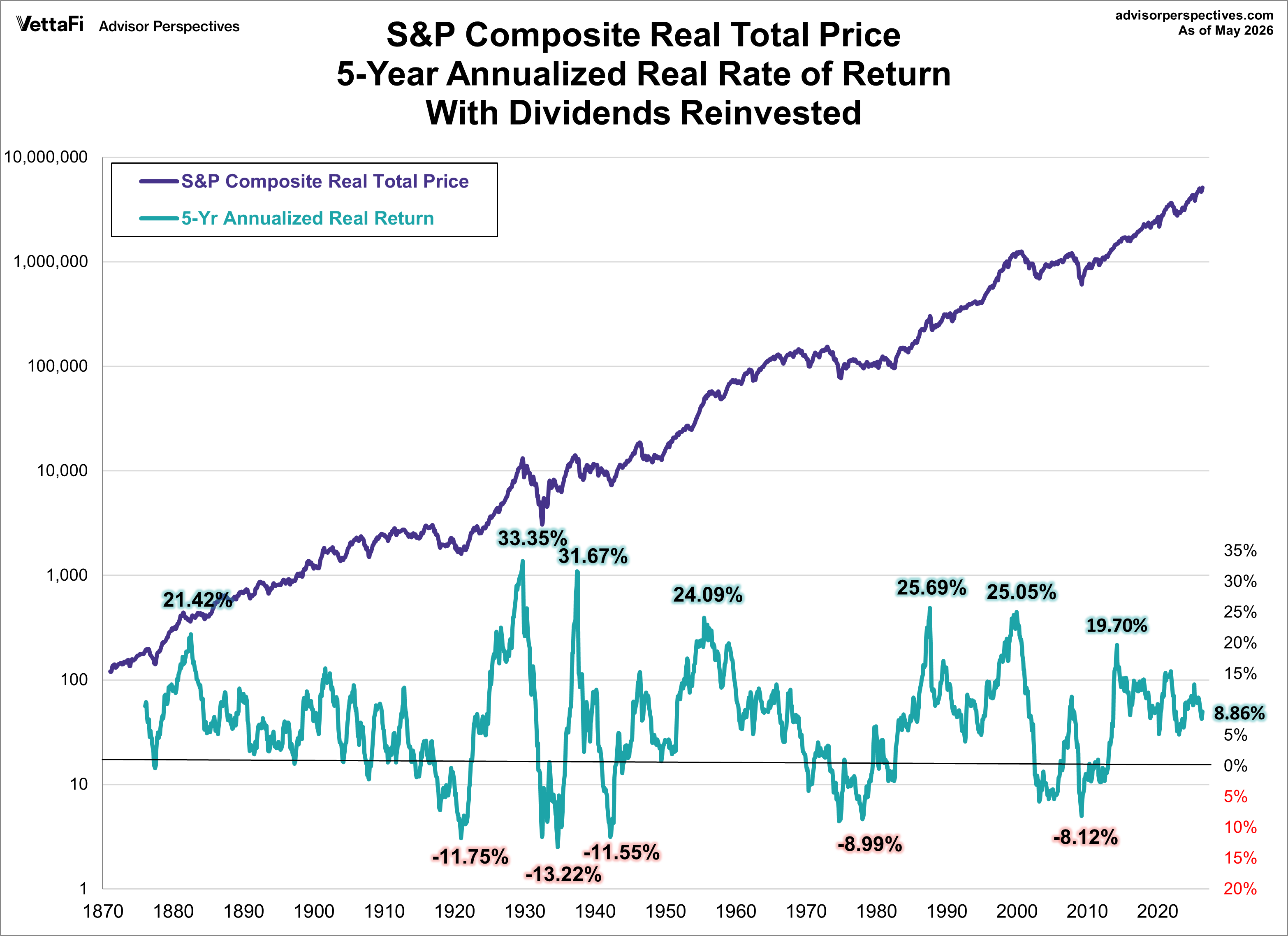

Here's an interesting set of charts that will especially resonate with those of us who follow economic and market cycles. Imagine that five years ago you invested $10,000 in the S&P 500. How much would it be worth today, with dividends reinvested but adjusted for inflation?

The purchasing power of your investment has increased to $15,551 for an annualized real return of 8.86%.

