In his thought-provoking 2007 book, The Future of Freedom, commentator Fareed Zakaria lamented the decline of professionals in American public life. At one time, according to Zakaria, professionals – lawyers, accountants, doctors, financial advisors and personal bankers – looked upon themselves as public servants whose high levels of character and conscience were their prized possessions. They “played the role of senior advisors – counselors – to their clients, looking out for their long-term interests.” Often a key service of the advisor was “telling his client he’s a damned fool and should stop.”

This character- and conscience-based professionalism met its downfall, Zakaria says, due to increasing competition, declining elitism and exclusivity in the professions, and an increased government role that made it seem unnecessary for professionals to be the ultimate guardians of conscience.

A profession, says a lawyer quoted by Zakaria, “is now a business, and a damn competitive business at that.”

Professionalism is not dead

And yet, Roger C. Gibson’s fine and exemplary book, Asset Allocation: Balancing Financial Risk, Fourth Edition, shows that character and conscience-based counseling still exist, even in the financial profession. It shows that it is still possible for advisors to look out for their clients’ long-term interests, even if it means telling a client that she’s a damned fool and should stop.

Given the proliferation of amateurish investment advice books lining bookstore shelves today, my expectations for Gibson’s work were modest. “Asset allocation” has become a buzz-term, used frequently as a cover for misinformation-based advisory services. Even when used in its helpful sense – a long-term decision about the investor’s relationship with risk and expected reward – it is often coyly hinted by many advisors that it is a route not merely to balancing risk and return, but to superior returns per se. There’s a reason why so many advisors misstate the conclusion of the famed 1985 Brinson, Beebower and Hood paper on asset allocation, citing it as saying that more than 90 percent of investment returns are due to asset allocation, instead of 90 percent of volatility, as it actually says. The misleading implication is that if you are well-advised on asset allocation, your returns will soar.

I was immediately gloriously surprised by Gibson’s book. The book exudes professionalism, honesty, character, and conscience. It avoids all the coy hints of arcane asset allocation benefits that I expected to find.

The book’s main message is that it is a good idea for U.S. investors to diversify their portfolios beyond U.S. stocks and bonds. It recommends diversifying into real estate, commodities, and non-U.S. stocks and bonds. I am grateful to Gibson’s book for enhancing my knowledge in an area where it was deficient – commodity-linked securities. He explains them clearly, and explains how indexes and mutual funds of commodity-linked securities work, and why they are different from (and preferable to) managed commodity partnerships.

The two worlds of asset allocation

I will further highlight the good points of Gibson’s book by means of a stark, but odious comparison.

I previously reviewed the book The Endowment Model of Investing, by Martin Leibowitz, Anthony Bova, and P. Brett Hammond. That book is just as much about asset allocation as Gibson’s. It could equally well have been titled Asset Allocation: The Endowment Model of Investing.

The parallel ends there. For those who haven’t read my review of the Leibowitz book, I panned it vigorously, and I stand by that review. The following points of comparison between the Leibowitz and Gibson books help show why Gibson’s book is so distinguished.

-

Gibson devotes an entire chapter to a clear explanation of how he arrives at his expected return assumptions. The development of these numbers is imbued with the modesty that is appropriate when making very rough, but reasonable estimates of numbers for which an estimate is required, even if very rough.

By contrast, the Leibowitz book provides no explanation whatsoever for its expected return assumptions, merely saying in a footnote that these crucial inputs were “supplied by an independent source.”

-

More than halfway through his book (Chapter 10) Gibson includes a chapter on portfolio optimization, or mean-variance optimization. He makes it plain that it is not a crucial chapter. In it, Gibson gives a clear explanation why – though the model is to be respected for the insight it can offer, and the modicum of guidance it can occasionally provide for practical decision-making – the mean-variance model does not work for most practical purposes. In fact, Gibson makes little or no use of it in the rest of the book.

By contrast, while admitting – without explaining it very well – that the mean-variance optimization model must be “tortured” in order for it to work after a

fashion, Leibowitz et. al. proceed to run the model overtime to generate virtually all the results in their book.

-

Gibson prefaces one of his chapters with Einstein’s quote, “Everything should be made as simple as possible, but not simpler.” He takes pains to abide by this dictum. For example, in his discussion of the Capital Asset Pricing Model, Gibson feels obliged to use the word “volatility” instead of “risk,” because “volatility” may not accurately represent the full meaning of risk.

By contrast, Leibowitz et. al., while taking note of the fact that there may be risks for “alternative asset classes” that are not captured by volatility, proceed to measure risk as volatility all the same, oversimplifying risk by equating it to volatility.

-

Most egregiously, in the Leibowitz book the word “alpha” appears 1,076 times and “beta” 1,288 times. The assumption of substantial positive alphas for several “alternative asset classes” in Leibowitz’ book sorely requires justification, but none is forthcoming – only the footnote stating that the expected returns were “supplied by an independent source.” Hence, the dubious premise on which the book is based goes unexplained, traced only to a mysterious independent source.

By contrast, in Gibson’s book the word “alpha” appears … not once! No unexplained, dubious assumptions are required to support his recommendations

Telling the client she’s a damned fool and should stop

Gibson offers very helpful advice to the advisor who must fight against the tide of the client’s misguided instincts. He does this by means of hypothetical (but very realistic) dialogues between a recalcitrant client and a gentle but persistent advisor.

For example, when a client’s assets are all in one stock that has appreciated greatly, the advisor may face difficulty persuading the client to sell the stock in order to diversify her investments. The client thinks it is an excellent stock because it has done so well, failing to perceive the risks that may lie ahead.

