The Q-Ratio is a popular method of estimating the fair value of the stock market developed by Nobel Laureate James Tobin. It's a fairly simple concept, but laborious to calculate. The Q-Ratio is the total price of the market divided by the replacement cost of all its companies. Fortunately, the government does the work of accumulating the data for the calculation. The numbers are supplied in the Federal Reserve Z.1 Financial Accounts of the United States, which is released quarterly.

Note on revisions: The Q-Ratio relies heavily on the Federal Financial Accounts Z.1 data, which is subject to revision. Here's a general note on revisions to the Fed accounts data:

"The data in the Financial Accounts come from a large variety of sources and are subject to limitations and uncertainty due to measurement errors, missing information, and incompatibilities among data sources. The size of this uncertainty cannot be quantified, but its existence is acknowledged by the inclusion of “statistical discrepancies” for various sectors and financial instruments."

Extrapolating the Q-Ratio

The ratio subsequent to the latest Z.1 Fed data (through 2026 Q1) is based on a subjective process that factors in the monthly closes for the Vanguard Total Market ETF (VTI). As of July 2026, the latest Q-ratio is at 1.83.

Unfortunately, the Q-Ratio isn't a very timely metric. The Z.1 data is over two months old when it's released, and three additional months will pass before the next release. To address this problem, our monthly updates include an estimate for the more recent months based on changes in the VTI price (Vanguard Total Stock Market ETF) as a surrogate for corporate equities; liability.

