result.

Figure 1: The legendary irrational investor

The problem with autoregressive models

Some simulation models, attempting to capture the mean-reversion effect, have modeled returns as an autoregressive process. This means that the return in a current time period is modeled as a fixed linear combination of returns in a few previous time periods, plus a random component.

The trouble with this approach is that it presupposes that a mean-reversion that may (or may not) take place at a random time, actually takes place at specific discrete times – such as on Jan. 1 of every year. This is of course inaccurate. Could it nevertheless be useful for some purpose? That is difficult to determine until the proposed use is specified. If one attempts to use this model, for example, to create a market-beating investment strategy, it is unlikely to be of any use.

Another possible explanation for the reduction in long-run volatility

As I described earlier, the volatility of long-run equity returns appears to have been less than the traditional theory of IID returns would suggest. The explanation for this phenomenon may not be easy to determine. (And remember that it is only a historical phenomenon – we don’t know if there is any reason for it to hold true in the future.) It may perhaps be possible, though certainly not easy, to explain it as partly due to the momentum-and-mean-reversion effect.

But another possible explanation presents itself, one that goes back to Mandelbrot’s observation that the distributions of security returns have fatter tails than those implied by the geometric Brownian motion assumption.

As Mandelbrot himself pointed out, there is another family of probability distributions, called stable Paretian distributions, which can be used in an IID model of investment returns. The result is a process similar to geometric Brownian motion, but with fat-tailed returns distributions.

The problem with the stable Paretian distribution is that it does not have a finite standard deviation, which, as I mentioned earlier, makes it difficult to work with mathematically.

It also means that the standard deviation of sample rates of return will increase as the number of returns sampled increases.5 In principle, it will increase without limit.

That means that the standard deviation calculated for a large sample will be greater than for a small sample. There are many independent (non-overlapping) short time periods in history (e.g., one month or one year) but few independent long (e.g., 20-year) time periods. Hence, the sample standard deviation measured for the many short time periods will tend to be greater than the standard deviation measured for the few long time periods.

This could be an explanation of why the rate-of-return volatility measured for longer time periods is greater than geometric Brownian motion would imply, given the short-term volatility.

This explanation is, nevertheless, only conjecture on my part But it is neither more in the realm of conjecture nor more imperfectly defined, than the mean-reversion explanation.

The bottom line is that a conclusion of mean-reversion has been leaped to, among a potential complex of possible explanations for observations derived from the history of investment returns, over only a limited period of 100 years. While more investigation in this area is certainly warranted, we are by no means on firm ground in predicting that equity returns will mean-revert – and therefore that equities will be a safe investment – in the long run.

This argues for a continuing role for secure safety-net investments, such as 30-year U.S. Treasury inflation-protected securities and fixed annuities, even if their return seems to be much less than what you think can be expected from equities.

- Geometric Brownian motion assumes percentage price changes are lognormally distributed and that price changes in non-overlapping time periods are independent of each other.

- Namely, the lognormal distribution (or the normal distribution if percentage price changes are stated as continuously compounded returns).

- Assumes the time periods are not overlapping.

- This is the range of annualized real returns for the 20 developed countries over the 113-year period 1900-2012, as measured by the London Business School / Credit Suisse study. Italy had the lowest return, 2%, while Australia had the highest, 7%.

Read more articles by Michael Edesess