Market Broadening, AI, and the Case for Diversification

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe investment professionals at Northwestern Mutual Wealth Management Company (NMWMC) provide views and commentary on the current marketplace. This content is intended to communicate our current views on the relative attractiveness of various asset classes and asset allocation strategies over the next 12 to 18 months.

Keep in mind that this viewpoint can and will change as valuations and economic variables evolve. These views should be considered in the context of a well-diversified portfolio, not in isolation, and do not offer recommendations for individual investors. Investment decisions should always be made on an individual basis or in consultation with a financial advisor based on an individual’s preferred risk levels and long-term goals.

Section 01: A tale of three markets

The first half of 2026 can be defined as a tale of three markets, with the opening two months of the year seeing a continuation of a broadening trend that began in the back half of 2025 after the Federal Reserve began reducing short-term interest rates toward a cumulative 0.75 percent of monetary easing by year-end 2025. With investors pricing an additional 50–75 basis points (bps) of cuts by the end of 2026, interest rates across the Treasury yield curve pushed sharply lower, with both the two- and the 10-year Treasury falling to 3.37 percent and 3.94 percent by February 27, 2026.

Throw in a healthy dosage of impending fiscal stimulus from the impacts of the One Big Beautiful Bill Act that was expected to increase economic growth, and the market began the year broadening ahead of what investors expected to be a wider economic expansion.

The bifurcated economy that we’ve consistently pointed to over the past few years—which has driven a similarly bifurcated market—finally appeared poised to narrow, as its primary driver, higher interest rates, began to ease.

As expected, this positively impacted our portfolios, which remain positioned for an economic and market broadening—though that outcome may follow a temporary “hiccup” if the Fed is ultimately forced to overtighten policy to bring inflation lower. Interest rate- and economically sensitive U.S. Small- and Mid-Cap stocks each rose nearly 8 percent, outpacing the artificial intelligence (AI)-heavy S&P 500, which rose a mere 0.67 percent as the Magnificent Seven and previously broader technology sectors each fell nearly 6 percent. However, the equal-weight S&P, which removes the concentration bias of AI and technology stocks, rose 7 percent as over 66 percent of the 500 stocks in the roster beat the index. International developed and emerging-market stocks continued their strong 2025 run, rising 10 and 15 percent, respectively. Investors were repositioning for a broader economy and broader earnings growth across corporate America given lower interest rates. That story changed abruptly on February 28, when the Middle East conflict ignited and interest rates began rising once again on the back of the potential for higher energy prices. This led to higher inflation, prompting the Fed to employ a “wait-and-see” approach when it comes to interest rates.

The two-year Treasury rose sharply to a high of 4.12 percent, with the 10-year pushing to a recent high of 4.66 percent. While stocks initially pulled back, they bottomed on March 30 with the announcement of a potential ceasefire. However, equity markets once again narrowed as investors positioned for a probability that higher rates would once again pressure the interest rate-sensitive parts of the U.S. economy. As a result, the markets narrowed to refocus on the AI theme, which has been largely unaffected by the performance of the overall economy over the past few years. From February 28 to June 2, 2026, the S&P 500 climbed 10.9 percent, making U.S. Large-Cap stocks one of the top-performing asset classes. This gain was largely driven by the technology sector, which surged 35 percent. However, performance was much narrower than it appears. The equal-weight S&P 500 rose just 2.9 percent, and only 24 percent of companies outperformed the index. Smaller companies lagged behind Large Caps, with Small-Cap stocks rising 7.7 percent and Mid-Cap stocks gaining 5.4 percent.

Read more: AI Is a Secular Growth Unicorn

This narrative has played out on various occasions over the past years, with the key dividing line being the impact interest rates have had on various segments of the U.S. economy. As rates have pushed lower, the market has broadened to include more economically sensitive segments as investors position for a broader economy, which will in turn result in broader earnings growth. When interest rates have risen or stayed high, investors have tended to focus on a small group of companies that have benefited from heavy spending on AI over the past two years. Many companies have treated AI as a “winner-takes-all” opportunity and continued to invest aggressively. In reality, this AI spending has not been very sensitive to interest rates because companies have largely funded it using their own free cash flow rather than relying on borrowed money.

We believe this narrative is in the process of shifting. No longer is cash flow the primary source of capital for the AI buildout: rather, companies now need ever-increasing levels of capital—both in terms of debt and equity—to continue bringing AI to life. From Alphabet (GOOG) to Amazon (AMZN) to Meta (META) to even currently free cash flow positive Nvidia (NVDA), companies are looking for capital to build data centers and other infrastructure for AI’s rapid expansion. We believe this notable shift makes AI more interest rate and economically sensitive.

This is where the market narrative seems to have shifted once again in the opening week of June, on the back of an announcement of a potential breakthrough with Iran that would open the Strait of Hormuz and cause oil prices to peak. Ironically, the week also saw stronger labor market data that brought with it the prospects of higher interest rates on the back of a Fed that may have to shift its focus to fighting inflation given that it has been missing that mandate for over five years. Interestingly, the stocks that were most negatively impacted by higher rates and the potential for the Fed to raise interest rates were AI and technology related, marking a reversal from recent trends. It is worth noting that even with the opening of the Strait under the recently enacted deal between the U.S. and Iran, the market remains priced for the next Fed move to be a hike and not a rate cut, which could potentially weigh on future economic growth. This may seem surprising, but it highlights where the market is most vulnerable to any potential economic hiccup. Much of the promise around AI depends on companies continuing to deliver strong earnings growth—even though many of those expected gains are still years away.

A resilient but narrowing U.S. economy

We strongly believe what is happening in the economy shows up in financial markets. This is where the bifurcated market of the past few years has been directly tied to the bifurcated economy. While economic growth has been resilient over the past years, it has increasingly narrowed and relied heavily upon the AI boom as the primary driver. Consider that in Q4 2025, two parts of the U.S. economy most tied to AI spending—information processing equipment and intellectual property—accounted for 0.96 percentage points of the country’s 0.6 percent overall growth, meaning they drove all of the growth and more. This continued into Q1 2026, with these two segments contributing 1.5 percentage points of the 1.6 percent overall economic growth.

These trends highlight how narrow economic growth has been. Over the past two quarters, overall growth has slowed, averaging just 1.1 percent. This does not mean other parts of the economy are not growing, but when everything is added together, two sectors—which make up about 10 percent of total economic output—are doing most of the heavy lifting.

More concerning is the slowdown in consumer spending, which is the largest component of U.S. economic output. Growth in consumer spending has slowed to 1.9 percent and 1.4 percent over the past two quarters. Aside from Q1 2025, when spending rose just 0.6 percent and overall economic growth was negative, this is the slowest pace of spending growth since Q4 2022.

Also worrisome is the fact that this spending is increasingly coming from a smaller group of higher-income consumers. Some of their resilience appears to be tied to a “wealth effect,” meaning gains in equity markets are helping support their spending.