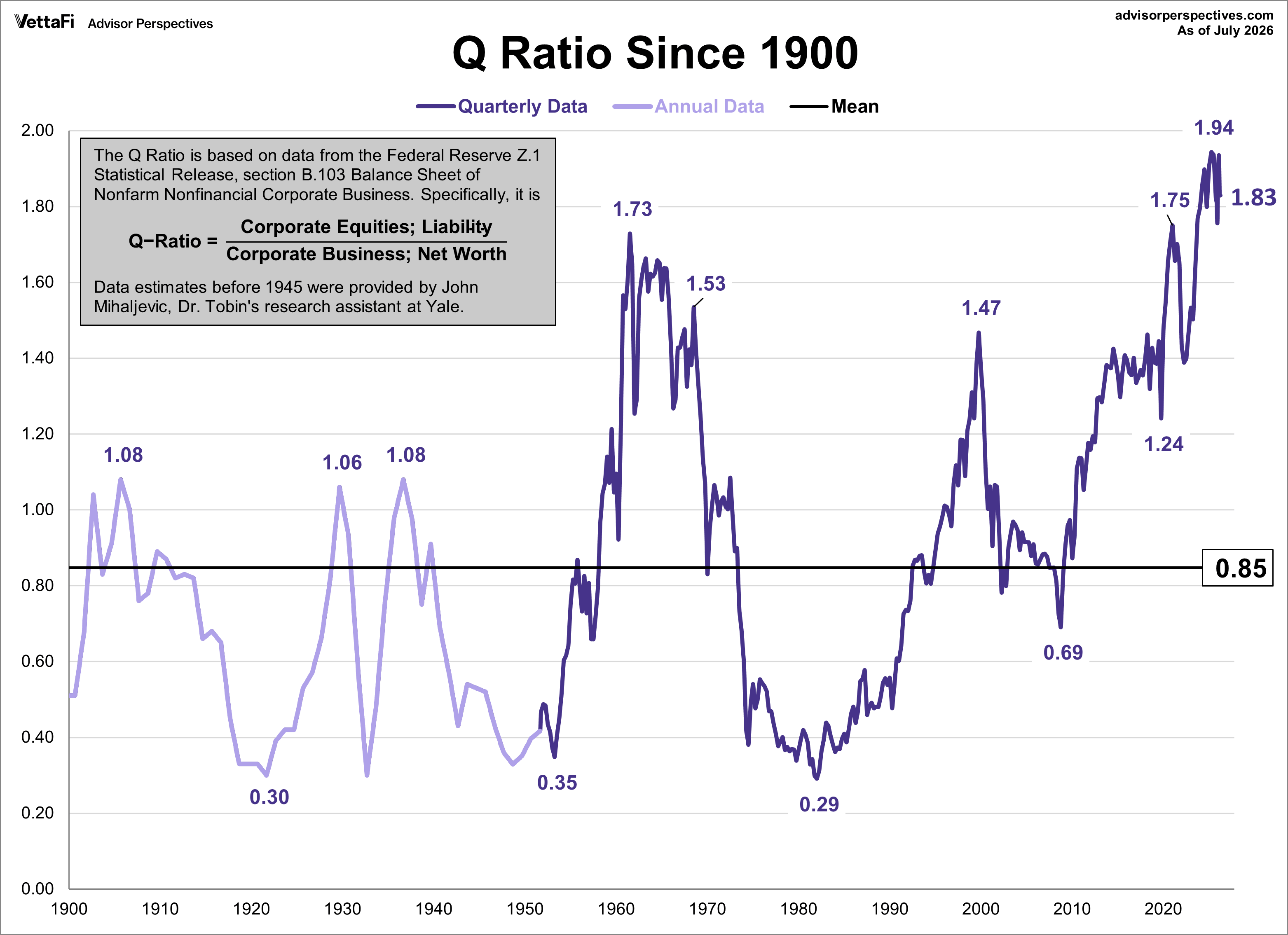

The first chart shows the Q-Ratio from 1900 to the present.

Interpreting the Q-ratio

The data since 1945 is a simple calculation using data from the Federal Reserve Z.1 Statistical Release, section B.103, Balance Sheet and Reconciliation Tables for Nonfinancial Corporate Business. Specifically, it is the ratio of market value divided by replacement cost. It might seem logical that fair value would be a 1:1 ratio. But that has not historically been the case. The explanation, according to Smithers & Co. (more about it later) is that "the replacement cost of company assets is overstated. This is because the long-term real return on corporate equity, according to the published data, is only 4.8%, while the long-term real return to investors is around 6.0%. Over the long-term and in equilibrium, the two must be the same."

