Producer Price Index: Wholesale Inflation Hits Highest Level Since November 2022

Membership required

Membership is now required to use this feature. To learn more:

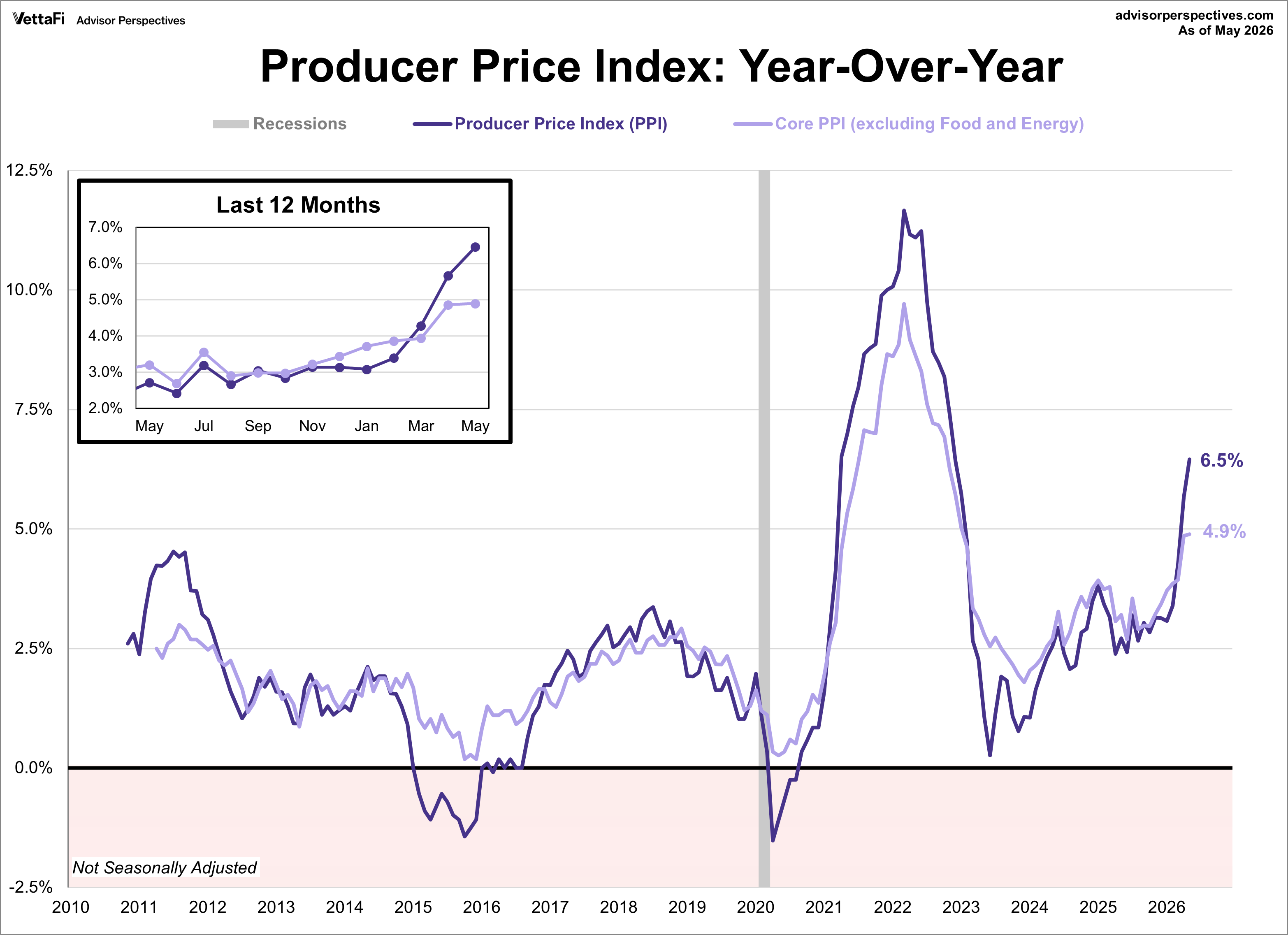

View Membership BenefitsMay's Producer Price Index (PPI) data delivered another blow to inflation watchers, as wholesale price growth came in hotter than expected. Final demand surged by 1.1% for the month, well above the anticipated 0.7% jump and marking the largest monthly increase since March 2022. On an annual basis, headline PPI accelerated from 5.7% in April to 6.5%, its highest level since November 2022 and just above the 6.4% forecast.

Core PPI, which strips out volatile food and energy costs, unexpectedly came in lower than projected. It rose 0.4% for the month, just below the 0.5% forecast. On an annual basis, the core rate remained at 4.9%, notably lower than the 5.4% forecast.

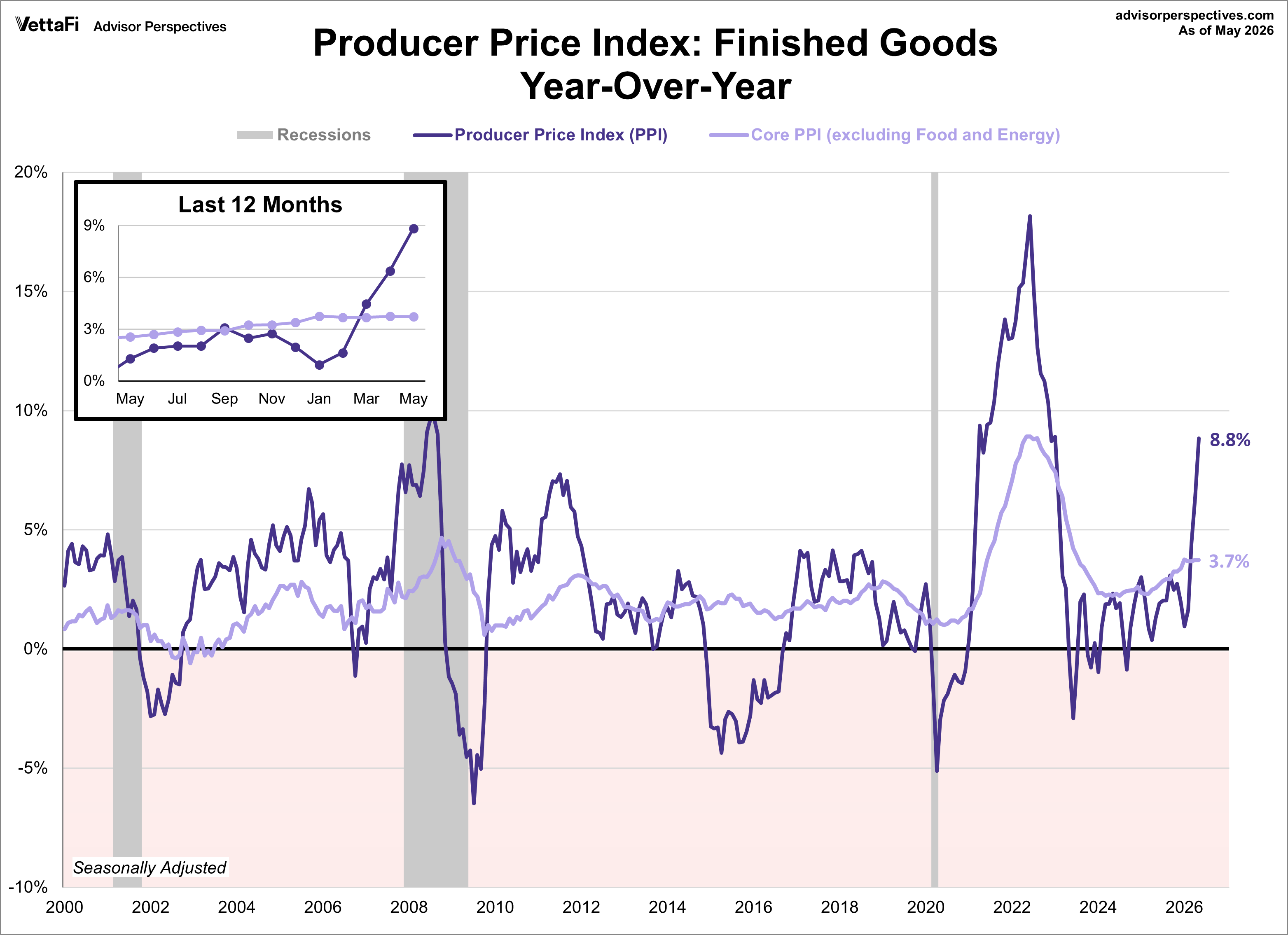

Producer Price Index: Finished Goods

The BLS shifted its focus to the "final demand" PPI series in 2014, but data for these series extend only back to November 2009 for headline PPI and April 2010 for core PPI. Since our analysis emphasizes longer-term trends, we continue to track the legacy PPI for finished goods, which the BLS still includes in its monthly updates. As a later overlay chart will illustrate, the final demand and finished goods indexes remain highly correlated.

In May, the PPI for finished goods was up 2.6% month-over-month, up from 1.6% in April and the largest monthly growth since June 2022. Year-over-year, headline PPI for finished goods accelerated from 6.4% to 8.8%, the highest level since November 2022. Meanwhile, core PPI for finished goods was up 0.3% on the month, down from 0.4% in April. On an annual basis, core PPI for finished goods was unchanged at 3.7%.

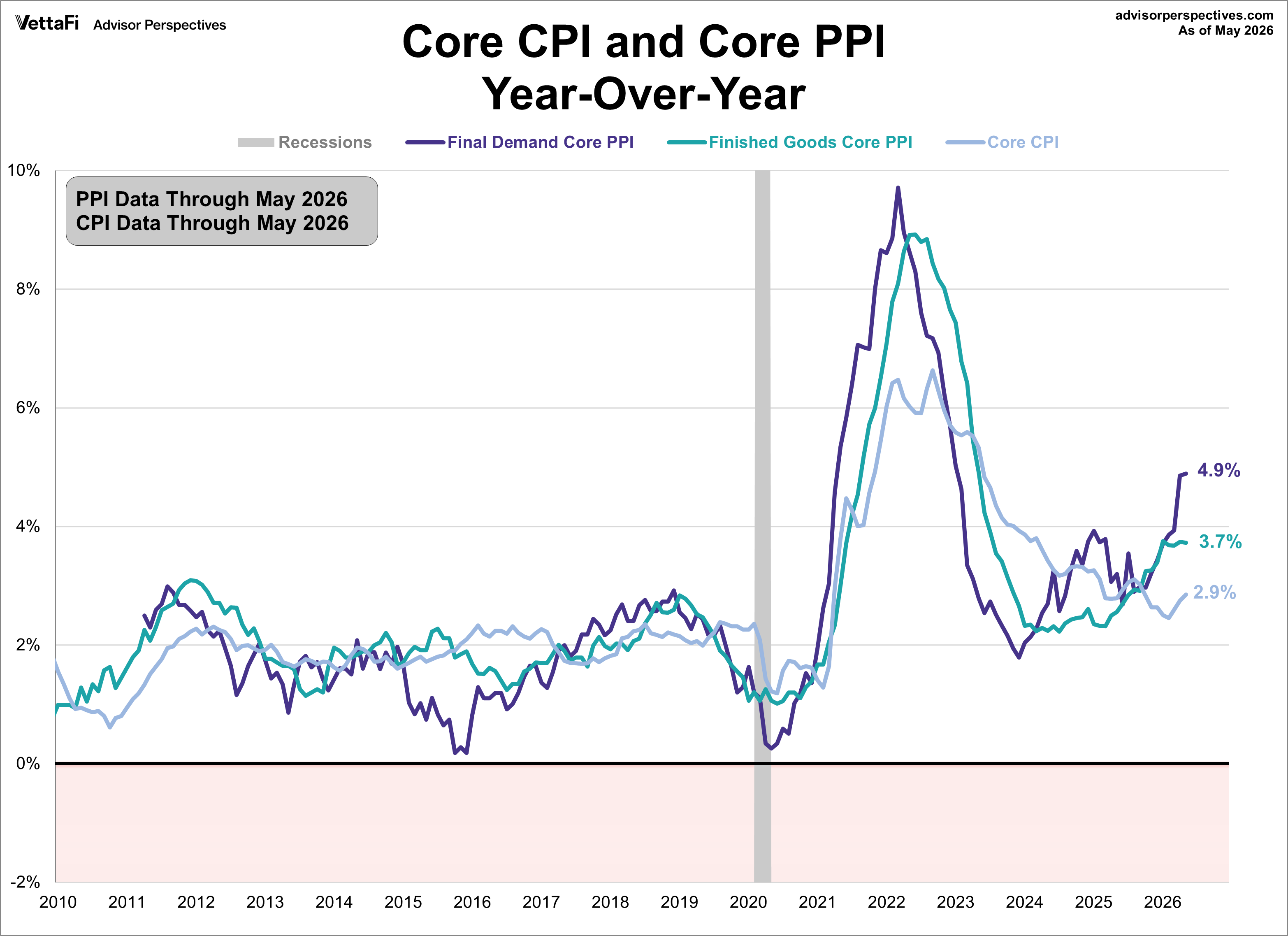

Producer Price Index (PPI) vs. Consumer Price Index (CPI)

Both PPI and CPI illustrate monthly price changes. However, as their names suggest, the Producer Price Index measures price changes from the producer perspective whereas the Consumer Price Index measures price changes from the consumer perspective. PPI is thought to be a leading indicator of consumer inflation because, for the most part, when producers pay more for goods and services they are likely to pass along those higher costs to the consumer. With that being said, during the 2020 recession producers were unable to pass along price increases, demonstrating the higher volatility of core PPI than core CPI. This relationship is further illustrated in the next chart.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Editorial Calendar

View Full Calendar Eastern Time Zone

+ Add the editorial calendar to your Google Calendar.

Upcoming Virtual Events View All