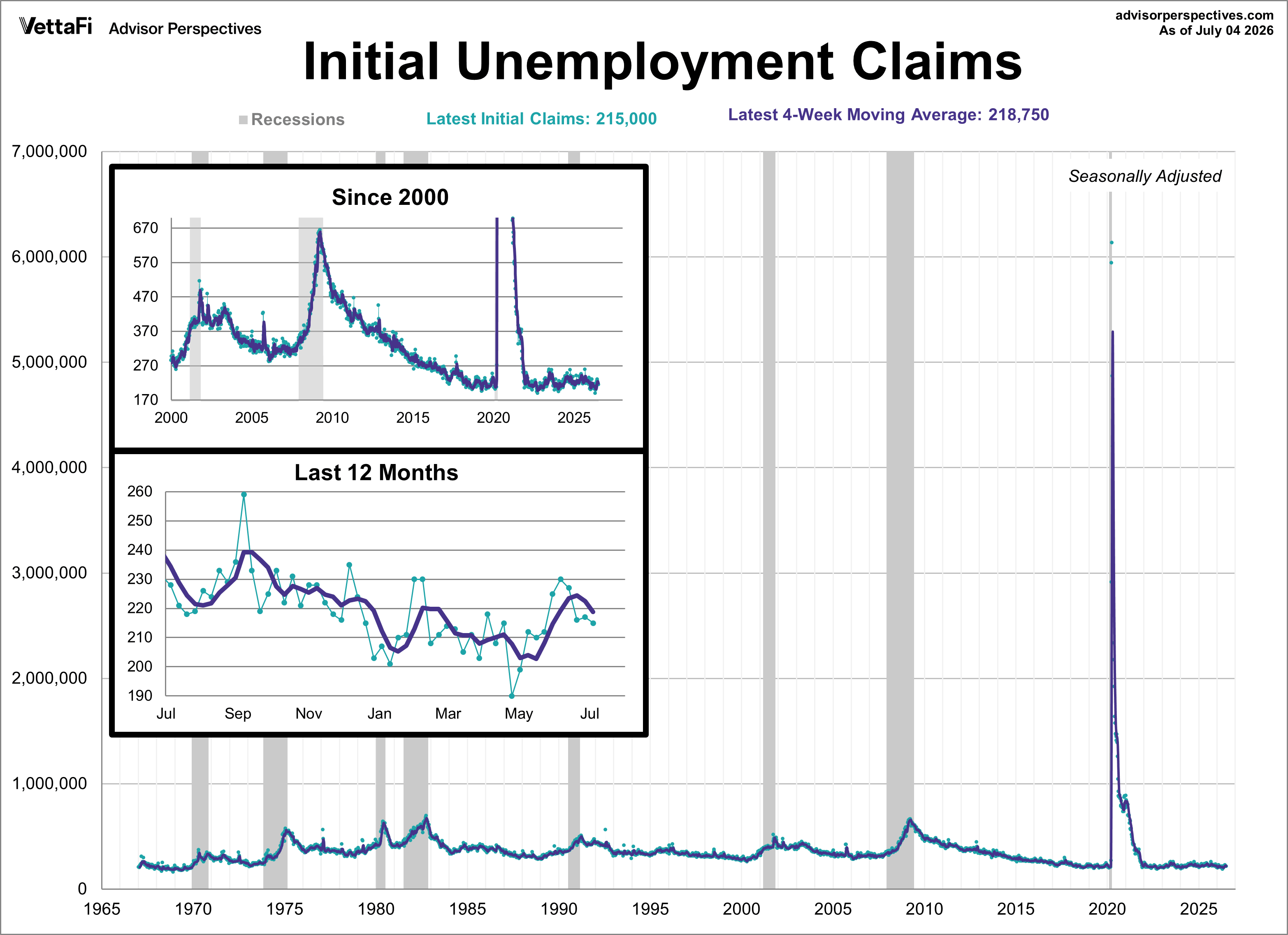

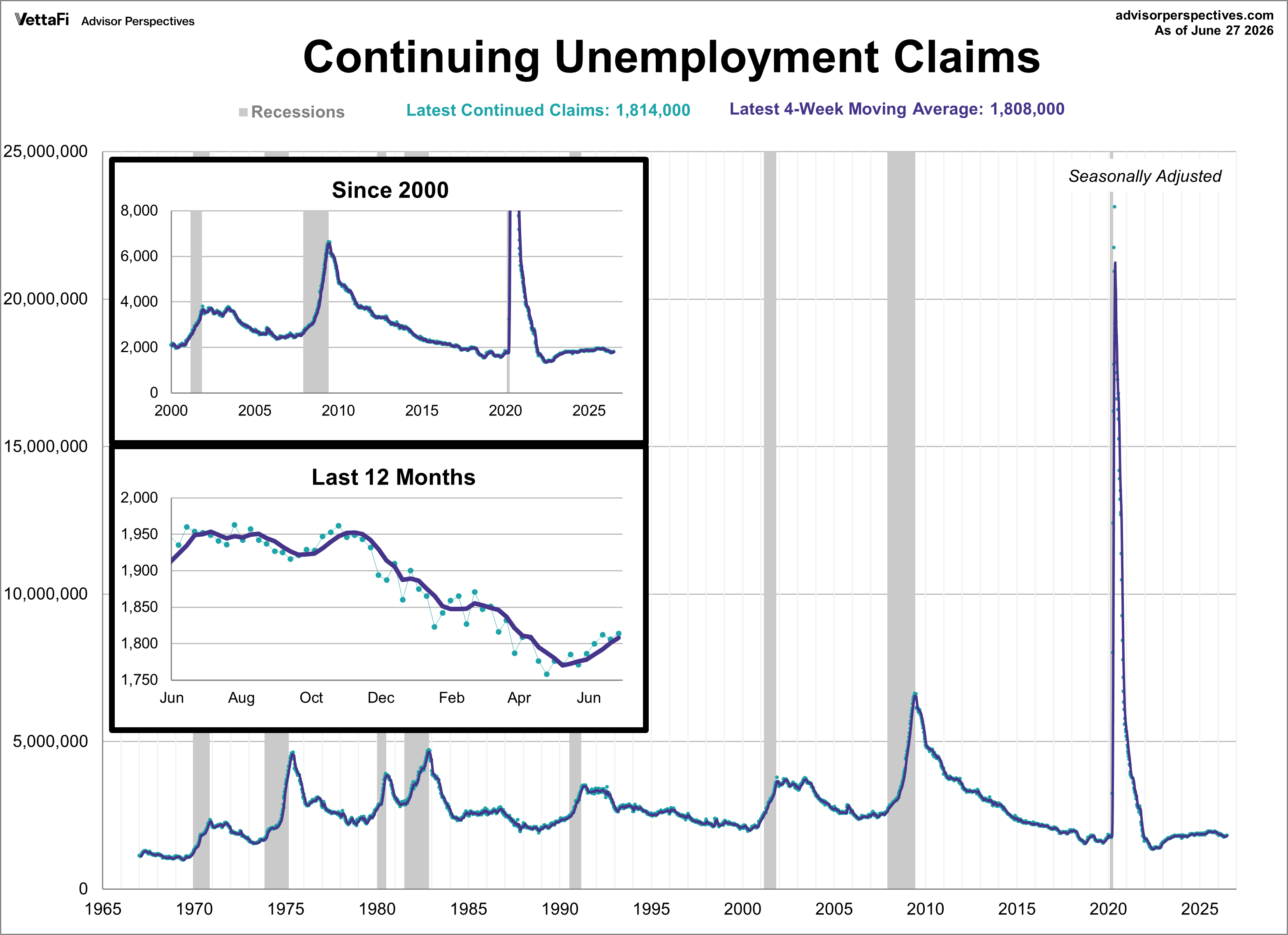

Every week, we provide an update on unemployment claims shortly after the BLS report is made available. While the financial press often reacts to volatile, simplistic weekly estimates, our focus remains on the four-week moving average to identify broader trends.