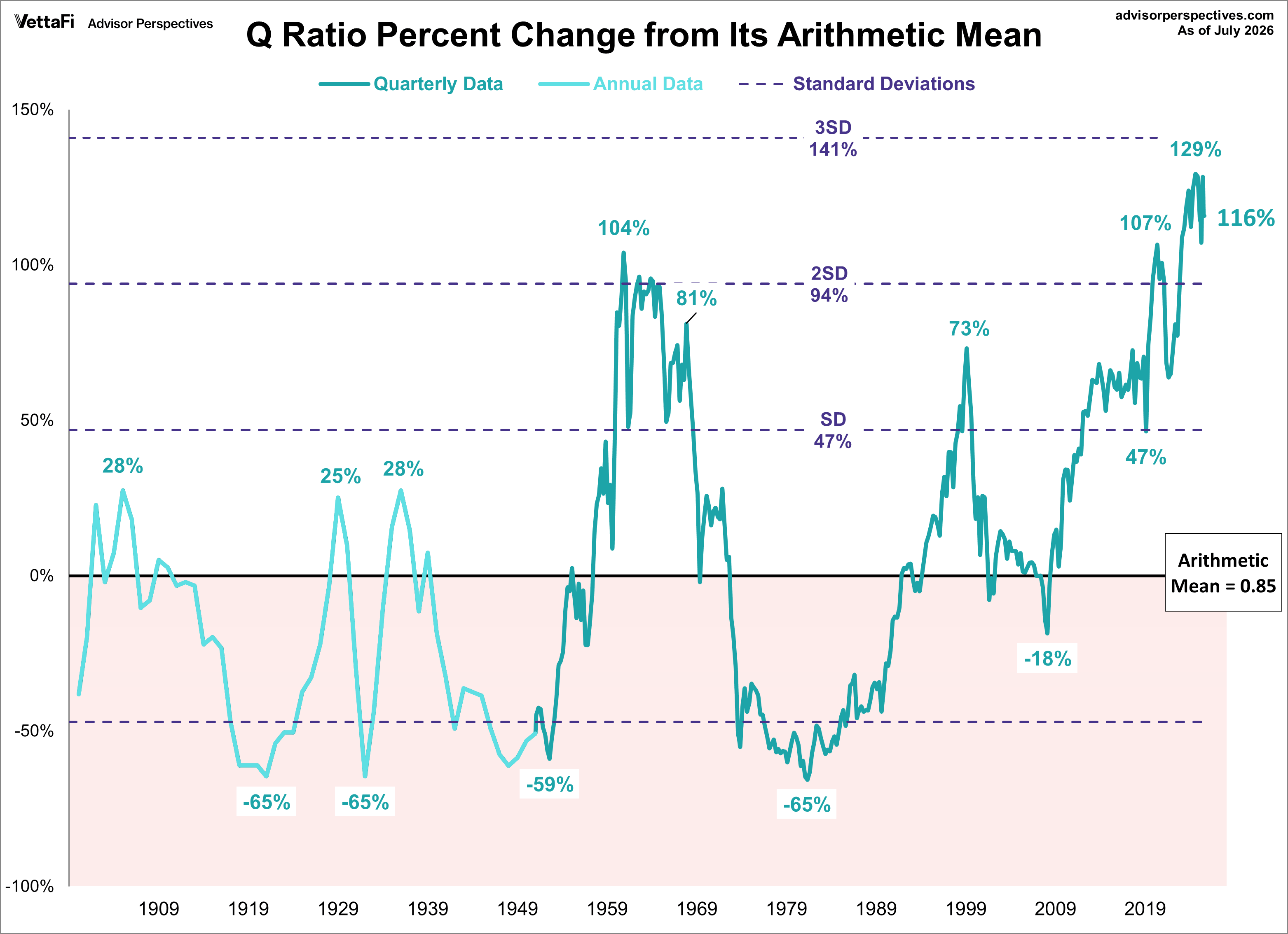

The Q-Ratio and Its Arithmetic Mean

The average (arithmetic mean) Q-Ratio is about 0.85. The chart below shows the Q-Ratio relative to its arithmetic mean of 1 (i.e., divided the ratio data points by the average). This gives a more intuitive sense to the numbers. For example, the Q-Ratio reached its all-time high of 1.94 in July 2025, which is approximately 130% above replacement cost. Meanwhile, the Q-Ratio hit an all-time low in 1982 was 0.29, which is approximately 65% below replacement cost. That's quite a range. As of July 2026, the Q-Ratio is 116% above its historic average.

Remember, the latest data point is extrapolated using the monthly VTI close and the most recent Q Ratio (which is 1.82 as of Q1 2026).

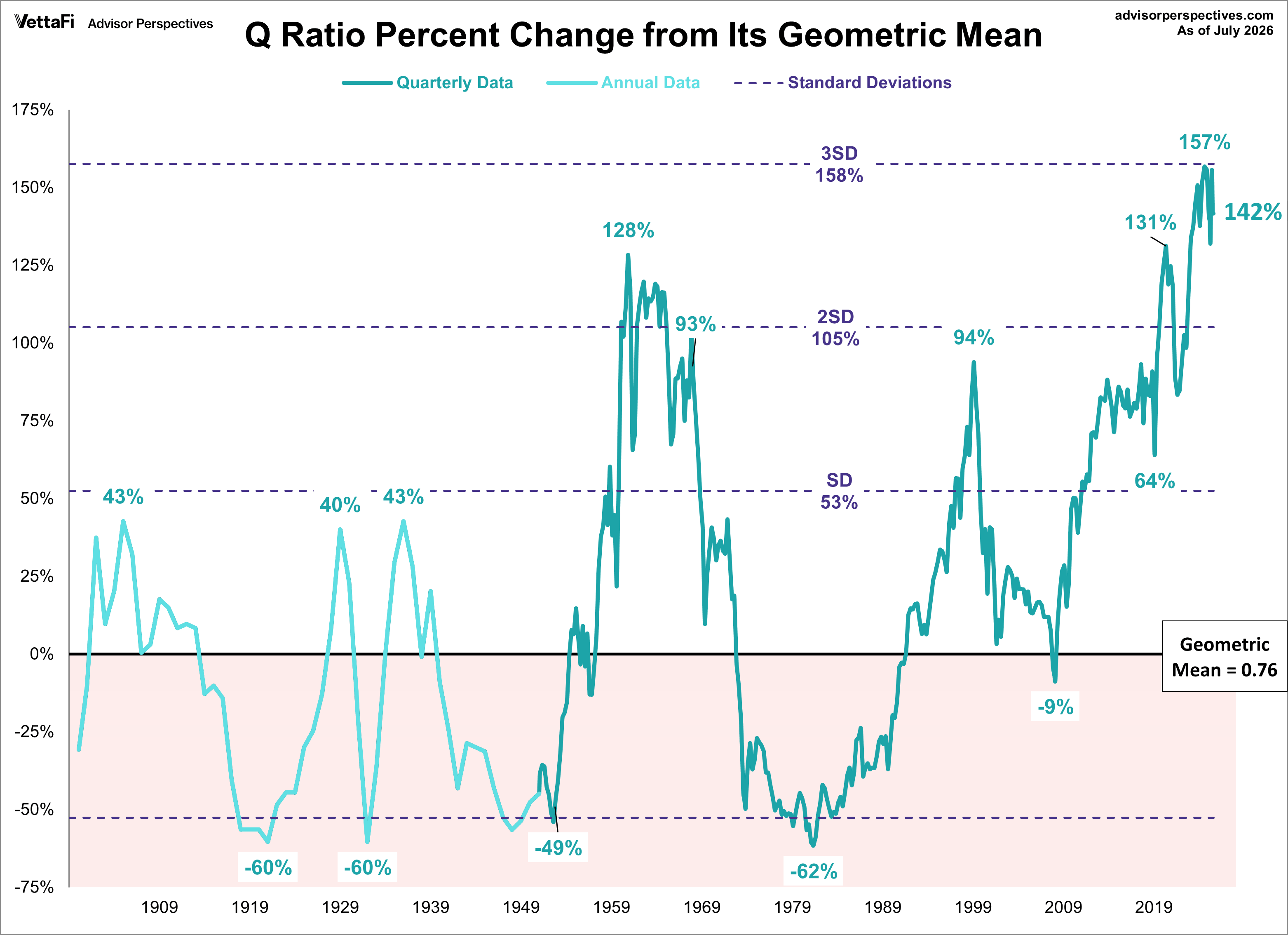

The Q-Ratio and Its Geometric Mean

Smithers & Co., an investment firm in London, incorporates the Q-Ratio in its analysis. In fact, CEO Andrew Smithers and economist Stephen Wright of the University of London co-authored a book on the Q-Ratio, Valuing Wall Street. They prefer the geometric mean for standardizing the ratio, which has the effect of weighting the numbers toward the mean. Adjusting to the geometric mean, the all-time high and low mentioned above are adjusted to 157% above and 62% below the historic average, respectively. As of July 2026, the Q-Ratio is 142% above its historic geometric average.

