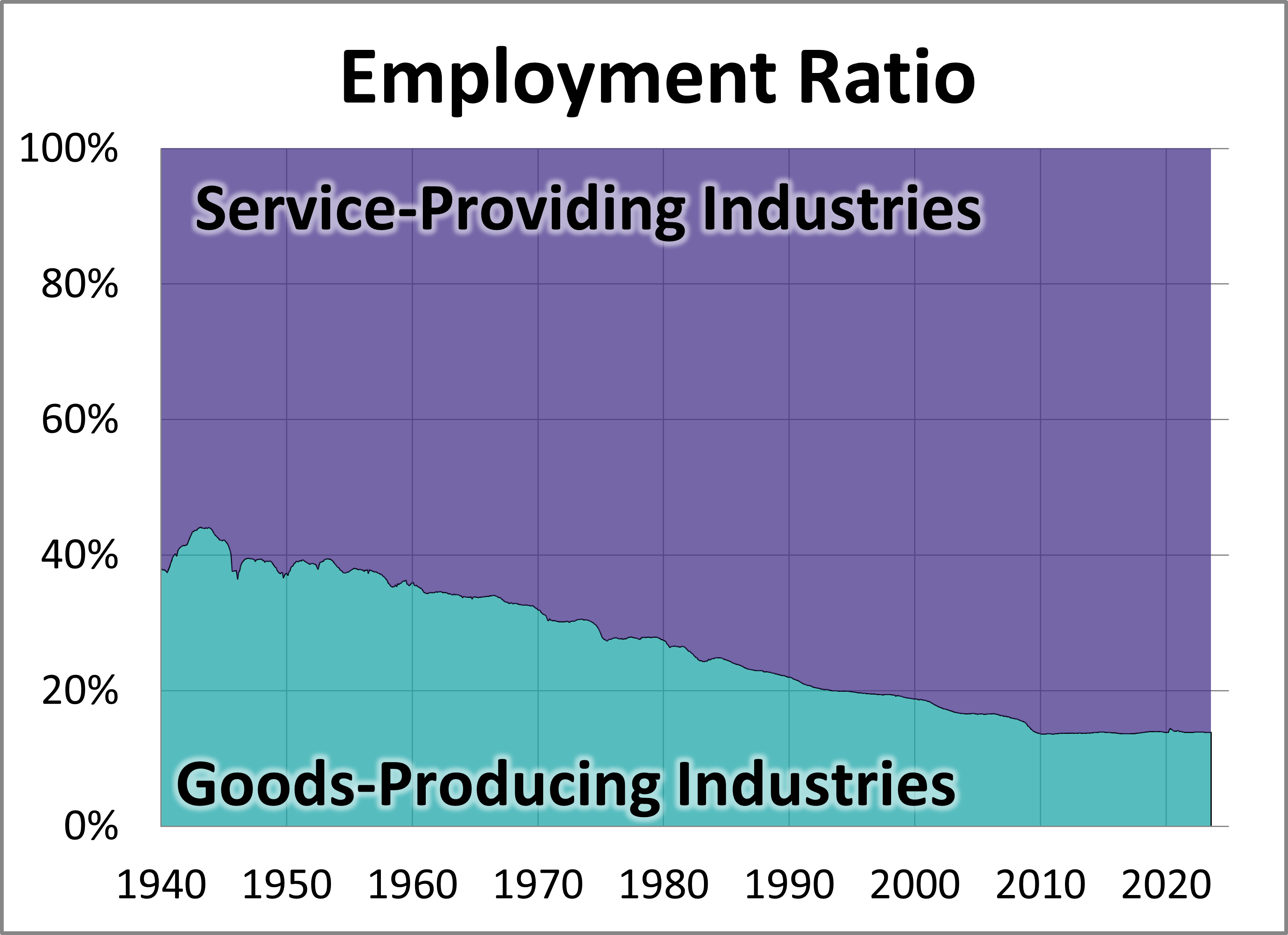

The Department of Labor has monthly data on employment by industry categories reaching back to 1939. At the highest level, all jobs are categorized in either service-providing industries or goods producing industries. The adjacent chart illustrates the ratio of the two since 1939.

The Department of Labor has monthly data on employment by industry categories reaching back to 1939. At the highest level, all jobs are categorized in either service-providing industries or goods producing industries. The adjacent chart illustrates the ratio of the two since 1939.

The latest monthly employment report showed 187,000 nonfarm jobs were added in August. An industry breakdown of that number shows a gain of 151,000 service-providing jobs and a gain of 36,000 goods-producing jobs.

In 1939, service-providing industries employed more people than goods-producing, 62.9% to 37.1%, a ratio of 1.7-to-1. World War II triggered a surge in goods-producing employment and an accompanying reduction in services. But following the war, we've seen a steady tilt toward services. The ratio is now 6.2 services jobs for every goods-producing job. The key drivers of this secular trend have been the growth of automation that reduces the need for human labor and the globalization of goods production.

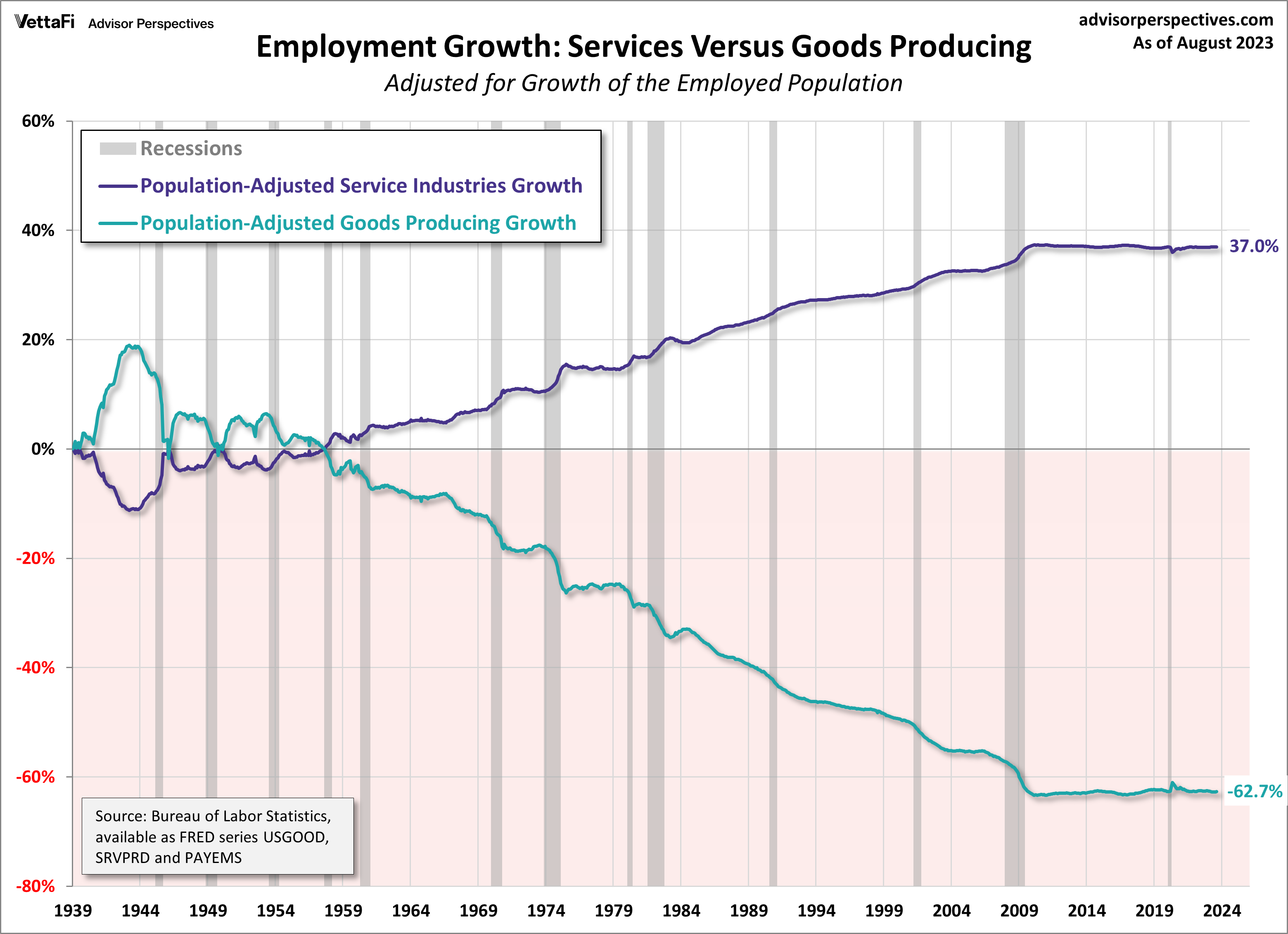

The next chart provides a more detailed view of these two employment cohorts. I've adjusted for the 423% growth in the employed population since 1939. A conspicuous feature of this snapshot is the sharp trend reversal in the early 1940s reflecting the impact of World War II on the demand for goods. Another notable detail is the stable ratio since the great recession in 2009. We saw shorter periods of a sustained ratio during the stagflation of the 1970s and for about three years starting at the end of 2003. The current ratio of services to goods-producing has been essentially unchanged for the last decade. It is currently at 6.2 - which means there are 6.2 times as many service-providing jobs as there are goods-providing jobs.

