Investors who look below the surface may discover opportunities beyond the AI superpowers.

The S&P 500’s recent advance is masking a more dynamic story for US equity investors. Market winners remain confined to a tight clique of AI-related technology stocks, yet more companies are showing attractive fundamentals. For active equity investors, we believe this points to a more diversified and differentiated opportunity set ahead.

US stocks have enjoyed a strong run, advancing by 15.2% in the second quarter. Catalysts for equity gains include a decline in oil prices amid Middle East negotiations, resilient corporate results and enthusiasm for the AI build-out. Yet some active investors may feel frustrated because a relatively narrow group of dominant stocks hasn’t translated into outperformance for many diversified equity strategies.

At first glance, the market’s advance appears to validate a simple conclusion: stay close to the companies leading the AI investment cycle. But we believe heightened valuations of technology firms leave little margin for error in market expectations for AI. And beneath the headline returns, fundamentals are improving across a much broader set of businesses than market performance alone would imply.

Fundamentals Improve Beyond the Usual Suspects

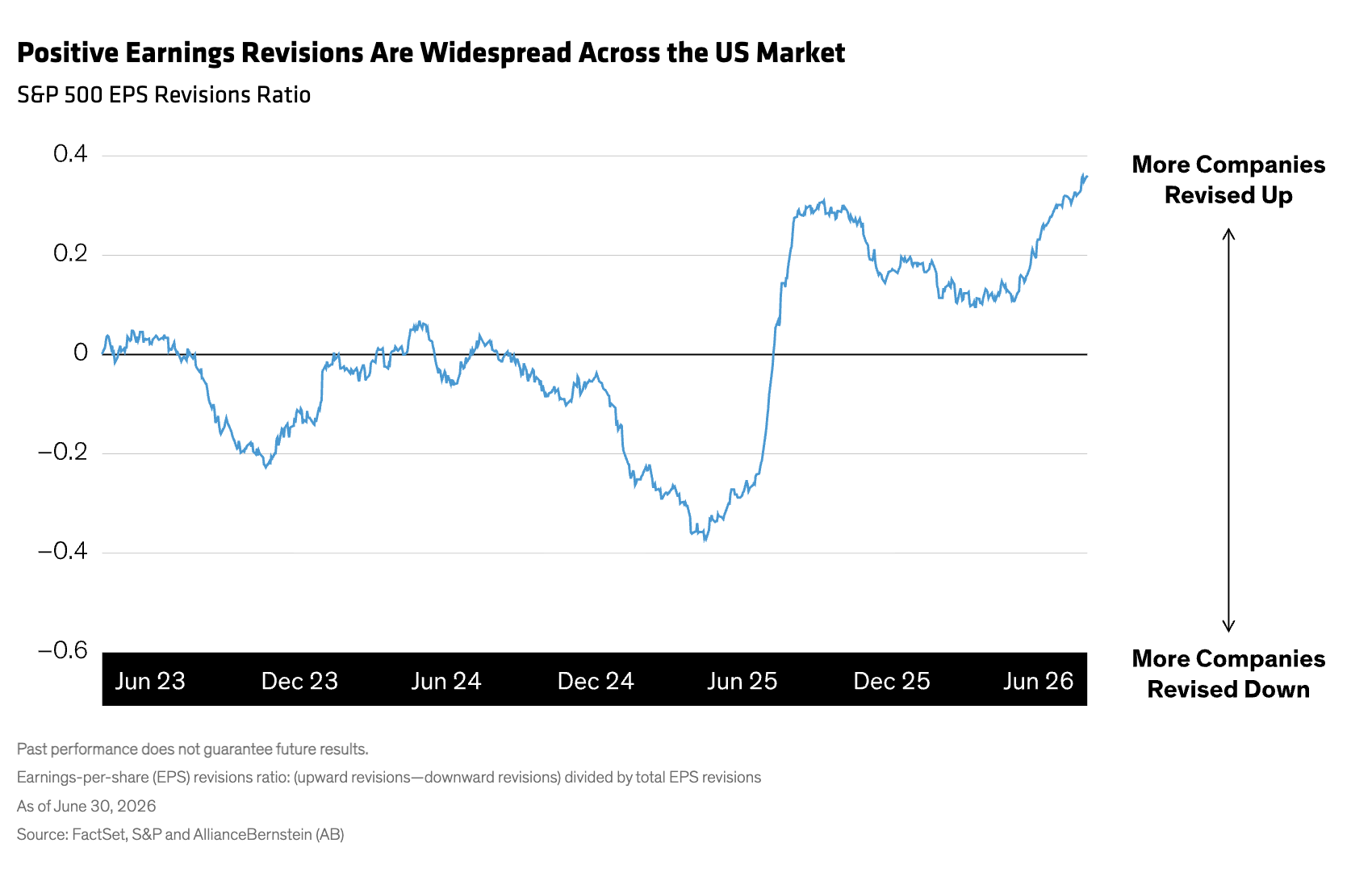

Following a strong first-quarter earnings season, analysts have raised forecasts for an increasing number of S&P 500 companies (Display). Positive revisions are no longer isolated to a handful of mega-cap technology firms. Instead, they point to strengthening corporate health across a wider range of industries.