In this dialogue, Gibson makes the most practical use of behavioral finance concepts that I have seen, identifying each of the client’s objections with a type of irrationality described by behavioral finance.

One can clearly see how difficult it is to be a wise and honest counselor to clients, looking out for their long-term interests. It is easier – and more remunerative – to give up and exploit their misconceptions.

Why must it be so? Why is it so difficult to get clients to understand the simple facts – for example that past performance of an investment vehicle is no guide to its future performance?

Practically everybody knows that a perpetual motion machine is impossible. That’s why we don’t see a huge industry of unscrupulous companies selling equipment that will save on energy bills by creating energy out of nothing.

Why do people know that creating energy out of nothing is impossible? Not because it’s intuitively obvious – its’ not – but because it’s a fundamental building block of basic education.

In the investment field people are not adequately informed of basic truths. Gibson argues that there is a conspiracy against knowledge of the fundamental facts of investing. The conspirators are investors themselves, the skill-based active money management profession, and the financial press.

Because honest advisors cannot rely upon clients’ knowing these fundamental facts, they must practically brow-beat them into accepting well-established statistical truths that they have been brainwashed by financial industry advertising and the financial media not to accept.

Minor problems

In this whole book, a highly critical reader like me finds few things to criticize. One is that more attention is not given to Treasury Inflation-Protected Securities, or TIPS. Gibson introduces them with a kind of fanfare: “1997 was a very good year. Quietly, a new asset class was being born – Treasury Inflation-Protected Securities (TIPS).”

Unfortunately, he doesn’t follow up on that drumroll by thoroughly integrating TIPS into his recommended portfolios. The first edition of Gibson’s book was in 1990, while TIPS were introduced in 1997. Perhaps Gibson just hasn’t fully updated his book. Or perhaps it is not obvious to him yet how to treat TIPS in the asset allocation context.

A second quibble is that he repeats the common canard about the benefits of dollar-cost averaging. Though harmless, widespread beliefs about the benefits of dollar-cost averaging are wrong.

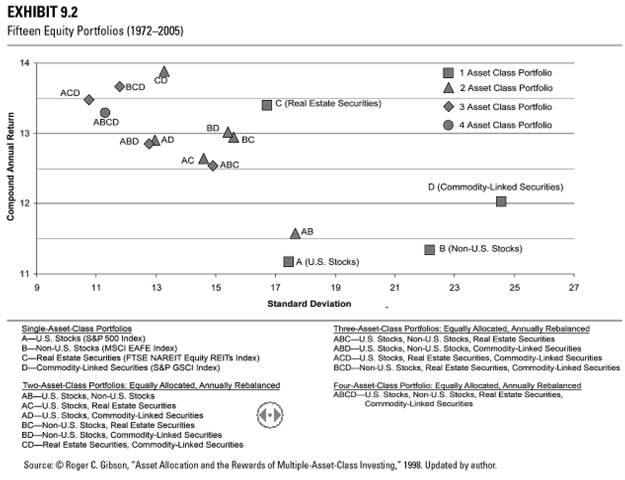

An important graph

On page 182 of his book, Gibson presents, as Exhibit 9.2, an all-important graph. It illustrates the benefits of diversification across asset classes. He considers this graph so important that he presents it again as Exhibit 12.3 on page 260. I reproduce it here:

It shows, for example, that portfolio ABD, an equal-weighted combination of U.S. Stocks (S&P 500), Non-U.S. Stocks (MSCI EAFE), and Commodity-Linked Securities (S&P GSCI), rebalanced annually, has a standard deviation more than four percent lower than the standard deviation of the least volatile of its constituents, and an annualized return almost one percent greater than the highest return of any of its constituents.

At first glance, I thought this was wrong. It is easy to show theoretically that diversification reduces volatility, but that it cannot by itself increase return above the weighted average return of the portfolio constituents.

But that is for a single period. Graphs of return versus standard deviation usually cover only a single time period. For that case, it is not possible for a portfolio return to be greater than the returns of all of its constituents.

After asking Gibson for his data and checking his result – and then running some simulations of my own, which showed that such a result is not only not impossible, but not uncommon – I became convinced that Gibson’s findings were neither an error nor a fluke. And then, I realized that I had explored this phenomenon before, but had forgotten about it.

As William Bernstein has said, “An understanding of the mechanics of rebalancing is fundamental to sound portfolio management, and yet surprisingly little theoretical attention has been paid to this area.”

This is an understatement. One of the few pieces of advice offered by nearly all advisors is that the investor should rebalance her portfolio periodically to re-establish the strategic asset allocation. Yet an explanation of why the investor should do this is almost always lacking. I myself have doubted whether there is a good reason to do it.

Gibson’s graph seems to present the reason – at least empirically, if not theoretically. It does so very clearly and simply. When I asked Gibson for the data that went into creating the graph, he pointed out to me that it was all there in Exhibit 12.14 of his book on pages 274-275, and indeed it was. True to form, Gibson’s presentation is utterly transparent, no shadowy behind-the-scenes data or research.

Gibson’s results may partially reflect the particular time period. Nevertheless they strongly suggest that the benefit of diversification, with rebalancing, not only applies to reducing risk, but to increasing return as well, as compared with an undiversified portfolio. This opens a Pandora’s box of additional questions. Should one rebalance among more finely-divided asset classes as well, perhaps even among individual stocks and bonds? How often? Where does it end? Bernstein’s lament about the paucity of theoretical attention that has been paid to this area dates back to 1996; it is still just as true now.

Academic papers usually end with recommendations for further research. It’s past time for more theoretical research on the combined effect of rebalancing and diversification. Stay tuned.

Read more articles by Michael Edesess