Key Takeaways

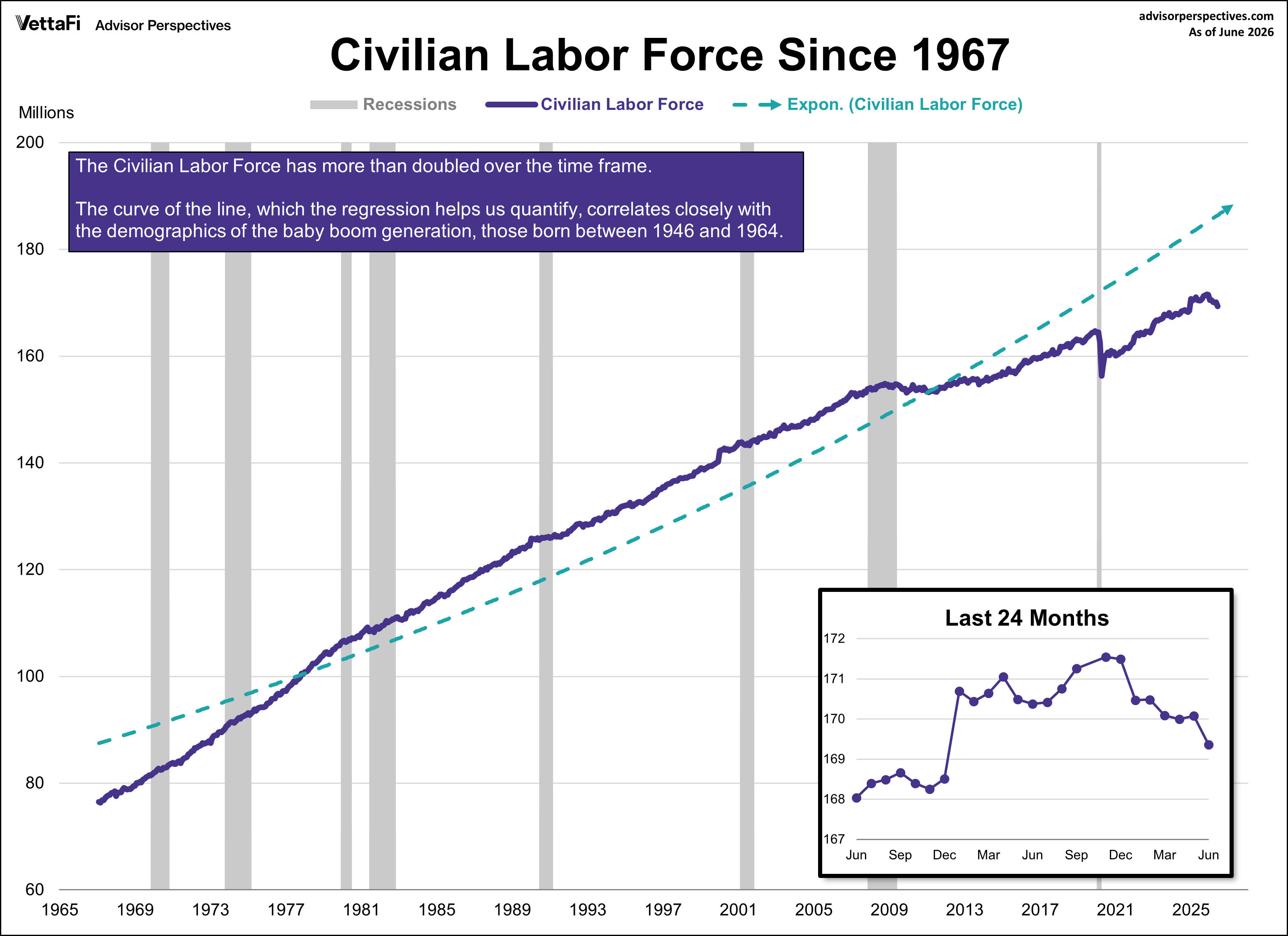

- The Civilian Labor Force has more than doubled from 76.5 million in 1967 to nearly 170 million in 2026.

