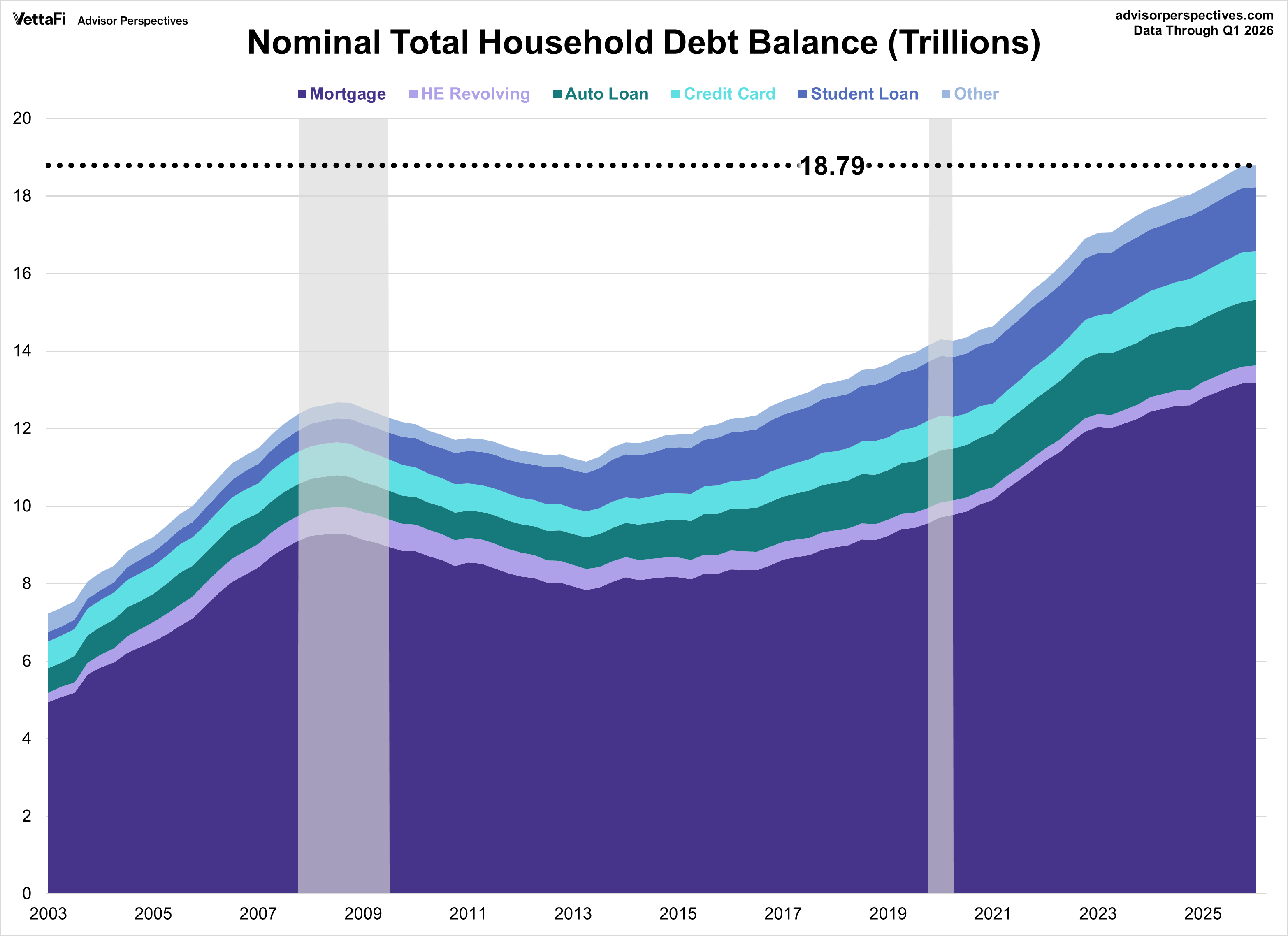

Total U.S. household debt climbed to a record $18.79 trillion in Q1 2026, a modest 0.1% ($18 billion) increase from the previous quarter. The overall rise was driven by increases across a handful of categories, specifically mortgage and auto loan balances.

