In choppy waters, many novice ship passengers will experience sea sickness. The only sure remedy is to wait it out. Symptoms will pass, as will the rough waters.

While the Middle East is still far from calm, it does appear the worst of the volatility in the region is in the past. The U.S.-Iran ceasefire is in place, with negotiations underway for a more durable peace. Most importantly for the global outlook, ship traffic through the Strait of Hormuz is starting to increase.

If the Iran conflict has ended, then so has the greatest risk to the growth outlook. Effects will linger: waves of inflation are still causing some upheaval, and shortages of critical commodities could continue to manifest for months to come. Central banks are watching prices closely to chart an appropriate course for policy.

Read more: The Strait is Open. What's Next for Markets?

Following are our outlooks for the world’s major markets.

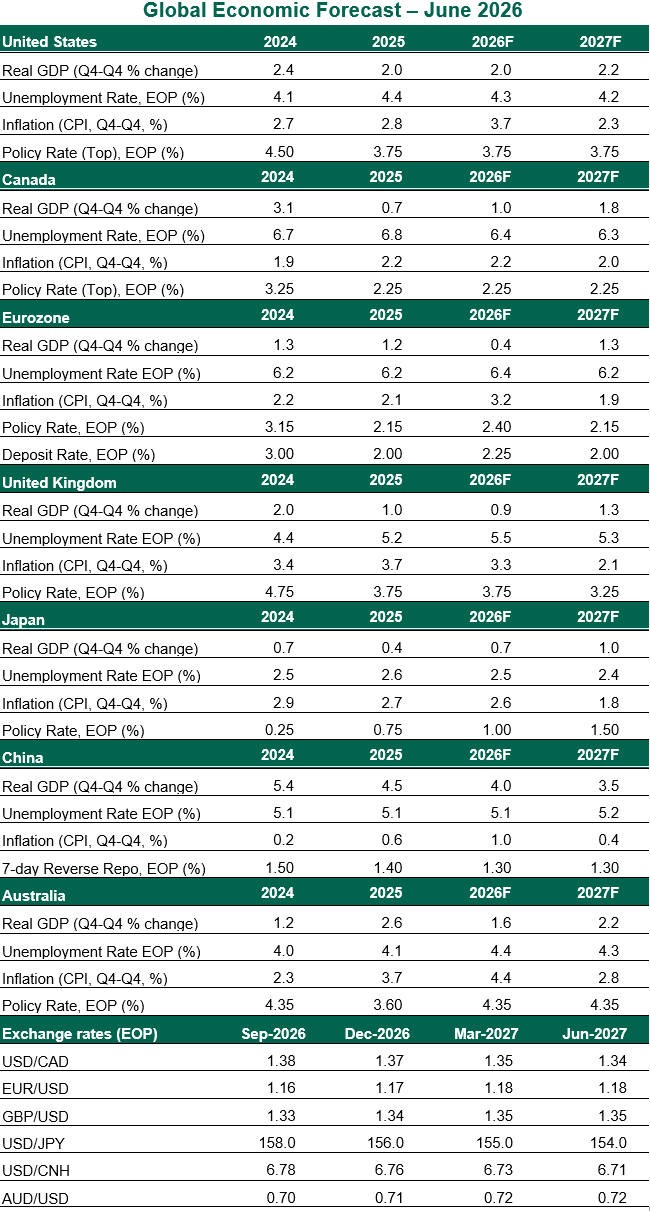

United States

- The U.S. labor market is coming back to life after a long dry spell. A gain of 172,000 new jobs in May, plus upward revisions to prior months, suggest the “no hire, no fire” dynamic is breaking toward renewed hiring. Inflation remains a challenge, with the headline consumer price index reaching 4.2% year-over-year in May; tamer core inflation (excluding food and energy) of 2.8% suggests the pass-through of energy costs has been limited. The Iran deal will support price stability, though a renewed tariff push will lead to a new round of uncertainty.

- Under the new leadership of Chair Kevin Warsh, the Federal Open Market Committee (FOMC) has squarely reaffirmed its commitment to price stability. New task forces will evaluate the central bank’s approaches to its communications, balance sheet, use of data, inflation frameworks, and views on productivity and jobs. Many aspects of the Fed may evolve, but the 2% inflation target will stand firm. In the June Summary of Economic Projections, nearly half of FOMC members expected a rate hike by end of year. We expect steady rates, with risk of a hike.

Canada

- Working through a technical recession, we have marked down our growth outlook for Canada. The decline of output in the first quarter was driven partly by one-off shifts in gold imports and government spending. Consumer spending and business investment showed modest gains, and they will support a return to growth. The Canadian economy saw an encouraging report of 88,000 job gains in its May Labor Force Survey, though this jump only serves to return employment to the level it had attained at the start of the year.

- The Canadian consumer price index gained 3.2% year-over-year in May, led by energy; core inflation remained composed at 1.6%. With core prices staying composed, the Bank of Canada held rates steady at its June meeting, a posture we expect to continue through 2027. A broadening of inflation could necessitate hikes, or a recession taking hold could bring about cuts; on balance, a prolonged hold is appropriate. The main policy event will be negotiations surrounding the U.S.-Mexico-Canada free trade agreement. A breakthrough before the July 1 deadline looks implausible. The default outcome of a shift to annual renewals will not be beneficial to cross-border investment.