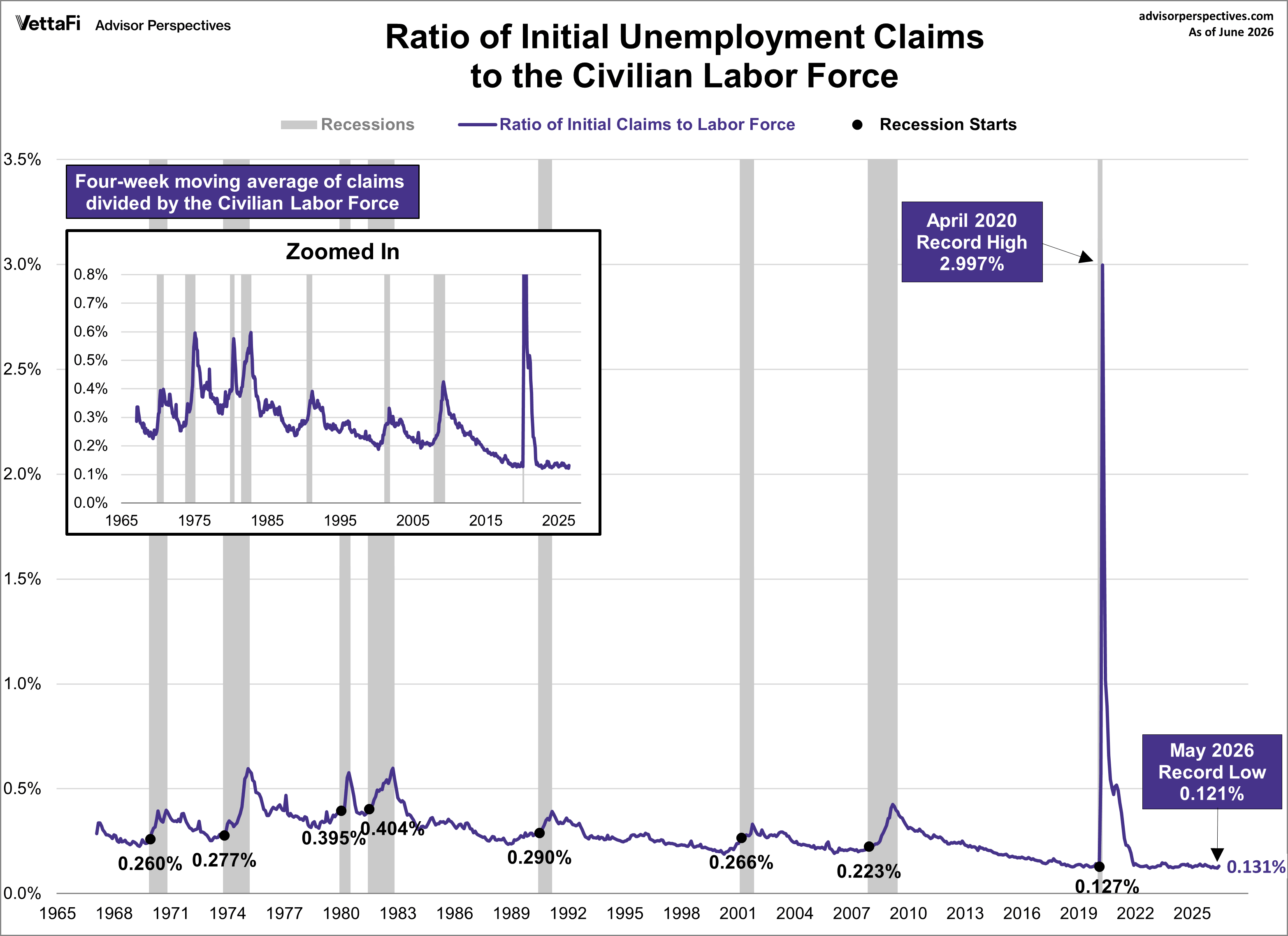

- Initial unemployment claims as a ratio of the Civilian Labor Force was at 0.13% in June.

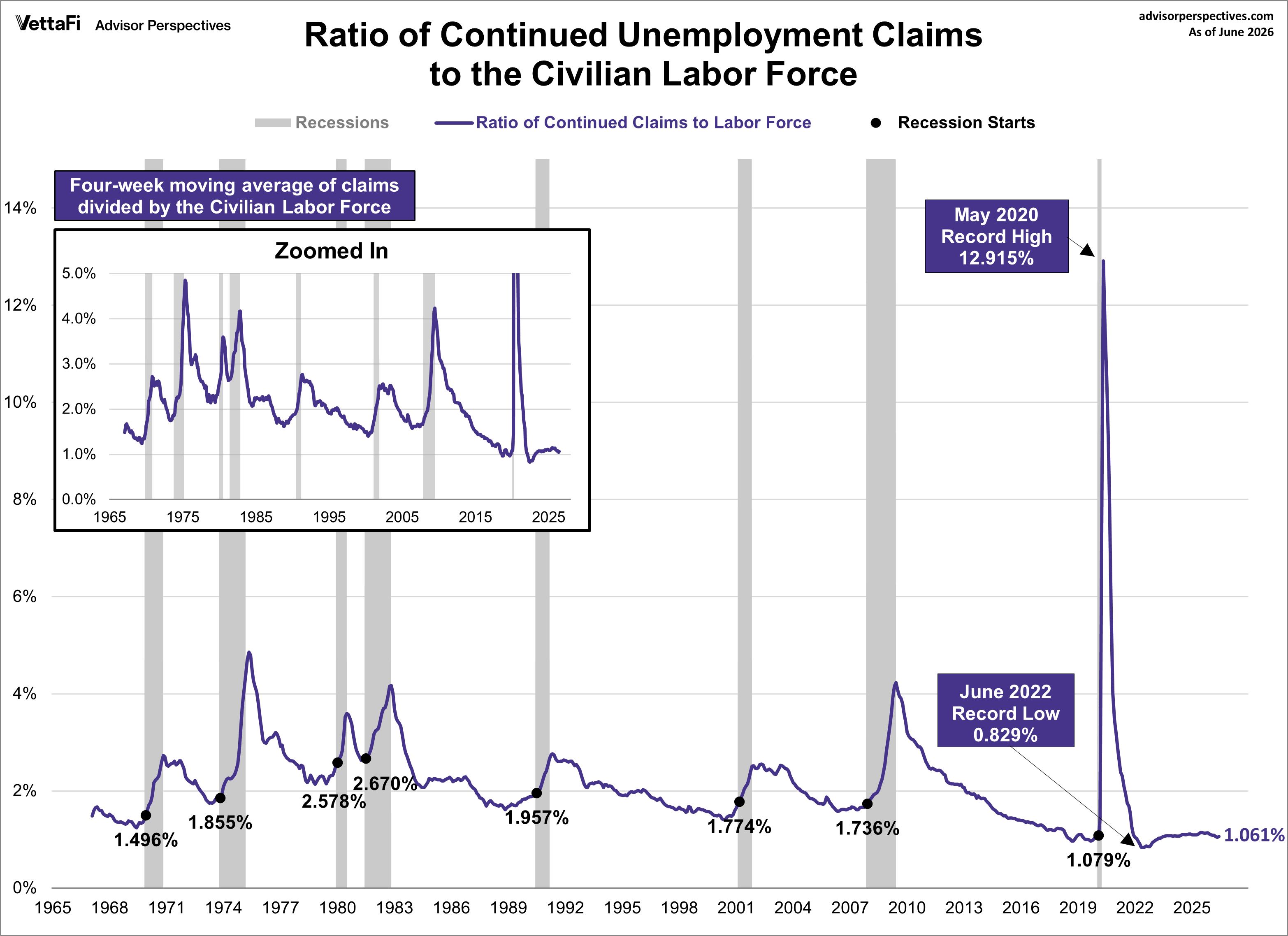

- Continued unemployment claims as a ratio of the Civilian Labor Force was at 1.06% in June.

The Raw Data vs. Reality

Historically, the four-week moving average rises at or before a recession and peaks as it ends. However, viewing raw, seasonally adjusted numbers can be misleading. To understand the true impact, we must account for the massive growth in the Civilian Labor Force (CLF), which has more than doubled from 76.5 million in 1967 to nearly 170 million today.

What is the Civilian Labor Force (CLF)?

The civilian labor force (CLF) is the total number of working age people (16 and over) who are either employed or unemployed. It does not include military personnel, federal government employees, retirees, institutionalized individuals, agricultural workers, handicapped people, or "discouraged" workers. The line's curve largely reflects Baby Boomer employment demographics, those born between 1946 and 1964. A linear regression helps us visually quantify this shift. In 1967 they were starting to turn 21. The oldest are currently eligible for full retirement benefits. Another factor in the curve is the rising participation of women in the labor force.

The Claims-to-CLF Ratio

By viewing claims as a ratio of the labor force, we get a much clearer picture of economic health.

For initial claims, the latest ratio is at 0.131%. This means only about 13 out of every 10,000 workers are filing for initial benefits. The latest ratio is well below its all-time high of 2.997% set in April 2020 and is just above the record low of 0.121% set in May 2026.

For continued claims, the latest ratio is at 1.061%. This means roughly 11 per 1,000 workers are receiving ongoing benefits. The latest ratio is well below its all-time high of 12.915% (May 2020) and is above its all-time low of 0.829% (June 2022).

Unemployment Claims as a Recession Indicator

What does the ratio of unemployment claims to the civilian labor force tell us about where we are in the business cycle and recession risk?

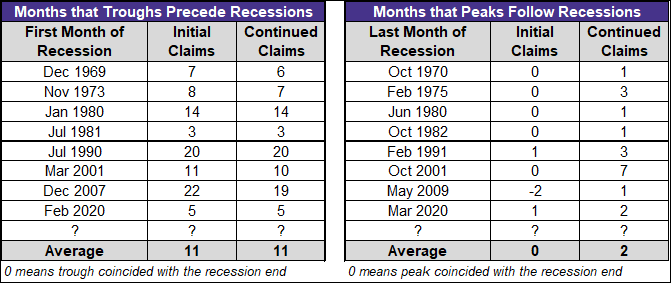

A particularly interesting feature of this unemployment claims ratio series is its effectiveness in the past as a leading indicator for recession starts and a virtually dead-on coincident indicator for recession ends. In both of the ratio charts above, we've highlighted the value at the month a recession starts. In every instance, the trough in claims preceded the recession start by a few too many months, but the claims peaks were nearly identical with recession ends. Here is a table showing the actual numbers.

The Bottom Line

Technically, we are now 1 and 48 months past our respective troughs because initial claims just set a new historical low. However, this doesn't alter the broader macro picture: it took 43 months to finally break the previous initial claims trough of 0.122% set back in October 2022.

In historical context, whether looking at that massive 43-month stretch or the ongoing 48-month window for continued claims, these are staggering durations that far exceed the previous maximum lead times for a recession.

Related Employment Updates:

Monthly Employment Report

Job Openings and Labor Turnover Summary (JOLTS)

ADP Employment Report

Weekly Unemployment Claims

Full-Time and Part-Time Employment

Multiple Jobholders

Five Decades of Middle Class Wages

Read more updates by Jen Nash