Mortgage balances increased $21 billion (0.16%) to $13.191 trillion, auto loan balances increased $18 billion (1.08%) to $1.685 trillion, and balances on home equity lines of credit increased $12 billion (2.86%) to $446 billion. Conversely, credit card balances decreased $25 billion (-1.96%) to $1.252 trillion, student loan balances decreased $6 billion (-0.36%) to $1.658 trillion, and all other debt decreased $2 billion (-0.37%) to $562 billion.

As of Q1 2026, mortgage and auto loan balances are at all time high debt levels while credit card, student loan, and other debt balances peaked in the previous quarter (Q4 2025). Balances on home equity lines of credit peaked in Q1 2009.

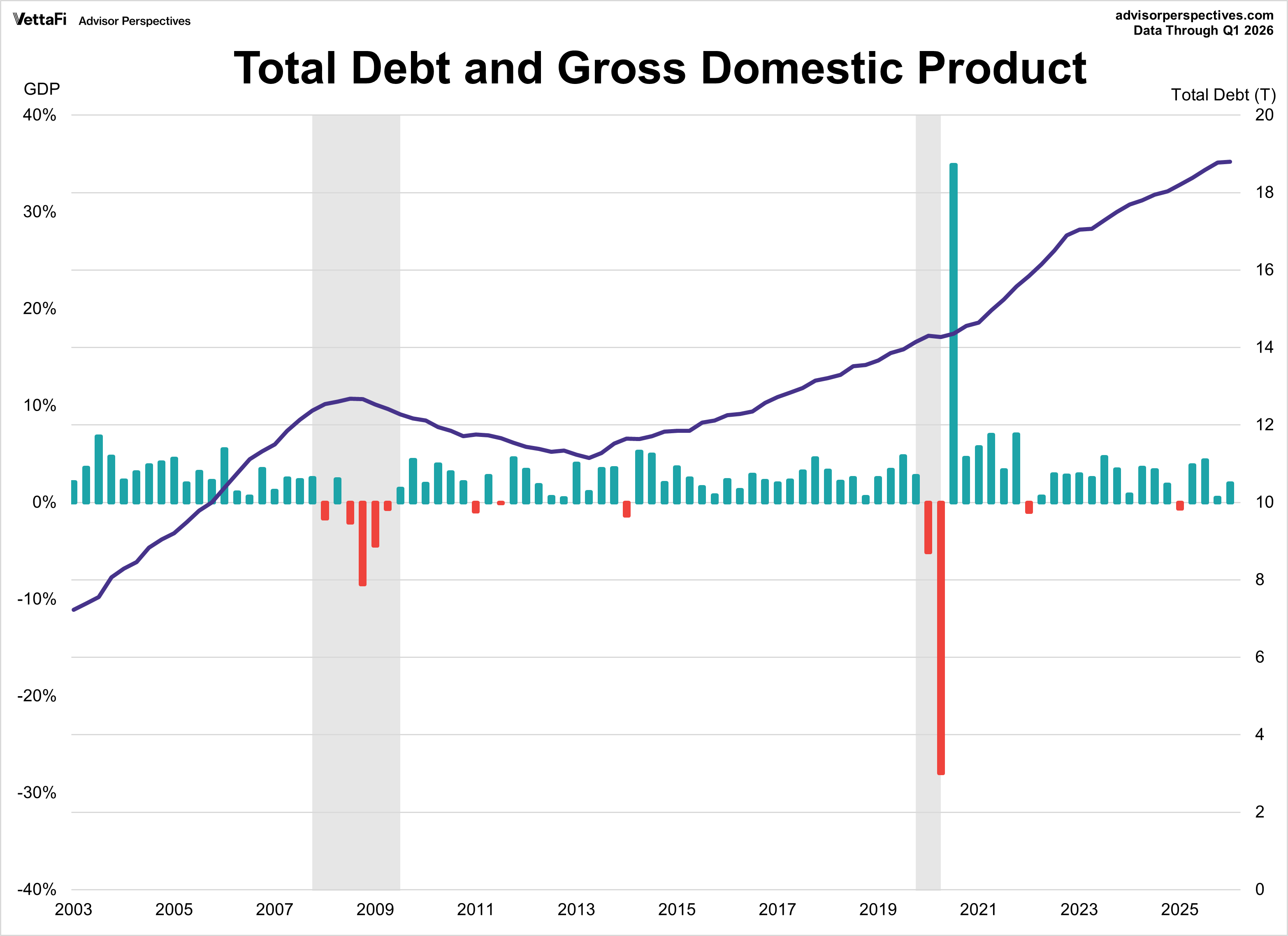

The chart below shows the total debt balance nationwide by composition in trillions of dollars. The current total is $18.79T, well exceeding the Q3 2008 peak.

