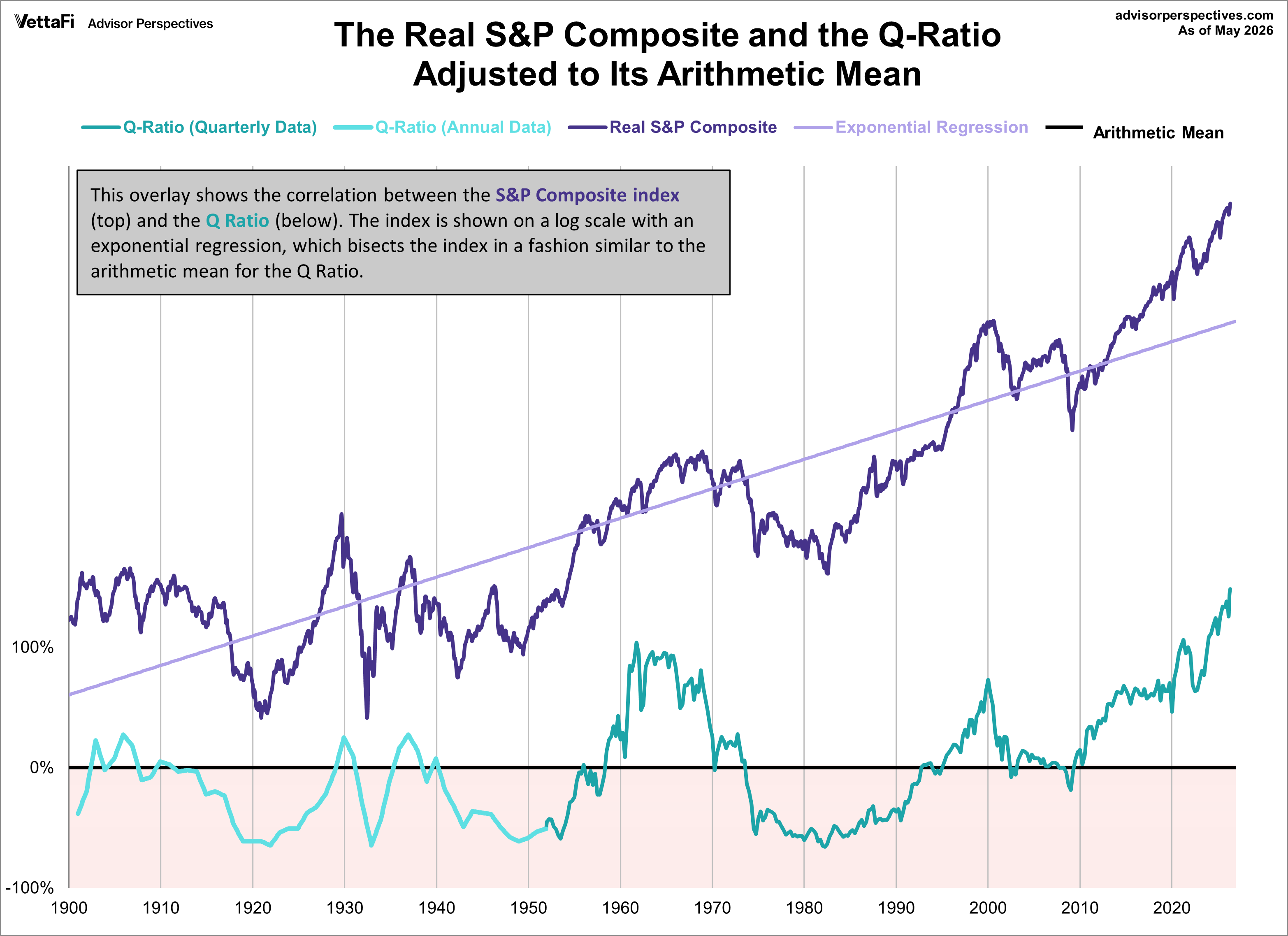

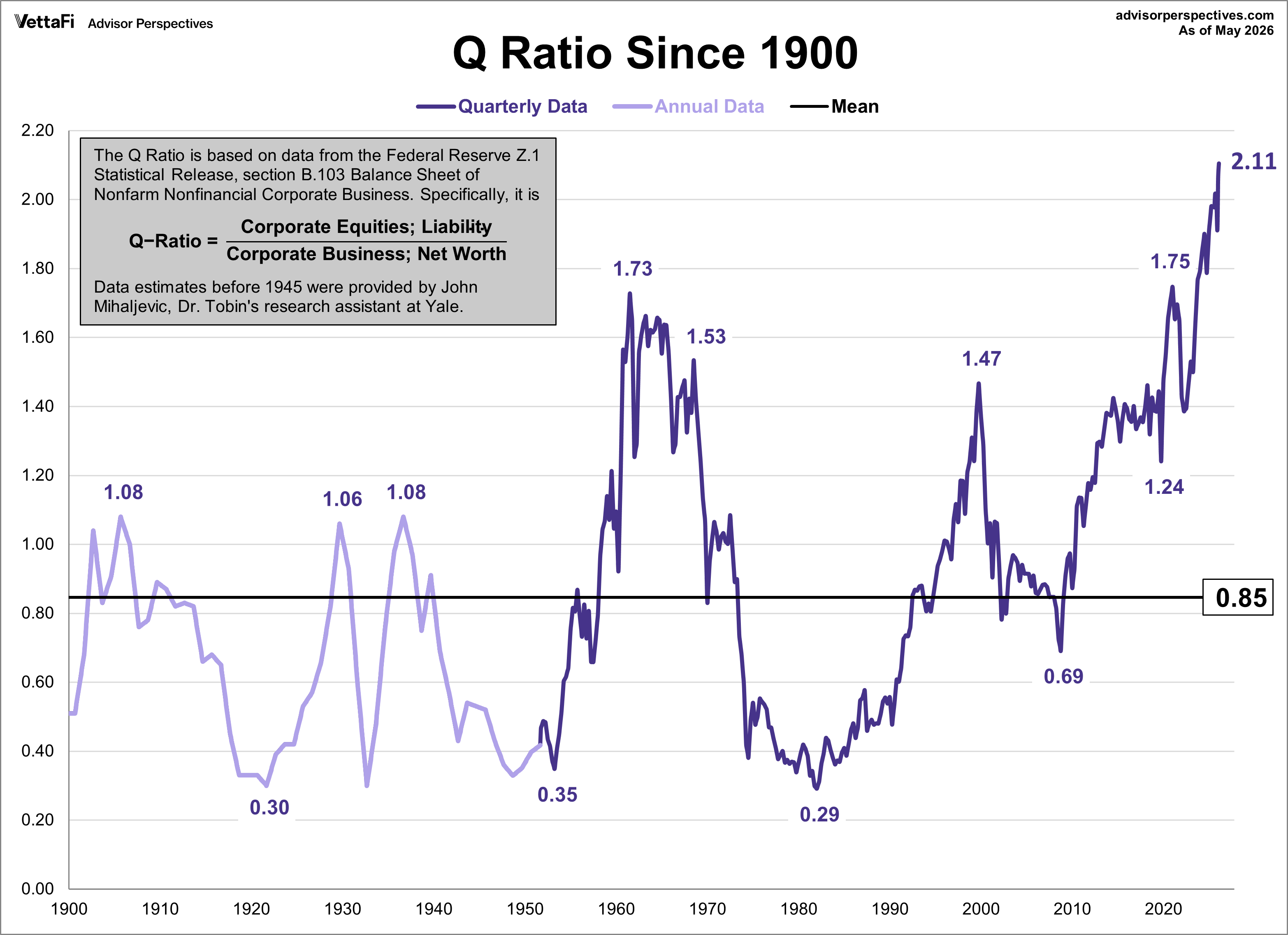

The Q-Ratio is a popular method of estimating the fair value of the stock market developed by Nobel Laureate James Tobin. It's a fairly simple concept, but laborious to calculate. The Q-Ratio is the total price of the market divided by the replacement cost of all its companies. Fortunately, the government does the work of accumulating the data for the calculation. The numbers are supplied in the Federal Reserve Z.1 Financial Accounts of the United States, which is released quarterly.

Note on revisions: The Q-Ratio relies heavily on the Federal Financial Accounts Z.1 data, which is subject to revision. Here's a general note on revisions to the Fed accounts data:

"The data in the Financial Accounts come from a large variety of sources and are subject to limitations and uncertainty due to measurement errors, missing information, and incompatibilities among data sources. The size of this uncertainty cannot be quantified, but its existence is acknowledged by the inclusion of “statistical discrepancies” for various sectors and financial instruments."

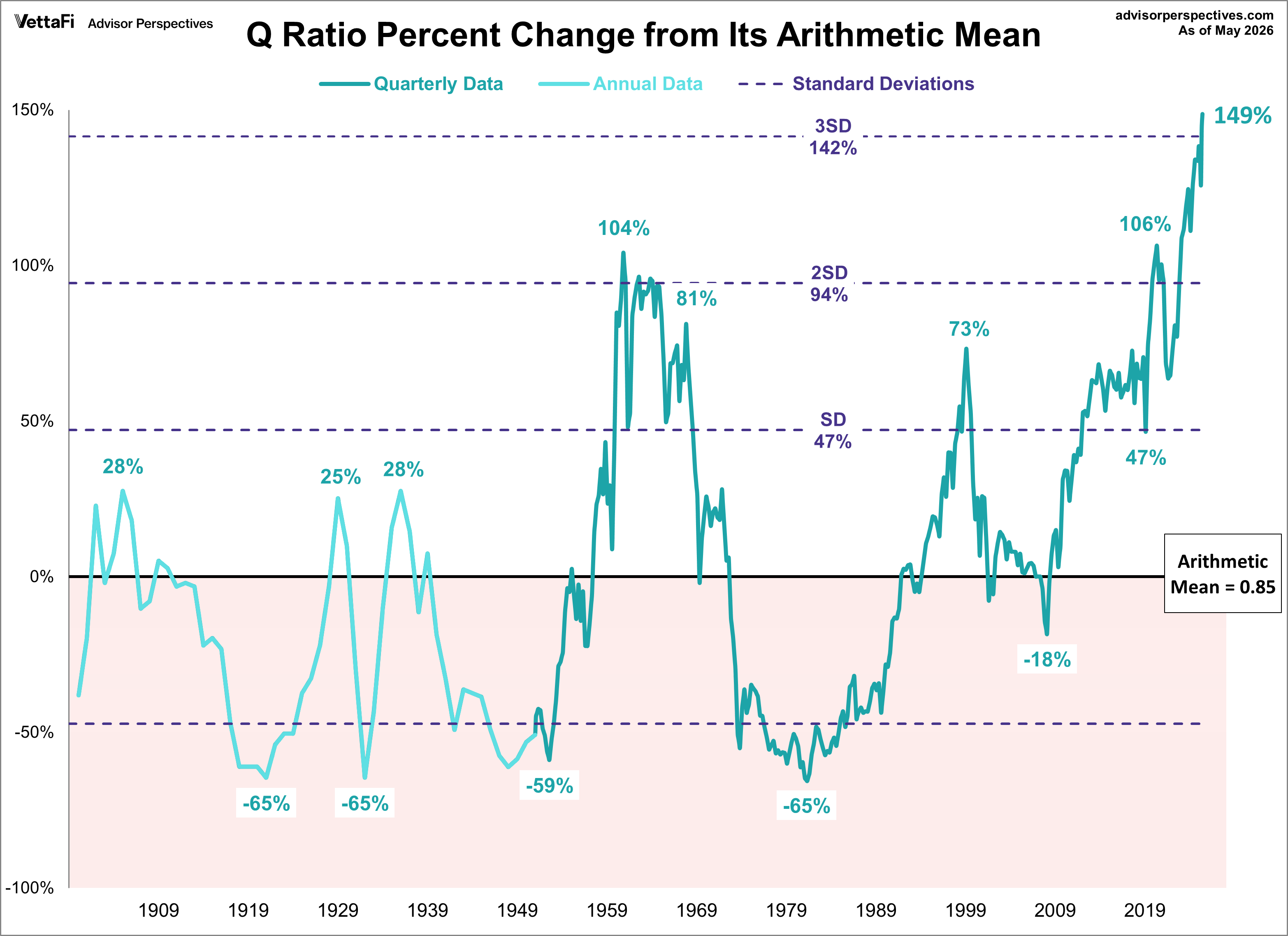

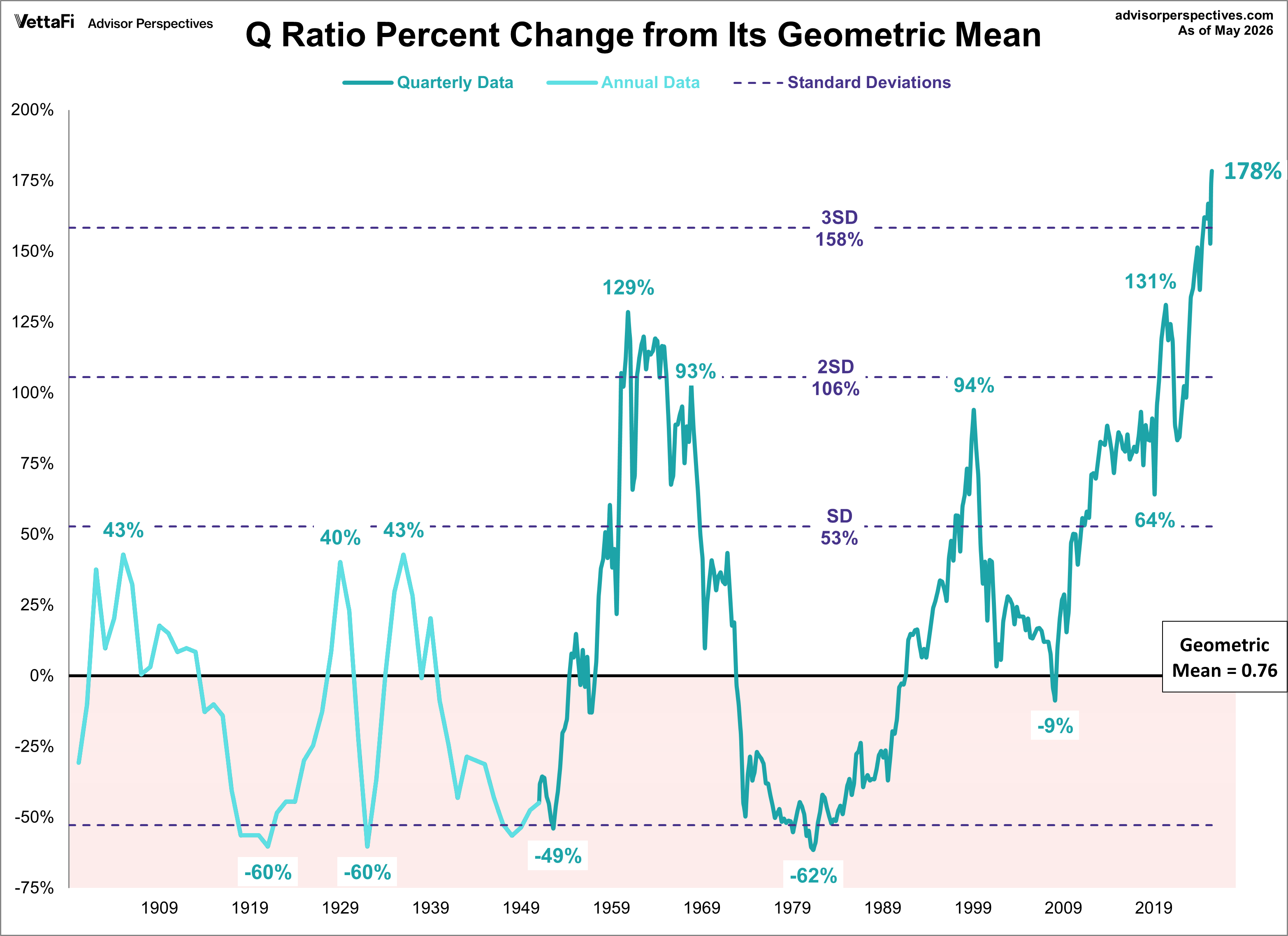

Extrapolating the Q-Ratio

The ratio subsequent to the latest Z.1 Fed data (through 2025 Q4) is based on a subjective process that factors in the monthly closes for the Vanguard Total Market ETF (VTI). As of May 2026, the latest Q-ratio is at 2.11, the highest level in history.

Unfortunately, the Q-Ratio isn't a very timely metric. The Z.1 data is over two months old when it's released, and three additional months will pass before the next release. To address this problem, our monthly updates include an estimate for the more recent months based on changes in the VTI price (Vanguard Total Stock Market ETF) as a surrogate for corporate equities; liability.

The first chart shows the Q-Ratio from 1900 to the present.

Interpreting the Q-ratio

The data since 1945 is a simple calculation using data from the Federal Reserve Z.1 Statistical Release, section B.103, Balance Sheet and Reconciliation Tables for Nonfinancial Corporate Business. Specifically, it is the ratio of market value divided by replacement cost. It might seem logical that fair value would be a 1:1 ratio. But that has not historically been the case. The explanation, according to Smithers & Co. (more about it later) is that "the replacement cost of company assets is overstated. This is because the long-term real return on corporate equity, according to the published data, is only 4.8%, while the long-term real return to investors is around 6.0%. Over the long-term and in equilibrium, the two must be the same."