Summary

- Financial strength and flexibility remain defining features of the midstream sector, with the majority of companies maintaining target leverage ratios between 3x and 4×.

- While leverage ratios vary, U.S. midstream MLPs and C-Corps tend to have lower leverage than the large Canadian midstream names.

- With leverage largely at or below target ranges, companies possess the financial flexibility to fund strategic growth and deliver shareholder returns.

When assessing the financial health of the midstream space, leverage ratios remain a priority for investors. Over the past few years, MLPs and midstream corporations have used robust free cash flow and steady EBITDA growth to pay down debt and strengthen balance sheets. Read more about 2025 leverage ratios across the midstream space and why these metrics matter for investors.

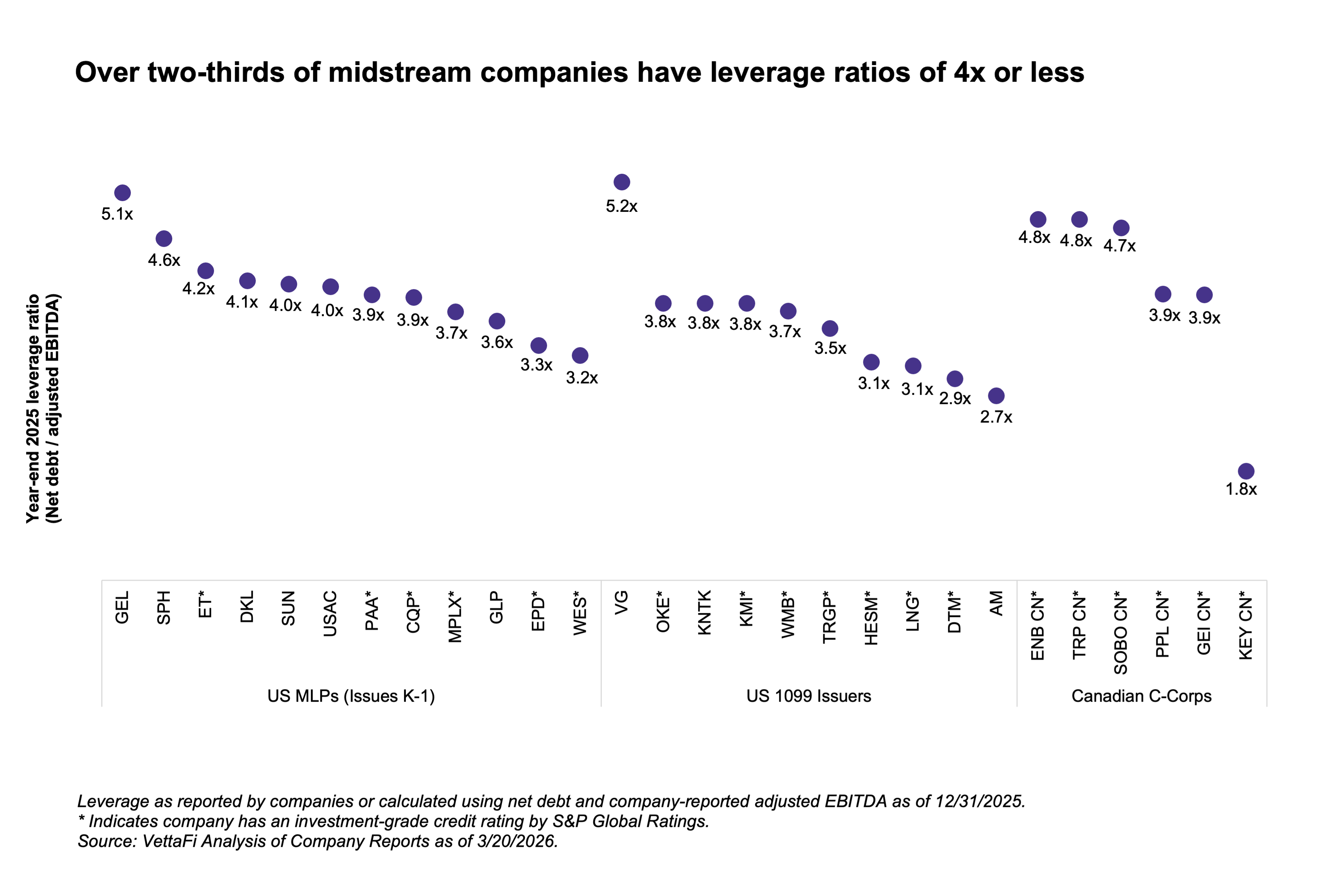

Midstream’s Current Leverage Ratios Are in Line With Targets

A decade ago, it was fairly common for midstream companies to have leverage ratios (defined as net debt/adjusted EBITDA) around 5×. Today, most midstream names have target leverage ratios between 3x and 4×.

The chart below shows year-end 2025 leverage ratios for all constituents in the Alerian MLP Infrastructure Index (AMZI) and the Alerian Midstream Energy Select Index (AMEI), excluding NextDecade (NEXT). Data largely reflects companies’ stated leverage, which could have some variations in the calculations. However, using company-reported metrics provides a cleaner comparison against companies’ leverage targets. It also appropriately accounts for specific capital structure treatments, such as hybrid notes. Some names include pro forma adjustments to prevent recent M&A timing, like Sunoco’s (SUN) Parkland acquisition, from distorting year-end figures. For companies that did not explicitly provide leverage, it was calculated using reported year-end net debt and full-year adjusted EBITDA.

The average leverage among the names shown in the chart below is 3.8×. Of the companies shown with stated targets, the average leverage target is 3.7×. Most companies reported leverage within or near their target ranges. Looking across the sector, over two-thirds of midstream companies currently maintain leverage ratios at 4x or below, though there is some variation.

Midstream Leverage Ratios Vary, With Canadian C-Corps at the Higher End

The U.S. 1099-issuers shown in the chart are uniformly below 4x leverage, with the exception of Venture Global (VG), driven by its capital-intensive buildout of liquefied natural gas (LNG) terminals. DT Midstream (DTM) has seen its leverage come down to 2.9×. The company was upgraded to BBB- by S&P in July 2025, achieving a long-held goal to become investment-grade rated. Antero Midstream (AM) ended the year at 2.7x but anticipates leverage in the low 3x range for 2026, with a $1.1 billion cash acquisition of Marcellus assets pending. On their February earnings call, AM management highlighted how low leverage allowed them to flex their balance sheet for the acquisition, improving after-tax accretion and avoiding equity dilution. AM issued an upsized offering of $600 million in senior notes in December to help fund the acquisition.

MLP leverage ratios tend to vary, though most names fall between 3x and 4×. In 2025, some large names saw their ratios tick up slightly due to heavy capital expenditure or the timing of late-year M&A, which can distort and temporarily inflate metrics.

Plains All American (PAA) reported year-end leverage of 3.9x, even with a pro-forma adjustment to its EBITDA for its Cactus III acquisition. However, PAA expects to get back towards the middle of its 3.25 – 3.75x target after the close of its Canadian NGL divestiture. The majority of the asset sale proceeds will be used to reduce debt. Similarly, MPLX’s leverage rose from 3.1x to 3.7x following significant capital spending in 2025, including its Northwind Midstream acquisition. New debt hit the balance sheet before a full year of earnings could be realized. MLPs have driven much of the sector’s recent M&A activity, announcing bolt-on acquisitions to capture increasing output from the Permian Basin (read more).

The large Canadian C-Corps, such as Enbridge (ENB) and TC Energy (TRP), have historically operated with higher leverage, which fits with their larger project backlogs. ENB is expecting its leverage ratio to stay between 4.5 – 5.0x, while TRP likewise targets a 4.75x leverage ratio. ENB’s secured growth backlog recently increased to approximately C$39 billion. TRP noted its late-stage “pending approval” bucket has grown to roughly C$8 billion, alongside another C$12 billion in early-stage opportunities. Looking ahead, these companies anticipate solid long-term adjusted EBITDA growth, with ENB guiding to 5% and TRP targeting 6% (read more).

Many of the larger names in the midstream space also have investment-grade credit ratings, as denoted in the chart. At the end of February, investment-grade companies accounted for 73.5% of AMZI and 91.5% of AMEI by weighting. Investment-grade credit ratings allow companies to borrow at lower rates and save on interest expense (read more).

Why Does Lower Leverage Matter?

Improved leverage metrics and stronger balance sheets enhance the overall financial positioning of midstream companies. Free cash flow generation further adds to the financial flexibility of energy infrastructure names (read more). These factors arguably ease the path for generous shareholder returns, including dividend growth and equity buybacks. Investors can feel more confident in dividend payouts with companies having strong balance sheets and solid free cash flow generation. As of March 19, AMZI and AMEI were yielding 6.9% and 4.7%, respectively.

Strong balance sheets and investment-grade credit ratings allow companies to more easily access the debt market and at reasonable rates. Lower financing costs can improve returns on acquisitions. Solid financial positioning can also help companies grow and acquire assets without having to raise equity. Equity raises were a common frustration in this space prior to 2015 but have become rare today.

Bottom Line

With leverage largely at or below target ranges, companies possess the financial flexibility to fund strategic growth while consistently returning value to shareholders through dividends and buybacks. This solid financial footing can add to confidence in midstream payouts.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research

Strong 4Q25 Caps Record Year for Midstream/MLP Buybacks

Broad-Based Growth in 4Q25 Midstream/MLP Dividends

Midstream and Rising Canadian Production & Exports

Strong Credit Ratings Dominate Midstream/MLPs

Midstream/MLP Free Cash Flow Yields Still Strong

Midstream Prepares for More Permian Natural Gas

Midstream/MLPs 2024 Leverage Ratios on Target

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, ENFR, and ALEFX, for which it receives an index licensing fee. However, AMLP, MLPB, ENFR, and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, ENFR, and ALEFX.

For more news, information, and analysis, visit the Energy Infrastructure Content Hub.