Illiquidity premia and manager skill can play key roles.

Private markets have become integral to modern portfolios, with many investors searching for higher returns and diversification, including from public markets. But recent fund redemptions have reinforced that illiquidity isn’t theoretical, raising questions about the benefits of giving up liquidity. We see several—but investors must understand the trade-offs.

Private Credit: A Case Study in Private Markets

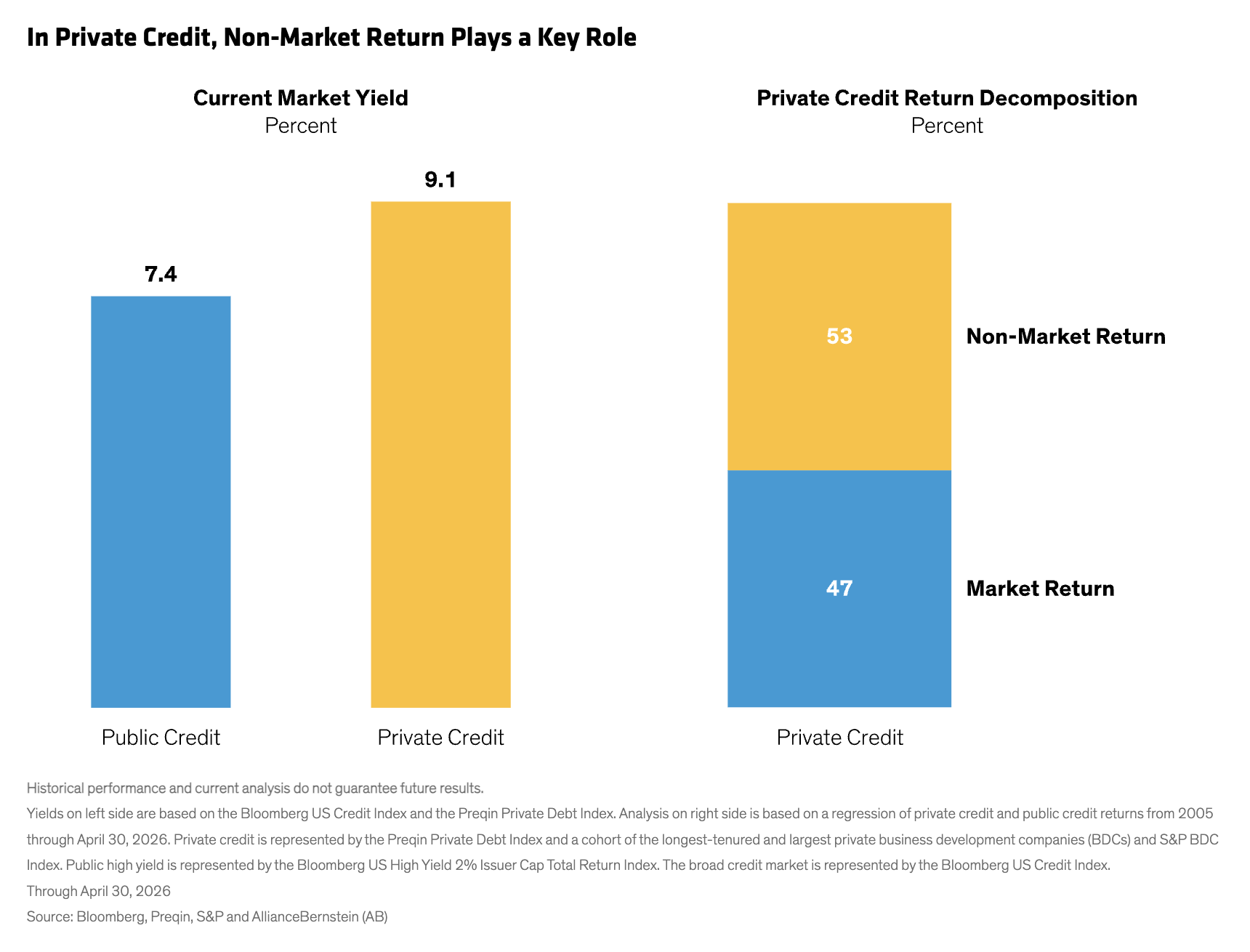

To better understand the trade-offs among liquidity, market exposure and manager-specific returns, we analyzed private credit. We think it’s ideal for this analysis because its underlying economic exposures can be reasonably compared to public credit markets. Private credit also has multiple market structures that let us observe these exposures. They typically have the same underlying economic engine but different liquidity and pricing frameworks.

We used statistical analysis to compare performance patterns, making adjustments because private assets are priced infrequently and often reflect market movements with a delay. The results indicate that private credit moves with broader credit markets but not to the same extent as many public investments. This pattern was consistent across private credit indices as well as non-traded and publicly traded business development companies.

The Private Credit Alpha Equation

So how much market risk are investors really taking in private markets? And how much of the return is driven by alpha or manager skill?

The research suggests that market factors explained less than half (Display) of what drives long-term private credit returns. The rest seemed tied to non-market factors, which could include underwriting quality, manager decisions, applying leverage, sourcing and portfolio construction.

So, it seems that private credit is neither pure alpha nor simply “hidden beta.” Instead, it appears to represent a hybrid structure, with systematic market exposure, illiquidity premia and manager-specific outcomes all playing meaningful roles.

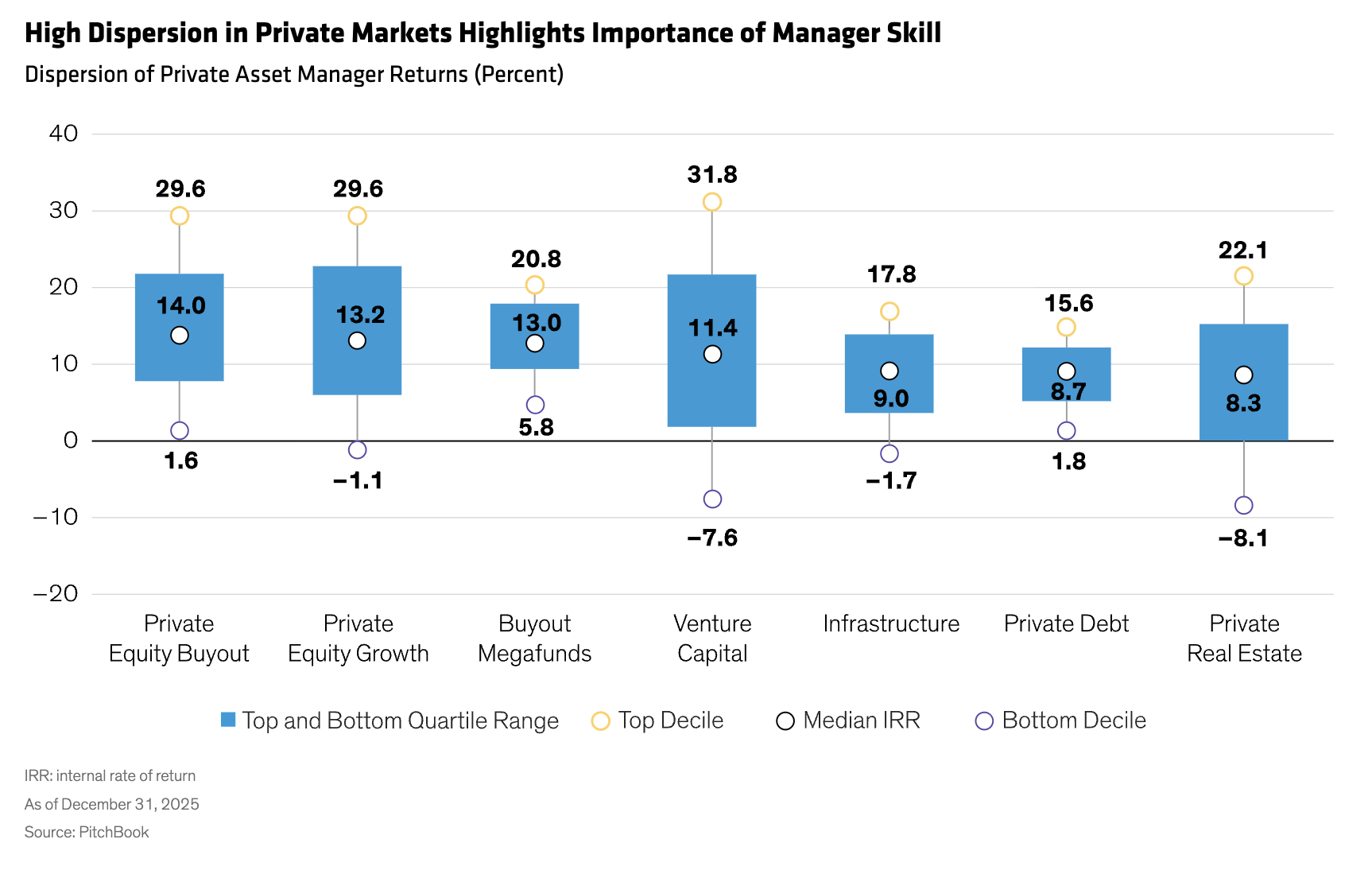

Manager Skill Matters in Outcomes

We also found evidence of a persistent private credit premium above what’s explained by public-market exposure. Some of it likely compensates for illiquidity, but part may also stem from structural and manager-specific advantages including sourcing, underwriting, leverage management, workout capability and portfolio construction.

Overall market conditions can certainly influence outcomes, but our analysis suggests that manager skill is in the driver’s seat in generating alpha. And the role of skill seems magnified in private markets, given the very wide dispersion of manager returns (Display). In public equity and fixed-income categories, the gap between top- and bottom-quartile managers may only be a few percentage points annually.

This distinction suggests to us that private market outcomes depend particularly heavily on manager skill, making manager selection one of the biggest drivers separating strong investment outcomes from weak ones in private market investing.

Creating Complementary Credit Exposures

For investors, we think the implication is clear: public markets offer daily liquidity and remain the most efficient vehicle for broad market exposure. But private markets offer the potential for enhanced returns through illiquidity premia and manager-specific value creation. Of course, these opportunities come with important trade-offs: lower liquidity and greater manager-selection risk.

The takeaway, as we see it, isn’t that private markets are superior to public markets, or the other way around. Rather, it’s that each provides a different mix of risks and rewards.

Investors willing to allocate a portion of their portfolio to less liquid investments and extend their investment time horizons may earn a significant premium by adding private market exposure, but we think choosing managers carefully is an essential part of the process.

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

Brian Resnick is a Director and Senior Investment Strategist for Alternatives.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

More Capital Growth Topics >