The Message of the Q-Ratio: Overvaluation

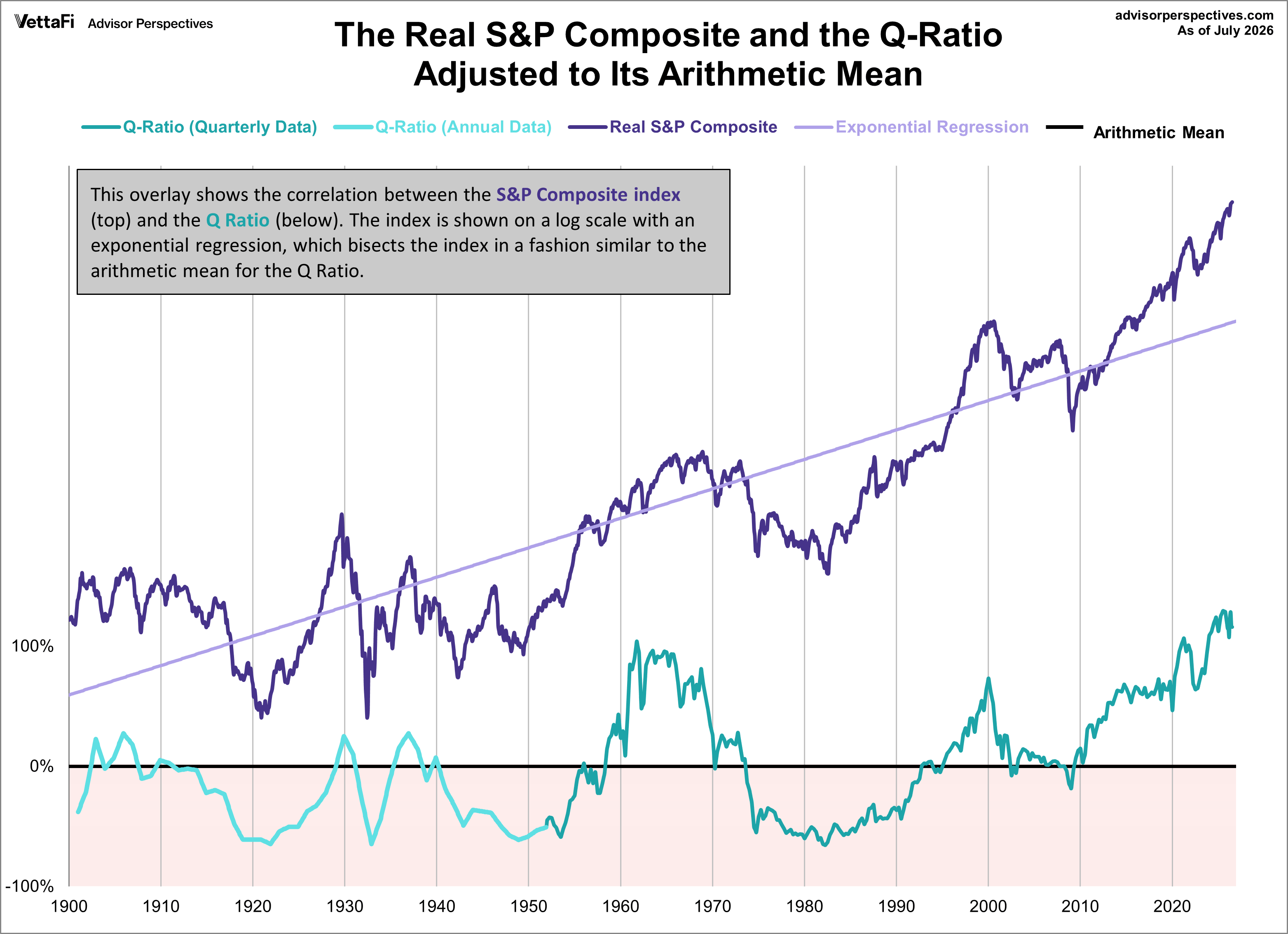

Of course, periods of over-and under-valuation can last for many years at a time, so the Q-Ratio is not a useful indicator for short-term investment timelines. This metric is more appropriate for formulating expectations for long-term market performance. As we can see in the next chart, peaks in the Q-Ratio are correlated with secular market tops - the tech bubble peak and current market values being extreme outliers.

Q-Ratio Calculation Components

As a reminder, the Q-Ratio is the total price of the market divided by the replacement cost of all its companies. For a quick look at the two components that make up this calculation, here is an overlay of the two since the inception of quarterly Z.1 updates in 1952.

There is an obvious similarity between the Fed's estimate of "Corporate Equities; Liabilities" and a broad market index, such as the S&P 500 or VTI. It is the more volatile of the two, but this component can be easily extrapolated for the months following the latest Fed data. The less volatile underlying net worth is not readily estimated from coincident indicators.

ETFs associated with the S&P 500 include: iShares Core S&P 500 ETF (IVV), SPDR S&P 500 ETF Trust (SPY), Vanguard S&P 500 ETF (VOO), and SPDR Portfolio S&P 500 ETF (SPYM).

Read more updates by Jen Nash