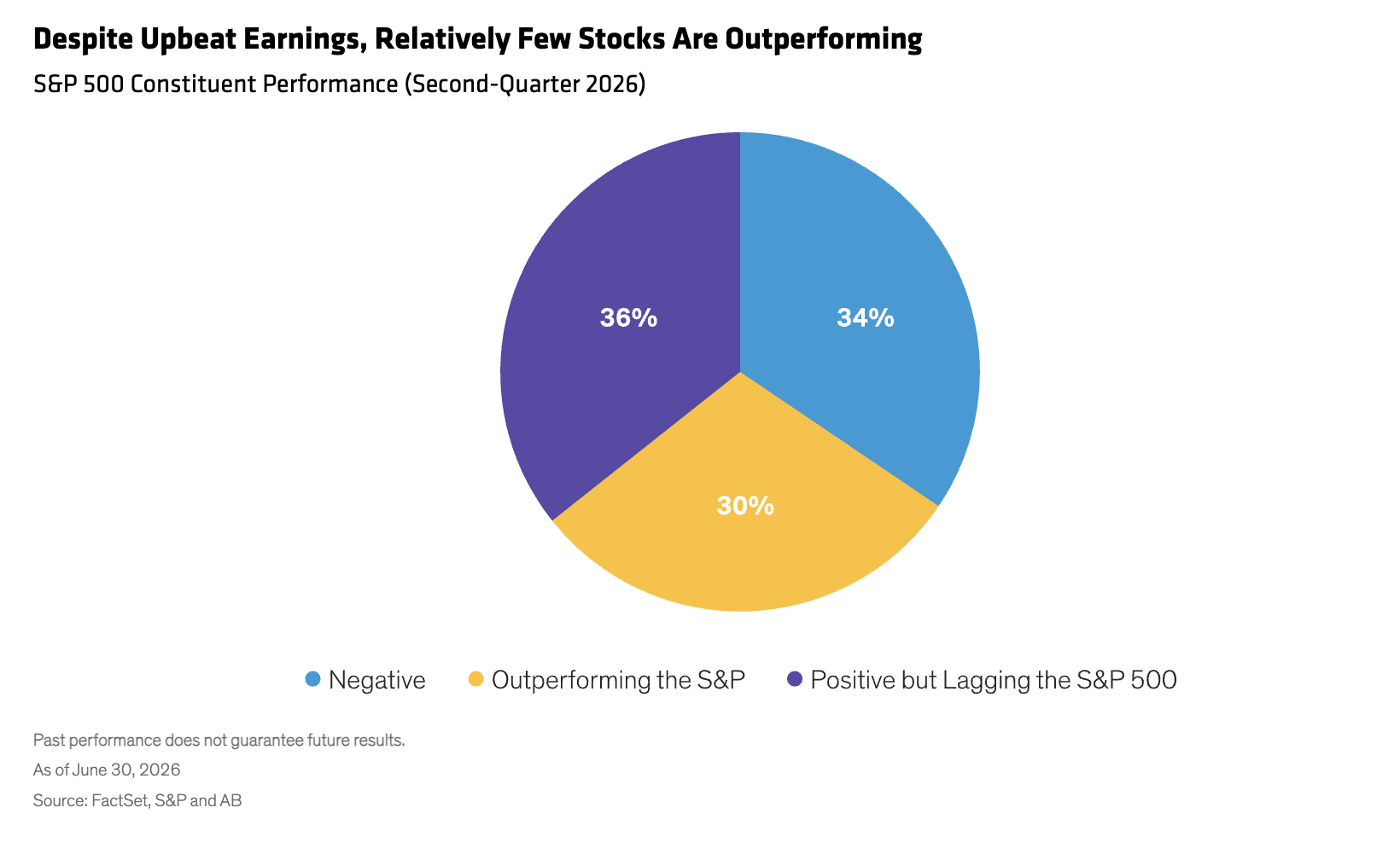

Yet even as earnings trends improve, market leadership remains highly concentrated. Only about 30% of S&P 500 constituents outperformed the index in the second quarter (Display).

Beneficiaries of AI spending have led the pack. The strongest gains have largely been captured by semiconductor manufacturers, hardware providers and other technology companies in the AI ecosystem. Many other firms have generated positive returns but still lagged the benchmark, while a significant share of stocks remain in negative territory.

In other words, broadening fundamentals have not yet translated into broadening performance. In our view, this disconnect helps explain why investors looking only at index-level returns may underestimate the range of opportunities developing.

See more: Risks Hiding in Plain Sight

Dispersion Points to Changing Patterns

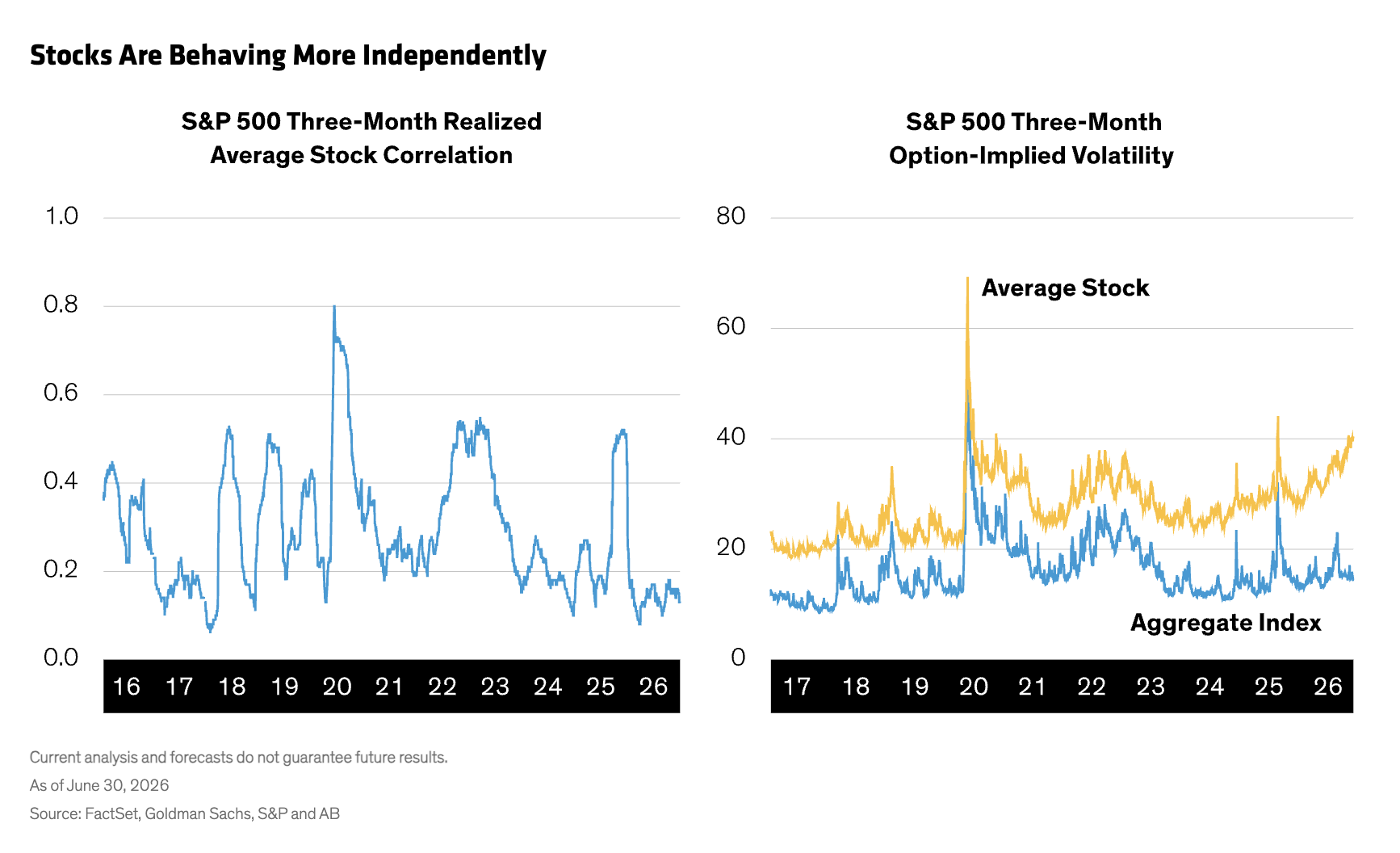

Stock correlations provide another important signal. When correlations are low, companies increasingly move according to their own fundamentals rather than broad market forces. Recent data suggest exactly that. Many stocks are following different paths, which we think is fostering a market environment in which company-specific outcomes may matter more than macro narratives alone.

For active investors, we believe this type of dispersion can be especially valuable because it expands the opportunity set for differentiated stock selection. Rather than being defined by a single dominant theme, we think the market will ultimately begin to reward a wider variety of business models, competitive advantages and earnings trajectories.

Subdued Index Volatility Is Misleading

The market’s risk profile also appears more complex than headline measures suggest. Index-level volatility remains relatively subdued, consistent with a market that has trended higher. Yet volatility for the average stock is substantially higher (Display, above).

This gap highlights a critical distinction: while the index may appear calm, individual companies face very different opportunities and risks. Such conditions often increase the importance of fundamental research and careful security selection. As we see it, investors willing to look beyond index-level signals may find a richer set of opportunities than the market’s narrow leadership would imply.

Could Dispersion Lead to More Diverse Winners?

We believe the AI leaders could be vulnerable if sentiment shifts. While the mega-caps include great businesses, we believe holding the entire cohort at or above market weights is risky, and positions should be determined by a portfolio’s research discipline and risk management. In our view, elevated valuations of the technology titans could face pressure as investors question whether massive AI-driven capital spending will create sufficient productivity and profitability benefits.

June offered an example of this tension: markets supported AI-related capital raises, yet the Magnificent Seven underperformed and contributed to a 1.0% decline in the S&P 500. At the same time, the S&P 500 Equal Weight Index, which reflects a broader spectrum of US companies, rose by 2.4%. While these observations apply to a very short time span, we think they illustrate what might happen if the AI leaders face a sustained challenge to their dominance.

Broadening the Mix

Nobody can say if June’s trading trends reflect the start of a lasting shift in market patterns. But we can say with conviction that improving earnings trends, low stock correlations and elevated stock-level dispersion suggest a more differentiated universe is emerging.

In our view, investors should look beyond today’s performance leaders and consider a broader mix of companies—including AI beneficiaries, successful adopters and businesses less exposed to disruption. If market participation eventually broadens to reflect the widening strength in fundamentals, today’s dispersion could become tomorrow’s reward.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

Walt Czaicki serves as a Senior Vice President and Senior Investment Strategist for Equities at AB.

Bryan Chang is a Vice President and Equities Investment Strategist at AB.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein