Investors are often drawn to healthcare for its innovation and long-term growth potential. Yet in practice, allocations are often concentrated in a few large pharmaceutical companies, whether through direct stock picking or index weightings. We believe these approaches can lead to narrow exposure in a diverse sector, instead of helping investors access healthcare’s broad opportunity set.

From new surgical technologies to life-saving treatments, healthcare companies produce some of the economy’s most exciting advancements. But market-cap weighted indexes may not fully capture that breadth because they naturally overweight a sector’s largest companies. In healthcare, many of those top names are pharmaceutical firms. While large drugmakers are an essential part of the healthcare landscape, they represent just one segment of an evolving sector.

See more: AI Enthusiasm Leaves Little Margin for Error

A Diverse and Dynamic Sector, Often Narrowly Defined

Healthcare encompasses a broad range of businesses serving patients, providers and researchers. Beyond pharmaceutical and biotechnology companies developing new medicines, the sector includes medical device and diagnostic firms; life sciences tools providers; and healthcare services, technology and distribution companies that help deliver care efficiently to patients worldwide. Each industry has distinct growth drivers and competitive dynamics.

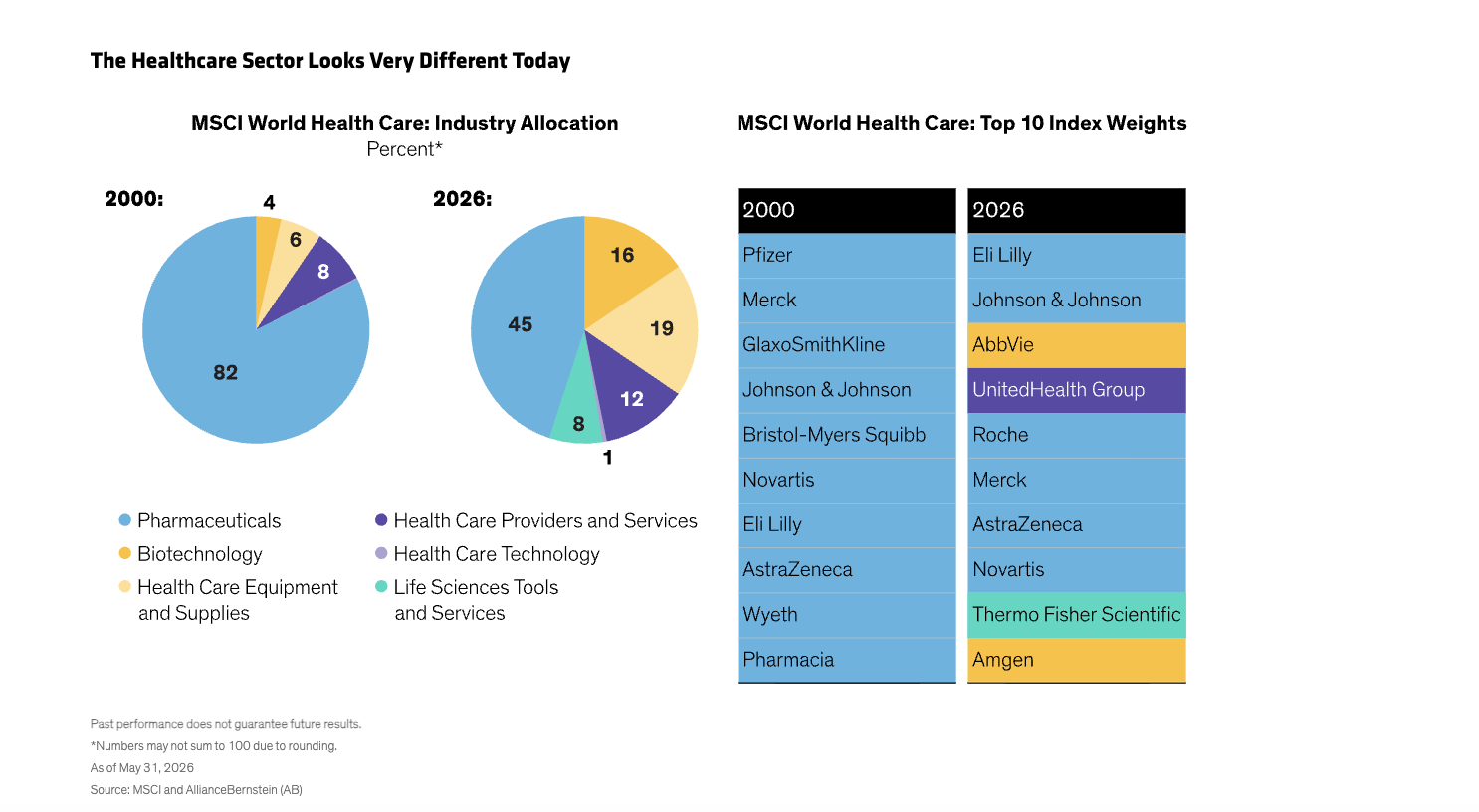