Challenging consumer fundamentals

The good news is that the labor market has recently stabilized after spending late 2024 and much of 2025 in a slowing and narrowing trend. In 2025 the pace of job growth stalled to an average of 10,000 jobs added overall, with the private sector faring better at a pace of 25,000 per month. However, all private payroll growth resided in the health care and social assistance segments of the U.S. economy, which saw an increase of 57,000 jobs added per month. This noncyclical segment reflects an aging population rather than a bustling economy that overall represents a mere 17 percent of total private-sector employment. When we look at the entirety of the 180 industries represented in the job report, the reality is that in nine of the 12 months, fewer than half of the industries were hiring, a condition that (besides a similar period from May 2024 to October 2024) has, at least historically, coincided with economic weakness.

Also encouragingly, 2026 has witnessed dramatic labor market healing with an average monthly job gain of 114,000 and private payrolls reaching a similarly strong 106,000. Importantly, the first five months of 2026 saw more than half of the industries hiring, with health care and social assistance remaining strong but contributing only 55,000 per month. With overall layoffs remaining low, consumer spending has been supported by the continued employment of Americans.

The bad news is that consumer wage growth has slowed, while inflation has risen sharply in the aftermath of the Middle East conflict. Contemplate that overall wages and salaries have risen 3.5 percent over the past year, while inflation is now clocking in at 4.2 percent on the Consumer Price Index (CPI) through May, with Personal Consumption Expenditure (PCE) inflation showing a 3.8 percent year-over-year increase through April. This has pushed real wage gains into negative territory, with real disposable after-tax personal income clocking in at negative levels for each of the past three months. That has pushed it to a -1.1 percent year-over-year loss in purchasing power. While this data is volatile, this is a condition that does not happen often, highlighting consumers’ increasing reliance on spending their savings. The April Personal Income and Outlays report from the U.S. Bureau of Economic Analysis (BEA) revealed that the consumer savings rate fell to 2.6 percent that month, down sharply from the 5.5 percent level the year prior and the lowest level since June 2022 at the tail end of the COVID-19 pandemic. Before that, savings rates were at similarly low levels during 2005 to early 2008, a period when the U.S. economy was heading toward weaker growth.

This growing risk is further compounded by the reality that a narrowing cohort of consumers is driving most of the spending—and that spending is increasingly coming from people who have money invested in the stock market rather than those who do not.

This has been reflected in consumer sentiment gauges such as the University of Michigan Survey of Consumers, in which since 2023, higher‑wealth households—those most exposed to equity gains—have reported markedly better conditions than middle‑ and lower‑income consumers, who continue to feel the pinch of higher prices.

A recent analysis from the New York Fed’s Liberty Street Economics blog reaches a similar conclusion: Prior to 2023, little difference existed among spending by households in different income cohorts. Since then, however, spending growth has been disproportionately driven by higher‑income households, with discretionary and luxury purchases driving consumption, while spending on necessities has softened. Wage differences explain part of the gap, but only since 2025, as the years before often saw similar wage gains among cohorts. The study points to two reasons that have driven the growing bifurcation:

- Since late 2022, lower-income households have consistently experienced higher inflation than middle- and higher-income households, which has in turn impacted their spending.

- Since 2023, real net worth has also become bifurcated, with higher-income groups seeing faster growth in new worth driven by large increases in financial assets, which also explains their increase in spending relative to lower-income groups.

The consumer remains incredibly important to the overall health of the U.S. economy, and while spending remains positive, rising inflation against slower wage growth raises concerns about the durability of the consumer.

Sticky inflation and a divided fed under new leadership

This conversation about the consumer paints a picture of the growing question about the Fed’s next move under its new chair, Kevin Warsh. The reality remains that inflation has not been at the Fed’s 2 percent target since February 2021 and is currently moving higher, not lower. The Fed’s preferred measure, Core PCE inflation, resides at 3.3 percent, a level it first touched back in November 2023.

Despite this reality, the Fed has cut interest rates by 1.75 percent over the past two years. This is where the Fed has made a call to prioritize its employment mandate over its price stability mandate. In short, the weakness in the labor market has allowed the Fed to cut rates over the prior few years, even as inflation has remained sticky. Therein lies the current concern given that the labor market appears to be strengthening: Does the Fed now have to focus more on the inflation mandate given that it is the remaining problem?

Warsh recently presided over his first Fed meeting in June, which surprised markets given its hawkish tone. At this meeting, the Fed committed to unambiguously and unanimously returning inflation to its 2 percent target, with Chair Warsh spending most of the press conference pledging to fix the problem of not having hit their target for over five years. While the dot plot showed nine of 18 members expect to hike rates at least once in 2026, the reality is Chair Warsh did not supply a dot. There was also no rate hike, and the committee remains divided with many of the “tough” questions to be answered by five task forces that, hopefully, will wrap up by year-end 2026. Despite the headlines, the results in markets only slightly adjusted expectations for how many rate hikes will be needed for the Fed to pull inflation lower. Before the meeting, one hike was priced in by early 2027, with that hike being pulled forward to the October 2026 meeting, with a second hike now fully priced by March 2027.

We believe that inflation remains a risk. The Fed is likely to continue to point to the “transitory” impacts of the energy price spikes resulting from the Middle East conflict, but the reality is that inflation appears to be leaking into the services sector. Core services ex shelter in both the Consumer Price and Personal Consumption Expenditures indexes remain stuck near 3.5 percent on a year-over-year basis. Additionally, the prices paid component of the Institute for Supply Management services index has pushed back toward levels it last resided at in August 2022, when inflation was elevated. The May National Federation of Independent Business small business optimism index saw a net 36 percent of respondents raising selling prices, which is the highest level since March 2023, while 34 percent plan to raise prices in the next three months, the highest level since July 2022.

While Chair Warsh and the Fed will likely highlight the possibility that AI could help lower inflation over time, inflation remains stubbornly high today. In fact, current bottlenecks related to AI may be adding to inflation, and the longer inflation stays elevated, the greater the risk that it becomes embedded in the broader economy. To be clear, this is not yet the case but is worth contemplating as one potential scenario for future economic outcomes.

Portfolio positioning

Our view after COVID was that inflation would come down—even after it rose further following the start of the Russia-Ukraine war. That is why we stayed optimistic in 2022 and 2023, even as market concerns grew. However, we believed that the last mile of pulling inflation back to the Fed’s 2 percent target would prove far more difficult than the market was pricing in. We stated our belief that there was a higher probability than what was priced in markets that the Fed would have to kill inflation the old-fashioned way, holding rates too high or having to push them higher, which at least historically has eventually caused economic contractions. While this theory has proved correct, the reality is that the Fed has chosen not to drive inflation lower but rather focus on the labor mandate. At the same time, strong economic support from AI-related investment, along with continued high levels of bipartisan government spending, has helped sustain both the economy and markets. The result has been a split economy—strong in some areas and weaker in others—but one that is still growing overall.

The reality remains that the Fed continues to face difficult decisions regarding monetary policy. Do they raise rates, or do they continue to hold and hope and risk inflation becoming embedded in the U.S economy? Does its 2 percent target shift to 3 percent? What impact does AI have on the economy through the labor market and inflation? While we believe both are likely positive longer term, the reality may be more nuanced in the nearer term, with AI likely causing layoffs and potentially creating inflationary pressure given the bottlenecks it is currently creating. Does the current level of spending on AI continue, and are companies willing to pay the price of higher productivity? And, finally, what happens with tariffs moving forward?

