In the week ending January 4th, initial jobless claims fell to their lowest level since February 2024. Initial jobless claims were at a seasonally adjusted level of 201,000, a decrease of 10,000 from the previous week's figure. The latest reading was better than the 214,000 forecast.

Here is the opening statement from the Department of Labor:

In the week ending January 4, the advance figure for seasonally adjusted initial claims was 201,000, a decrease of 10,000 from the previous week's unrevised level of 211,000. The 4-week moving average was 213,000, a decrease of 10,250 from the previous week's unrevised average of 223,250.

The advance seasonally adjusted insured unemployment rate was 1.2 percent for the week ending December 28, unchanged from the previous week's unrevised rate. The advance number for seasonally adjusted insured unemployment during the week ending December 28 was 1,867,000, an increase of 33,000 from the previous week's revised level. The previous week's level was revised down by 10,000 from 1,844,000 to 1,834,000. The 4-week moving average was 1,865,500, a decrease of 3,000 from the previous week's revised average. The previous week's average was revised down by 2,250 from 1,870,750 to 1,868,500.

Here is a closer look at the series since 2007, with a callout to the past 12 months. The four-week moving average, which gives a clearer sense of the overall trend, is currently at 213,000 . This is a decrease of 10,250 from the previous week's figure.

For an even shorter timeline, the chart below shows initial unemployment claims starting in 2022.

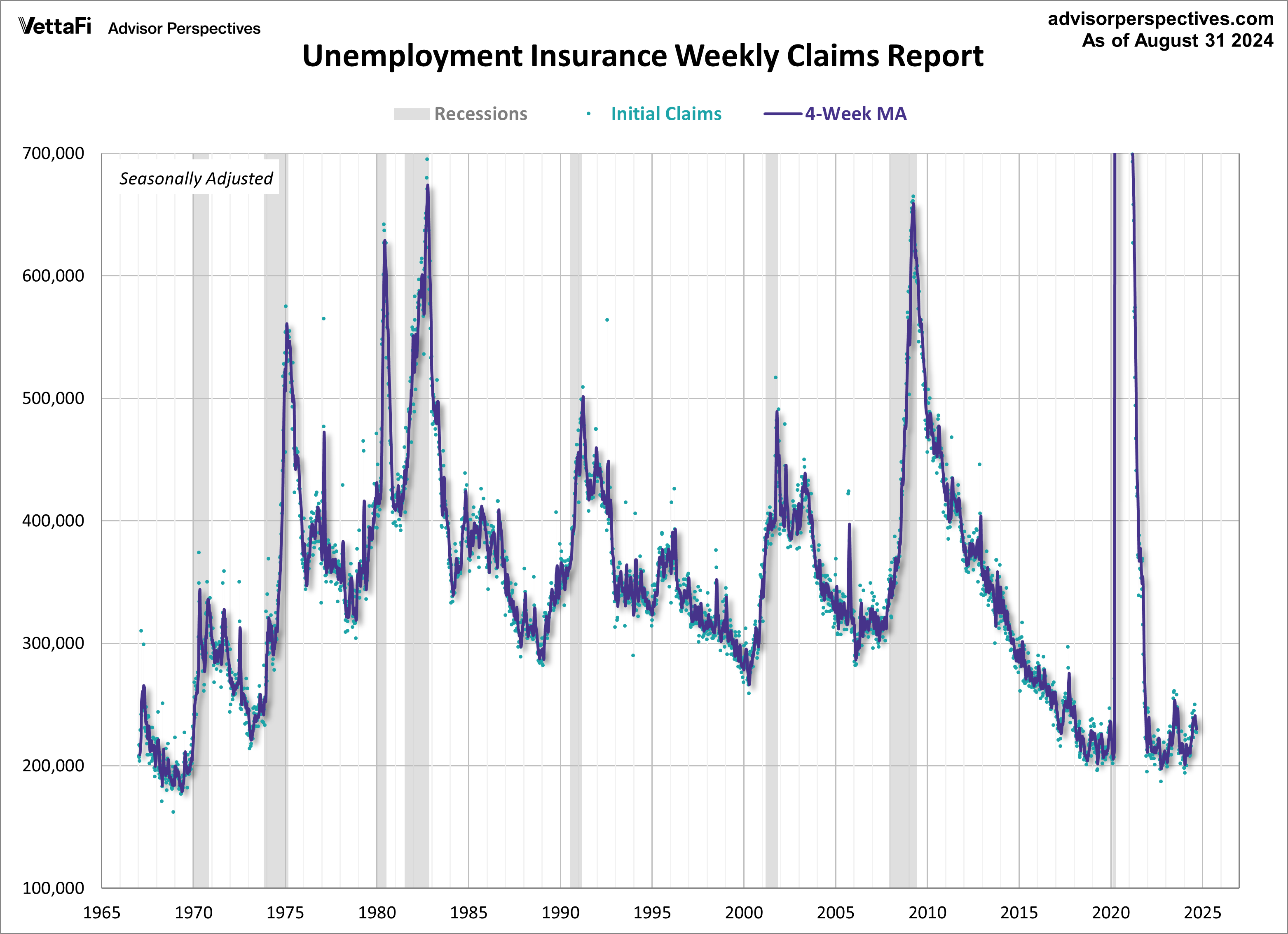

As we can see, there's a good bit of volatility in this indicator, which is why the four-week moving average is a more useful number than the weekly data. Here is the complete data series dating back to 1967.

Outside of the COVID spike, initial unemployment claims have never been greater than 700,000 for a given week. With that said, we've adjusted the y-axis on the chart below so that we can get a zoomed in view of the series where the COVID spike isn't as prominent.

Notice the relationship between recessions and the rise in weekly unemployment claims. To no surprise, the 4-week moving average begins to rise at or before the start of a recession and reaches a relative peak at the end of a recession.

The headline unemployment insurance data is seasonally adjusted, as are the charts above. What does the non-seasonally adjusted data look like? See the chart below, which clearly shows the extreme volatility of the non-adjusted data (the green dots). The four-week MA gives an indication of the recurring pattern of seasonal change (note, for example, those regular January spikes).

Again, in this next chart we've adjusted the y-axis to get a zoomed in view of the series where the COVID spike isn't as prominent.

Because of the extreme volatility of the non-adjusted weekly data, we can add a 52-week moving average to give a better sense of the secular trends. The chart below also has a linear regression through the data (red line), which we are currently below.

Unemployment Claims as a Recession Indicator

For an analysis of unemployment claims as a percent of the labor force, see this regularly updated piece Unemployment Claims as a Recession Indicator.

Here's our list of monthly employment updates:

Job Openings and Labor Turnover Summary (JOLTS)

Full-Time and Part-Time Employment

Unemployment Claims as a Recession Indicator

Five Decades of Middle Class Wages