Another notable insight is the consistent impact of recessions on the relative growth of the two cohorts: Even though the unemployment rate increased during recessions, the employed service-providing population increased, and goods-producing jobs disappeared. We also see that post-recession recoveries didn't reverse this pattern.

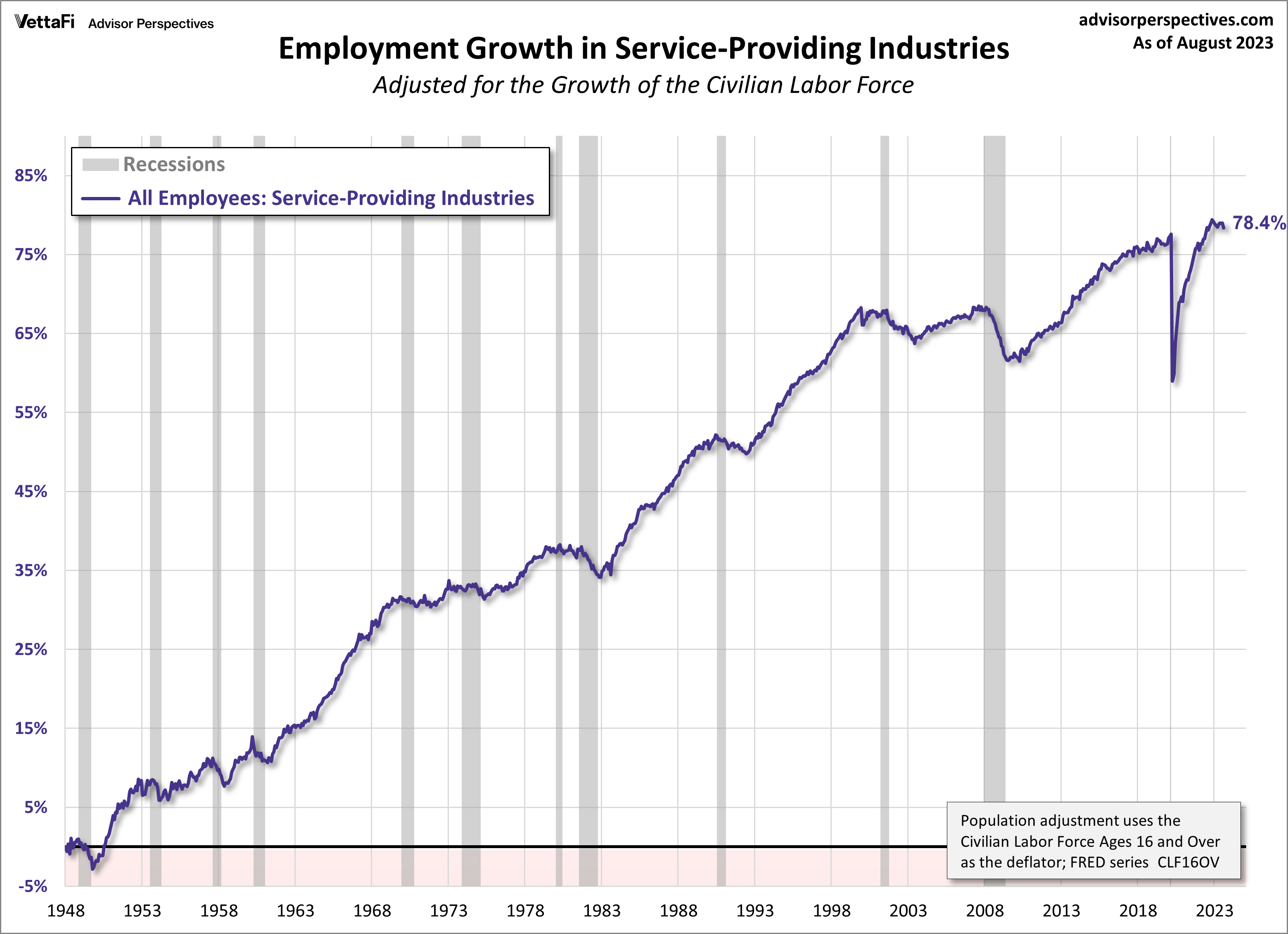

The chart above is adjusted for population inflation based on growth of the employed population. The next chart focuses on the services providing employed adjusted with a broader population base, the civilian labor force age 16 and over, which includes both the employed and those seeking employment.

As a result of the COVID-19 pandemic, the number of employees in service-providing industries plummeted but has recovered significantly.

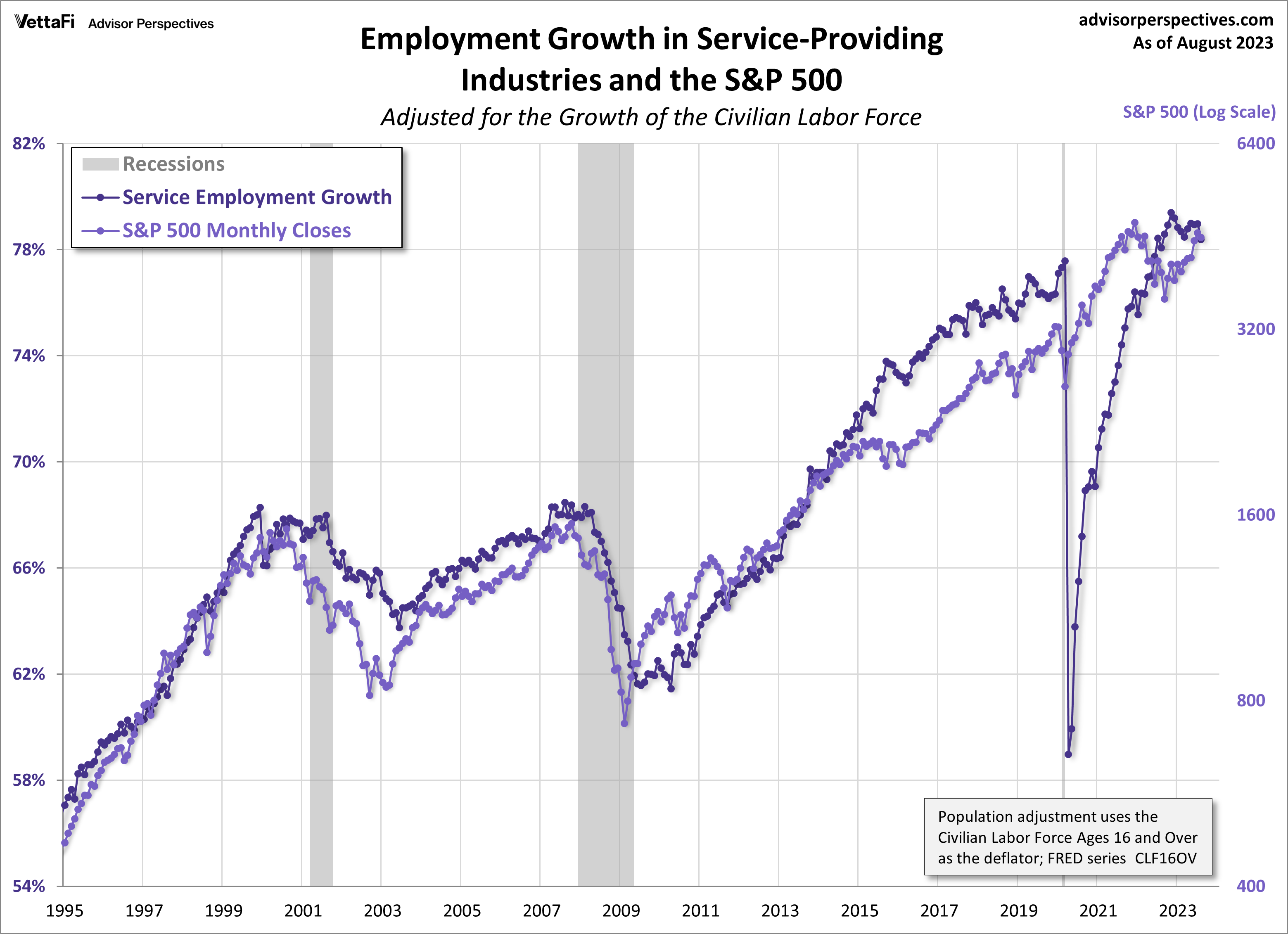

A striking feature of this chart is its uncanny resemblance to the S&P Composite (the S&P 500 spliced with its predecessor, the S&P 90). How close is the correlation with the S&P 500? Here is an overlay of the services-providing employed population (left axis) and the S&P 500 (log-scale right axis) since 1995.

The index reached a peak in March 2000, although the monthly close peak was five months later in August 2000. Service employment didn't sharply decline until September of the following year. The index peaked again in October 2007 for both its daily and monthly close highs. Service employment began its nosedive eight months later in June of 2008. The index reached its all-time high on January 3, 2022, even though the monthly all time high was set a month prior in December 2021. Service employment reached its all-time high, eleven months later in November 2022.

This article was originally written by Doug Short. From 2016-2022, it was improved upon and updated by Jill Mislinski. Starting in January 2023, AP Charts pages will be maintained by Jennifer Nash at VettaFi | Advisor Perspectives

Here's our list of monthly employment updates:

Ratio of Part-Time and Full-Time Employment

Workforce Recovery Since Recession

Civilian Labor Force, Unemployment Claims, and the Business Cycle