Official recession calls are the responsibility of the NBER Business Cycle Dating Committee, which is understandably vague about the specific indicators on which it bases its decisions. This committee statement is about as close as they get to identifying their method.

There is, however, a general belief that there are four big recession indicators that the committee weighs heavily in their cycle identification process. They are:

- Nonfarm employment

- Industrial Production

- Real Retail Sales

- Real Personal Income (excluding Transfer Receipts)

Key Takeaways

-

June nonfarm employment increased by 57,000 jobs, down from May's 129,000 gain and missing the 114,000 forecast.

-

The June unemployment rate dropped to 4.2%, reaching its lowest level in nearly one year.

-

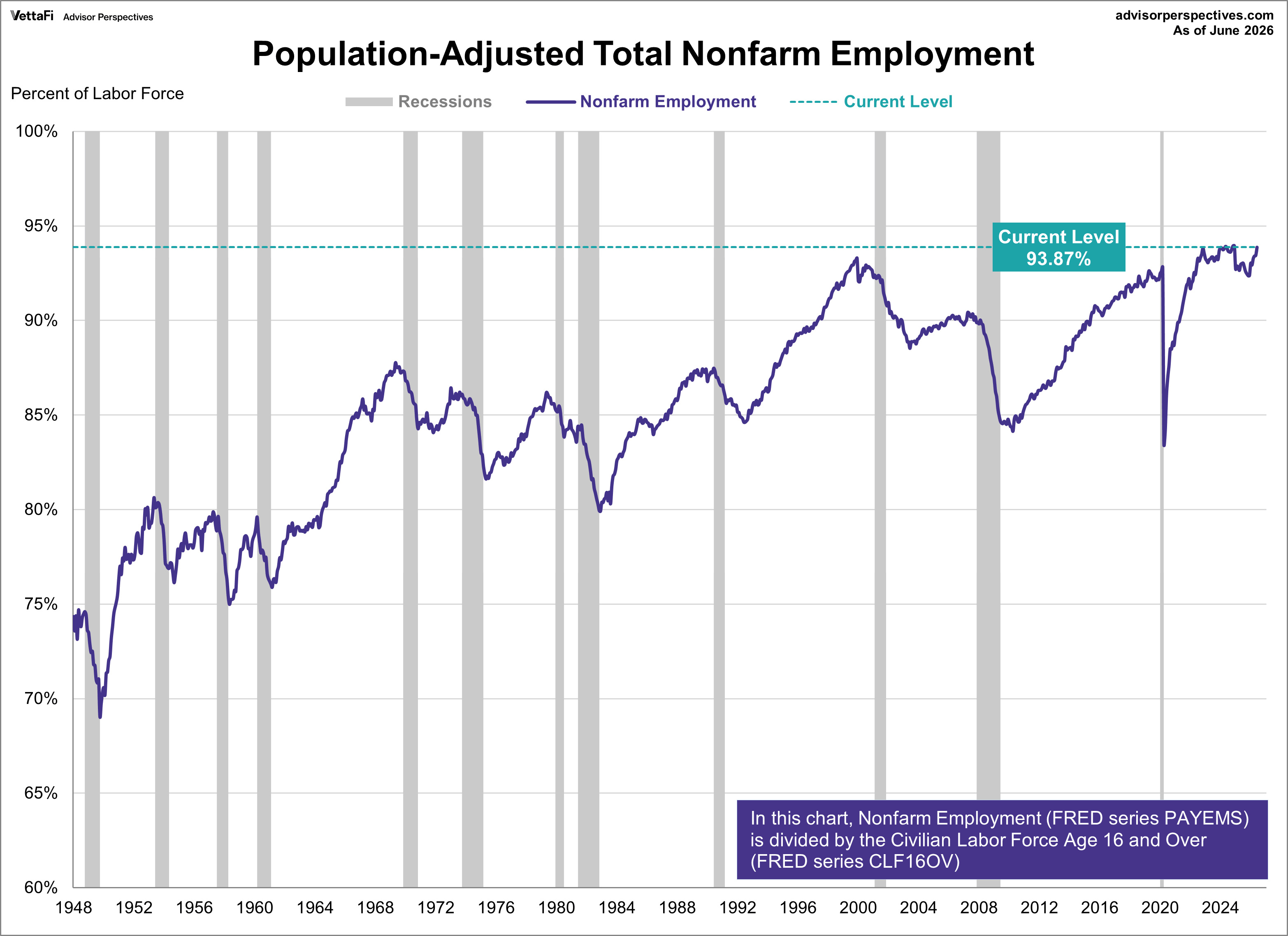

Population-adjusted nonfarm employment, measured by civilian labor force age 16 and over, currently sits at 93.87%.

The Latest Indicator Data: Nonfarm Employment

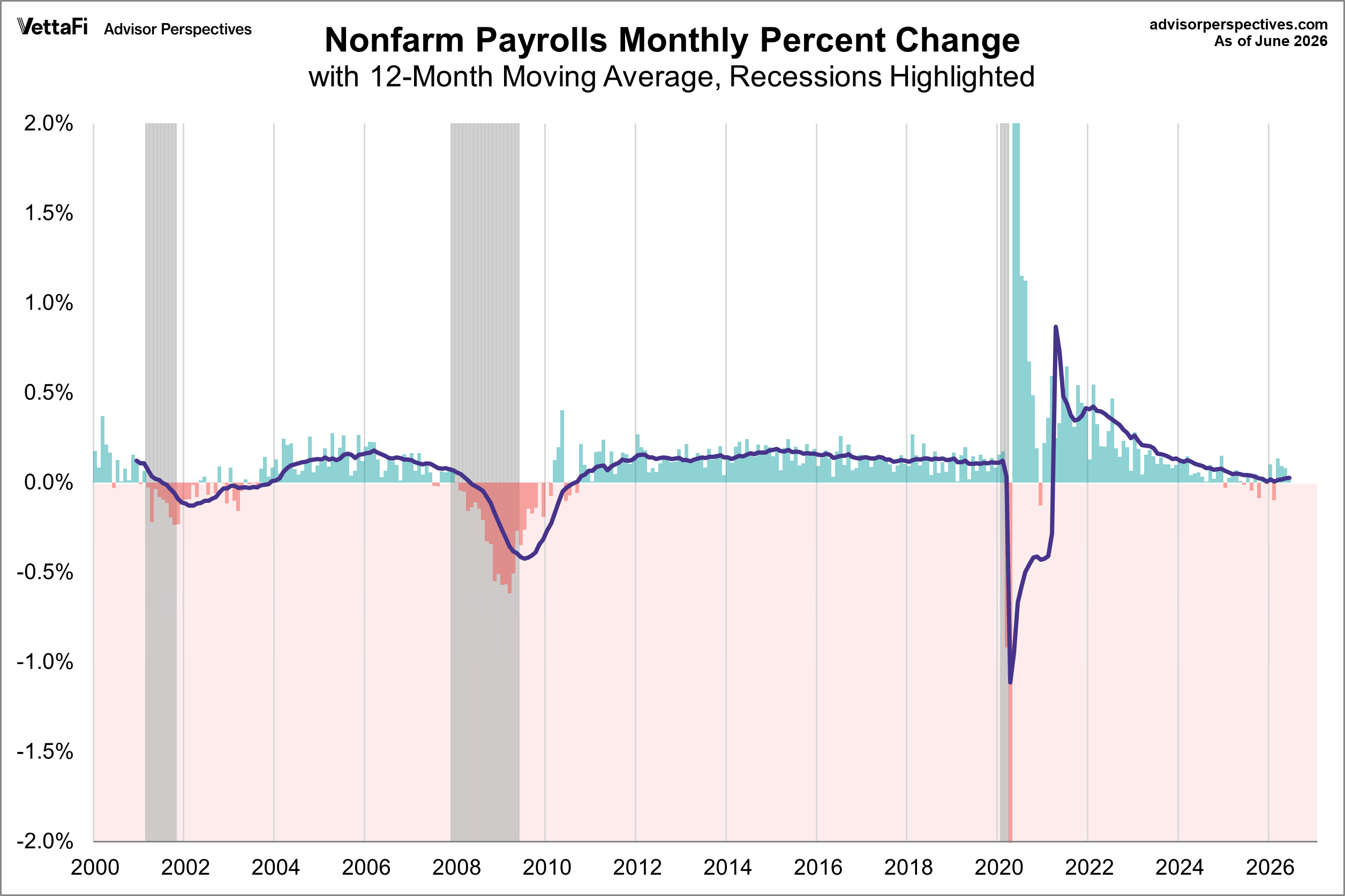

The latest employment report showed that 57,000 jobs were added in June, down from May's 129,000 gain. This figure was significantly lower than the projected addition of 114,000 jobs. Meanwhile, the unemployment rate unexpectedly ticked down to 4.2%, its lowest level in almost a year.

The chart below shows the monthly percent change in this indicator since the turn of the century, a period that includes three recessions. We've included a 12-month moving average to help visualize the trend.

Nonfarm Employees: Visualizing the Data

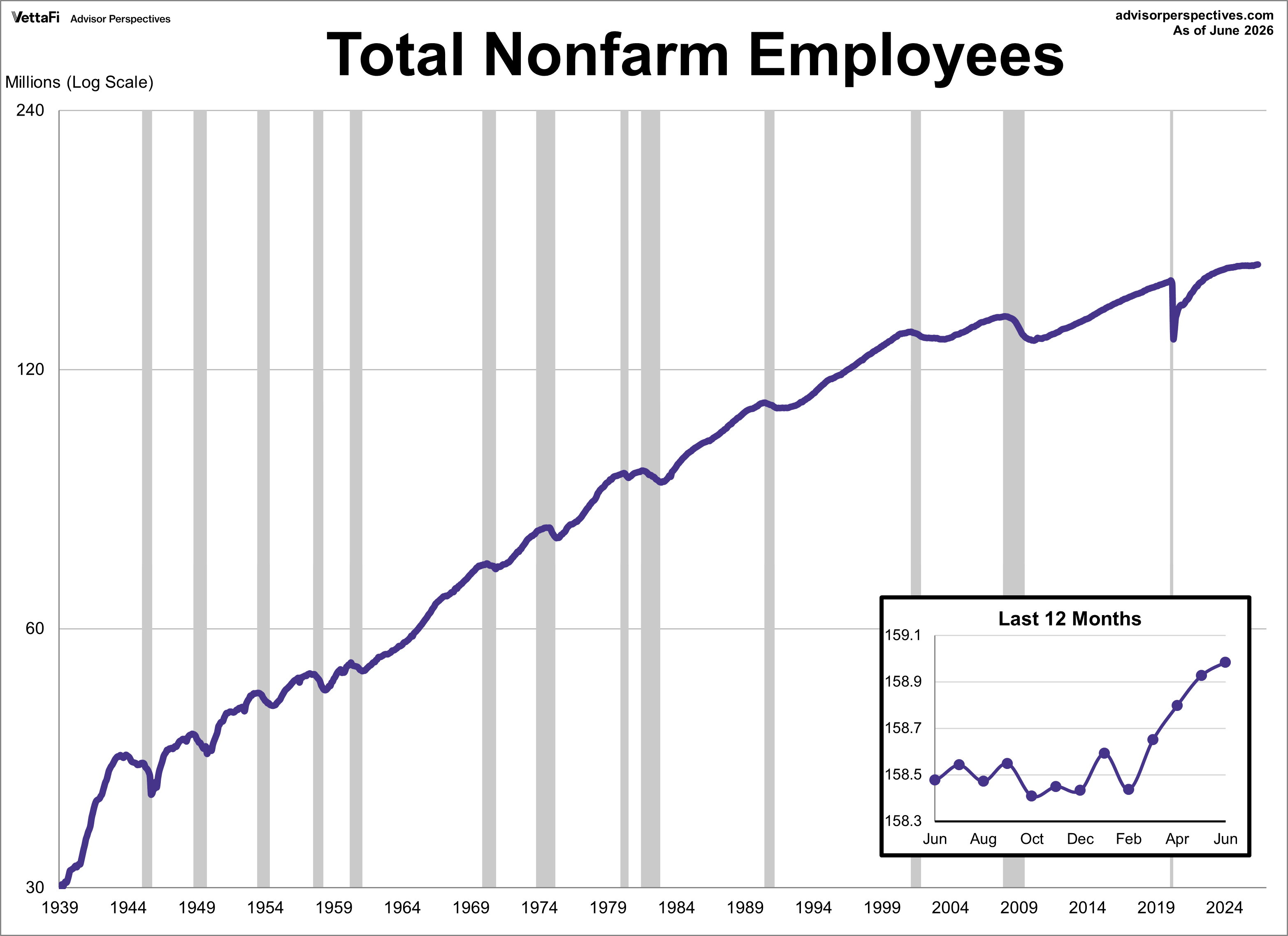

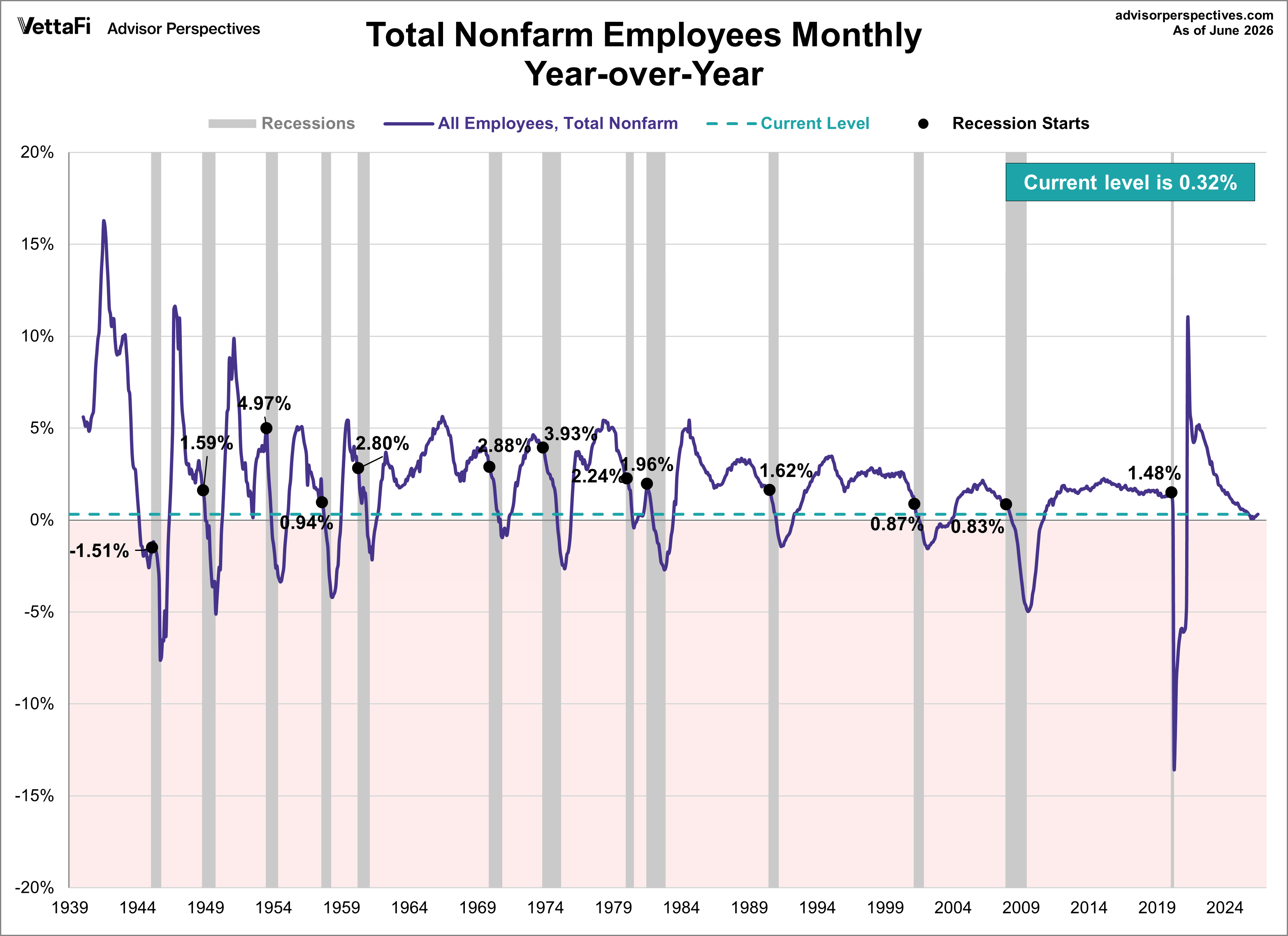

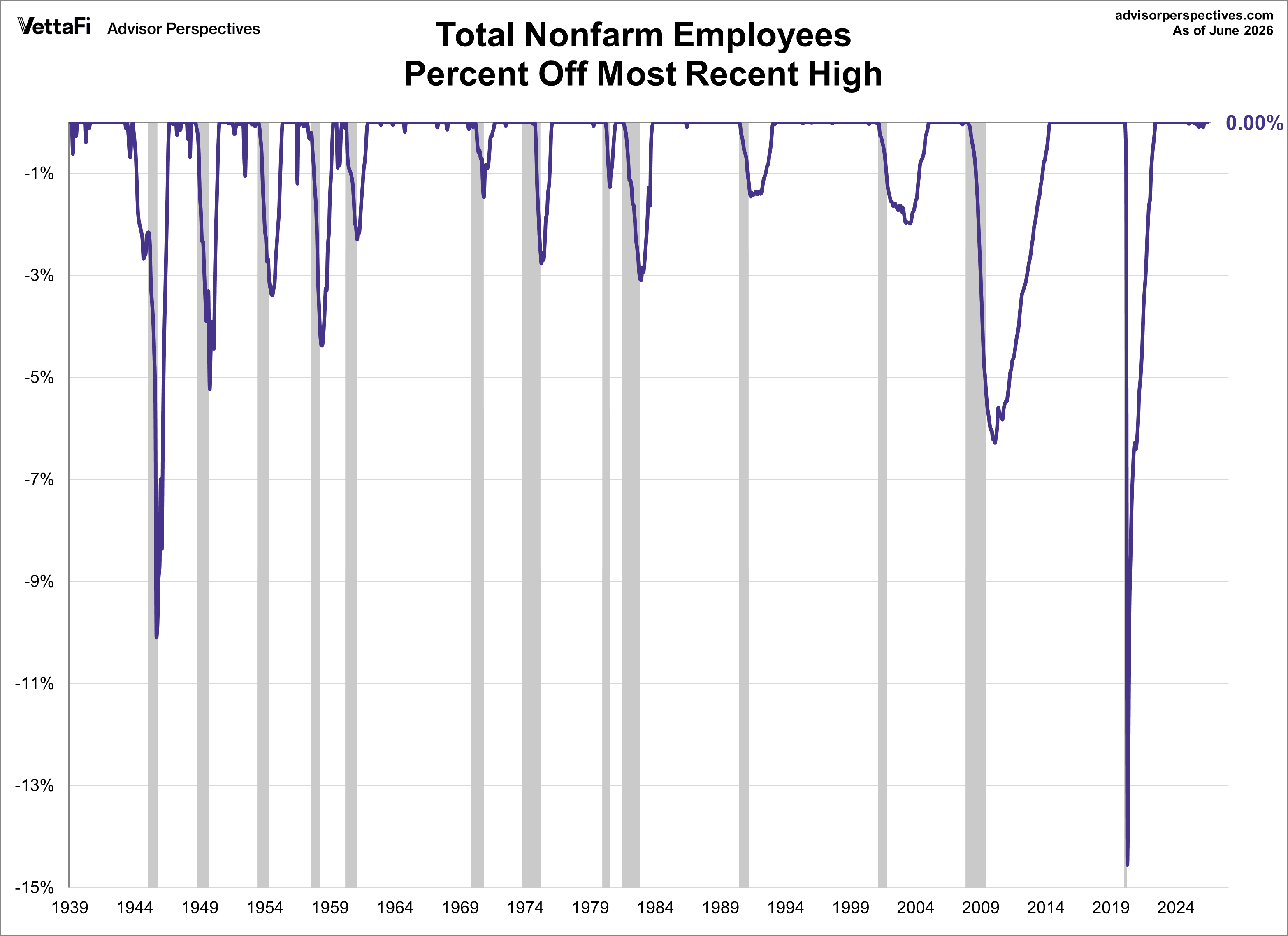

There are many ways to plot employment. The one referenced by the Federal Reserve researchers as one of the NBER indicators is total non-farm employees (PAYEMS). In the charts below we have illustrated three different data manipulations:

- A log scale plotting of the complete data series to ensure that distances on the vertical axis reflect true relative growth. This adjustment is particularly important for data series that have changed significantly over time.

- A year-over-year representation to help, among other things, identify broader trends over the years. Nonfarm employment year-over-year is currently at or below the level at the start of 12 of the 13 recessions that have started since 1940.

- A percent-off-high manipulation, which is particularly useful for better understanding of trend behavior and secular volatility. Nonfarm employment is currently at its all-time high.

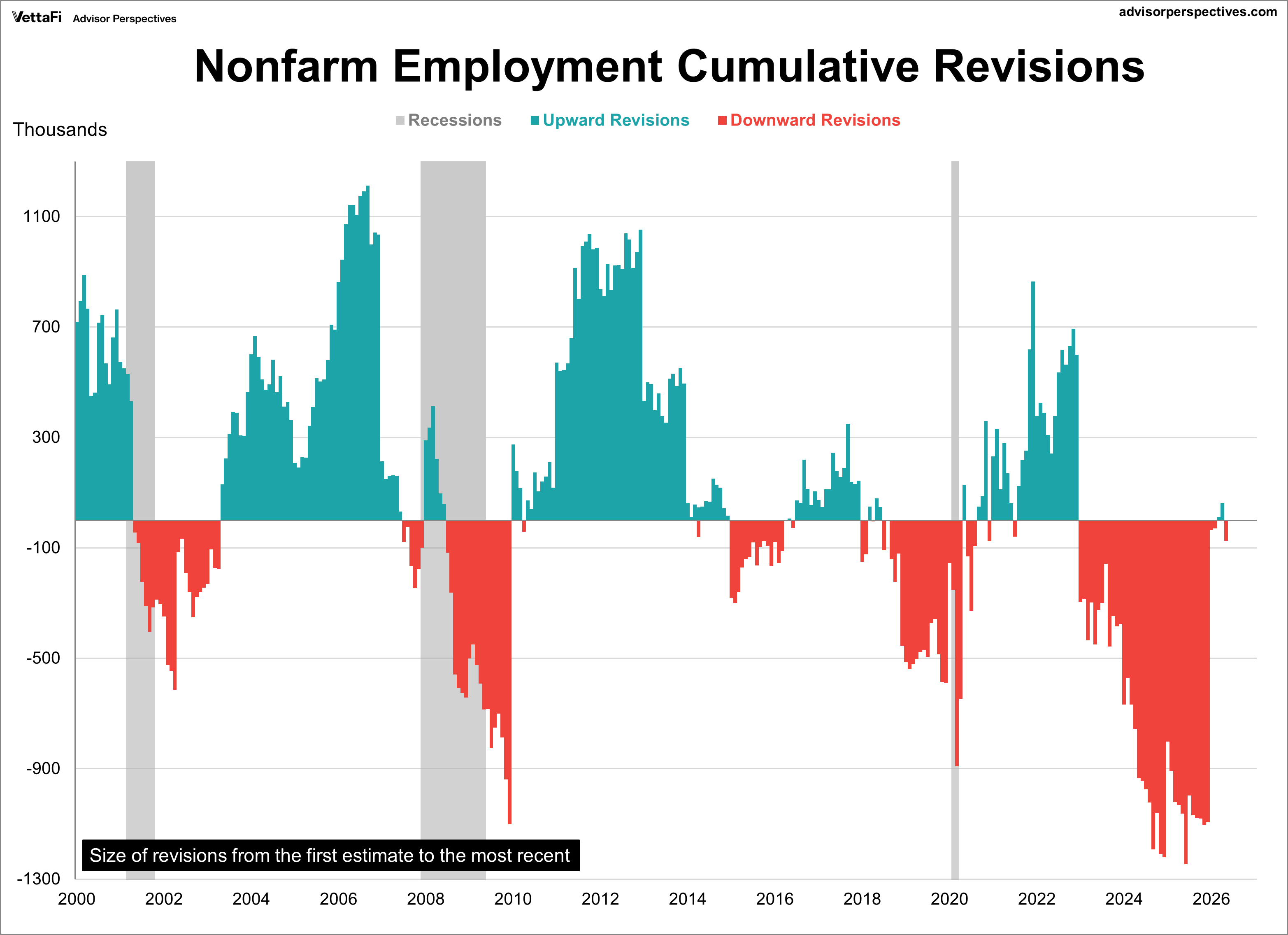

Nonfarm Employment: The Problem of Revisions

At first glance, this indicator appears to have a strong correlation with the business cycle. However, there is a major problem with this assumption: The data in this survey of business establishments undergo multiple revisions. The initial monthly estimate is subject to a first and second revisions, subsequent benchmark revisions and annual revisions that stretch back many years. The cumulative size of the revisions is quite stunning, much of which is owing to the "hindsight" of those annual revisions. The chart below measures the size of the revisions from the initial estimate to the latest employment report.

Nonfarm Employment: The Problem of Population Growth

Another problem with the non-farm employment data is that it isn't adjusted for population growth, which reduces its usefulness in illustrating secular trends. The chart below incorporates a population adjustment by dividing the non-farm employment (FRED series PAYEMS) by the civilian labor force age 16 and over (FRED series CLF16OV). The current level is at 93.87%.

Read more for an in-depth analysis of our four big recession indicators which incorporates the latest employment data.