This is where we continue to advocate for diversification and encourage investors not to place all of their eggs in the AI thematic basket. At least historically, leadership has shifted, and investing based upon one theme has eventually subjected individuals to increase risks or large downside as winners shift and losers emerge. The good news is that AI benefits have continued to push through the value chain needed to bring it to life. From chips to hyperscalers to memory providers to AI data centers and servers, leadership continues to evolve.

We believe the benefits of AI will continue to broaden throughout the wider economy as more companies use AI to boost employee productivity and profitability. In fact, this may already be happening. The Ramp AI Index, which tracks how quickly companies are adopting AI products and services, has risen sharply from 23 percent at the start of 2025 to nearly 51 percent by April 2026. This echoes the dot-com era, during which (similar to today) the benefits of the technology du jour began to accrue throughout the wider U.S. economy, helping broaden markets in the process.

A common argument today is that rising stock prices are backed by real earnings growth, especially for companies benefiting from AI. That’s partly true—but there are several important caveats. First, there is still meaningful uncertainty around how sustainable this AI-driven earnings growth will be. In many cases, current growth is being supported by heavy capital spending to build out AI infrastructure, and those investments are still outpacing the actual revenue being generated. The key questions are whether that dynamic can continue and for how long.

It’s also important to remember that stock prices reflect discounted future cash flows. In other words, much of a company’s current valuation depends on expectations for earnings many years into the future. That raises questions about how reliable those expectations are. For example, will memory chip prices stay elevated? Companies like Micron Technology (MU) have seen strong stock performance driven by intense demand for AI infrastructure. But terms like “insatiable demand” should give investors pause. In a competitive, capitalistic system, high profits tend to attract new entrants, which can eventually increase supply and put pressure on prices. At the same time, the technology itself will continue to evolve and improve.

Second, there are some similarities to past speculative periods, when companies were valued more on their future potential than their current earnings capabilities. Take struggling shoe company Allbirds, which was able to reposition itself around AI and saw its stock jump, buying high-performance GPUs and selling computing power to companies that need AI processing (often called “GPU-as-a-service”). Similarly, Ford’s (F) stock rose from 11 to 17 percent largely on the possibility that it could shift part of its business to supplying power for AI data centers—an opportunity that may or may not generate meaningful earnings.

Finally, broader market behavior also reflects rising speculation. An index of unprofitable tech companies created by Goldman Sachs has surged 185 percent since its low in April 2025. However, it is still 28 percent below its February 2021 peak, which came after a 427 percent run-up from its COVID-era low in March 2020. In between, it fell 78 percent—a sharp reminder that speculative investments often experience both significant gains and steep declines.

Stay diversified, stay invested, and speculate in moderation.

Section 02: Current Positioning

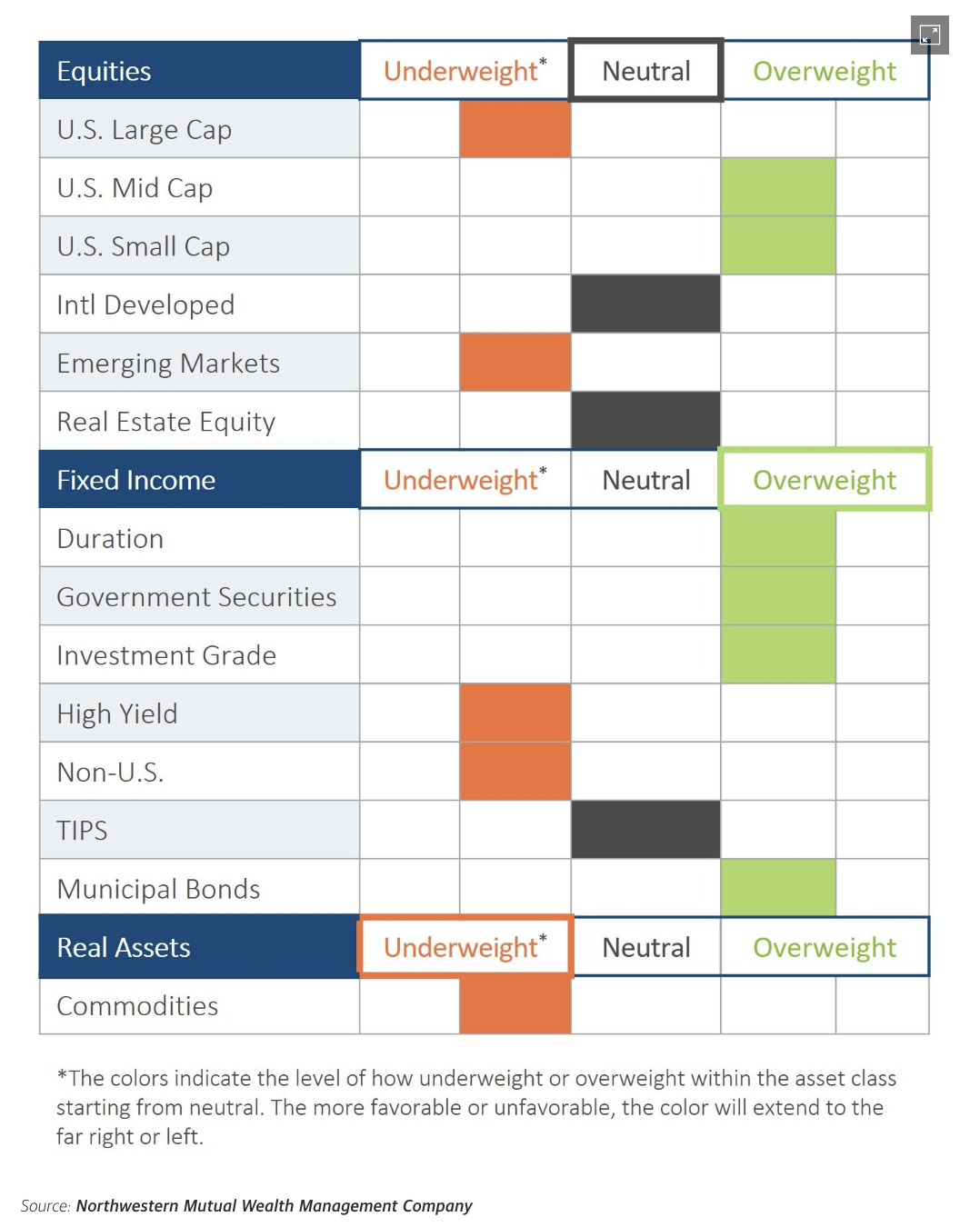

We remain positioned for a broadening, which has already begun to occur in 2026 despite the volatility we have described. Our diversified basket of U.S. and global equities, as well as real estate and commodities, is outperforming the S&P 500. This follows similar outperformance in 2025, largely driven by the strong performance of international equities, while U.S. markets remained heavily concentrated. Year to date, U.S. markets have broadened in 2026, with Mid and Small Caps and the equal-weight S&P outperforming the cap-weighted S&P 500, in which 10 companies represent nearly 40 percent of the index.

We believe this trend will continue into the future given the current relatively attractive valuations in Small- and Mid-Cap stocks coupled with our economic and market outlook. We maintain our overweight to these areas of the U.S. markets while slightly underweight the S&P 500 index and skewing our positioning away from the concentration risk inherent in that index. We continue to believe this current backdrop is reminiscent of the late 1990s economy, which was a later-cycle economy that narrowed but was likely held afloat by the dot-com frenzy and secular focused internet spending, similar to today’s AI-driven advance.

Much like then, U.S. Small- and Mid-Cap stocks have, until this year, underperformed their Large-Cap peers and as a result trade at similar valuation discounts to their Large-Cap peers as they did in late 1999. Even after the past seven years of U.S. Large-Cap outperformance, U.S. Mid- and Small-Cap stocks have returned 9.6 and 9.4 percent annually over the past 26 years compared to just 8.1 percent for their Large-Cap peers listed on the S&P 500. Valuation matters to intermediate- to longer-term investors. We expect a similar repeat in the years ahead. While we see opportunities moving forward, we remain neutral on international developed equities with an underweight to emerging markets.

While these positions have not changed, we are tweaking our portfolios to reflect a greater desire for diversification and a reality that inflation embers may not be snuffed out anytime soon. Given this backdrop, we have decided to add to our Real Estate Investment Trust (REIT) exposure and return it to a neutral allocation after being slightly underweight in the asset class for most of the recent past, culminating with an exposure that was one-fourth of our target in November 2019. While we narrowed that underweight exposure in 2021, this will be our first neutral allocation in 10 years. Since our underweight in 2016, REITs have provided the lowest return of our equity/commodities asset classes while returning more than fixed income.

For much of the past 10 years, we viewed REITs as an expensive asset class that had become that way as investors searched for income-producing asset class alternatives in a near-zero interest rate environment. It was also an asset class highly impacted by the realities of COVID and the spike in interest rates after 2021. Today, this is an asset class that provides a competitive yield with steady cash flow growth, touting relatively cheap valuations and lower correlation to other equity asset classes as well as near-zero correlation to fixed income. Most importantly, if inflation pressures rise, this is an asset class that we believe has the ability to raise rents given low construction starts over the past four years.

The source of the funds is fixed income, which we believe retains attractive yields but with the risk of potentially rising inflation. Overall, we retain a slight overweight to fixed income and a neutral allocation to equities overall with a slight underweight to commodities. The overarching focus is on relative valuation, market broadening, and risk management through diversification. We reiterate our opinion that much as in the last year and a half, diversification is not only a risk management tool but also a way to return enhancement pushing forward.

Section 03: Equities

U.S. Large Cap

The S&P 500 has demonstrated remarkable fundamental resilience through early 2026, transitioning from a period of valuation-driven gains in recent years to a regime where robust earnings growth serves as the primary performance engine. While the index experienced a brief 9 percent pullback in the first quarter due to geopolitical uncertainty and higher oil prices, it has since rebounded to new record highs, reaching over 7,500 in early June. This follows a powerful 2025 campaign, during which the index delivered a total return of 17.9 percent, a rare third consecutive year of double-digit gains. Current momentum is supported by a “rolling recovery” characterized by broadening earnings participation, with a Q1 2026 earnings surprise for the median stock, reaching 6 percent—the strongest level in four years.

The primary driver of this performance is an accelerating capital expenditure cycle centered on AI, which is beginning to yield direct productivity gains and support record-high profit margins. Realized last 12 months earnings before interest and taxes margins of 18.8 percent are projected to reach 20 percent by the end of 2026, aided by “run it lean” corporate efficiency and improved pricing power. While the Magnificent Seven continue to lead with expected 34 percent earnings growth in 2026, the remaining 493 stocks are seeing meaningful upward revisions, with forecasts for that group rising to 13 percent. This broadening strength is further underpinned by a resilient U.S. macro environment, supported by high levels of consumer and corporate fiscal stimulus.

Despite this fundamental strength, valuation remains a headwind consideration, as the S&P 500’s forward price-to-earnings (P/E) ratio of 21x sits well above its 10-year average of 18.7x. Market concentration also remains at historic extremes, with the top 10 stocks accounting for over 40 percent of the index’s total market capitalization, surpassing the peaks seen during the dot-com era. With 2026 earnings per share (EPS) growth estimates recently raised to 26 percent, the index appears positioned to grow into these elevated multiples as long as the AI-driven productivity thesis remains intact. We continue to emphasize diversification in this environment of elevated innovation and productivity, and the S&P 500’s high concentration and valuation levels are risks that we feel require proactive risk management. We remain slightly underweight.

U.S. Mid Cap

The S&P 400 MidCap index has emerged as a focal point for investors in early 2026, transitioning into a period of robust fundamental recovery and significant improvement relative to its 2025 results. Year to date as of mid-June 2026, the index has advanced nearly 16 percent, a sharp acceleration compared to the modest 5.9 percent return seen in the previous year. This performance is underpinned by a rolling recovery in earnings, with Q1 2026 year-over-year growth reaching 14 percent, a substantial rebound from the stagnant growth levels observed throughout 2025. Investors increasingly view the Mid-Cap segment as a “sweet spot” for capital allocation, as these firms are capturing the same AI-driven capital expenditure tailwinds as Large Caps but often with greater operational agility. Current forecasts project S&P 400 earnings to grow by 21.5 percent for the full year 2026, supported by resilient U.S. gross domestic product (GDP) growth and a stabilizing labor market. The fundamental engine driving this acceleration is a broadening of the capital expenditure cycle, which is moving beyond mega-cap technology and into the broader “S&P 493” and Mid-Cap universe.

From a valuation perspective, the S&P 400 remains highly attractive compared to Large-Cap benchmarks and reasonable versus its own historical norms. While the S&P 500 continues to trade at a premium at 21x forward earnings, the S&P 400 is priced at 16.7x, effectively in line with its 20-year average of 16.5x. Historically, periods when Mid Caps trade at such significant discounts to Large Caps while simultaneously delivering double-digit earnings growth have preceded multiyear cycles of outperformance. As investors look to rotate away from record-high market concentration in mega-cap tech, the S&P 400’s combination of reasonable valuations and accelerating productivity makes it an attractive vehicle for capturing the next phase of the domestic economic expansion as companies move to commercialize AI driven efficiencies. We remain overweight.

U.S. Small Caps

The S&P 600 Small Cap index has reached a fundamental inflection point, moving from a period of earning estimate downgrades and stagnant growth in 2023 and 2024 toward a robust earnings recovery in early 2026. While Small-Cap EPS estimates for 2024 and 2025 declined by 8 percent and 6 percent, respectively, due to tight monetary policy, forward EPS growth has recently accelerated to 23 percent. This turnaround is driven by broadening participation in the AI capital expenditure cycle, particularly in the capital goods and semiconductor sectors, as well as a pivot toward productivity-driven margin expansion. S&P 600 Small Caps demonstrated exceptional resilience, posting an aggregate EPS beat rate of 80.3 percent in Q1 2026 as companies leverage operational discipline and AI to offset cyclical headwinds.

Despite this fundamental strength, the S&P 600 continues to trade at a significant discount compared to its Large-Cap peers and its own 30-year historical norms. While the S&P 500 currently trades at forward P/E multiples in the low-to-mid 20s—well above its 10-year average—the S&P 600 is priced in the mid-teens. This valuation gap has reached extremes seen only during the dot-com bubble of 1999–2000 and the market trough of 2002, with relative valuations falling to 74.4 percent of their long-term average by late 2025. This wide divergence demonstrates a longer-term opportunity in diversified portfolios, as Small-Cap valuations are currently near a two-standard-deviation discount relative to U.S. Large Caps.

The eventual closing of this valuation gap is somewhat tied to Fed policy and domestic economic growth expectations. Small caps have historically been sensitive to interest rate expectations, typically outperforming when market forecasts for rate cuts increase. This year began with these specific monetary tailwinds in place only to sharply reverse as oil prices surged following the commencement of the Iran conflict. Higher oil prices have translated into higher near-term inflation conditions, which ultimately have pushed out any expectation for interest rate cuts from the Fed in 2026. While this change has acted as a headwind to sentiment in recent months, U.S. Small Caps have still delivered strong absolute and relative outperformance this year as earnings growth continues to be strong, appreciating over 20 percent year to date as of this writing. We remain overweight on the attractive combination of valuation and improving fundamentals while also appreciating the diversification benefits of this asset class to the concentrated reality of U.S. Large Caps.

International developed markets

International developed economies enter the second half of 2026 facing a challenging environment characterized by subdued growth, persistent inflation—partially reignited by disruptions to Middle East energy distribution—and divergent monetary policy paths. These economies are bearing the brunt of higher energy costs, trade fragmentation, and geopolitical uncertainty.

Eurozone growth forecasts have been cut substantially since the start of the year, with real GDP year-over-year growth now expected to be 0.8 percent in 2026 vs. an estimate of 1.2 percent to start the year. This 33 percent reduction in growth expectations is largely driven by anticipated declines in economic activity due to higher energy prices. The fiscal spending tailwind seen in 2025 is now being offset by these elevated costs. When gauging economic activity by looking at the S&P Global Eurozone Composite Purchasing Managers' Index (PMI), after remaining in expansion territory throughout 2025 (a reading above 50), in April the indicator dipped into contraction (below 50) for the first time since December 2024, with the latest reading at 48.5 for May. On the inflation front, current headline year-over-year inflation of 3.2 percent in May sits well above the European Central Bank’s (ECB) target of 2 percent. While much of this increase is energy driven, the ECB raised deposit rates by 0.25 percent at their June meeting, with markets still expecting another rate hike by year-end despite the recent pullback in energy prices. This less favorable mix of slowing growth and rising inflation has increased stagflation risks, weighing on equity market performance. Eurozone equities have delivered mid-single-digit returns year to date, lagging most major markets.

In Japan, 2026 real GDP year-over-year growth is projected at just 0.7 percent, according to the International Monetary Fund. While tailwinds such as improving household income and rising private consumption remain in place, Japan is highly exposed to the economic implications of the Iran conflict and potential disruption in the Strait of Hormuz, given that it imports approximately 95 percent of its seaborne crude from the Middle East. Core CPI (excluding fresh food) was 1.4 percent in May. Inflation has been contained in part through government fuel subsidies. However, concerns over fiscal support measures and deteriorating fundamentals recently pushed the 10-year Japanese government bond yield up to near 2.8 percent, its highest level since October 1996.

This has also contributed to the yen’s depreciation to around 161 yen per U.S. dollar, increasing the risk of a cost-push inflation scenario, where a weaker currency raises the price of fuel, food, and raw materials. This dynamic is evident in wholesale inflation, which rose to a three-year high of 4.9 percent year over year in April. Japan has even intervened in the currency markets to cut off continued depreciation past the 160 yen per dollar level, which is thought to be an intervention threshold level. These pressures prompted the Bank of Japan to raise rates in June to avoid falling behind the curve in fighting inflation. Despite these challenges, Japan has been one of the best-performing developed markets this year. While growth remains modest, equities have benefited from AI-related exposure and corporate governance reforms aimed at improving capital efficiency and shareholder returns. Additionally, after being negative throughout 2025, real wage growth turned positive this year and, if sustained, could support consumer spending.

Looking ahead, the second half of 2026 will be shaped primarily by the trajectory of energy prices, central bank responses, and the duration of Middle East disruptions. While the length of the conflict remains highly uncertain, a reopening of the Strait of Hormuz and normalization in energy prices would likely restore key tailwinds for international developed equities. Valuations remain attractive relative to U.S. Large-Cap equities. The MSCI EAFE Index’s 2026 year-end price-to-earnings estimate stands at 16.5x, representing a 25 percent discount to the S&P 500 Index. Earnings-per-share growth is projected at 11 percent in 2026—double-digit growth that has been scarce in recent years. The theme of diversification away from concentrated U.S. Large-Cap exposure has the potential to re-emerge once conflict-driven volatility subsides.

Our long-term view remains positive on the asset class; however, given recent near-term headwinds, we are cautious about increasing exposure. As a result, we remain tactically neutral for now, pending greater clarity in the Middle East and the situation surrounding the Strait of Hormuz.

Emerging markets

Emerging-market equities have rebounded since lows in late March, with the MSCI Emerging Markets index now up nearly 30 percent year to date after rising 33 percent in 2025. Emerging markets’ strong advance recently has been a result of an improved appetite for risk since the March geopolitical sell-off and strong AI and semiconductor exposure in emerging markets, particularly in South Korea and Taiwan. South Korea has gained almost 80 percent since the end of March, and Taiwan is up nearly 50 percent in dollar terms at the time of this writing during the same time period. This has helped attract fresh capital inflows into both equities and local currency bonds.

Key drivers behind emerging-market performance over the last 18 months include currency market dynamics, particularly a softer U.S. dollar throughout 2025, which has eased financing conditions for emerging-markets borrowers, boosted return for dollar-based investors, and encouraged capital reallocation back into emerging markets. Structural drivers, such as AI-related demand and semiconductors, have been powerful tailwinds for export-oriented markets in Asia, lifting corporate earnings. Commodity-exporting economies in Latin America have benefited from sustained demand for metals and agricultural products, adding breadth to the rally beyond technology sectors. Foreign investment inflows have recently returned as investors search for new ways to play the AI story and find more attractively valued equities and add to non-dollar assets. The on-and-off nature of tariffs combined with worries over an ever-increasing U.S. deficit have led to more flows to emerging and international developed markets.