Even though healthcare benchmarks have evolved over time, drugmakers still dominate. Pharma stocks, which represented 82% of the MSCI World Health Care Index in 2000, comprise 45% of the index today (Display). While other industries such as healthcare equipment and supplies and healthcare services have increased in representation, benchmark-tracking investors are still disproportionately exposed to the success or setbacks of large pharmaceutical companies.

Why Concentration in Pharmaceuticals Matters

We believe pharmaceutical companies play an important role in a well-diversified healthcare portfolio. Many have developed crucially important therapies while building global commercial franchises, generating substantial cash flows and creating significant long-term shareholder value.

That said, building healthcare exposure through a small number of pharma stocks can introduce risks. Drug development is costly and uncertain, with less than 10% of drugs entering clinical trials ultimately receiving the US Food and Drug Administration’s approval, according to academic research1. Competition is intensifying in many therapeutic areas, which puts pressure on pricing and market share for even the most established franchises. Every large pharmaceutical company faces the same structural reality: patents expire over time and pipelines must constantly be refilled to maintain profitability. Some will manage this well, others won’t.

In recent years, several widely held names have faced these challenges, from pipeline setbacks and competitive pressures to merger-related issues. As a result, we think investors should view pharmaceuticals as one component of a broader healthcare allocation rather than as a proxy for the sector.

Sector Leadership Changes from Year to Year

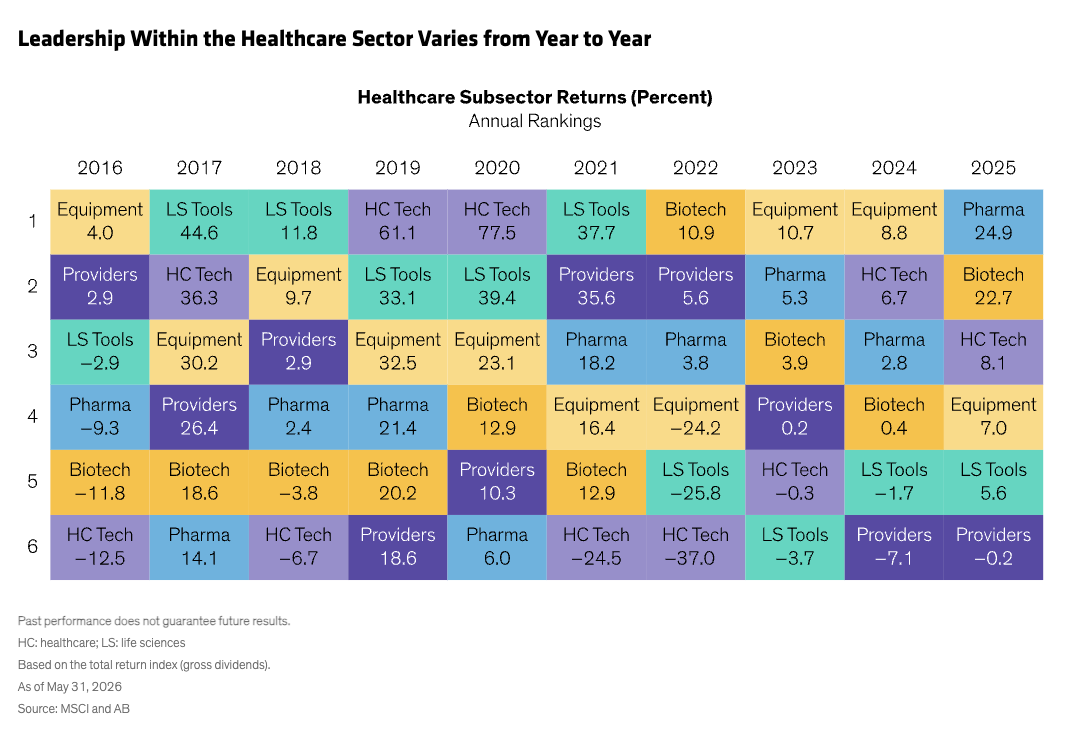

Return patterns reinforce the need for diversification. The companies driving healthcare returns tend to change from year to year, which is why we believe it’s important to maintain flexibility across industries and market-cap ranges. Over the last decade, for example, pharmaceuticals only led the sector once—in 2025 (Display). Most of the time, pharma finished in the middle of the pack while other industries such as equipment and life sciences tools led.

Healthcare Leaders Typically Start Outside the Spotlight

For investors who want to allocate broadly to healthcare, the next question is how to gain that exposure—through passive strategies or active management.

As we see it, identifying healthcare leaders early is key. Often, the most exciting companies only become index constituents after they reach a substantial market cap, when most of their early growth has already occurred.

Some of today’s biggest healthcare names held small index positions—or none at all—while they were building pipelines, refining technologies and establishing market share. Active management can seek to identify similar companies earlier, when their opportunities may be less widely appreciated. Examples include Argenx, which develops antibody-based therapies for rare and severe autoimmune diseases, and Vertex Pharmaceuticals, a market leader in cystic fibrosis treatments. Each spent years innovating and gaining recognition in their respective markets before securing spots in major healthcare indices.

Innovation increasingly extends beyond drug development. Advances in medical technology, diagnostic testing and surgical equipment are creating new growth opportunities and AI is increasingly being introduced in commercial tools across the sector. For instance, Edwards Lifesciences, which makes devices for structural heart diseases, has expanded its business to minimally invasive valves that can improve longevity and quality of life for more patients. Halozyme Therapeutics, a biotech company that has developed drug-delivery technologies to support pharmaceutical clients, has yet to be included in the MSCI World Health Care Index.

Active Strategies Can Create Advantages

In our view, active management can add value to healthcare allocations in several ways:

- responding to changing company outlooks—for example, adjusting exposure as fundamentals shift, rather than maintaining static index weights that typically only change after share prices move;

- identifying emerging leaders earlier, particularly companies gaining traction before they enter benchmarks; and

- selecting stocks within subsectors, where index exposure may favor the largest or most established names rather than those best positioned to benefit from changing competitive dynamics and long-term industry trends.

Active healthcare fund managers can pair selective exposure to established large-cap companies with overweight positions in smaller, potentially faster-growing companies.

Large pharmaceutical companies with quality businesses certainly have a place in any healthcare portfolio. But an active approach can look beyond headline index weights to identify firms with durable fundamentals and diverse business models. In a sector that continues to reinvent itself, we believe that flexibility can create powerful advantages for long-term investors.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

References to specific securities discussed are for illustrative purposes only and should not to be considered recommendations by AllianceBernstein L.P. It should not be assumed that investments in the securities mentioned have necessarily been or will necessarily be profitable.

© AllianceBernstein

Read more commentaries by AllianceBernstein