Had we posed the same question in March 2009, the answer would have been a depressing $6,654. The -8.12% real return would have cut the purchasing power of your initial investment by a third.

Total Returns Roller Coaster

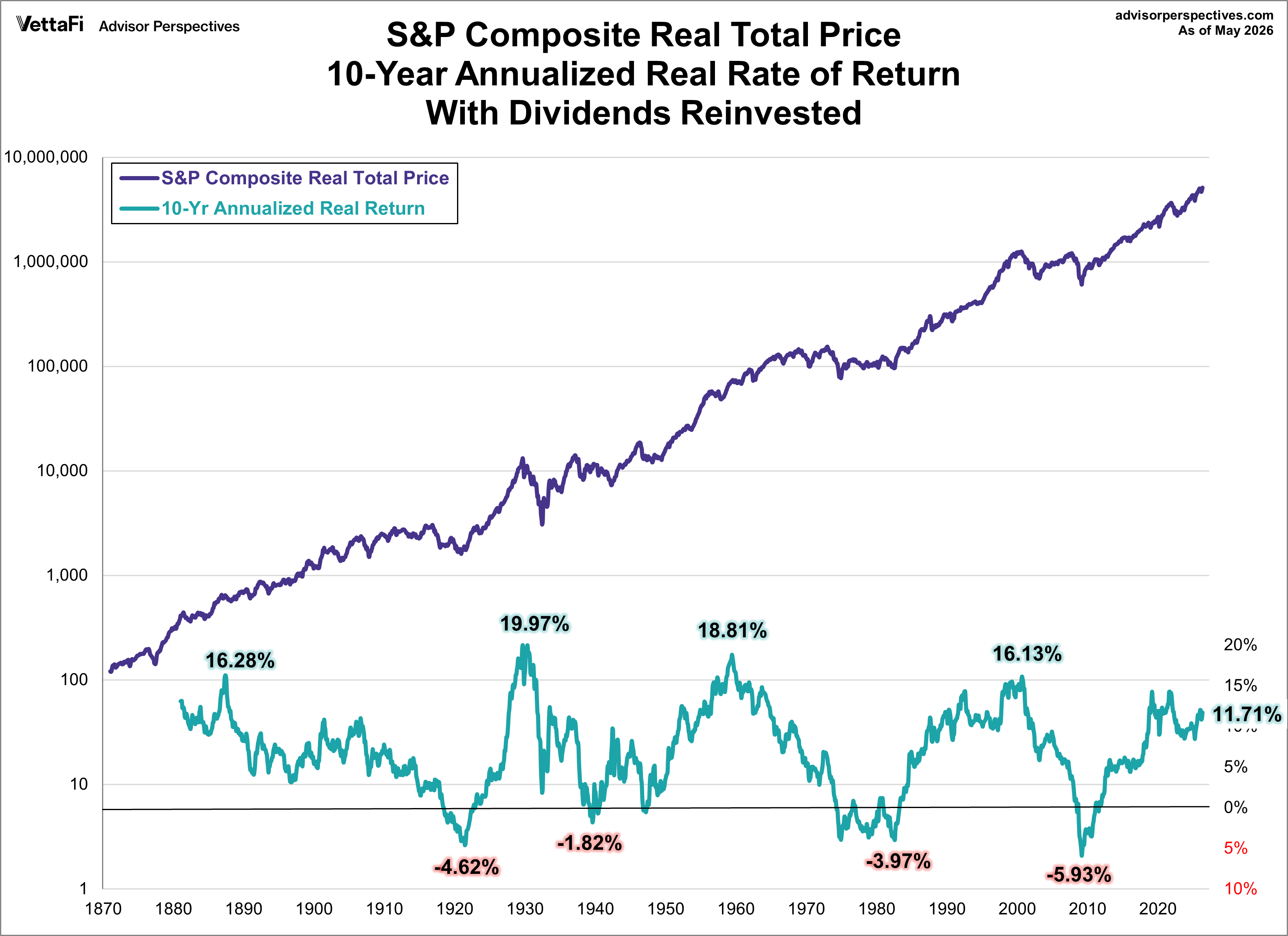

Let's increase the time frame to 10 years. The annualized return becomes slightly smaller than the 5-year time frame. As of the end of last month, your $10,000 invested 10 years ago has grown to $32,055 adjusted for inflation, an annualized real return of 11.71%.