However, this is counterbalanced by ongoing geopolitical risks amid the recent conflict in the Middle East, leading to a sharp spike in the price of oil and natural gas, which has in turn impacted many emerging-market economies. This is due to their large dependence on energy imports, with a large majority of its oil supply relying on transit through the Strait of Hormuz. We also note the continued risk between the U.S. and China on top of ever-increasing levels of Chinese debt, in addition to poor demographics and tariff uncertainty. These risks remain as short- and longer-term challenges for the Chinese economy.

The diverse nature of the emerging-markets asset class has dramatically shifted over the past 20 years, with technology and financials now being the two largest sectors. GDP growth is expected to be higher, with valuations relative to the developed world, which even with this year’s run-up continue to sit at relatively cheap levels. Demographics in some developing economies such as India are very favorable as well. Given this, we believe it is important to have long-term exposure to emerging markets in a well-diversified portfolio. However, given the continued economic risk and various geopolitical risks, we continue to modestly underweight the asset class.

Section 04: Fixed Income

Bond yields have proven volatile in 2026 as investors continue to navigate an ever-shifting geopolitical and macroeconomic backdrop. In the aftermath of the three Fed rate cuts to end 2025, interest rates across the yield curve spent the first months of 2026 pushing lower as investors contemplated the potential for more rate cuts given what appeared to be a weakening labor market. This dynamic was upended by the increased energy prices and inflation fears resulting from the onset of the Middle East conflict that drove yields across the yield curve higher. Additional fuel to the increase in rates was the renewed strengthening of the labor market as we pushed through spring into the early summer monthsand investors began to contemplate whether the Fed might be forced to focus on the inflation mandate given that it was moving further from its 2 percent mandate in the context of a labor market that was strengthening.

Warsh’s first meeting as the Fed chair provided another twist to the overall path of interest rates. With the Fed chair seemingly focused squarely on defeating inflation and fixing their continuous miss on the 2 percent target for the past five years, investors pushed up the probability of future rate hikes. However, interest rates across the yield curve did not rise by like amounts. While the two-year Treasury continued its ascent higher and rose to 4.195 percent, yields further out on the yield curve rose substantially less and sit at lower levels as of this writing. This has pushed the spread between the 10- and two-year Treasurys to 27 bps from 40 bps pre-meeting and its recent high of 73 bps in early February. At least historically, when this spread narrows, it implies that investors are pricing in an increased risk that monetary policy is becoming restrictive enough to threaten economic expansion. Despite this the reality is that the yield curve is not yet inverted and as such bears watching but not action.

The coming months will likely see further rate volatility. While oil prices are pushing lower given that the newly signed U.S.-Iran deal allows for oil to flow through the Strait of Hormuz, the reality is this could prove temporary given that it is not a deal but rather starts another 60-day ceasefire that allows the sides to continue to negotiate. Despite this, investors are optimistic that this will bring inflation down as inflation expectations are faltering. Perhaps, but the reality is that inflation today is more than just energy driven, with services inflation continuing to reside at levels above those consistent with 2 percent inflation. Core PCE inflation (ex-food and energy) reflects the reality that it is not all about energy, as it has pushed higher from a 3 percent year-over-year level pre-conflict to 3.3 percent today. Talk is also not action, and many questions remain as to whether the Fed will follow through with rate hikes that finally eliminate the last mile of inflation that has proven sticky over the past few years. Will the Fed risk overtightening and potentially cause an economic downturn, or will it settle for something less (especially given Chair Warsh’s working groups that promise to answer many of the outstanding questions, albeit not until later this year)?

Given this volatile backdrop we have chosen to trim our fixed income exposure but to retain a slight overweight to the asset class given the risk of over-tightening and our belief that U.S. Treasurys would offer a port in the storm if an economic slowdown were to occur. Likewise, we are slightly trimming our duration but in the context of remaining slightly longer than our benchmark. The proceeds are moving to REITs, an asset class that we believe provides a competitive yield to fixed income, but with the opportunity to grow income if inflation does prove sticky or benefit if inflation falters.

Overall, we remain slightly overweight to fixed income and duration. While we worry about the potential for inflation and the deteriorating U.S. fiscal position, we believe that the real rate of compensation on Treasurys currently compensates investors for this risk.

Duration

With the inflation mandate moving further from the Fed’s 2 percent target and the U.S. central bank’s new chair, Warsh, seemingly committed to deliver on price stability, interest rates and the yield curve have reacted. Any potential rate cuts in 2026 have now been priced out of the market and rate hikes are being priced in.

This is reflected in the shape of the Treasury curve changing dramatically over the past few weeks. While the market narrative has focused on the 30-year bond hovering near 5 percent and the 10-year note yields near 4.5 percent, the real story is the one- to five-year part of the curve. The two-year has moved higher this year, rising by 72 bps (0.72 percent), and the five-year by 53 bps, while the 10-year is higher by 32 bps. While this has flattened the curve over the past few months, the reality is that it remains positively sloped, especially on the front end.

While this movement has impeded total bond market returns year to date, path dependency matters, as higher interest rates create opportunities for increased returns from carry, roll, and reinvestment. This reality presents opportunities for investors to take advantage of the curve shape by focusing on the seven- to 10-year bonds. This increased focus on inflation by the Fed as well as the potential for an end to the Middle East conflict has caused front-end Treasury Inflation Protection break-even inflation rates to fall sharply. When you combine that reality with the rise in nominal Treasury interest rates, real yields have become even more attractive. While we have recently slightly decreased our duration to fund our increased allocation to REITs, we continue to recommend a modest overweight to overall portfolio duration.

Government bonds/TIPS

Not only do we focus on the shape of the nominal Treasury yield curve, but we also believe the shape of the Treasury Inflation-Protected Securities (TIPS) break-even curve provides clues to the market’s outlook for Fed policy. Much of the post-Great Financial Crisis time period saw the Fed use aggressive “forward guidance,” which we believe resulted in a flat TIPS break-even curve given that inflation was not a concern. That changed post-COVID as inflation worries rose, which resulted in a volatile front-end TIPS curve while the 10-year-plus part of the curve was relatively calm. Simply put, while nearer-term inflation concerns have risen and fallen, longer--term inflation concerns have remained low. The longer end, while higher from a break-even standpoint, still tends to be in the mid-2 percent range for future expected inflation. Over the past few weeks, shorter-term break-evens have fallen sharply even while nominal Treasurys have risen. Look no further than the two-year break-even, which has fallen by 1.09 percent since March 20, while the two-year yield has risen by 0.29 percent. The market believes inflation will falter and may in fact already be doing some of the Fed’s work. Currently, we continue to focus on nominal Treasurys over TIPS, but future opportunities may present themselves if the Fed does not follow through on its promises of price stability.

Credit

Credit spreads, both investment grade and high yield, have been steady given that equity markets have captured investor fancy. With the end of Q1 into Q2 being volatile in all markets due to the Middle East conflict, credit spreads have remained tight, as they have kept marching on even while residing at seemingly “richer” levels than history has supported. With equity markets continuing to advance and inflation potentially rolling over, this macro backdrop has supported credit markets. However, any hint of economic weakness would likely provide pressure, as investors would likely need to recalculate the potential default risk. We continue to recommend focusing on the higher end of the credit spectrum given the compensation for potential risk remains small in lower-end credits.

Municipal bonds

Municipal bonds, like most fixed income assets outside of Treasurys, remain richly valued. There has been a consistent and strong bid for municipals for about the past 15 years. Much like credit spreads, on a ratio basis they trade quite richly compared to historical levels. We believe there are a few reasons this condition continues to exist: general concern about higher tax rates in the future given the continued large budget deficits, the increased individual investor access to municipal bonds through the growth of Separately Managed Accounts (SMA) with lower investment minimums, and the lower volatility of the asset class in general relative to taxable fixed income over the past few years. Like everything in fixed income, from a real rates perspective it is attractive to be invested in fixed income for the long term here; just accept spreads tighter than historical measures.

Section 05: Real Assets

We believe real assets play an integral role in building diversified portfolios due to their lower correlation to traditional equities and fixed income. Real assets can provide valuable hedges to unexpected inflation and have a strong sensitivity to changes in real interest rates, important considerations when it comes to constructing resilient portfolios over an intermediate- to long-term period. Both 2021 and 2022 provided a lens into the value of this diversification with the standout performance of commodities in response to rising inflationary pressures and Russia’s invasion of Ukraine. Contemplate that all major asset classes pulled back in 2022, while commodities provided investors with a 16.1 percent return. Once again, the diversification benefits of commodities were on display in early 2026 as the impact of the Middle East conflict pressured both fixed income and equities, while commodities pushed sharply higher. With the recent pullback in oil on the continued Iran ceasefire, commodities have faltered, but both stocks and bonds have picked up the slack and rallied on hopes for lower inflation.

Conversely, the sharp decline in real interest rates from 2010–2012 and generally through the end of 2021 provided a fertile backdrop for the eye-popping performance of REITs. Put simply, sharp changes on the inflation and real interest rate fronts are exceedingly difficult to call correctly from a timing perspective, underlining the rationale for a structural allocation to real assets.

For much of the past 25 years (excluding 2022), many of the risks that have existed in the global economy have been tumbling into a period of deflation. This is where fixed income has previously proven to be an effective hedge against most economic and market downturns. However, both sides of the distribution are seemingly now in play, as inflation has remained elevated over the past years. This is the narrow path that policymakers are attempting to navigate, with heightened risks on each side of the equation. Tariffs, de-globalization, increased geopolitical risks, heightened levels of debt, and questions of Fed independence serve only to increase those risks going forward. Given the heightened level of uncertainties that exist, we believe that real assets play an increasingly important role in hedging market risks.

We continue to recommend the inclusion of real assets and maintain our underweight exposure to commodities. However, we have decided to increase our allocation to REITs given their improving fundamentals and increased diversification benefits. While real yields remain positive and inflation expectations have pulled back, we believe that environment may prove temporary. Improving fundamentals and a shifting macro backdrop are providing an opportunity to return this asset class to neutral. In other words, real assets have spent the past few years repricing to a new interest rate environment and are attractively valued versus their equity market peers.

Real estate

We are increasing our REIT asset class exposure from slightly underweight back to our full policy weight, funded by a corresponding reduction in core fixed income. This adjustment restores strategic neutrality following a prolonged period of underweight REITs while enhancing our portfolio’s diversification, inflation sensitivity, and forward return potential without materially increasing overall risk. Importantly, this is not a tactical “call” based solely on real estate sentiment; rather, it’s a recognition that the conditions that justified the underweight have materially evolved over the past few years, and maintaining a structural under-allocation is no longer warranted.

The committee’s original rationale for underweighting REITs was well founded and ultimately effective. The rapid increase in interest rates from near zero to over 5 percent presented a significant valuation risk for long-duration assets such as REITs, driving cap rate expansion and multiple compression. This manifested in weaker REIT performance relative to other asset classes and a repricing of public real estate valuations in line with higher discount rates. However, this proved to be a cyclical adjustment tied to rate shock, not a fundamental long-term impairment of REIT cash flows or business models. The central question now is whether that repricing has largely run its course, and the evidence suggests that it has.

Looking forward, the risk environment for public REITs has become more transparent. Elevated Treasury yields, interest rate volatility, and commercial real estate refinancing pressures remain, but they are now widely understood and embedded in asset prices. The asymmetric downside associated with incremental rate increases is therefore meaningfully reduced relative to the period when the underweight was first initiated. In parallel, REIT fundamentals have remained resilient: occupancy, net operating income, and funds from operations have generally held steady, while balance sheets reflect more conservative leverage, predominantly fixed-rate financing, and manageable maturity structures. This divergence between stable operating performance and depressed valuations creates a more favorable forward return profile.

From a portfolio construction standpoint, reallocating from fixed income to REITs introduces a more balanced mix of cash flow characteristics. Core fixed income provides stable coupon income but limited growth, whereas REITs offer a combination of current income and embedded growth through rent escalations, leasing dynamics, and property-level pricing power. REITs also provide greater inflation sensitivity and function as a hybrid asset class, combining attributes of both equities and real assets. Importantly, this shift is incremental and does not compromise the role of fixed income as a portfolio stabilizer but instead improves the portfolio’s overall real return potential in a range of economic environments.

The macro regime itself has also shifted in a way that supports reestablishing our REIT policy weighting. Real interest rates have moved from a prolonged period of zero or negative territory to sustained positive levels that are now among the highest seen in many years. Historically, REIT performance has depended less on the absolute level of rates and more on the underlying rate drivers, particularly growth and inflation. In environments where rates are elevated due to healthy economic activity and positive inflation, REITs have often been supported by rising property-level cash flows, rent increases, and improved pricing power. The current environment reflects this dynamic more than the abrupt, policy-driven rate shock that initially drove REIT underperformance. As a result, REITs are well positioned to generate real (inflation-adjusted) income and participate in economic growth even with real rates remaining elevated.

Restoring REIT exposure also improves portfolio diversification. Increasing REITs back to a neutral position reduces reliance on traditional equity drivers, particularly Large-Cap U.S. equities, and pure duration exposure in fixed income while adding a differentiated real asset cash flow stream. Potential risks, including further rate increases, refinancing stress, or continued relative underperformance, are more manageable going forward, as market participants have had adequate time to price these into the broad asset class.

In conclusion, the REIT underweight was an effective and justified response to an extraordinary rate shock. Today, the environment has shifted: Valuations reflect those risks, fundamentals remain intact, and real rates have normalized at positive levels. Restoring REITs to policy weight is a disciplined, forward-looking decision that enhances portfolio balance, improves real return potential, and reduces the risk of remaining underexposed to a repriced and evolving asset class.

Commodities

Commodities have delivered strong year-to-date performance in 2026, primarily driven by the surge in energy prices resulting from the Iran conflict. While energy prices have begun to fall after the recent signing of the U.S.-Iran memorandum of understanding, commodities still have provided a nearly 19 percent return year to date. Even as the oil prices are pulling back, this episode once again highlights why commodity exposure can help diversify portfolios when geopolitical shocks create inflation pressure and disrupt traditional asset-class relationships. While energy markets remain a large driver of returns, the reality is that overall gains have been broad based, with only precious metals providing a slightly negative return year to date. Gold was one of the standout performers in 2025 and continued to lead early in 2026 as investors sought hedges against geopolitical risk and policy uncertainty.

The shift from a precious metals-led rally to a broader commodity advance strengthens the diversification case, since performance has come from multiple macro drivers rather than from a narrow safe-haven trade alone. Outside of energy, the remaining major commodity groups have also posted positive year-to-date returns. Industrial metals have benefited from supply pressures and firmer demand expectations, agriculture has been supported by select crop and biofuel-related trends, and livestock has continued to advance on tight supplies. The result is a more balanced commodity backdrop in which several themes are contributing at once, reinforcing the role of commodities as a source of diversification during periods of inflation, uncertainty, and geopolitical stress.

Looking ahead, commodity returns are likely to remain sensitive to geopolitical developments, energy supply conditions, and the strength of global growth. Year-to-date gains have been strongest in sectors most exposed to supply disruptions, but positive contributions from metals, agriculture, and livestock point to a broader foundation than a single-event rally. If that breadth continues, commodities may offer both return potential and diversification benefits within our portfolios.

Our intermediate- to long-term outlook for commodities remains positive, supported by expectations for persistent inflationary pressures and elevated political uncertainty. In the near term, however, we remain underweight commodities because we prefer asset classes that generate income.

Northwestern Mutual Wealth Management Company (NMWMC) Investment Strategy Committee:

Brent Schutte, CFA®, Wealth Management Company Chief Investment Officer

Matthew Stucky, CFA®, Chief Portfolio Manager, Equities

Michael Helmuth, Chief Portfolio Manager, Fixed Income

David Andrzewski, WMCP®, Vice President, Private Client Services

Nicolas Brown, CFA®, CAIA, Senior Research & Portfolio Analyst, NMWMC Research

Richard Iwanski, CFA®, CAIA, Senior Research & Portfolio Analyst, NMWMC Research

Matthew Wilbur, Senior Director, Advisory Investments

David Humphreys, CFA®, RICP®, Assistant Director, Advisory Investments

Matt Sobocinski, CFA®, Senior Portfolio Manager, Private Client Services

The opinions expressed are those of Northwestern Mutual Wealth Management Company as of the date stated on this material and are subject to change. There is no guarantee that the forecasts made will come to pass. This material does not constitute individual investor advice and is not intended as an endorsement of any specific investment or security. Information and opinions are derived from proprietary and non-proprietary sources.

Northwestern Mutual is the marketing name for The Northwestern Mutual Life Insurance Company (NM), Milwaukee, WI, and its subsidiaries. Investment brokerage services are offered through Northwestern Mutual Investment Services, LLC (NMIS), a subsidiary of NM, broker-dealer, registered investment adviser, and member FINRA and SIPC. Investment advisory and trust services are offered through Northwestern Mutual Wealth Management Company® (NMWMC), Milwaukee, WI, a subsidiary of NM and a federal savings bank. Products and services referenced are offered and sold only by appropriately appointed and licensed entities and financial advisors and professionals. Not all products and services are available in all states. Not all Northwestern Mutual representatives are advisors. Only those representatives with “Advisor” in their title or who otherwise disclose their status as an advisor of NMWMC are credentialed as NMWMC representatives to provide investment advisory services.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. Indexes and/or benchmarks are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance and are not indicative of any specific investment. Diversification and strategic asset allocation do not assure profit or protect against loss.

Although stocks have historically outperformed bonds, they also have historically been more volatile. Investors should carefully consider their ability to invest during volatile periods in the market.

With fixed income securities and bonds, when interest rates rise, bond prices usually fall because an investor may earn a higher yield with another bond. Moreover, the longer the maturity of a bond, the greater the risk. When interest rates are at low levels, there is a risk that a significant rise in interest rates can occur in a short period of time and cause losses to the market value of any bonds that you own. At maturity, the issuer of the bond is obligated to return the principal (original investment) to the investor. High-yield bonds present greater credit risk than bonds of higher quality. Bond investors should carefully consider risks such as interest rate risk, credit risk, liquidity risk, securities lending risk, repurchase and reverse repurchase transaction risk.

Investing in special sectors, such as real estate, can be subject to different and greater risks than more diversified investing and may present more financial and other risks than investing in companies of larger capitalizations and more seasoned companies. Declines in the value of real estate, economic conditions, property taxes, tax laws and interest rates all present potential risks to real estate investments.

Investing in real estate companies entails some of the risks associated with investing in real estate directly, including sensitivity to general and local economic and market conditions, demographic patterns, changes in interest rates and governmental actions.

Investors should be aware of the risks of investments in foreign securities, particularly investments in securities of companies in developing nations. These include the risks of currency fluctuation, of political and economic instability and of less well-developed government supervision and regulation of business and industry practices, as well as differences in accounting standards.

Commodity prices fluctuate more than other asset prices, with the potential for large losses, and may be affected by market events, weather, regulatory or political developments, worldwide competition and economic conditions. Investment can be made directly in physical assets or commodity-linked derivative instruments, such as commodity swap agreements or futures contracts.

Treasury Inflation-Protected Securities (TIPS) are securities indexed to inflation in order to protect investors from the negative effects of inflation.

The U.S. Large Cap asset class is measured by the S&P 500 Index, which is a capitalization-weighted index of 500 stocks. The S&P 500 Index is designed to measure performance of the broad domestic economy through changes in the combined market value of 500 stocks representing all major industries. The gross domestic product (GDP) is the amount of goods and services produced in a year in a country.

The U.S. Mid-Cap asset class is measured by the S&P MidCap 400 Index, which is the most widely used index for mid-sized companies and covers approximately 7 percent of the U.S. equities market.

The U.S. Small Cap asset class is measured by the S&P Small Cap 600 Index, a market value-weighted index that consists of 600 Small-Cap U.S. stocks chosen for market size, liquidity, and industry group representation.

The International Developed Markets asset class is measured by the Morgan Stanley Capital International Europe, Australasia, and Far East (MSCI EAFE) Index, which is composed of all the publicly traded stocks in developed non-U.S. markets. The MSCI EAFE Index consists of the following 22 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the United Kingdom.

The International Emerging Markets asset class is measured by the MSCI Emerging Markets Index, which is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 21 emerging-market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand and Turkey.

The Real Estate asset class is measured by the Dow Jones U.S. Select REIT Index, which intends to measure the performance of publicly traded REITs and REIT-like securities. The index is a subset of the Dow Jones U.S. Select Real Estate Securities Index (RESI), which represents equity real estate investment trusts (REITs), and real estate operating companies (REOCs) traded in the U.S. The indices are designed to serve as proxies for direct real estate investment, in part by excluding companies whose performance may be driven by factors other than the value of real estate.

The Commodities asset class is measured by the Bloomberg Commodity Index (BCOM), formerly the Dow Jones-UBS Commodity Index, which is a highly liquid, diversified and transparent benchmark for the global commodities market. It is calculated on an excess return basis and reflects commodity futures price movements.

CPI inflation examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits