Key Takeaways

- Six constituents in the broad Alerian Midstream Energy Index (AMNA) spent a combined $818 million on equity repurchases in 1Q26.

- Cheniere Energy (LNG) continued to dominate repurchase activity for the quarter, spending over $500 million on buybacks in 1Q26, following two consecutive quarters of over $1 billion in repurchases.

- Almost three-fourths of AMNA by weighting has a buyback authorization in place, representing 17 constituents.

Quarterly equity repurchases for midstream MLPs and corporations remained healthy in 1Q26 even as stocks saw solid gains. Cheniere Energy (LNG) spent over $500 million on buybacks, and familiar players also used their authorizations during the quarter. Buybacks complement ongoing dividend growth (discussed last week), which tends to be the primary means for returning cash to shareholders. Learn more below about 1Q26 repurchase activity below.

Midstream Buyback Activity Remained Strong in 1Q26

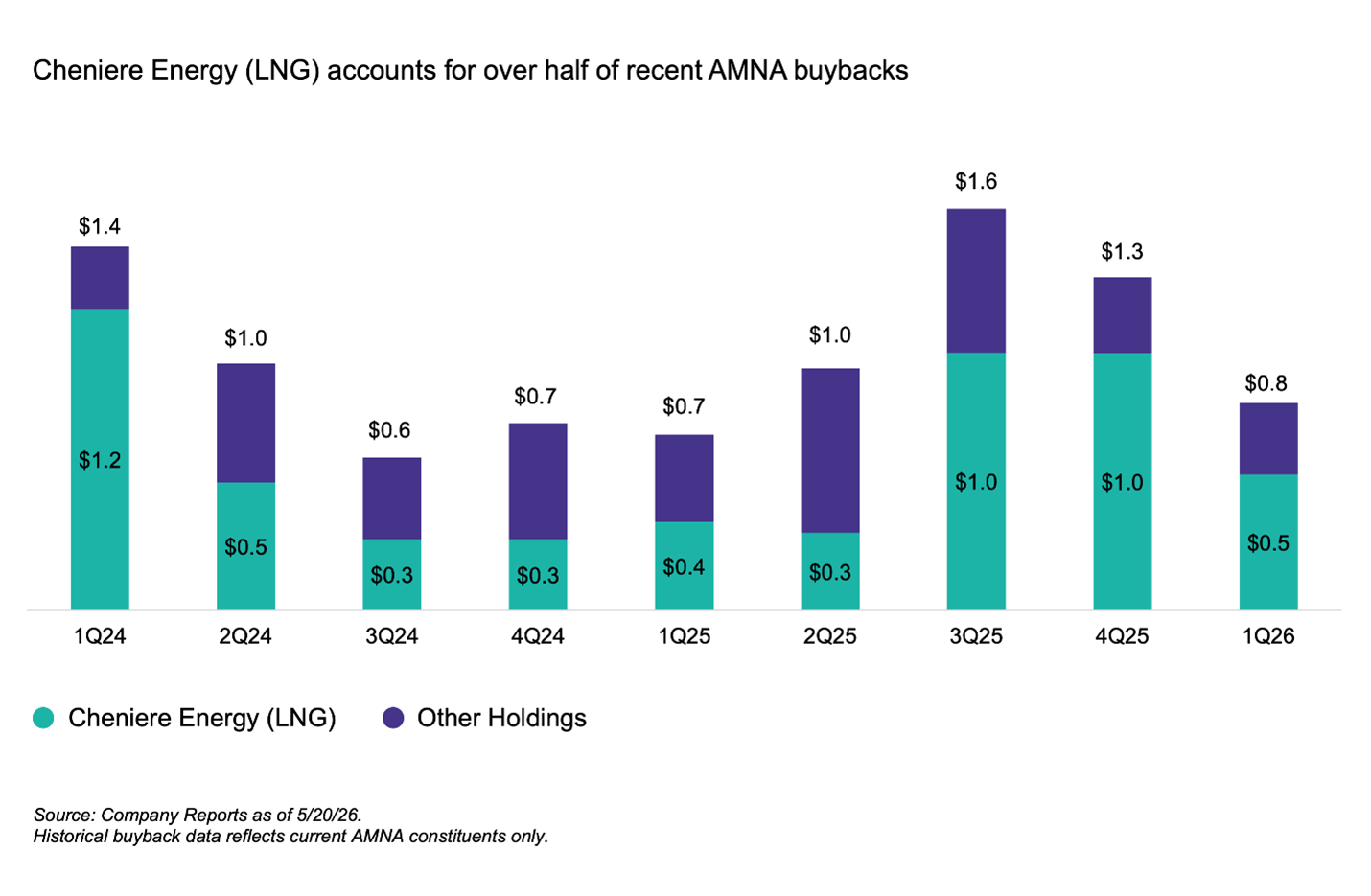

For 1Q26, six constituents of the broad Alerian Midstream Energy Index (AMNA) repurchased an aggregate $818 million in equity, compared with eight names repurchasing a combined $1.31 billion in 4Q25 (read more). For context, 3Q25 and 4Q25 total buybacks were among the highest quarterly numbers ever seen for AMNA constituents, as equity weakness created a buying opportunity.

Cheniere led the way in 1Q26 with $537 million in repurchases. Cheniere has typically had the highest quarterly buyback spend among midstream companies in recent years. The company had two consecutive quarters of over $1 billion in repurchases in 3Q25 and 4Q25. It is worth noting that the stock declined during those prior periods, supporting more opportunistic buying. The buybacks for 1Q26 are particularly notable, considering Cheniere’s shares gained 46.0% on a price-return basis in 1Q26. Cheniere’s Board approved an incremental $9 billion in repurchase authorization in February, bringing its total buyback authorization to over $10 billion through 2030. As shown below, Cheniere’s buybacks were almost 60% of the total for AMNA constituents in 2025. For context, Cheniere was ~30% of the total repurchase spend in 2022.

MLPs Enterprise Products Partners (EPD) and MPLX (MPLX) repurchased "$116 million":https://ir.enterpriseproducts.com/news-releases/news-release-details/enterprise-reports-first-quarter-2026-earnings and $50 million in common units during 1Q26, respectively. For the full year, EPD expects around $1 billion in discretionary free cash flow and plans to allocate 50–60% of it toward buybacks, with the remainder directed to debt retirement.

Targa Resources (TRGP) and Antero Midstream (AM) repurchased $55 million and $18 million in shares during 1Q26, respectively. Of note, Pembina (PPL) recently renewed its Normal Course Issuer Bid, despite not making any repurchases under its prior program that was set to expire in May.

In the past, Hess Midstream (HESM) only repurchased units from its sponsor, but the company began buying back units from the public under Accelerated Share Repurchase programs in May 2025. After repurchasing $80 million in units from the public last year, HESM announced a $60 million repurchase in March, including $18 million of shares from its sponsor, Chevron (CVX), and $42 million from the public. HESM noted the repurchases will increase distributable cash flow per share and provide capacity for incremental distribution growth above its annual target of at least 5% through 2028.

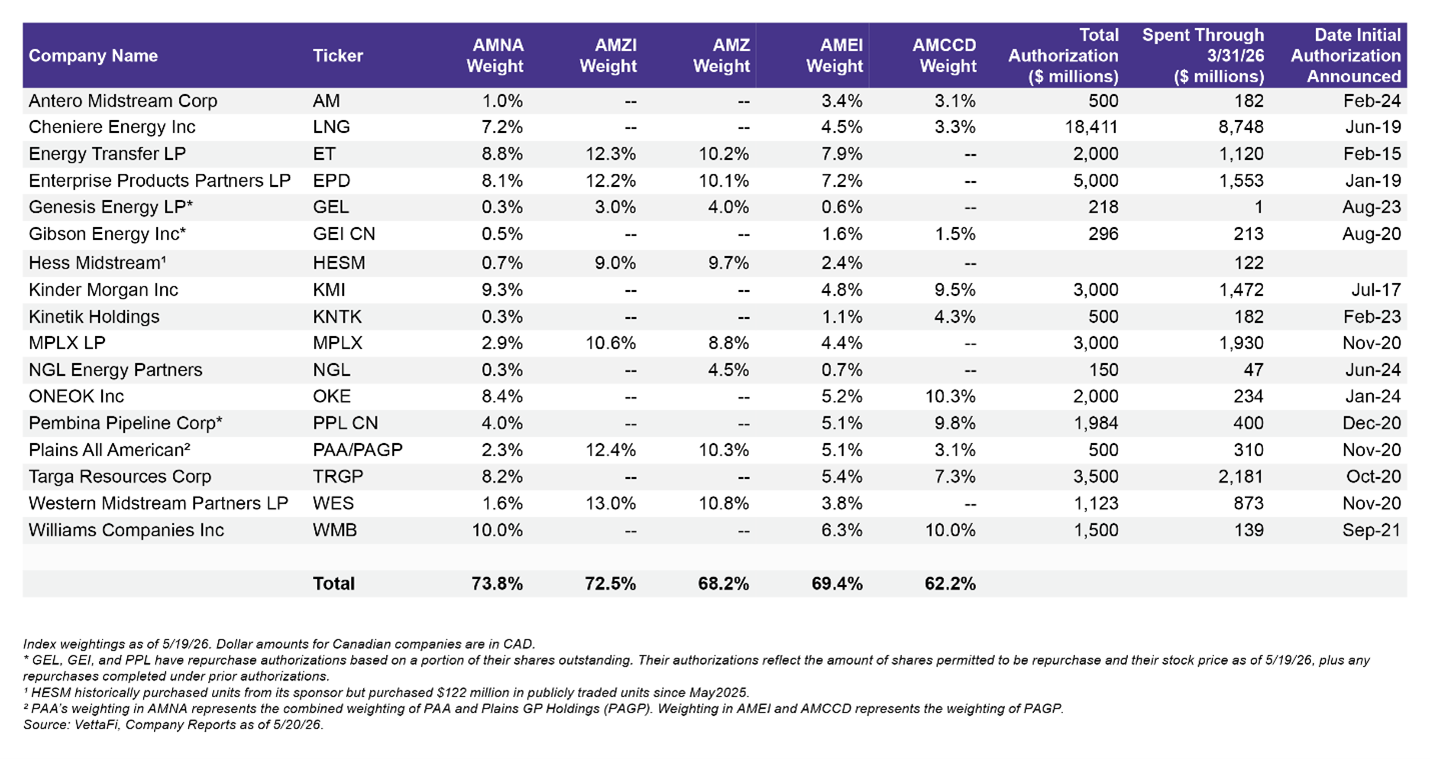

The table below shows the energy infrastructure companies with buyback authorizations and their total repurchases as of March 31, 2026. The table also includes each company’s weighting in AMNA, the Alerian MLP Infrastructure Index (AMZI), the Alerian MLP Index (AMZ), the Alerian Midstream Energy Select Index (AMEI), and the Alerian Midstream Energy Corporation Dividend Index (AMCCD). The majority of the indexes by weighting as of May 19, 2026 have buyback authorizations in place.

Bottom Line

Midstream/MLP buyback activity cooled off with the equity strength in 1Q26, as buybacks continue to compete with other uses of capital, including dividend growth and growth projects. While dividend growth tends to be the preferred method of returning cash to shareholders, select names continue to prioritize buybacks in their capital allocation plans, adding to total shareholder returns.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

AMZI is the underlying index for the Alerian MLP ETF (AMLP ) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB ). AMZ is the underlying index for the JPMCFC Alerian MLP Index ETN (AMJB ), the ETRACS Alerian MLP Index ETN Series B (AMUB ), and the ETRACS Quarterly Pay 1.5x Leveraged Alerian MLP Index ETN (MLPR). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR ) and the ALPS Alerian Energy Infrastructure Portfolio ALEFX. AMCCD is the underlying index for the Alerian Midstream Energy Dividend UCITS ETF (MMLP.LN).

Related Research:

1Q26 MLP/Midstream Dividends: Growth Trend Continues

Strong 4Q25 Caps Record Year for Midstream/MLP Buybacks

Midstream/MLP 3Q25 Buybacks Surged to Record Level

Midstream/MLP Buybacks Jumped in 2Q25

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, AMJB, AMUB, MLPR, ENFR, ALEFX, and MMLP.LN, for which it receives an index licensing fee. However, AMLP, MLPB, AMJB, AMUB, MLPR, ENFR, ALEFX, and MMLP.LN are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, AMJB, AMUB, MLPR, ENFR, ALEFX, and MMLP.LN.