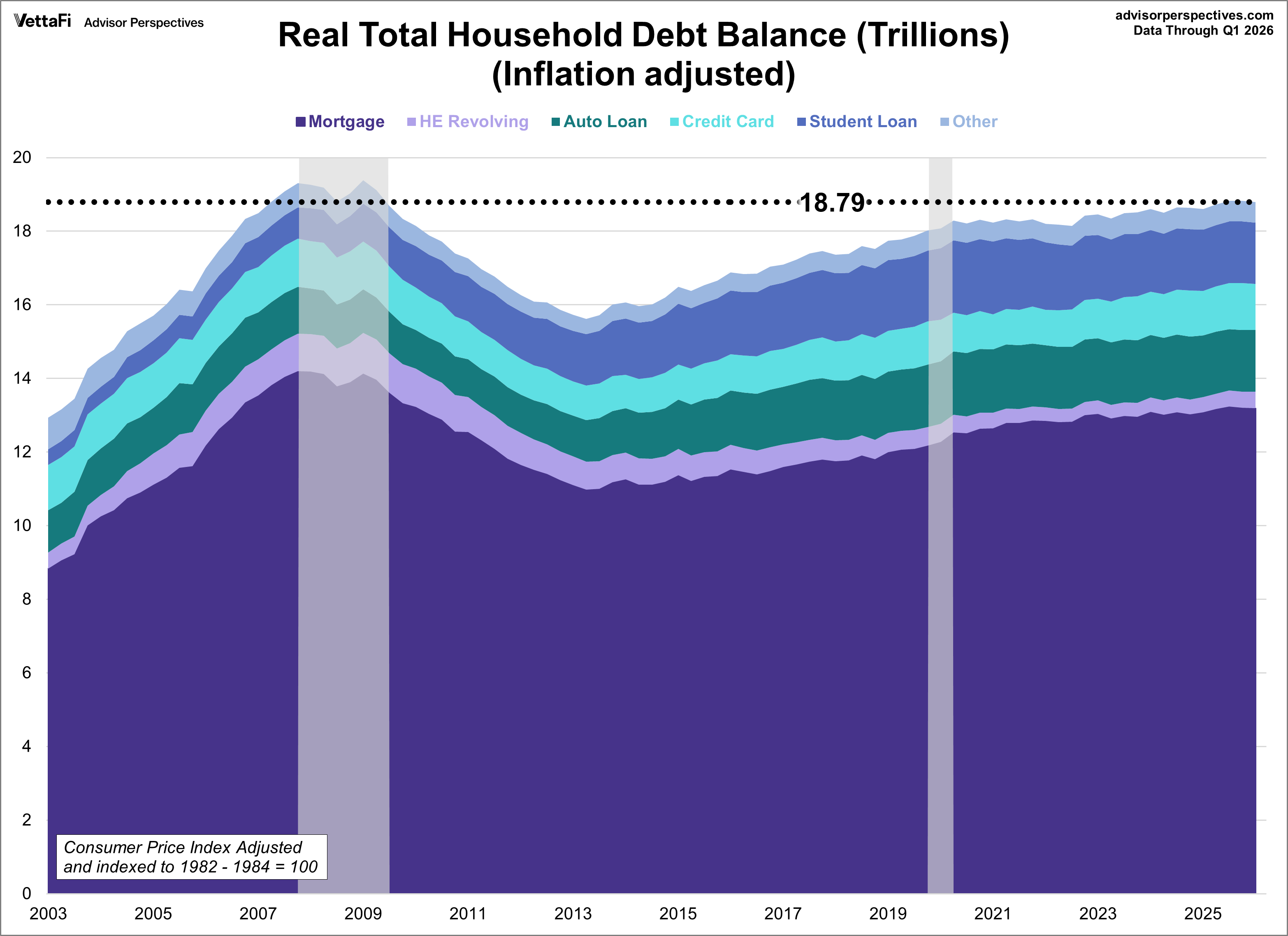

When adjusted for inflation using the Consumer Price Index (CPI), the household debt balance falls just below its Q1 2009 peak of $19.38 trillion. Similarly, debt categories that hit all-time highs in nominal terms (mortgage and auto) are no longer at their peaks in real terms. Mortgage and credit card loans hit their real all-time high in Q4 2007. Balances of home equity lines of credit reached their real all-time high in Q1 2009. While student and auto loans hit their real all-time highs in Q1 and Q2 2021, respectively. Other debt levels reached their real all-time high in Q2 2003.

