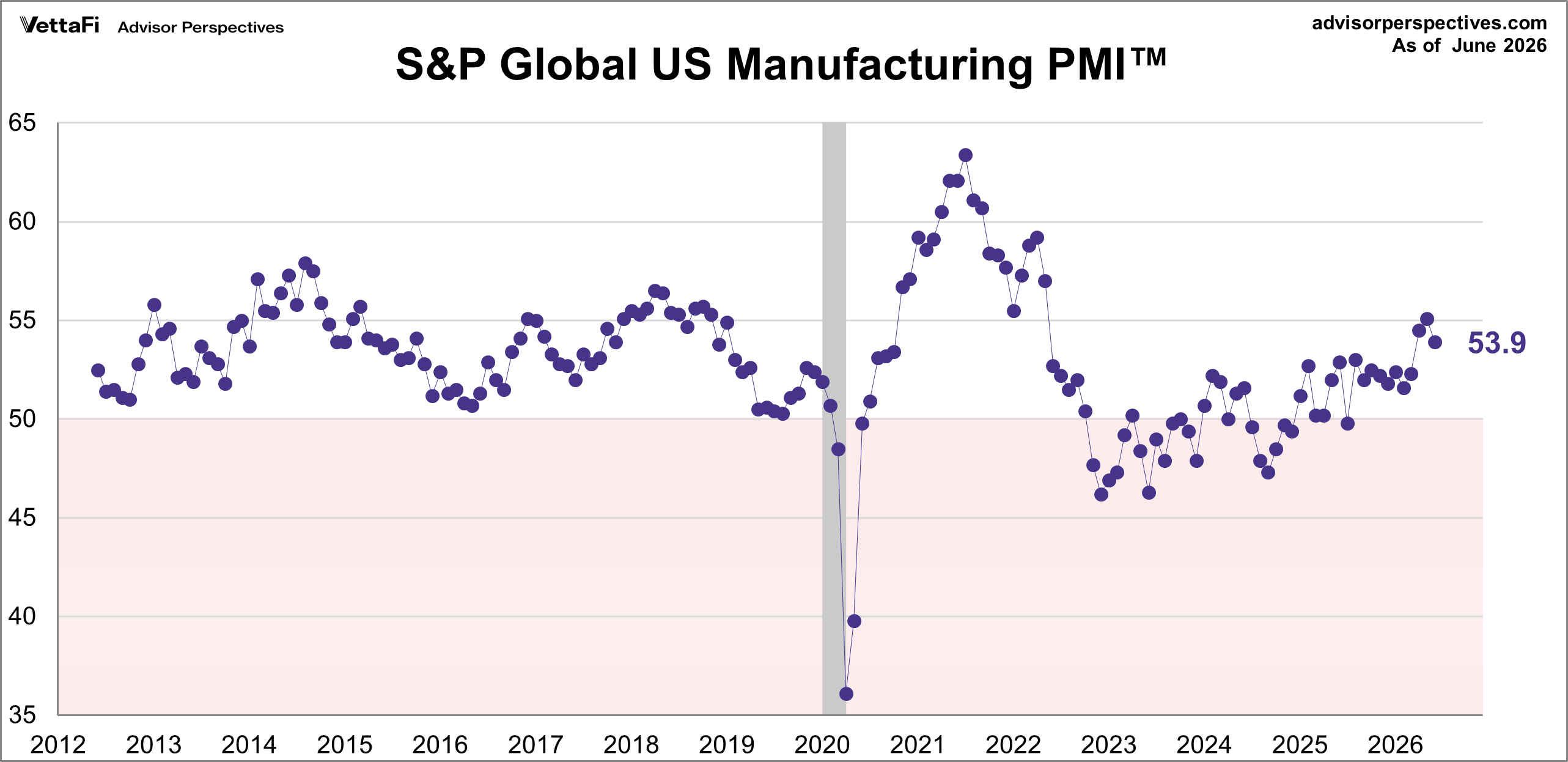

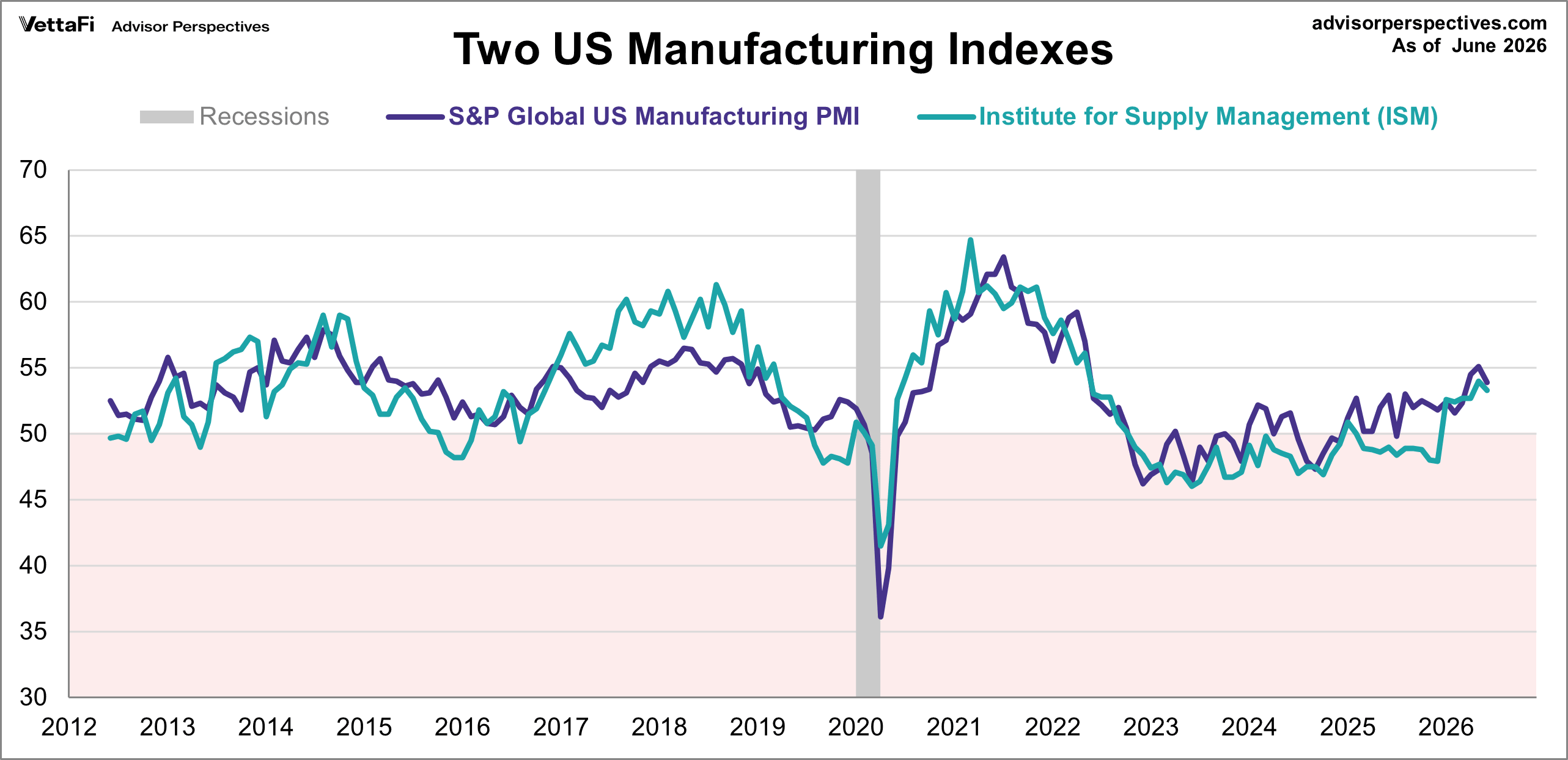

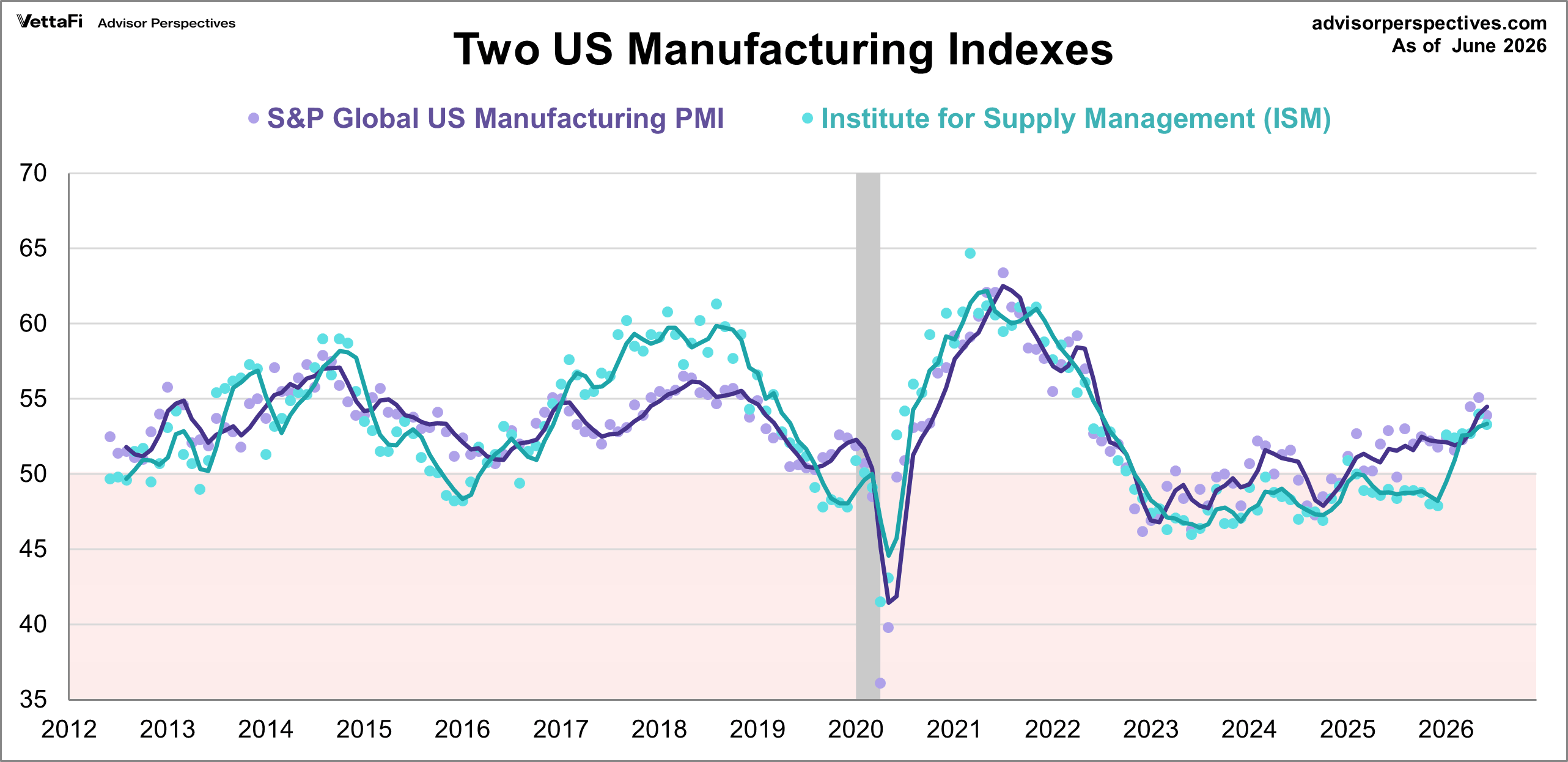

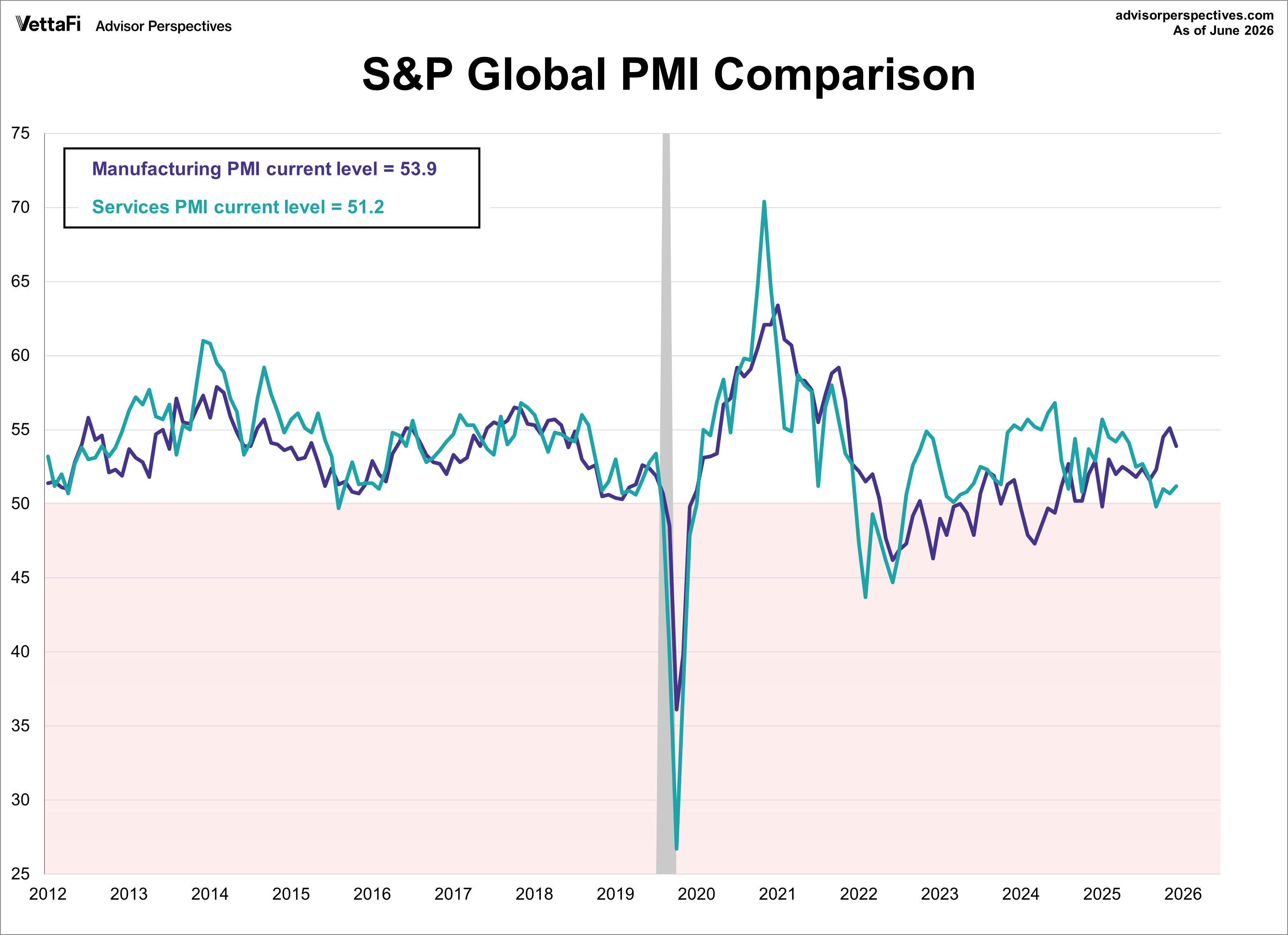

U.S. manufacturing expanded for an eleventh straight month in June but the growth eased to its lowest level in three months. The S&P Global PMI fell 1.2 points to 53.9 last month, falling short of the 55.7 forecast.

Here is an excerpt from Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, in the latest press release:

“US manufacturers reported a further marked improvement in growth of output and order books in June, according to S&P Global’s PMI data, extending the growth spurt that has been reported since the outbreak of the war in the Middle East. Employment was nevertheless cut sharply as firms often sought to offset the rising cost of energy and raw materials.

“Supply chain delays and upward price pressures continued to be widely reported, albeit moderating thanks to recent news of an improving situation in the Middle East. However, despite the recent drop in energy prices and brighter outlook for shipping, business confidence has fallen sharply, in part reflecting concerns that an end to war-related inventory building could start to act as a drag on sales."

Background on the S&P Global US Manufacturing PMI

The S&P Global US Manufacturing PMI™ measures the activity level of purchasing mangers in the manufacturing sector through a questionnaire of ~600 manufacturers. The reported headline number is a weighted average of New Orders (30%), Output (25%), Employment (20%), Suppliers' Delivery Time (15%), and Stocks of Purchases (10%). The S&P Manufacturing PMI is a diffusion index, meaning that a reading above 50 indicates expansion in the sector compared to the previous month and a reading below 50 indicates contraction.