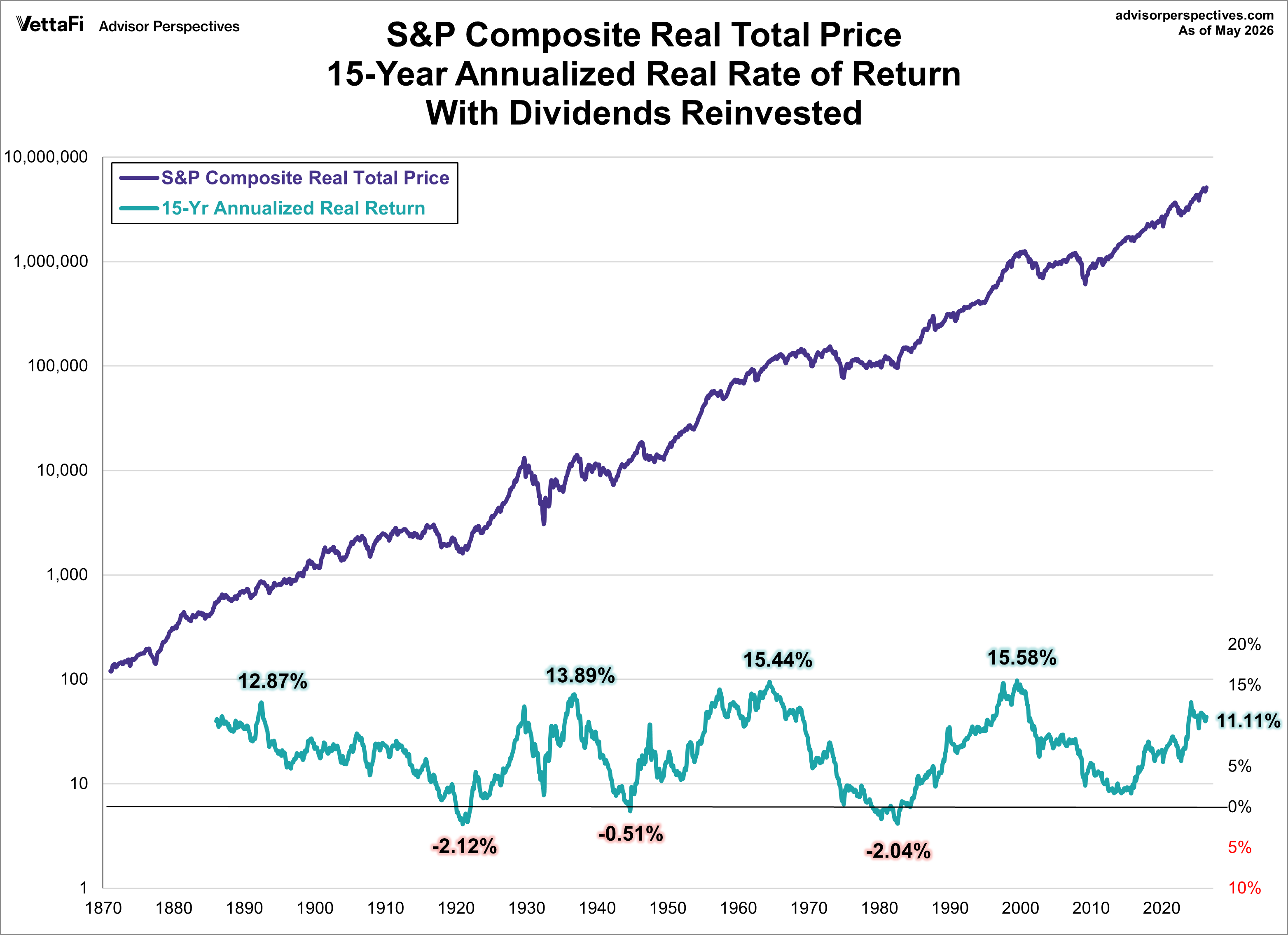

The 15-year time frame has a larger annualized return than both the 5- and 10-year periods. Your one-and-a-half decade investment of $10,000 has grown to $52,565 adjusted for inflation for an annualized real return of 11.11%.

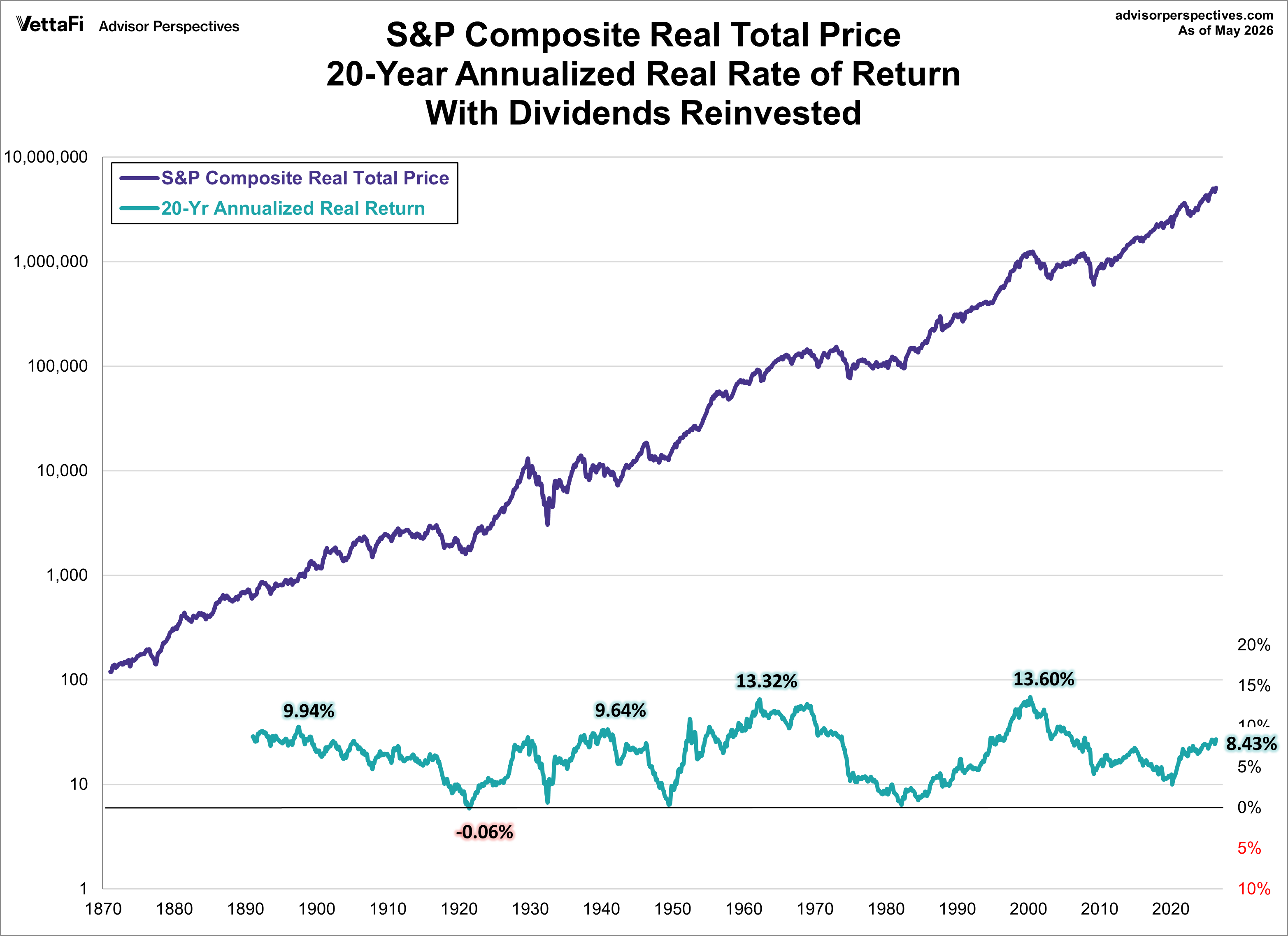

If we extend our investment horizon to 20 years, the roller coaster is less volatile with higher lows and lower highs. Your two decade investment of $10,000 has grown to $53,625 adjusted for inflation for an annualized real return of 8.43%.

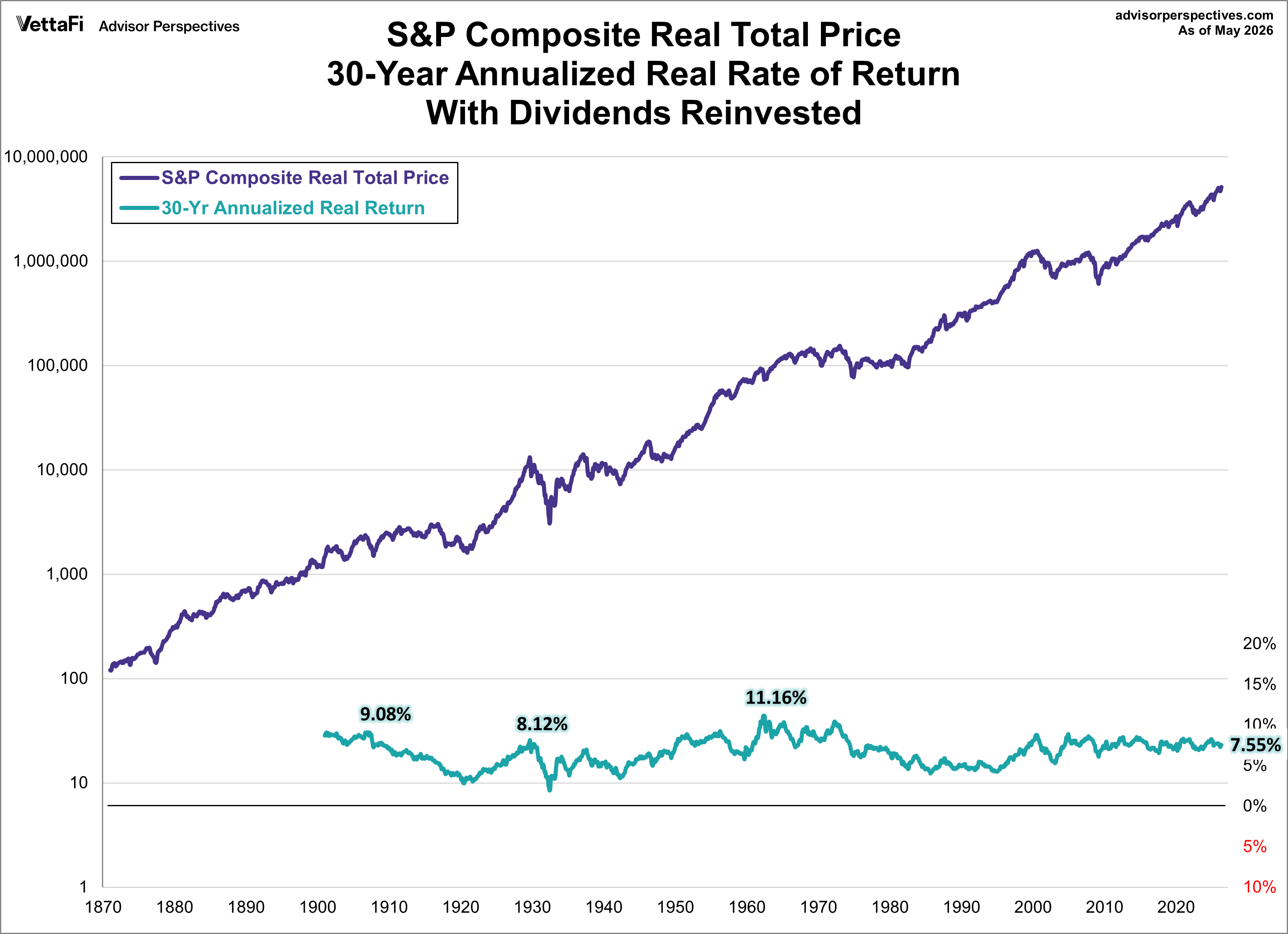

An investment of $10,000 made 30 years ago has now grown to $95,505 adjusted for inflation for an annualized real return of 7.55%. The volatility decreases further with a 30-year timeline. But even for that three-decade investment, the annualized returns since 1901 have ranged from less than 2% to over 11%.

As these charts illustrate, and as many households have discovered during the 21st century so far, investing in equities carries substantial risk. Households approaching retirement should understand this risk and make rational decisions about diversification.

ETFs associated with the S&P 500 include: iShares Core S&P 500 ETF (IVV), SPDR S&P 500 ETF Trust (SPY), Vanguard S&P 500 ETF (VOO), and SPDR Portfolio S&P 500 ETF (SPYM).