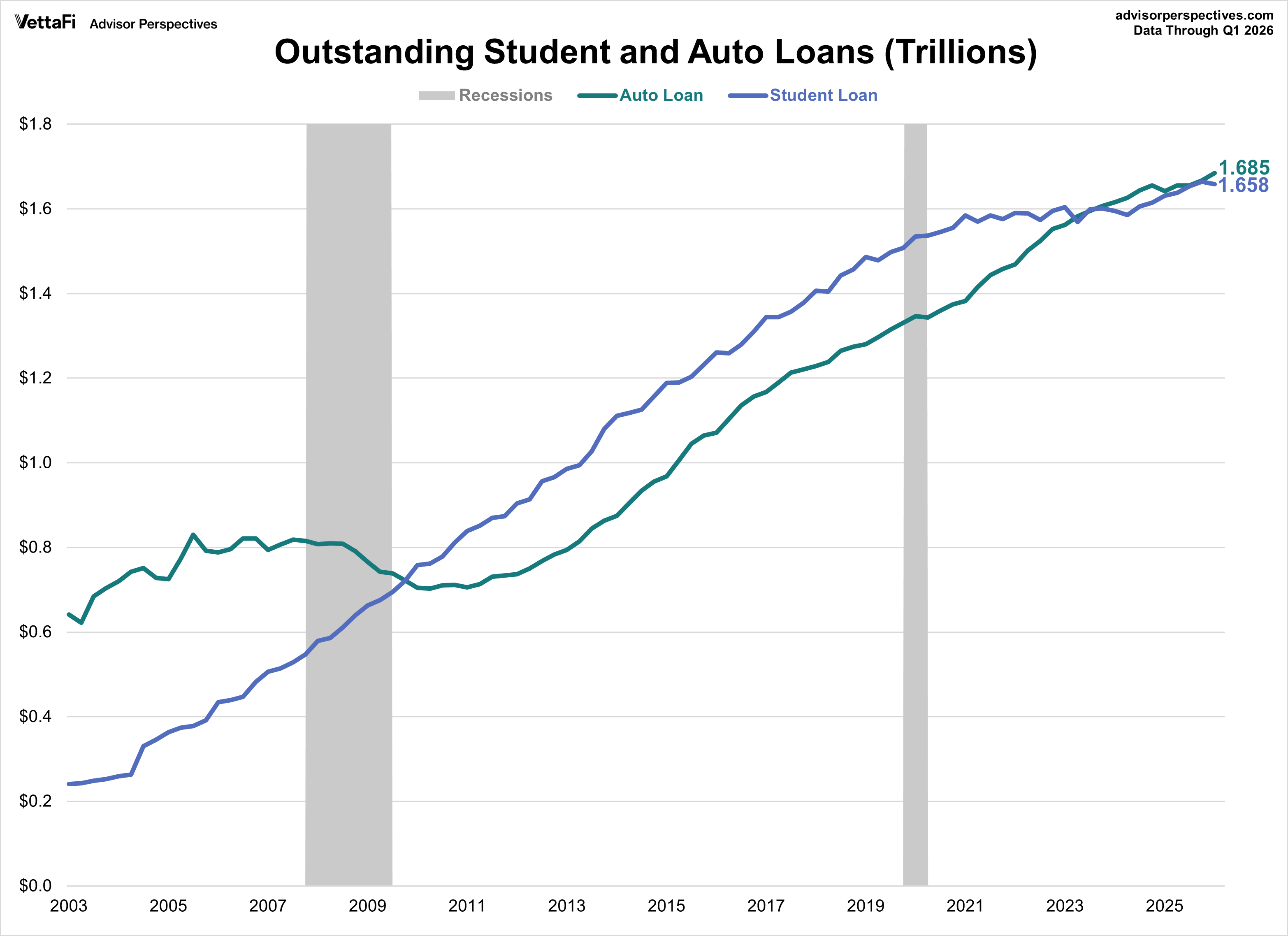

The next chart drills down into student loan debt and auto loans. Prior to 2010, outstanding auto loan balances were greater than outstanding student loan balances. However, starting in January 2010, the outstanding student loan balance rose at a faster and steadier pace. Over the past few years the student loan balance flattened out in large part because of the student loan pause that began at the start of the COVID pandemic.

In Q2 2023, the auto loan balance surpassed the student loan balance for the first time in over a decade. However, with the resumption of student loan payments, the student loan balance increased in Q3 2023 before falling behind again in Q4 2023, where it has remained since. The latest data shows that the auto loan balance exceeds the student loan balance, with a current gap of $27 billion.

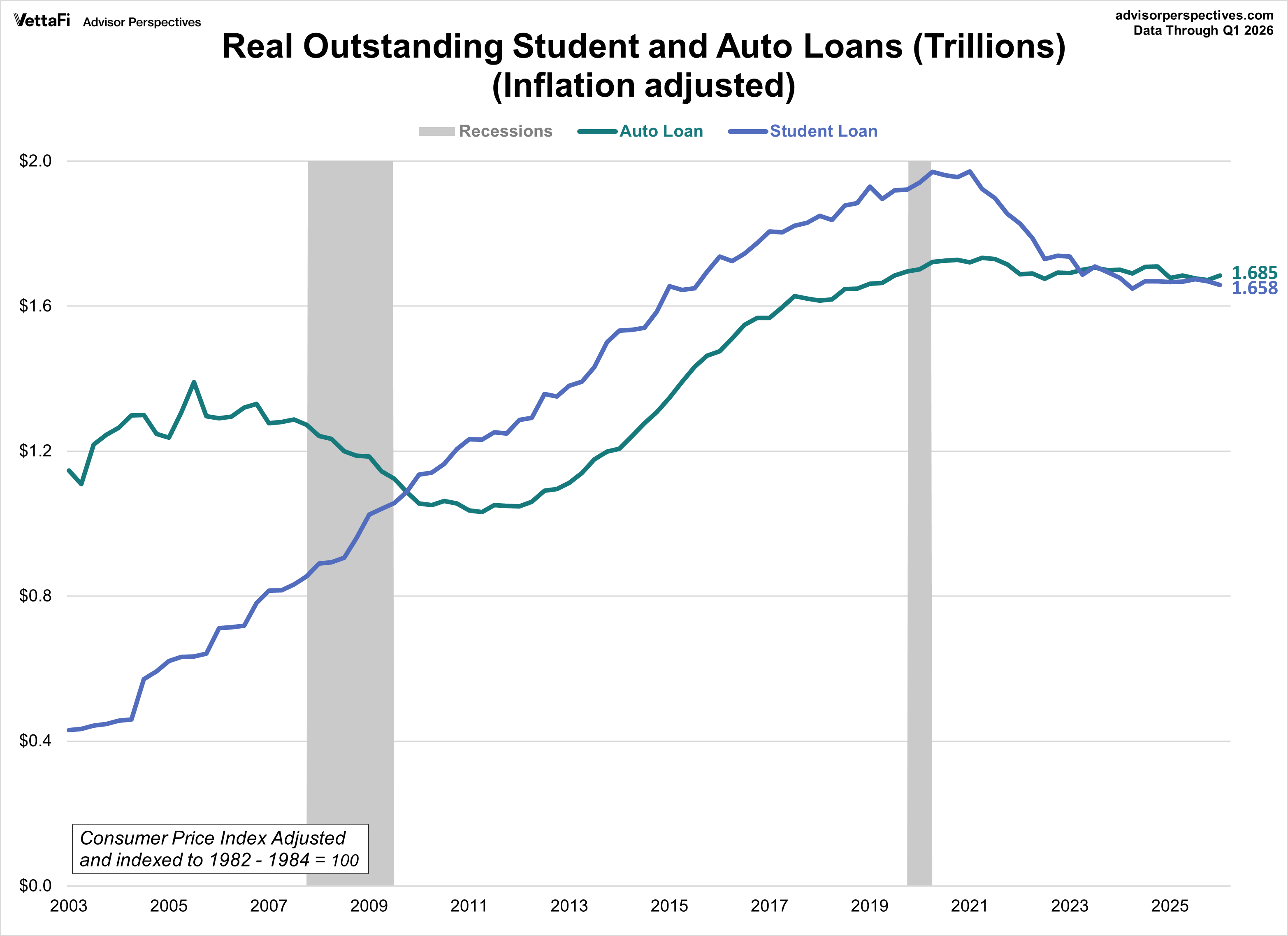

Again here is an inflation-adjusted version.

Here we include GDP for reference.

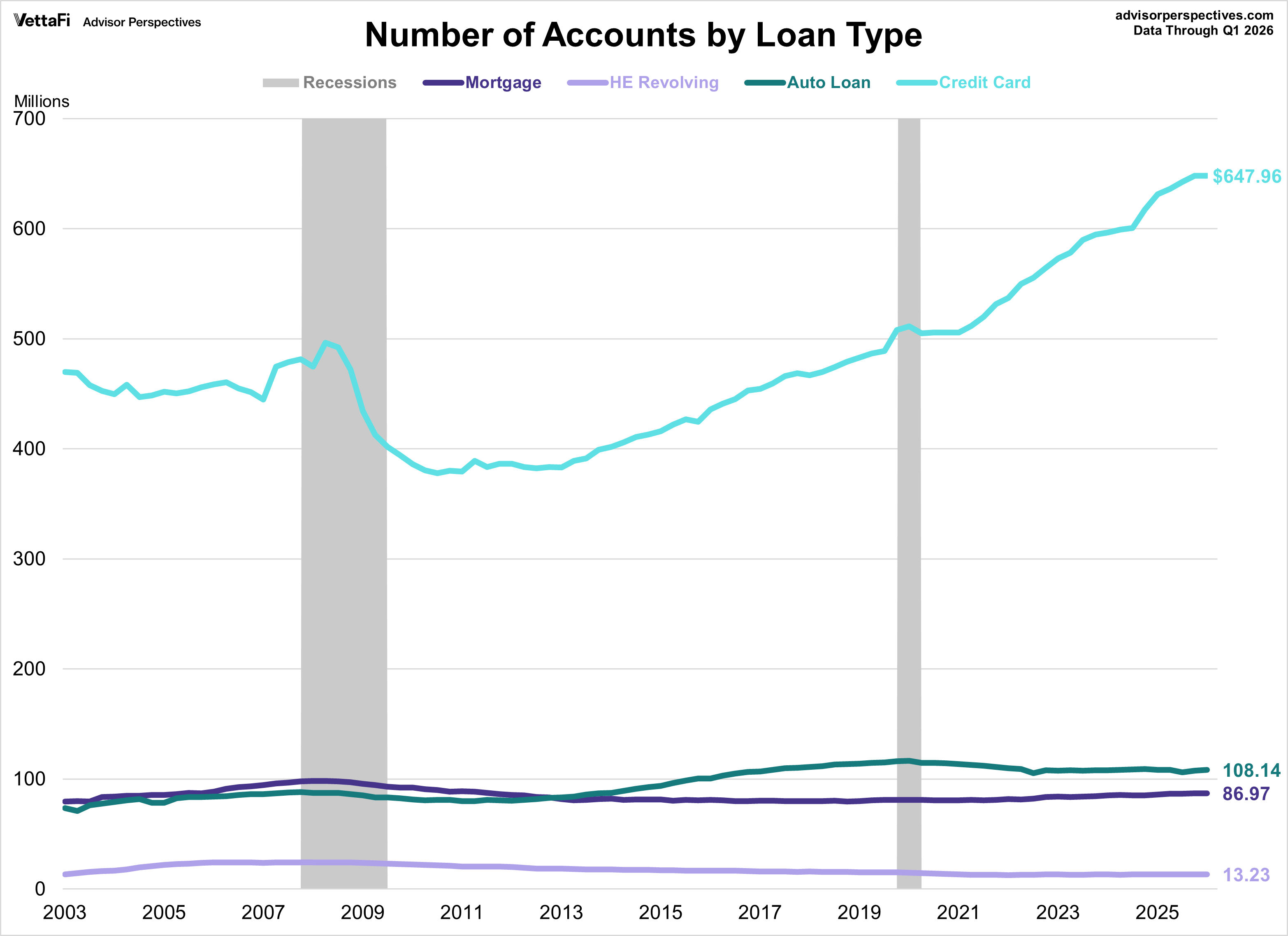

Number of Accounts by Loan Type

Our last chart shows the number of open accounts for each loan type. It's important to note that these counts include joint accounts twice, so the number of open accounts in each category is overstated.

The number of mortgage and HELOC loans reached its peak in Q1 2008 during the housing crisis, while auto loans peaked in Q1 2020, just before the COVID pandemic. Meanwhile, the number of credit card loans is now at an all-time high.

Background on the Household Debt and Credit Report

As a result of the housing and mortgage crisis of the Great Recession, economists have been paying more attention to the liabilities portion of household balance sheets. Among the New York Federal Reserve Board's many economic reports is the Household Debt and Credit report, which is released quarterly with data going back to 2003.

Data is collected through the NY Fed's Consumer Credit Panel which is constructed from a nationally representative random sample of Equifax credit report data resulting in a sample size of over 40 million individuals quarterly. Here is some background on the report from the NY Fed:

The large increases in consumer debt and defaults—of mortgage debt in particular—during the Great Recession highlighted the importance of understanding the liabilities reflected on household balance sheets. To that end, one of the CMD’s large data collection projects is the New York Fed Consumer Credit Panel, which is constructed from a nationally representative random sample of Equifax credit report data. Analysis of this data set is regularly reported in the CMD’s Quarterly Report on Household Debt and Credit. The data set can be used to calculate national and regional aggregate measures of individual- and household-level credit balances, and delinquencies by product type. The Consumer Credit Panel also provides new insights into the extent and nature of heterogeneity of debt and delinquencies across individuals and households.

Read more updates by Jen Nash